PFFD - PFFD: Own This When Yields Are Falling

Summary

- PFFD provides exposure to a broad index of preferred securities.

- PFFD is dominated by fixed-coupon preferreds.

- In a rising interest rate environment, PFFD underperforms its peer, the VRP ETF, due to negative duration impacts.

The Global X U.S. Preferred ETF (PFFD) provides broad exposure to an index of preferred stocks. Preferred stocks have a similar risk profile to junk bonds. Due to PFFD's heavy weight towards fixed-coupon preferreds, investors who want exposure to the preferred equity asset class may want to consider owning PFFD when interest rates are flat or declining, but switch into the Invesco Variable Rate Preferred ETF (VRP) when interest rates are rising.

Fund Overview

The Global X U.S. Preferred ETF provides exposure to a broad basket of preferred stocks in the U.S. The PFFD ETF tracks the ICE BofA Diversified Core U.S. Preferred Securities Index ("Index"), an index designed to measure the broad-based performance of the U.S. preferred securities market. The underlying index includes different categories of preferred securities, including floating rate, variable, and fixed-rate preferreds. To quality for the index, the securities must be listed in the U.S. and have a minimum of $50 million outstanding. The index is capitalization-weighted based on amount outstanding, and an issuer-cap of 10% is applied to limit the exposure to any one issuer.

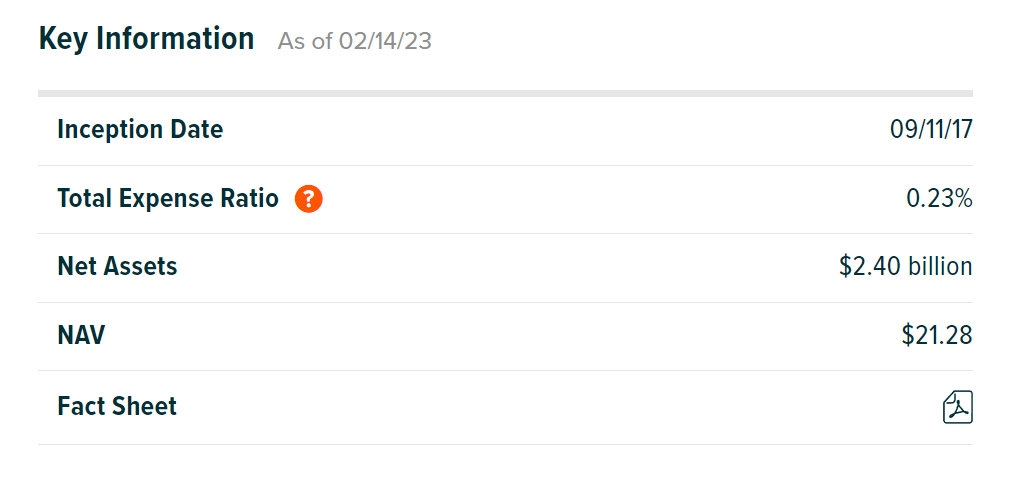

PFFD is a popular ETF with $2.4 billion in assets and charges a 0.23% expense ratio (Figure 1).

{kind=link}

What Are Preferred Shares

Preferred stock sits between bonds and common equity within a company's capital structure (Figure 2). They share commonalities with both bonds and equity. In the event of a credit default, preferred shareholders have a priority claim to assets compared to common shareholders, but are subordinated to bondholders.

Figure 2 - Preferreds sit between bonds and equity in capital structure (corporatefinanceinstitute.com)

Similar to bonds, preferred stocks usually pay a periodic yield, in this case, it is called a preferred dividend. However, unlike bond interest, preferred dividends are not contractually guaranteed, so a company in distress may stop paying preferred dividends without pushing the company into credit default. Preferred shareholders are usually compensated with higher yields than bonds.

Compared to common shares, preferred shares usually have no say on corporate matters. Also, preferred stock's appreciation potential is limited compared to common equity, as they trade like bonds and preferred shares usually have call provisions allowing the company to redeem them.

Portfolio Holdings

Figure 3 shows PFFD's sector allocation. As financial companies are the primary issuers of preferred securities, they dominate the PFFD index with a 70.7% weight. Utilities and Communication Services are allocated 11.8% and 6.5% respectively.

Figure 3 - PFFD sector allocation (PFFD factsheet)

Figure 4 shows PFFD's credit quality allocation. The fund is 59.4% allocated to investment-grade ("IG") rated preferreds, with 32.2% allocated to non-investment grade, and 9.3% unrated.

