PFIX - PFIX: Tactically Neutral On Interest Rates (Ratings Downgrade)

2023-11-06 23:47:08 ET

Summary

- Simplify Interest Rate Hedge ETF has returned over 25% since August, offsetting fixed income losses from rising interest rates.

- However, Treasury Department's recent Quarterly Refunding Announcement acted as a catalyst to relieve some pressures in the treasury bond markets on lower total issuance and coupon bond share.

- Longer term, my macro outlook still calls for structurally higher long-term interest rates as the U.S. government continues to rack up deficits at an alarming rate.

In early August, I wrote an article reiterating my bullish view on the Simplify Interest Rate Hedge ETF ( PFIX ) as an interest rate hedge. At the time, I was worried about the U.S. government's fiscal profligacy, which had prompted a debt downgrade from Fitch. The Fed's 'higher for longer' monetary policy also threatened to keep short-term interest rates elevated, which could in turn force long-term interest rates higher through the 'term premium'. Finally, global yields were breaking out, so the path of least resistance was for higher interest rates globally.

Since my article, the PFIX ETF has returned over 25% (PFIX returns reached 46% in late October before pulling back in recent days), offsetting most of the fixed income losses in my portfolio (Figure 1).

Figure 1 - PFIX has performed well as an interest rate hedge (Seeking Alpha)

However, consistent with my recent upgrade of the iShares 20+ Year Treasury Bond BuyWrite Strategy ETF ( TLTW ) from a sell to a hold, my near-term outlook for interest rates is more balanced and hence I am downgrading the PFIX ETF to a hold at this time.

Brief Fund Overview

For those not familiar with the PFIX ETF, the Simplify Interest Rate Hedge ETF provides investors with a hedge against rising long-term interest rates through its portfolio of over-the-counter ("OTC") interest rate swaptions that provide convex exposure to large upward moves in interest rates and interest rate volatility.

