PFL - PFL: A Solid Bond CEF For Income But It Isn't Cheap

2023-07-24 19:26:30 ET

Summary

- Investors today are desperate for any source of income as the high inflation in the United States has pushed up all of our regular expenses.

- PIMCO Income Strategy Fund invests in a portfolio of debt securities to provide investors with a high level of income to meet their overall desire.

- The PFL closed-end fund has a mix of fixed-rate and floating-rate securities, but it still has a great deal of exposure to interest rates.

- The fund's 12.00% distribution yield appears to be sustainable, particularly considering the recent recovery in the bond market.

- The fund is trading at a premium to the net asset value, which is rather disappointing.

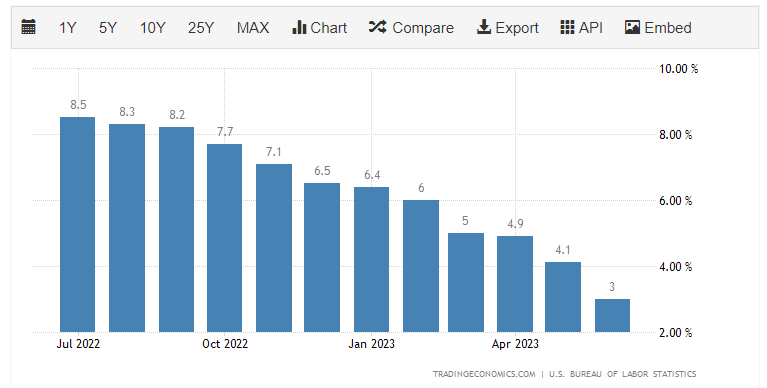

There can be little doubt that one of the biggest problems facing the average American today is the rapidly rising cost of living. This is due to the inflation that has been ravaging the nation ever since the economy reopened from the pandemic and the enormous amount of freshly-created money from that period entered circulation. This has pushed up the price of just about everything that we buy, which is clearly evident if we look at the consumer price index. The consumer price index claims to measure the price of a basket of goods that is regularly purchased by the average person. As we can see here, the consumer price index has posted a year-over-year increase of more than the 2% that is considered healthy during each of the past twelve months:

{kind=link}

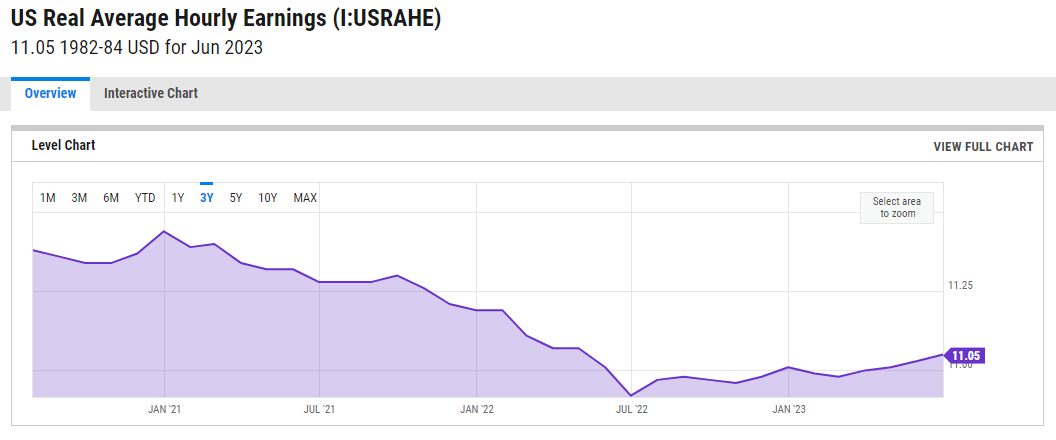

This has had a devastating effect on most people because wages have not kept up with the rising prices. As we can see here, real average hourly earnings are down substantially over the past three years:

{kind=link}

Thus, the paychecks that consumers receive from their employers do not go as far as they once did. While sources disagree on what percentage of Americans live paycheck to paycheck (I found surveys stating 58% to 69%, all published within the past four weeks), enough of them do that it should be very obvious why people would become financially squeezed when the purchasing power of their wages declines. As such, we have seen many people resorting to taking on second jobs, entering the gig economy, or even dumpster diving just to make ends meet. In short, people are desperate for additional sources of income just to maintain their lifestyles.

As investors, we are certainly not immune to this. After all, we need money to pay the bills, heat our homes, and purchase an occasional luxury. All of these things are expensive and what income we once had no longer goes as far.