Figure 4 - PFFD credit quality allocation (PFFD factsheet)

Figure 5 shows that PFFD predominantly comprised of fixed-rate preferreds.

Figure 5 - PFFD coupon allocation (PFFD factsheet)

Returns

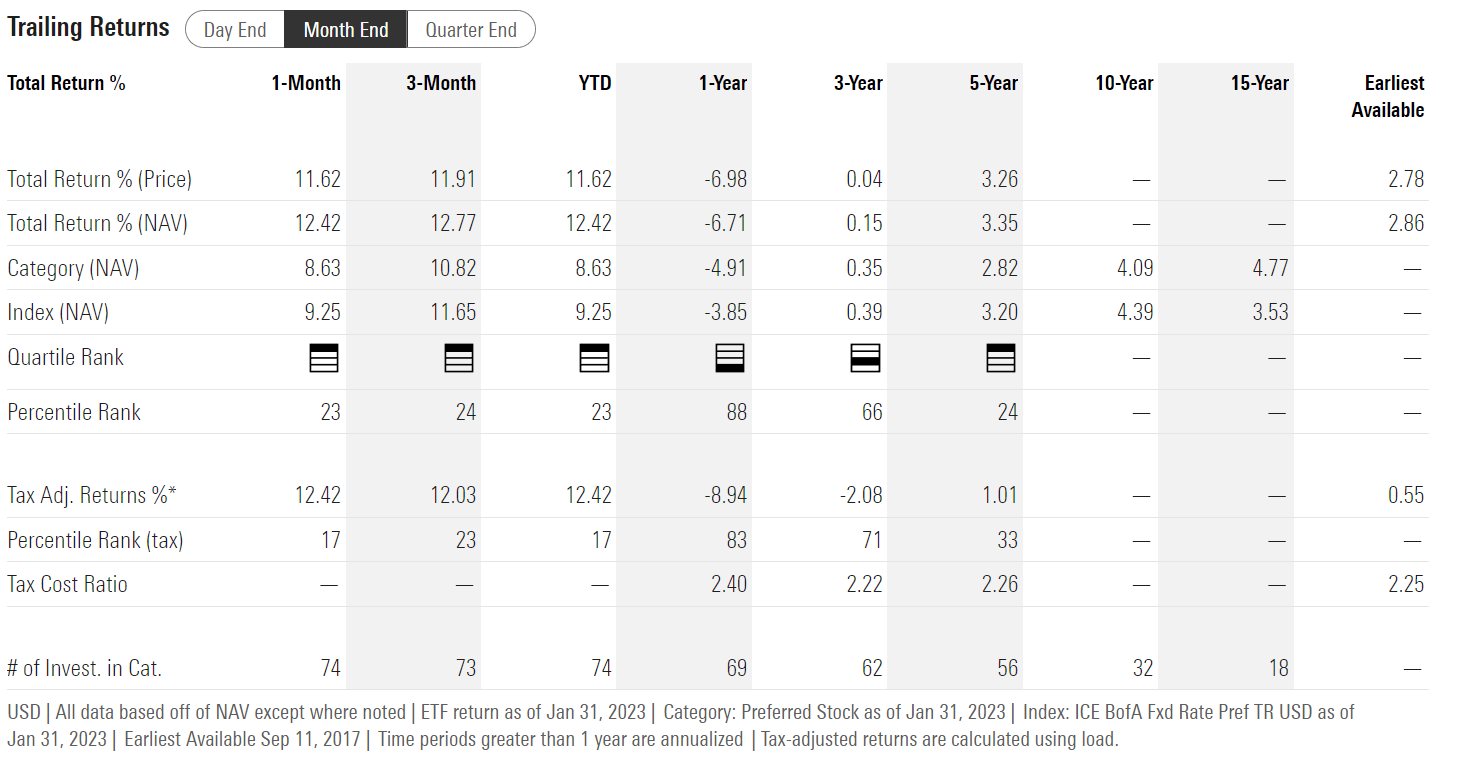

Figure 5 shows PFFD's historical returns. PFFD had an extremely poor 2022, with the fund returning -20.5%. This dragged down the average annual returns to 0.2% on 3Yr and 3.4% on 5Yr.

{kind=link}

PFFD's poor 2022 returns is most likely caused by its 78.8% weight in fixed-coupon preferreds. Fixed-coupon preferreds can be thought of like bonds, and in 2022, bonds suffered tremendously as the Fed increased Fed Funds Rates by 425 bps in order to fight inflation. For example, the iShares 7-10 Year Treasury Bond ETF ( IEF ) with an effective duration of 7.6 years, lost 15.2% in 2022. So I estimate PFFD's portfolio duration is likely larger than IEF's 7.6 years.