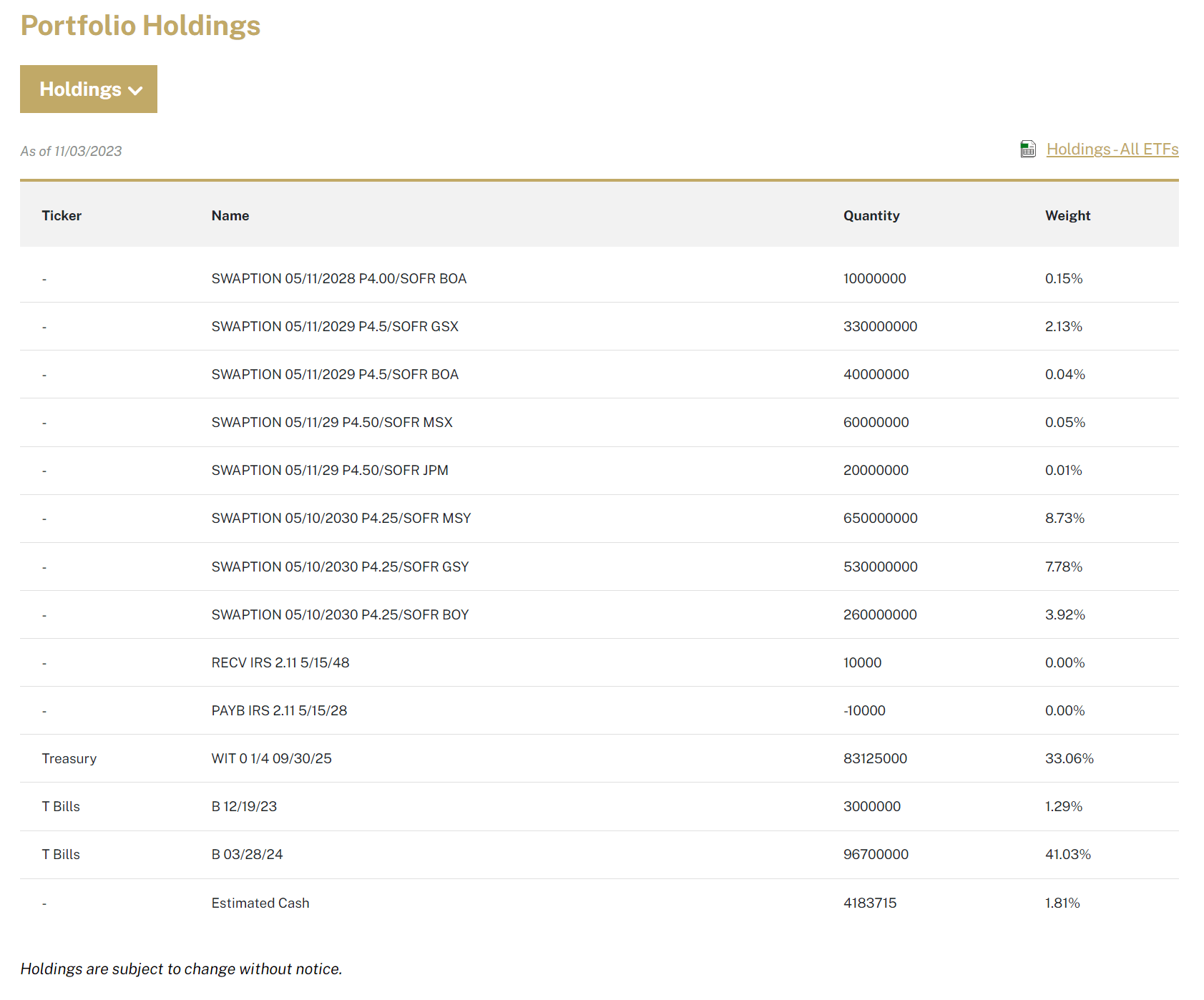

The PFIX ETF holds OTC swaptions with maturities ranging from 2028 to 2030 paying 4.25% to 4.5% fixed interest rates, struck against major investment banks like Goldman Sachs and Bank of America (Figure 2).