Fortunately, we have methods that we can use to increase our incomes so that we do not have to resort to some of the extreme activities that others are engaging in. After all, we have the ability to put our money to work for us to earn an income. One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in income. These funds are unfortunately not very well followed by the financial media and many investment advisors are unfamiliar with them. As such, it can be difficult to obtain the information that we would really like to have to make an informed decision about a share purchase.

This is unfortunate, because these funds offer a number of advantages over ordinary open-ended and exchange-traded funds. In particular, a closed-end fund is able to employ certain strategies that allow them to boost the effective yield of their portfolios well beyond that of the underlying assets or indeed pretty much anything else in the market.

In this article, we will discuss the PIMCO Income Strategy Fund ( PFL ), which is one fund that investors can purchase to earn an income. This fund's income qualifications are fully on display with the fact that it has a 12.00% yield at the current price. That is certainly enough to grab the attention of anyone that is seeking a high level of income, but admittedly anytime a fund achieves such a high yield there is a concern that it will be forced to cut the distribution in the near future. This is something we will want to be sure to examine in detail in this article. I have discussed this fund before, but a great deal of time has passed since then so naturally some things have changed. This article will therefore focus specifically on these changes as well as provide an updated analysis of the fund's finances. Let us investigate and see if this fund makes sense for your portfolio.

About The Fund

According to the fund's webpage , the PIMCO Income Strategy Fund has the objective of providing its investors with a high level of current income. The fund also seeks to preserve the value of its shareholders' principal, which is a fairly common goal for a fixed-income fund. In fact, both of these goals are very much expected for a fund that is almost entirely invested in bonds:

CEF Connect

The fact that this fund is entirely invested in bonds should not be surprising considering that this is a PIMCO fund. This particular fund house is quite well known for being focused on bond investments. The fund's objective should likewise not be surprising in this light since bonds by their very nature deliver their investment returns in the form of current income. A bond investor purchases a bond at face value, receives regular coupon payments that serve as income, and then receives the face value back when the bond matures. Over its lifetime, the only investment return that is delivered by the bond is the coupon payments. There are no net capital gains over time because bonds have no inherent link to the growth and prosperity of the issuing company. They are simply a loan made to a company and the company does not pay its creditors more just because its income went up.

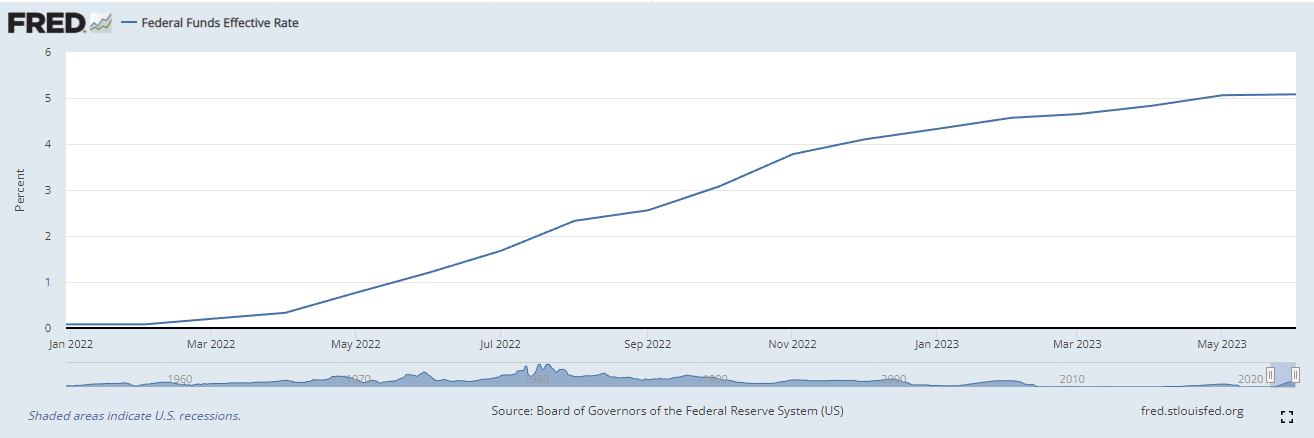

With that said, it is possible to make a profit by trading bonds because the price of a given bond does vary over time in the market. In particular, bond prices tend to move with interest rates. It is an inverse relationship, so when interest rates go up, bond prices decline. The reverse is also true. As everyone reading this is likely well aware, the Federal Reserve has been aggressively raising the benchmark federal funds rate over the past eighteen months or so in an attempt to control the high inflation rate plaguing the economy. As we can see here, the effective federal funds rate went from 0.08% at the start of 2022 to 5.08% today:

