PEYUF - Peyto Exploration & Development: Secure Dividend Is A Differentiator

2023-10-20 13:47:43 ET

Summary

- Peyto Exploration & Development is the fifth largest natural gas producer in Canada enjoying a low cost advantage.

- Using a market diversification and hedging strategy, Peyto has sustainably grown and protected its dividend under volatile gas prices.

- With the recent surge in share price, it's better to wait for a pullback before making an entry.

Editor's note: Seeking Alpha is proud to welcome Ideas for Wealth as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Despite the recent uptick in natural gas prices, the significant rise in Peyto's ( PEY:CA ) ( PEYUF ) stock price since July 2023 lows doesn't make it an attractive investment option today. Nevertheless, a sound balance sheet, a high dividend, and exposure to diverse gas markets would make it a prudent investment if the stock price goes back to lands closer to C$11 per share, at which a total return of ~18% is expected.

Business Overview

Peyto Exploration & Development Company, a Canadian oil and gas firm, derives nearly 87% of its production from natural gas, while natural gas liquids account for the remainder. The majority of its reserves are situated in the Alberta Deep Basin, with key assets including Brazeau River (Cardium and Spirit River gas), Greater Sundance (Cardium and Spirit River gas), and Northern Alberta (Deep Basin gas). Over time, Peyto has earned a reputation for being not only one of the most cost-effective producers but also one of the most shareholder-friendly companies in Canada.

Acquisition of Repsol Assets

Peyto recently completed the acquisition of Repsol Canada's assets, involving a payment of C$636 million. This acquisition has significantly boosted Peyto's production, increasing it from approximately 100,000 barrels of oil equivalent per day (boe/d) to 123,000 boe/d. Additionally, the deal has brought in 90 million barrels of proved developed producing ((PDP)) reserves, extending the reserve's life by nearly 11%.

Furthermore, the acquisition included 17 operated gas plants with a total capacity of 1.5 billion cubic feet per day (Bcf/d), of which only 52% is currently being utilized. Peyto sees substantial untapped potential in the acquired lands, particularly in terms of horizontal drilling opportunities, which offers a significant upside in terms of inventory.

As a result of these opportunities, Peyto's management has set an ambitious target to further increase production from the current level of approximately 123,000 boe/d to 160,000 boe/d by the year 2026.

Peyto's Advantages

1. Low cost

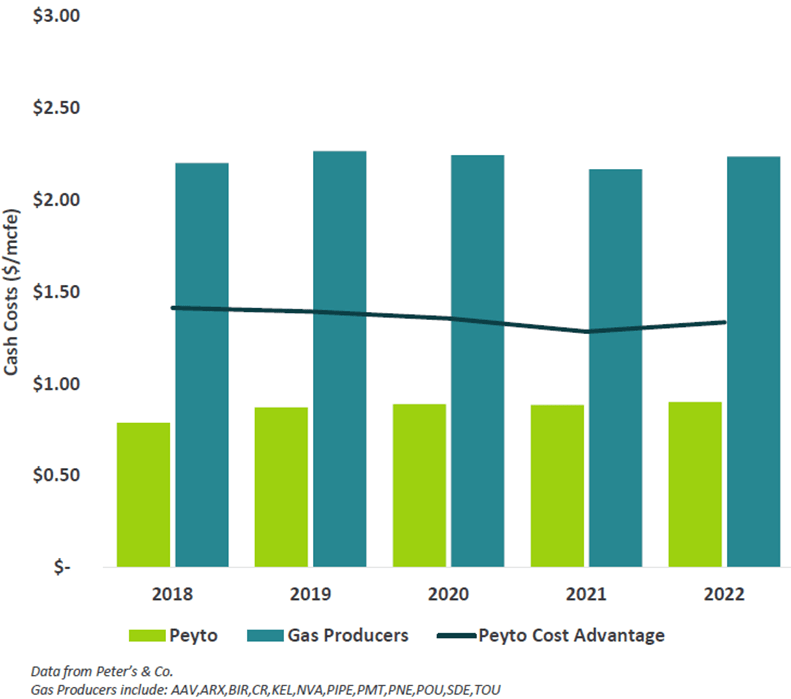

Peyto's approach of owning and managing production plays a crucial role in maintaining its cost efficiency, providing a significant edge over its industry counterparts. This results in a cash cost that is below $1.34/mcfe (million cubic feet equivalent) compared to its gas-weighted peers. Even prior to the Repsol acquisition, Peyto had operational control over 98% of its production, including 12 gas plants that it owned and operated. These gas plants had a processing capacity of nearly 1 billion cubic feet per day (bcf/d), a capacity that has more than doubled since the Repsol transaction.