{kind=link}

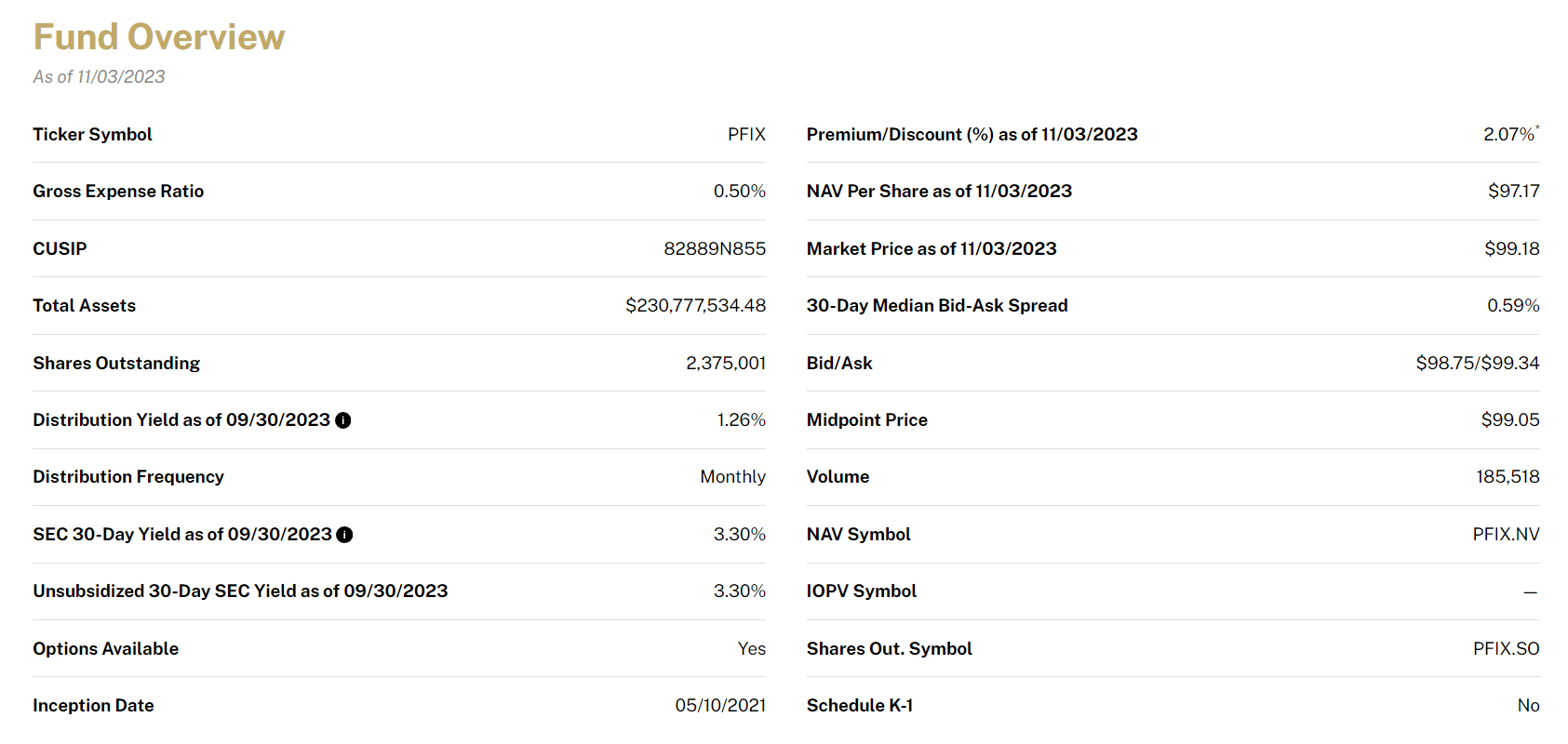

Surprisingly, despite PFIX's strong performance, assets in the fund have remained stagnant at only $231 million compared to $204 million in August. This suggest traders have actually been redeeming their positions (Figure 3).

{kind=link}

Shift To Bill Issuance Relieves Term-Premium Pressures

In the short-term, the Treasury Department's recent Quarterly Refunding Announcement ("QRA") on November 1st acted to relieve some of the pressures in the treasury bond markets. For the upcoming October to December quarter, the Treasury is forecasting a need to borrow $776 billion in privately held net marketable debt.

While this figure is enormous, it is actually $76 billion lower than the Treasury's first estimate made in August. In a recent article on the US Treasury 3 Month Bill ETF (NASDAQ: TBIL ), I explained how some macro analysts viewed the August QRA as a liquidity drain on the financial markets as the Treasury had to borrow $274 billion more than originally forecasted. Since the November QRA is a surprise to the downside, it may act as a liquidity boost instead.

Moreover, much of the pressures on long-term treasury yields since August have been due to the increased auction sizes of long-duration coupon treasury bonds to fund the U.S. government's enormous deficits.