{kind=link}

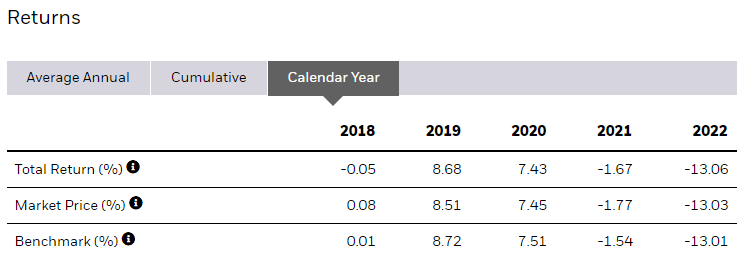

This is one of the most rapid interest-rate hiking cycles that the United States has ever seen. In fact, as of the time of writing, American interest rates are at the highest level that we have seen since 2007. This rapid increase in rates has had a devastating impact on bond prices and bond funds. We can see this in the simple fact that the Bloomberg U.S. Aggregate Bond Index ( AGG ) was down 13.01%:

{kind=link}

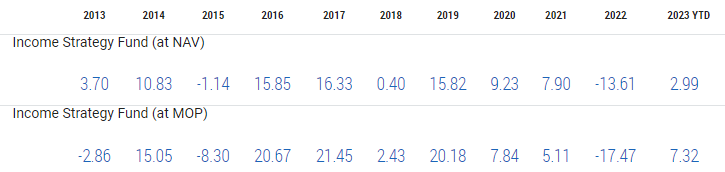

The PIMCO Income Strategy Fund was certainly not saved from this carnage as it delivered a total return of -13.61% in 2022:

{kind=link}

That was one of very few bad years for this fund. We can also see that 2022 is one of the only years in which the PIMCO Income Strategy Fund underperformed the Bloomberg bond index. This is probably partly due to the fund's use of leverage, which we will discuss later in this article.

The bond market has certainly improved a bit since 2022 though. As we can see above, the PIMCO Income Strategy Fund has delivered a 2.99% total return year-to-date, which is slightly better than the 2.09% return of the Bloomberg U.S. Aggregate Bond Index over that period. This came in spite of the fact that interest rates have actually increased since the start of 2023, albeit not as rapidly as we saw in 2022. This would seem to go against the maxim that bond prices and interest rates move inversely to one another. That is certainly true, but in this case, the bond market is being driven by expectations of future interest rates. The market right now assumes that the economy will enter a recession during the second half of 2023 and that said recession will prompt the Federal Reserve to cut rates. As of right now, the market is assuming one or possibly two more rate hikes in 2023 and then a series of cuts in 2024. Bond price action currently points to expectations of a federal funds rate of about 3.60% at the end of 2024. It is fair then to assume that bond prices will rapidly decline if that outcome appears to be unlikely.

In order to determine the future trajectory of this fund then, we need to determine how likely it is that the Federal Reserve will cut rates in 2024. Jerome Powell has been consistently taking a hawkish policy of "higher for longer." However, at the June meeting, a majority of policymakers did see lower rates in 2024 (see here ). Anyone that has watched the markets knows to take such predictions with a grain of salt. After all, this is the same central bank that said that 2021 inflation was "transitory" and that the subprime crisis was "no big deal" in 2007. The big thing that policymakers may be overlooking here is that nearly all of the improvements to the headline inflation rate recently have been caused by the fact that energy prices are lower than at this time last year.

I have discussed this in numerous previous articles. There are certainly reasons to believe that energy prices may begin to rise during the second half of this year due to a possible crude oil shortage . If that happens, it will push up the headline inflation numbers and essentially force the Federal Reserve to keep interest rates higher than the market expects. Naturally though, predicting Federal Reserve policy is an inexact science at best so we cannot be certain what to expect going forward.

One of the interesting things about the PIMCO Income Strategy Fund is that it can buy both floating-rate and fixed-rate securities. According to the webpage,

The fund has the flexibility to allocate assets in varying proportions among floating- and fixed-rate debt instruments, as well as among investment grade and non-investment grade securities. It may focus more heavily or exclusively on an asset class at any time, based on assessments of relative values, market conditions, and other factors.