Distribution & Yield

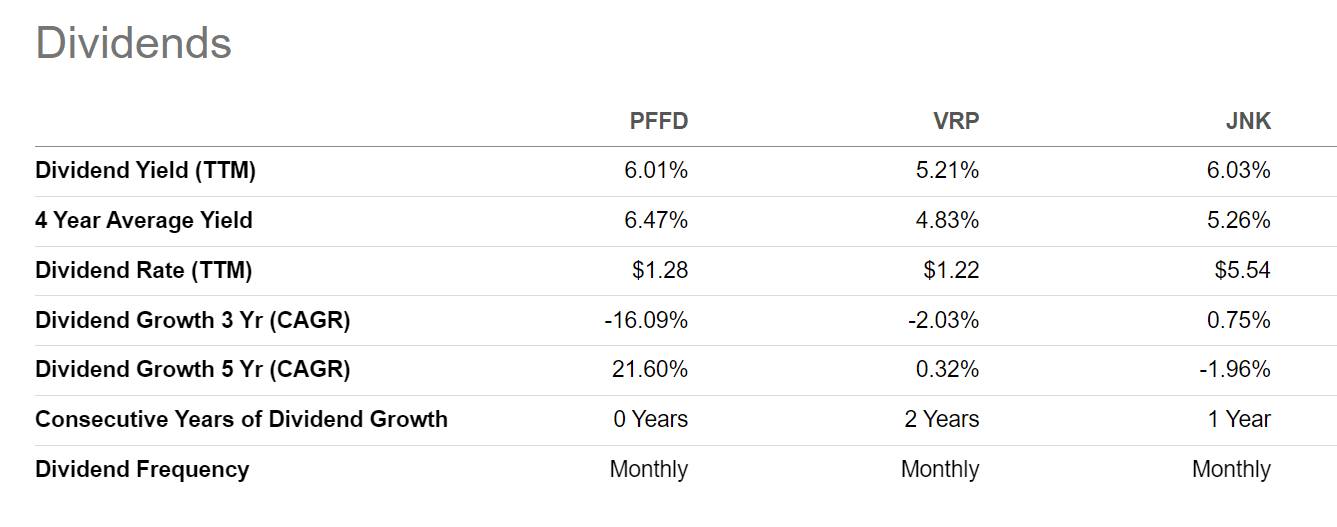

PFFD pays a fairly high monthly distribution of $0.105, which translates into a forward yield of 5.9%. Investors should note that PFFD's monthly distribution has been cut in the past few years. When the fund was first launched in 2017, it paid a monthly distribution of $0.1178. The distribution was cut to $0.1165 and $0.1148 in 2018, then $0.1135 in 2019, $0.1090 in 2020, and finally $0.105 in 2020.

PFFD vs. VRP

A few months ago, I reviewed another preferred share-focused ETF, the Invesco Variable Rate Preferred ETF ("VRP"). How does PFFD compare to VRP?

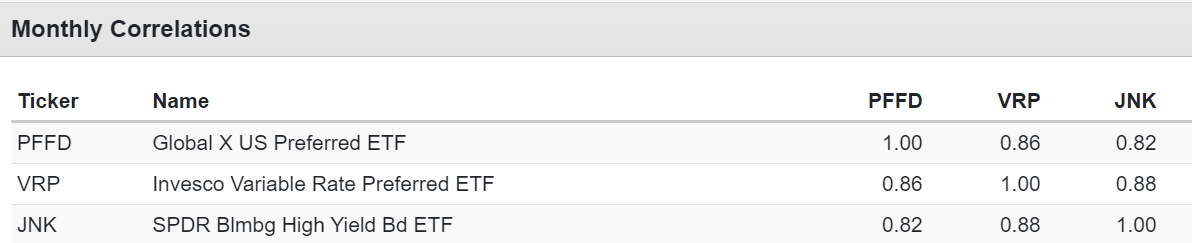

Analysing the funds with the time period October 2017 (PFFD's inception) to January 2023, we can see that PFFD and VRP are highly correlated (which makes sense, since both invest in the preferred equity asset class). It should also be noted that both funds have a high monthly return correlation to the SPDR Bloomberg Barclays High Yield Bond ETF ( JNK ) (Figure 6).

Figure 6 - PFFD vs. VRP vs. JNK correlation (Author created with Portfolio Visualizer)

{kind=link}

This speaks to the high-yield bond-like return profile of preferreds.