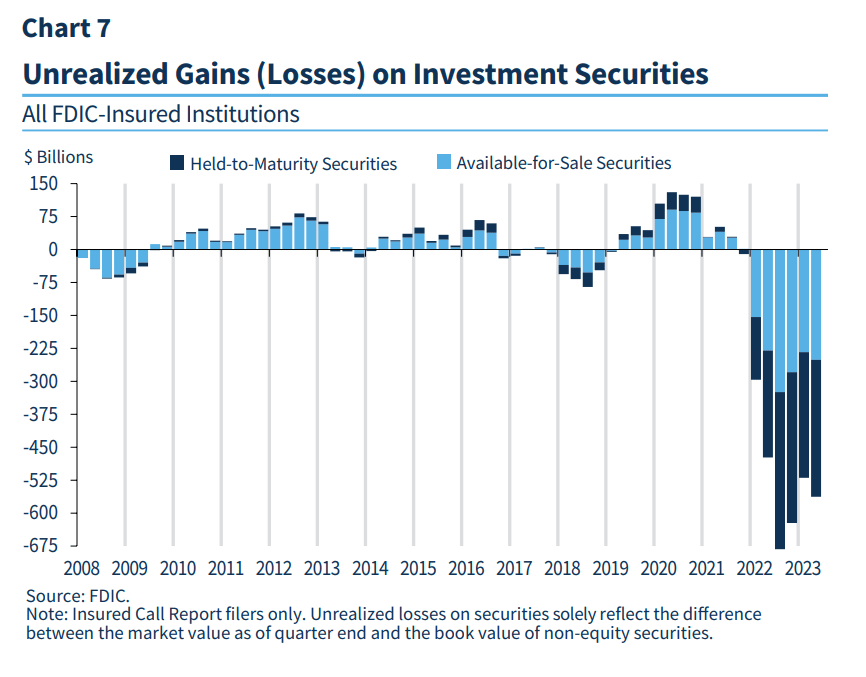

Increased treasury bond supply swamped investor demand, which was already suffering from a lack of buyers as banks were capital constrained from huge unrealized mark-to-market losses from prior purchases (Figure 4).

Figure 4 - Banks were capital constrained due to unrealized losses (FDIC)

{kind=link}

Foreign buyers like China were also stepping away from U.S. treasuries due to geopolitical reasons. This led to multiple 'tailed' treasury auctions where investors demanded far higher interest rates to bid for treasury bonds.

Recognizing the upwards pressure on 'term premiums' from an unbalanced supply/demand picture on coupon bonds, the Treasury Department decided to increase the share of treasury bills in the upcoming quarters, meaningfully deviating " from the historical recommendation for 15-20% T-Bill share."

A lower than expected total issuance and lower coupon bond share in the coming few months helped relieve the upward pressures on long-term interest rates and sparked a massive short-squeeze in treasury bonds, with the 10 year treasury yield declining from 4.90% on the Tuesday before the QRA to 4.52% by Friday, November 3rd (Figure 5).

Figure 5 - 10 year treasury yields have experienced a massive squeeze (www.marketwatch.com)