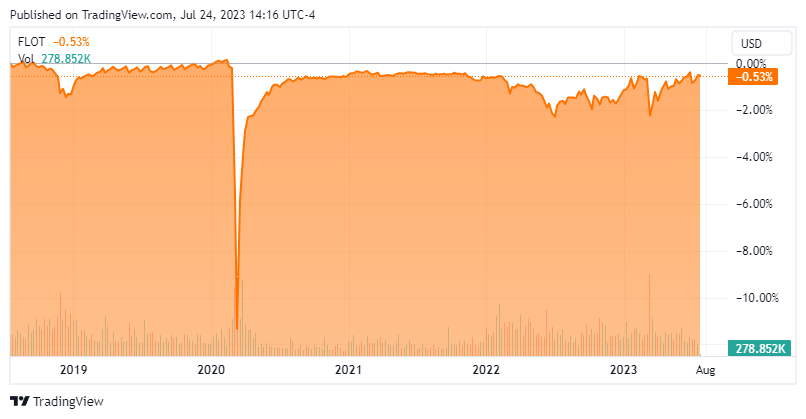

The big difference between fixed-rate bonds and floating-rate securities is that a floating-rate security will not really be negatively impacted by rising interest rates. This is because the bond will always pay an interest rate that is competitive with other securities in the marketplace. Thus, the price does not need to decline in order to bring up its yield. We can see this in the fact that the iShares Floating Rate Bond ETF ( FLOT ) has been almost perfectly flat over the past five years despite the variance in interest rates over the period:

{kind=link}

Thus, the PIMCO Income Strategy Fund could opt to put most of its assets into this asset type during a rising rate environment and thus offset the fact that bond prices in the aggregate are declining. The reverse is also true though, as these securities do not benefit at all from interest rate declines.

It is surprising that the fund did not heavily invest in these securities last year, as it would not have suffered the losses that it reported if it had. Unfortunately, neither the fund's webpage nor the third-quarter holdings report states what percentage of the fund is invested in floating-rate versus fixed-rate securities. Thus, we cannot be certain what percentage of the fund's assets are protected from interest rates through investment in floating-rate versus fixed-rate securities. CEF Connect states that 38.52% of the fund is invested in bank loans:

CEF Connect

Bank loans are usually floating-rate securities, whereas the other things on here are fixed-rate. It is by no means certain that this is the case here, though. I will admit that I would like to see official numbers from the fund as to what proportion of the fund is invested in floating-rate versus fixed-rate debt as that is important for determining our exposure to interest rate risk. As it is, it's just a matter of making an educated guess about the bank loans being the entirety of the floating-rate debt in the fund.

Leverage

In the introduction to this article, I stated that closed-end funds such as the PIMCO Income Strategy Fund are capable of using certain strategies that have the effect of boosting the effective yield of the portfolio. One of these strategies is the use of leverage. In short, the fund will borrow money and then use that borrowed money to purchase bonds and other debt securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case. With that said though, the beneficial effects of leverage are not as great today as they were a year ago when interest rates were at 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This is one reason why this fund tends to outperform the index during bond bull markets and underperforms during bear market declines like we saw last year. As such, we want to ensure that the fund is not taking on too much risk since that would expose us to too much risk. I generally do not like to see any fund have leverage exceeding a third as a percentage of its assets for that reason. The PIMCO Income Strategy Fund currently satisfies this requirement as its levered assets comprise 31.13% of the fund. Thus, this fund appears to be striking a good balance between risk and reward.

