PFO - PFD Vs. FLC: Outlook For Preferred CEFs

2023-05-28 05:23:23 ET

Summary

- We had suggested a trade for these two preferred CEFs from Flaherty and Crumrine.

- We examine where that stands today and update that recommendation.

- A look at the broader macro issues shows why the two are really struggling.

We wrote about Flaherty & Crumrine Preferred Income Fund ( PFD ) and Flaherty & Crumrine Total Return Fund ( FLC ) in late December 2022. While the holiday cheer and pending new year celebrations took priority for most, we thought it was the best time to pay attention to a great opportunity for "free alpha". That "free alpha" required little changes in one's beliefs about investing and only required playing one of the easier mean reversion trends that repeats itself, again and again. Here, we were referring to the relative discount or premium for two funds that made identical twins look dissimilar. Our call, was to sell out of PFD (if you owned it) and buy FLC instead.

What is fascinating is that you get at least one chance every year when the spread compresses to 0% and then reverts back with vengeance. If you sold PFD and bought FLC every time you got a 9% spread and then sold FLC and bought PFD every time you got a 0-1% spread, you would easily add the equivalent of your distributions, every single year. You have one such opportunity again and investors should capitalize on this.

Source: Sell PFD, Buy FLC

How did that work out? It was pretty sweet, with FLC delivering 6.44% of alpha in 5 months, or at an 15% annualized clip.

The key aspect here is not the return but the relative risk. If you switched between virtually identical funds, your relative risk remains unchanged. So making extra, while not increasing risk, is fantastic.

Outlook For Preferred Share CEFs

Throughout this cycle, we have not held any leveraged closed end funds. Our rationale was that it was hard enough to predict the blowback from a normalization of Federal Reserve policy after a decade of easy money. We did not want to compound our difficulties by adding leverage into the mix. Both these funds, like most CEFs, use substantial leverage. Here is PFD shown, which has an effective leverage of 40.3%.

CEF Connect-PFD

This is our own pet peeve, and possibly it does not bother anyone else, but we really hate the way this number is shown. It is calculated as a percentage of total assets, whereas we would prefer that it be shown as a percentage of common assets.

That later number would be 67.5% ($91.10/$134.95). Of course, for comparing between two funds, either number is fine (as long as you use the same one). But our thinking is that total asset percentage tends to mask the relative risk of these funds compared to unleveraged ETFs. Here is the next chart showing iShares Preferred & Income Securities ETF ( PFF ) versus PFD (price only) since late 2020.

That does not look like a 40% increase in losses, does it? It looks a lot worse. Some of PFD's problems came from the stupid premiums that investors ponied up at the start of this period. We identified this in our work (see, A Preferred Fund Valued For Exceptionally Poor Returns). But the bigger problem was the leverage into a downcycle. This is still a problem today for PFD.

Daily panels of U.S. dollar LIBOR rates are scheduled to end after June 30, 2023. Effective on or around February 21, 2023 (the “Transition Date”), the lender will charge an annualized rate of the Secured Overnight Financing Rate (“SOFR”), reset daily, plus 0.90% on the drawn (borrowed) balance. Prior to the Transition Date, the lender charged an annualized rate of one-month LIBOR, reset monthly, plus 0.80% on the drawn balance. The lender’s charges on the undrawn (committed) balance remain unchanged at an annualized rate of 0.65%. For the year ended November 30, 2022, the daily weighted average annualized interest rate on the drawn balance was 2.176% and the average daily loan balance was $90,922,466.

Source: PFD Report

The same can be seen for FLC.

Effective on or around February 21, 2023 (the “Transition Date”), the lender will charge an annualized rate of the Secured Overnight Financing Rate (“SOFR”), reset daily, plus 0.90% on the drawn (borrowed) balance. Prior to the Transition Date, the lender charged an annualized rate of one-month LIBOR, reset monthly, plus 0.80% on the drawn balance. The lender’s charges on the Flaherty & Crumrine Total Return Fund Incorporated on undrawn (committed) balance remain unchanged at an annualized rate of 0.65%. For the year ended November 30, 2022, the daily weighted average annualized interest rate on the drawn balance was 2.176% and the average daily loan balance was $118,500,000.

Source: FLC Report

There are two big takeaways there.

1) The funds are now paying about 6% on borrowing and this rate will go higher as at least one rate hike is coming.