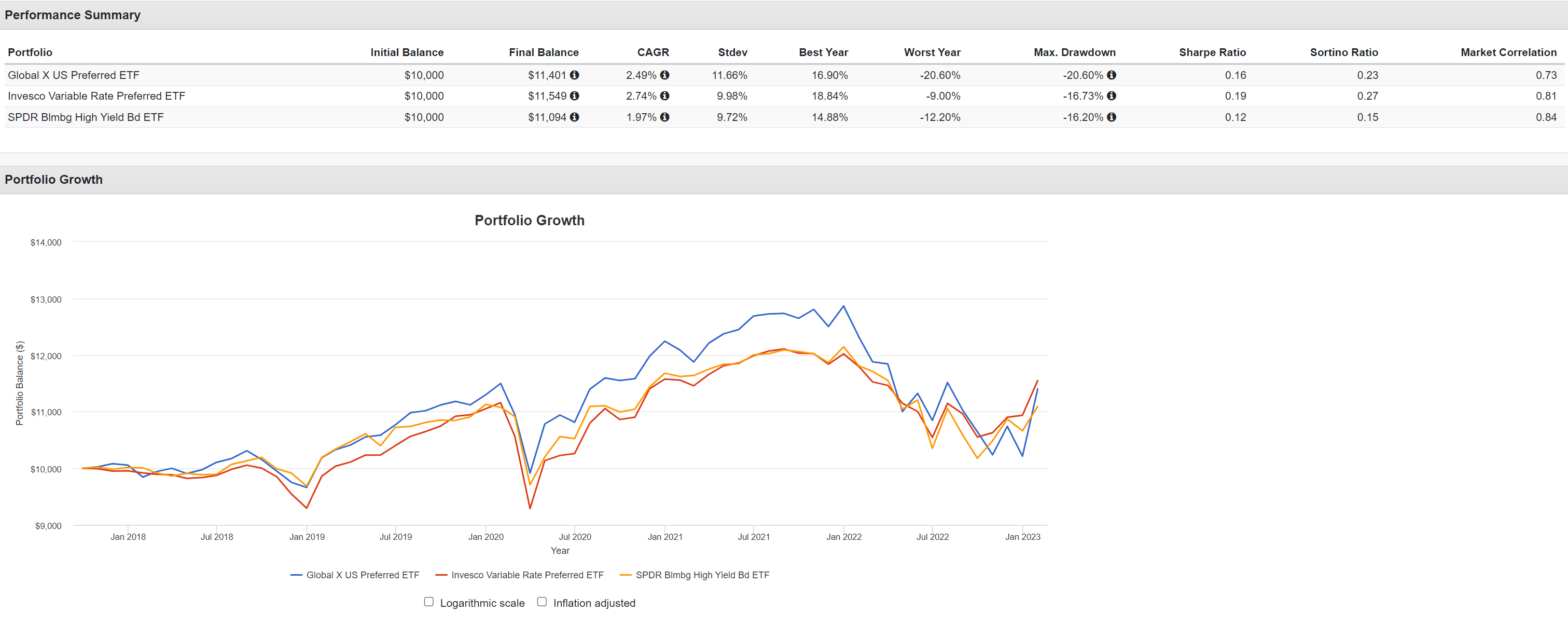

In terms of returns, both PFFD and VRP have outperformed JNK, with CAGR returns of 2.5% and 2.7% respectively vs. 2.0% for JNK (Figure 7).

Figure 7 - PFFD vs. VRP vs. JNK returns and risk (Author created with Portfolio Visualizer)

{kind=link}

PFFD does have significantly higher volatility of 11.7% vs. 10.0% for VRP and 9.7% for JNK. This leads to VRP having a better Sharpe Ratio of 0.19 vs. 0.16 for PFFD.

Comparing distribution yields, the PFFD has a 6.0% trailing 12 month distribution yield, equal to JNK's 6.0% yield and slightly ahead of VRP's 5.2% (Figure 8).

{kind=link}

Prefer VRP When Yields Are Rising

It is no surprise, but when I compare PFFD to VRP head to head, I prefer to own the variable rate VRP ETF when yields are rising, as it does not suffer from negative duration impacts.