Distribution Analysis

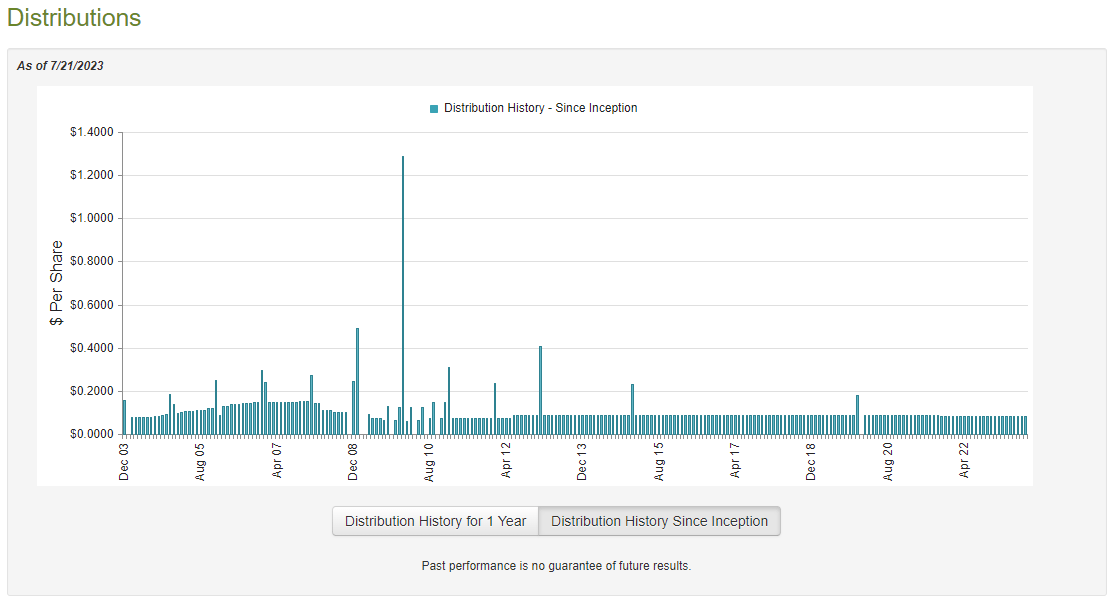

As mentioned earlier in this article, the primary objective of the PIMCO Income Strategy Fund is to provide its investors with a high level of current income. In order to achieve this objective, it invests in a portfolio of both investment-grade and junk debt securities that deliver nearly all of their investment returns in the form of direct payments to their owners. It then applies a layer of leverage to the portfolio to boost the effective yield and pays all of its returns out to the shareholders. As such, we can probably assume that the fund will have a very high yield. This is indeed the case as the fund currently pays a monthly distribution of $0.0814 per share ($0.9768 per share annually), which gives it a 12.00% yield at the current price. The fund has generally been consistent about its distribution for a fixed-income fund, although it has changed its distribution from time to time:

{kind=link}

The fact that the fund's distribution has not been perfectly stable might reduce its appeal in the eyes of some investors that are looking for a stable and secure source of income to use to pay their bills or finance their lifestyles. However, it has been much less volatile in this respect than some fixed-income funds so it could still be an attractive source of income. Of course, that assumes that the fund's current distribution is sustainable, and generally whenever a fund's yield goes over 10% the market assumes that it will need to cut soon. Let us investigate this and determine if that is the case.

Unfortunately, we do not have an especially recent report to consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on December 31, 2022. As such, it will not have any information about the fund's performance over the first half of this year. As already mentioned, that was a stronger bond market than 2022 was so it is fair to assume that the fund managed to improve its finances since this report was issued. With that said, this report will still give us a pretty good idea of how well the fund handled the challenging conditions that were present over most of the course of 2022. During the six-month period, the PIMCO Income Strategy Fund received $19.541 million in interest along with $173,000 in dividends from the assets in its portfolio. This gives the fund a total investment income of $19.714 million over the period. It paid its expenses out of this amount, which left it with $15.623 million available for shareholders. That was, unfortunately, not enough to cover the $17.766 million that the fund actually paid out over the period but it did manage to get reasonably close. Still, the fact that the fund's net investment income was insufficient to cover the distributions is concerning at first glance. This is especially true because we like fixed-income funds to be able to fully cover their distributions out of this figure.

The fund does, however, have other methods through which it can obtain the money that it needs to cover the distributions. For example, it might have been able to generate some trading profits from the movement in bond prices that can be distributed. Unfortunately, the fund failed at this task during the period as it reported net realized gains of $7.195 million but this was offset by $17.063 million in net unrealized losses. Overall, the fund's assets declined by $1.370 after accounting for all inflows and outflows, but that is only because the fund did a $10.184 million capital raise during the period. This is certainly concerning, but it is important to keep in mind that the net investment income plus the net realized gains were sufficient to cover the fund's distributions and still have some money left over. Unrealized losses are not necessarily a huge deal with bonds since the holder will always receive the face value of the bond at maturity assuming the issuer does not default. As such, the fund's distribution is probably sustainable, especially because the bond market recovered year-to-date and the fund probably profited from that.

Valuation

It is always critical that we do not overpay for any assets in our portfolio. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the PIMCO Income Strategy Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of July 21, 2023 (the most recent date for which data is available as of the time of writing), the PIMCO Income Strategy Fund had a net asset value of $7.72 per share but the shares currently trade for $8.18 per share. This gives the fund's shares a 5.96% premium to the net asset value at the current price. That is relatively in line with the 5.13% premium that the shares have had on average over the past month but it is still a premium. It is rare for PIMCO funds to trade at a discount though, so this might be as good a price as we are going to get.

Conclusion

In conclusion, the PIMCO Income Strategy Fund is one of the better bond funds available on the market. That is what we have come to expect from PIMCO though, which has long been one of the premier fund houses for this asset class. The fund boasts a very high yield, but it appears that it can sustain it. Unfortunately, the fund's valuation is a bit steep but it almost always is for anything from PIMCO so unfortunately you might have to pay the premium if you want the fund. I wish we had somewhat more visibility into the PIMCO Income Strategy Fund's actual mix between fixed-rate and floating-rate securities, but that is my only real complaint here.

For further details see:

PFL: A Solid Bond CEF For Income, But It Isn't Cheap