Peyto's cash costs versus peers (Company Presentation, April 2023)

{kind=link}

2. Dividend powerhouse

Peyto's commitment to shareholder-friendly initiatives has positioned it as one of the leading companies in the oil and gas sector in terms of dividend yield. In contrast to some companies that opt for share buyback programs, Peyto has prioritized returning cash to its shareholders. Presently, the company offers a yield of approximately 10%, which has increased significantly from a dividend of 9 cents per share in 2020 to the current rate of $1.32 per share.

3. Hedging strategy

Over the past five years or so, the AECO gas price, which is relevant to Peyto's operations, has consistently trailed the standard NYMEX gas price. This discrepancy is primarily attributed to the limited export infrastructure available in Western Canada, where Peyto operates. Another contributing factor to this significant price differential is the substantial physical distance between Peyto's assets and the major natural gas markets in the United States. To mitigate the impact of price volatility, Peyto has implemented a hedging strategy. This approach has proven effective in realizing higher prices for its gas production. Consequently, Peyto has outperformed the AECO monthly price in 12 out of the last 17 years. While this strategy provides adequate downside protection, it may also constrain potential gains in the event of a significant increase in natural gas prices. Nevertheless, considering Peyto's high dividend yield, the hedging strategy appears wise as a means of safeguarding the dividend.

4. Diversification strategy

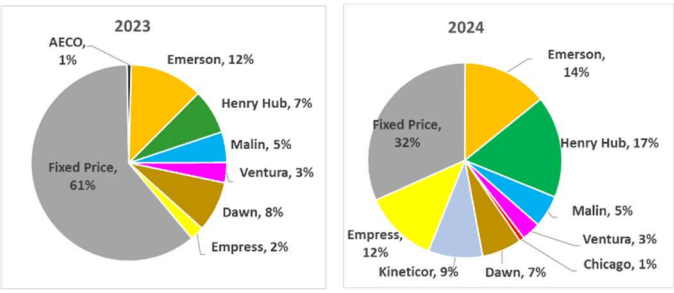

For the last five years or so, AECO gas price has lagged the standard NYMEX gas price in the recent past due to a lack of export markets in Western Canada where Peyto operates. Another reason for the heavy price discount is the large physical distances that exist between Peyto's assets and the major natural gas markets in the United States. To combat this, Peyto announced a gas marketing diversification strategy in 2018, which included steps to gain exposure to both US markets and local Alberta ("AB") markets like power, petrochemical, or other industrial users. The diversification strategy was intended to reduce the risk of dependency on just one market and ultimately drive a higher overall realized price for Peyto's gas. This market diversification approach complemented Peyto's existing hedging policy, which seeks to stabilize gas prices at these various hubs, thereby reducing gas price volatility and ensuring predictability in cash flows.

As the number of LNG facilities being constructed worldwide continues to grow, there is an expectation that gas prices will become more stable and potentially even strengthen. This situation holds the potential for Peyto to benefit, bringing us to the final and potentially a major advantage for Peyto in the future with its gas reserves and processing facilities.

Peyto's gas market exposure (Company report, May 2023)

{kind=link}

5. Gas a cleaner fuel and LNG

As the world rapidly shifts away from coal and oil companies face mounting pressure to curtail crude oil production for the sake of reducing carbon emissions, natural gas has emerged as the pivotal "transition" fuel. The growth of LNG facilities globally serves as clear evidence of this trend, and Peyto's leadership acknowledges (as can be seen from the CEO's views reproduced below) and understands its significance.

Ultimately, we believe that natural gas is the fuel of the future. We have a real opportunity to displace dirtier fuels around the world if we continue to build out our LNG export capacity here in Canada and in the U.S. because nobody does it better than Canadian producers when it comes to responsible low-emissions development. Renewables have a place, but natural gas has proven to be the most reliable energy source, especially in harsher climates, where solar and wind just can't meet demand when you most need it. And we believe Peyto is well equipped to supply that gas as we go forward with our low-cost structure, our low-emissions intensity production, our price risk management and our disciplined approach to shareholder returns". JP Lachance, Peyto CEO (Q1'23 earnings call)

Therefore, Peyto is in a favorable position to locate customers and markets for its gas production, and it also stands to potentially gain from an increased realized gas price as LNG demand expands. It's also worth noting Peyto's significant achievement in reducing carbon emissions too. Since 2013, the company has lowered its emission intensity by 28% while concurrently decreasing land and water usage.