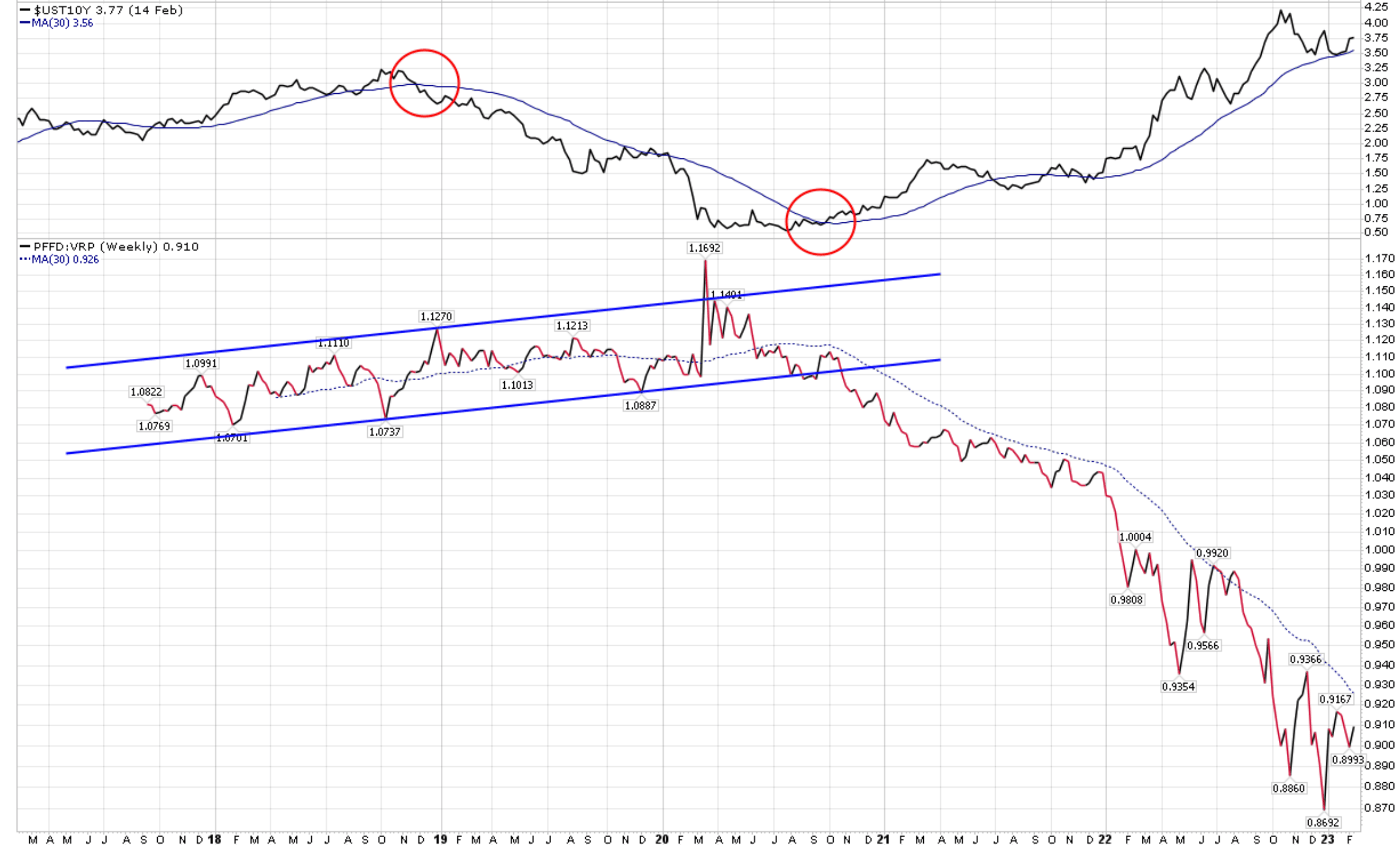

For example, looking at figure 9 below, we can see that the PFFD / VRP ratio is in a rising trend when interest rates, as represented by the U.S. 10Yr treasury yield, is steady or falling. However, since late 2020, 10Yr treasury yields have been in an uptrend, and the PFFD / VRP ratio has been in a steep decline.

Figure 9 - PFFD / VRP ratio vs. 10Yr treasury yields (Author created with price charts from stockcharts.com)

{kind=link}

As long as interest rates remain in an uptrend, I believe investors should own the variable rate VRP ETF instead of the fixed-coupon dominated PFFD ETF. Investors can use a simple 150 day moving average ("DMA") or 200 DMA to delineate between up / downtrends on yields.

Conclusion

The PFFD ETF provides broad exposure to an index of preferred securities. It is predominantly fixed-coupon weighted, which hurt the fund's performance in 2022. Investors who want exposure to the preferred equity asset class may want to consider owning PFFD when interest rates, as measured by the 10Yr treasury yield, are flat or declining, and own the VRP when interest rates are rising.

For further details see:

PFFD: Own This When Yields Are Falling