2) These numbers are not remotely reflected in the last expense ratio as the average, for 2022, was ridiculously low. Taking PFD as an example out of the two, the expense ratio was 2.53% last year.

CEF Connect-PFD

Great. Where are we today?

If we are paying 6% on $91.1 million, that works to $5.466 million total. On common assets of $134.95 million, the interest expense ratio is 4.05%. Your total expense ratio (assuming those other expenses stay the same) is 5.33%. Stunning, right? That is why the distributions keep falling.

Verdict

The only hope for this to stabilize is for a very rapid set of interest rate cuts. Those would boost preferred share prices and also cut expenses for these funds. We don't this that is going to work out. In all likelihood, the Federal Reserve will stay pat on rates (after raising them once more) for at least 6–9 months. If we see a rapid reversal, it will be due to a credit event and one that should create big blowback on preferred share pricing. Despite all the suffering for these funds, we are not ready to wade into these waters. Don't get us wrong. We like preferred shares as an asset class and have made multiple purchases recently. We also like bonds, and we are selectively buying corporate bonds where the yields are in the 7-8% range (see here , here , and here ) with exemplary credit and minimal to moderate duration risk. But leveraged CEFs are not in our playbook, for now.

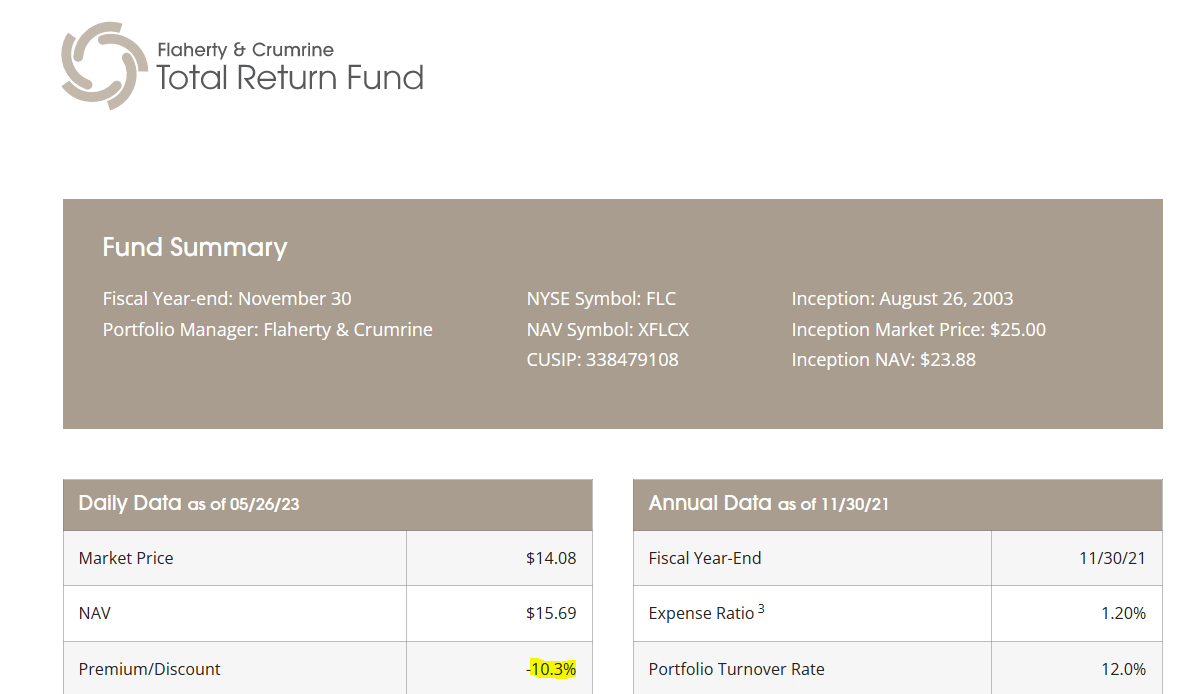

Getting back to the FLC vs PFD trade we had suggested, that looks close to getting done as well. FLC is trading at a 10.3% discount to NAV (7.5% discount to NAV in the last article).