Balance Sheet

Peyto's balance sheet has remained solid due to its strategy of diversifying its product markets and hedging. Before the Repsol acquisition, the company had been actively reducing its debt, bringing it down to $0.7 billion from $1.17 billion in 2020. After the Repsol deal, the debt is now $1.2 billion but the management has re-iterated its focus on sustaining dividend and debt reduction with a Debt/EBITDA target of below 1.0x by year-end 2025. My base case scenario suggests that this debt target should be achievable with a cumulative free cash flow (net of dividends) of $0.7B by 2025.

Valuation

An oil and gas company is typically evaluated based on factors like reserves/production growth, and its shareholder policies such as cash returns, return on capital employed (ROCE), and return on equity ((ROE)). Here are some key insights into these metrics, highlighting Peyto's exceptional performance:

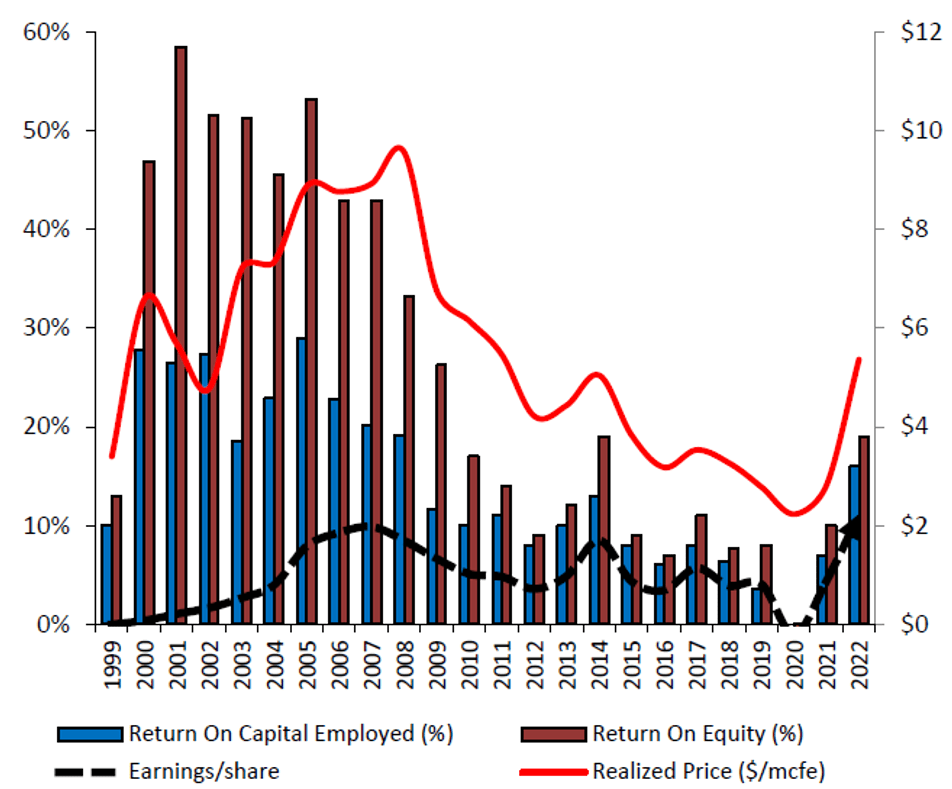

Reserves Growth: Over the past two decades, Peyto has successfully discovered 8 trillion cubic feet equivalent (TCFe) of natural gas reserves, with approximately 90% of its land holdings still untapped, offering substantial potential for future growth.

Shareholder returns: Despite facing challenging commodity price environments, Peyto has not only maintained but also expanded its dividend payouts. Furthermore, the company has consistently delivered impressive financial metrics, with ROE and ROCE figures standing at an impressive 25% and 14%, respectively, from 1999 to the present day.