{kind=link}

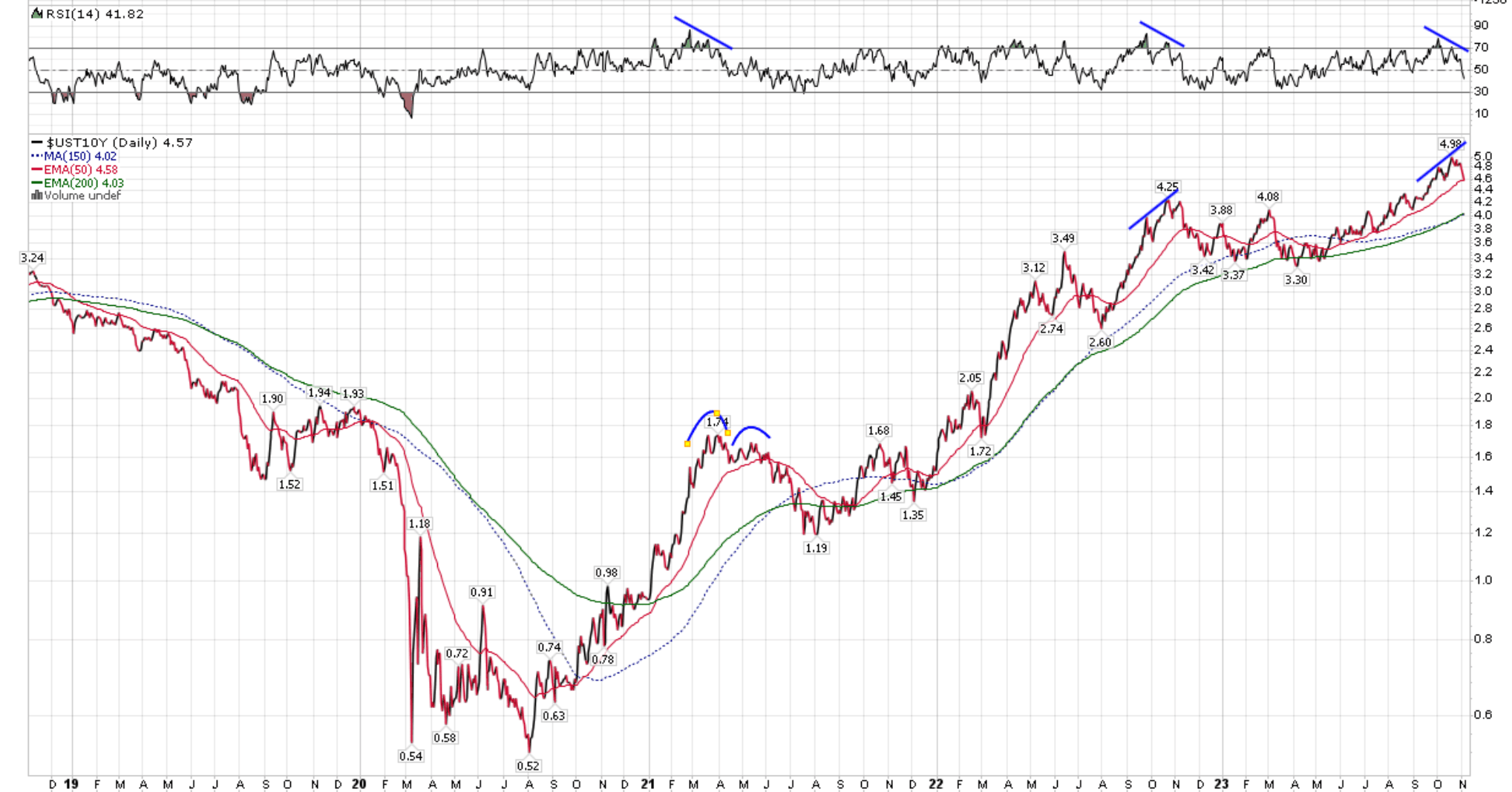

Looking forward, this squeeze may continue in the short term, as long-term treasury yields are deeply overbought, with negative divergence, similar to several recent bond rallies (Figure 6).

Figure 6 - 10 year yield was deeply overbought with negative divergence (Author created with price chart from stockcharts.com)

{kind=link}

Long-Term Fiscal Problems Remain Unresolved

However, my long-term view remains unchanged regarding interest rates. As long as the U.S. government continues to spend like a drunken sailor, there will continue to be pressures for long-term interest rates to go higher.