{kind=link}

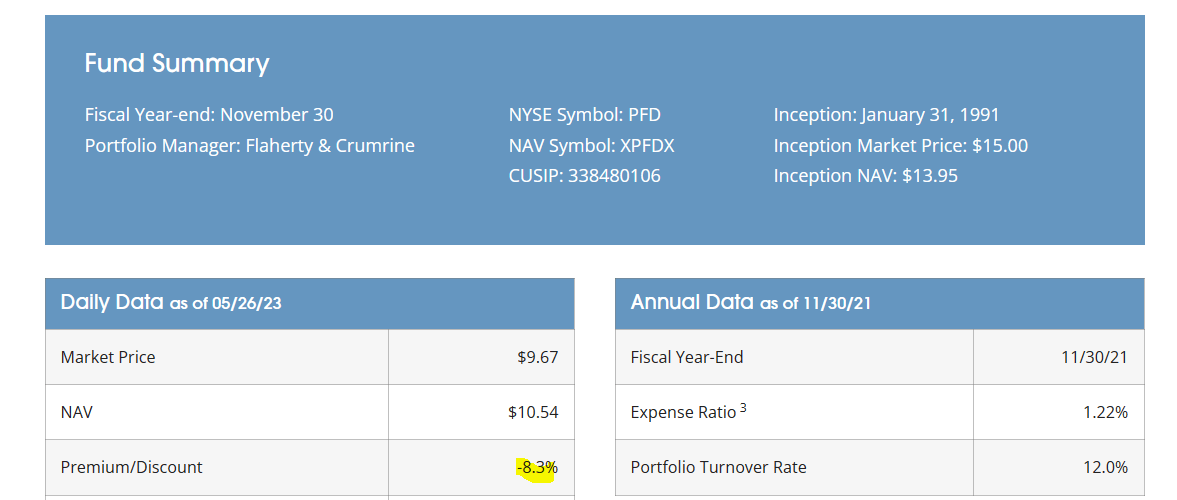

PFD is trading at a 8.3% discount (1.8% premium to NAV in last article).

{kind=link}

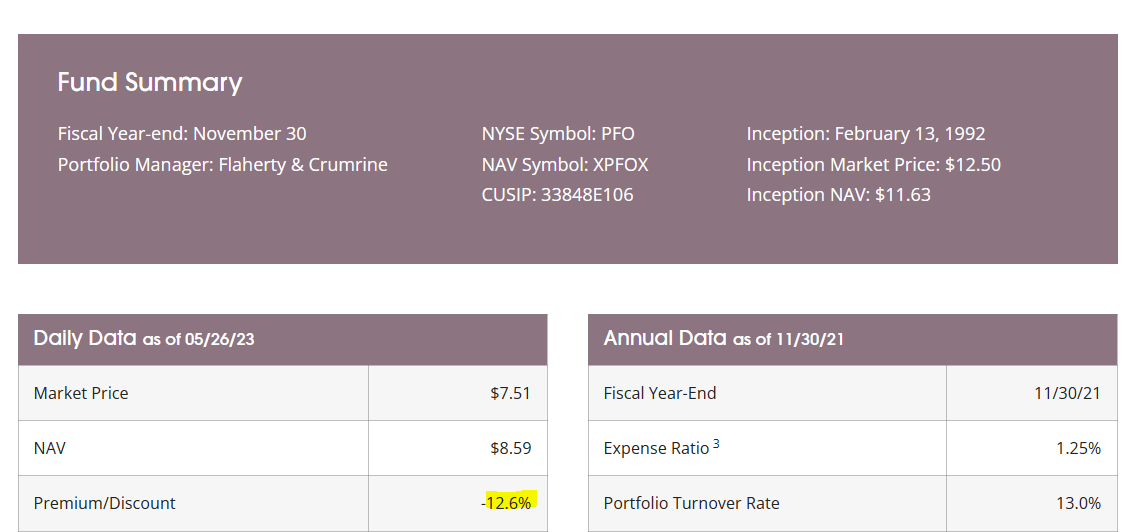

So this relative discount compression is in the final innings. We are relatively indifferent to not holding (yes, not holding) either of these today. In the Flaherty and Crumrine suite of identical funds, Flaherty & Crumrine Preferred Income Opportunity Fund ( PFO ) trades at the widest discount.

{kind=link}

Those wishing to speculate on a rebound in preferred shares, can consider taking a stab at that. We are enjoying the view from the sidelines and will not be buying any of these.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

PFD Vs. FLC: Outlook For Preferred CEFs