Peyto's financial metrics (Company presentation, July 2023)

{kind=link}

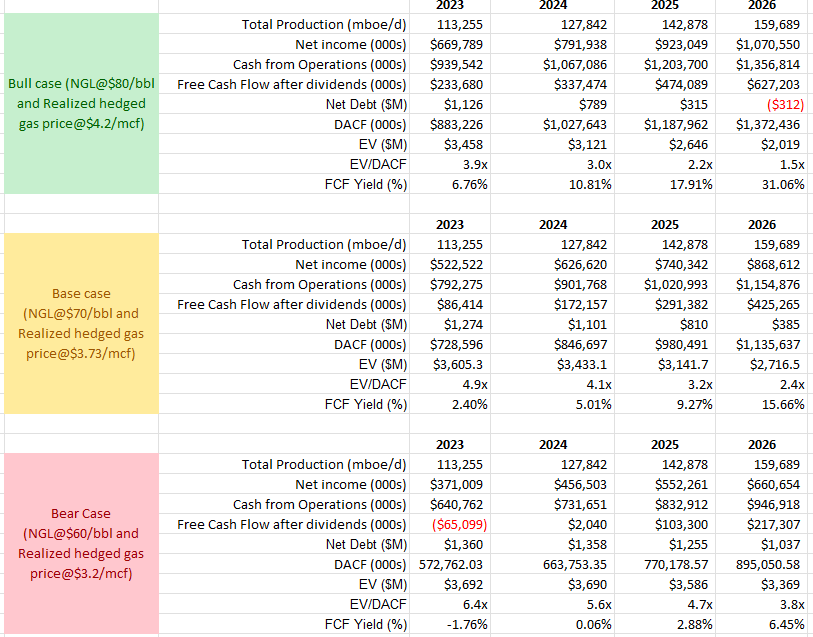

Peyto's dividend yield stands at a handsome ~10%. For a company sporting such a high dividend yield, it's imperative to look at its payout credentials. For the last two years since the dividend was jacked up, the dividend payout ratio has been 26% and 48% respectively and based on consensus estimates, it is expected to stay around ~50% this year. To evaluate Peyto's investment potential today, I conducted a discounted cash flow analysis considering three different price scenarios. The production for the next three years aligns with the management's guidance, aiming for 160,000 barrels of oil equivalent per day (boe/d) by 2026. Currently, Peyto is trading at an EV/DACF multiple of approximately 4.5x, which is in line with its industry peers.

By assigning probabilities of 25% for the bull case, 60% for the base case, and 15% for the bear case, the weighted return, including dividends, amounts to approximately 6% at today's prices. It's worth noting that the dividend remains sustainable in both the bull and base case scenarios, with a reduction in net debt. However, in the bear scenario, free cash flow is not substantial enough to facilitate meaningful debt reduction. In my view, the base case is the one that is likely to play out, hence I have assigned a 60% probability to it.

{kind=link}

Risks

Peyto possesses a reasonably robust financial position, having only recently taken on some debt as a result of the Repsol transaction. While commodity pricing poses a risk to all oil and gas companies, Peyto has been able to achieve market prices above the industry average thanks to its hedging and diversified market strategies. Additionally, Peyto's reserve life index, which was already impressive at nearly 24 years, has further improved following the Repsol acquisition. Cost control is key element that a commodity producer has under its own control, and Peyto's sparkling record in terms of reducing cost is a testament to management's quality. While all the boxes appear checked, one major concern is the dividend payout ratio. With the high dividend yield of ~10%, the payout ratio almost touched 100% last quarter, which could make investors suspicious about the sustainability of the dividend. The yearly payout ratio is around 50% which appears reasonably safe for now and will get lower with higher earnings coming from increased gas production, though this is one thing to keep an eye out for. Another concern would be the dilution of existing shareholders through inorganic growth. Peyto's share count has been increasing off late and with management's focus on dividend sustainability first and debt reduction second, this is another risk for potential investors to partner with a management who is not keen on share buybacks for now.

Final Thoughts

As a result of the recent surge in the share price, Peyto's potential returns at current valuation do not appear particularly attractive when compared to the yield of a 10-year treasury rate. Nonetheless, in the event that the share price hovers around $11 per share or if natural gas prices exhibit a favorable bullish trend without causing substantial shifts in Peyto's share value, this can become an enticing investment opportunity. This prospect is underpinned by Peyto's growing production at industry-leading low costs, strong balance sheet, and its shareholder-friendly approach exemplified by substantial dividend distributions.

For further details see:

Peyto Exploration & Development: Secure Dividend Is A Differentiator