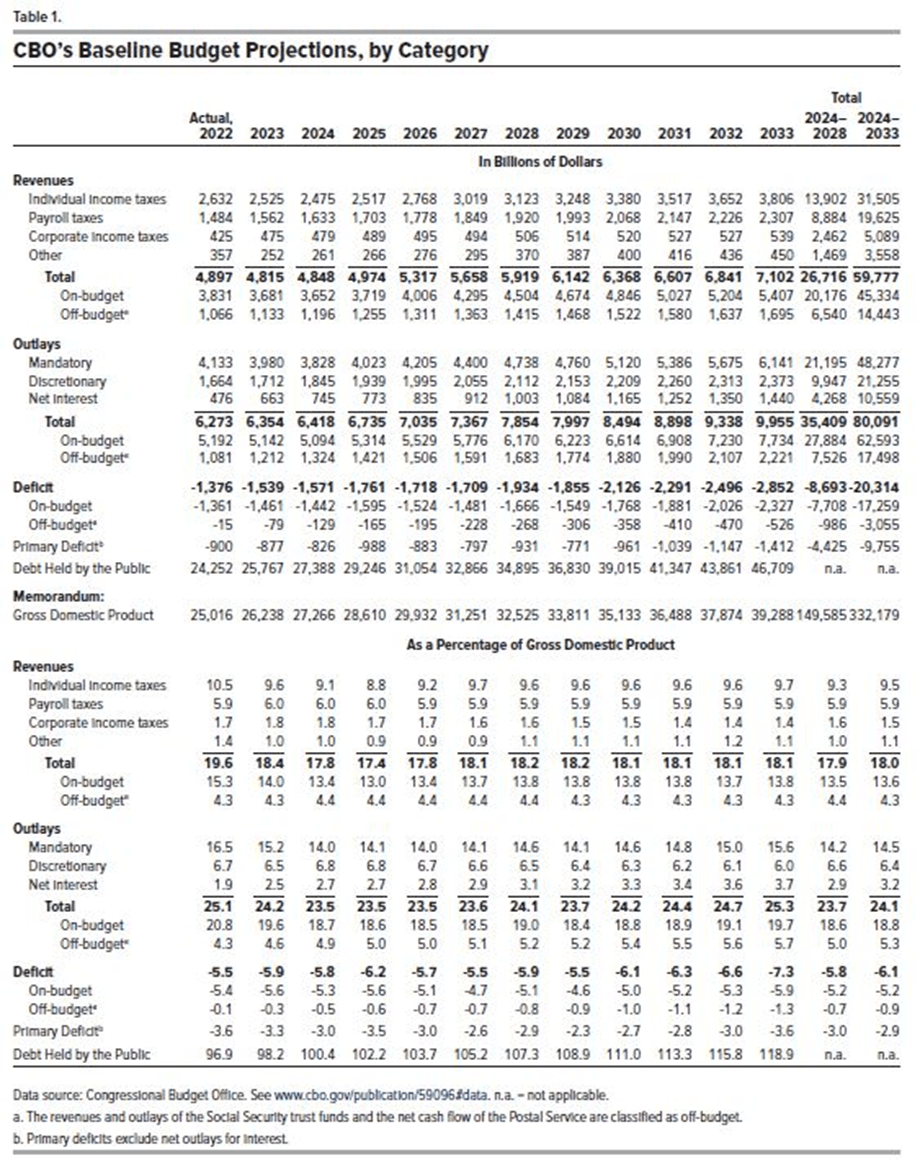

As a reminder, based on the CBO's latest projections , the U.S. government is expected to rack up an additional $21 trillion in debt from 2023 to 2033 due to persistently large annual deficits (Figure 7).

Figure 7 - CBO baseline projections (Congressional Budget Office)

{kind=link}

The interest expense in the figure above is based on an average interest rate of 3.2% in 2033. If current interest rates ~5% are used instead of the CBO's projections, famed hedge fund manager and Treasury critic Stanley Druckenmiller warns that the government's yearly interest expense will reach 4.5% of GDP by 2033 and 7% by 2043. At 7% of GDP, interest expense alone will surpass total current discretionary spending on programs like national defense, foreign aid, education, and transportation.

So while I am tactically neutral on long-term interest rates, I believe there is still enormous structural pressures for long-term interest rates to rise unless the U.S. government can rein in its spending.

Conclusion

In the past few months, the PFIX ETF has performed its job admirably, acting as an excellent hedge against rising interest rates. However, with the recent Treasury QRA announcement, I am turning tactically neutral on interest rates, as I believe the bond markets are deeply oversold and primed for a short squeeze on the outlook for lower coupon bond issuances in the near-term. I will revisit the PFIX ETF at a later date if conditions warrant hedging from rising interest rates.

For further details see:

PFIX: Tactically Neutral On Interest Rates (Ratings Downgrade)