PAXS - PFL: Good Bond CEF But Bond Bear Market Is A Big Risk

2023-09-28 13:56:32 ET

Summary

- PIMCO Income Strategy Fund offers a high current yield of 12.92%, but the market suggests it may be unsustainable in the future.

- The PFL closed-end fund's performance has been poor, falling 7.69% since July 2023, but still outperformed the S&P 500.

- Fixed-income securities have been suffering due to the Federal Reserve's fight against inflation and high interest rates are expected to continue.

- The fund failed to cover its distribution over the past year, even though it conducted a capital raise. It is difficult to see how it can sustain its distribution.

- The fund is currently trading at a discount to net asset value, which is very rare for a PIMCO fund.

The PIMCO Income Strategy Fund ( PFL ) is a popular fixed-income closed-end fund aka CEF among investors who are seeking to earn a very high level of current income from their assets. The fund certainly performs that task quite admirably, as its 12.92% current yield is much higher than just about anything else in the market. In fact, this yield is sufficiently high that the market seems to be telling us that it is unsustainable and will need to be cut in the future. We will want to be sure to investigate this possibility in this article.

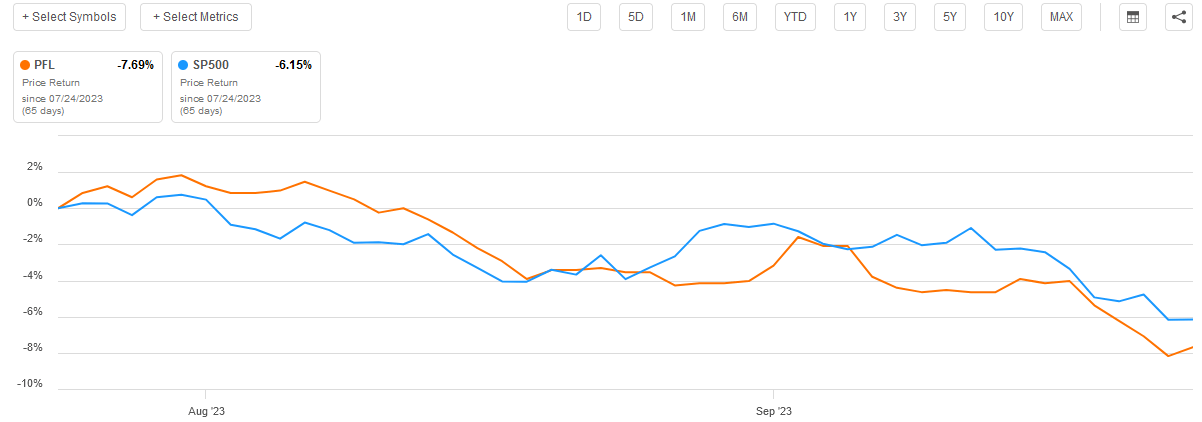

As regular readers may recall, we last discussed the PIMCO Income Strategy Fund on July 24, 2023. The fund's performance since that time has been nothing sort of dismal. As we can see here, the fund's shares have fallen by 7.69%, which is actually worse than the price performance of the S&P 500 Index (SP500):

{kind=link}

As fans of this fund may point out, a significant proportion of this fund's returns come from the large distribution that it pays out and I will not debate that. However, the fund's investors still lost 5.81% over the period in question when we included the effects of the distribution. That was a pretty terrible performance for two months, although that was sufficient to beat the broader market.

Unfortunately, it seems somewhat unlikely that things will improve anytime soon. Fixed-income securities in general have been suffering for the past several months as the market begins to wake up to the reality that the Federal Reserve's fight against inflation is far from over. Indeed, some analysts believe that rates will have to go much higher as we are looking at a global shortage of crude oil over the next several years that will push the prices of everything much higher. When we combine this with the very high likelihood that high Federal deficits will continue to demand capital from the markets, the only possible conclusion is that high interest rates will be with us for quite some time.

Fortunately, the price of the PIMCO Income Strategy Fund does not appear to be too bad right now. The fund is currently trading at a discount on its net asset value right now, which is a rarity for a PIMCO fund. Thus, it seems that the market might have some concerns about this fund.

About The Fund

According to the fund's website , the PIMCO Income Strategy Fund has the primary objective of providing its investors with a very high level of current income while still preserving the value of its principal. This is a very common objective for a fixed-income fund. After all, bonds will always return their face value at maturity unless the issuing entity defaults. Thus, anyone who buys a bond at issuance and holds it to maturity is guaranteed not to lose money as long as the issuer remains solvent. It is important to keep in mind that this only means that the bond investor will not lose money on a nominal basis. It is still possible to lose purchasing power over time as most bonds do not adjust for inflation. As such, it is fairly easy for a bond fund to ensure that it preserves the principal of its investors as it can just purchase a bond and hold it until maturity.

With that said PIMCO funds have a tendency to engage in a fairly significant amount of trading activity, at least for bond funds. Consider the following:

| Fund |

| Annual Turnover |

| PIMCO Access Income Fund ( PAXS ) |

| 28.00% |

| PIMCO Corporate & Income Opportunity Fund ( PTY ) |

| 35.00% |

| PIMCO Corporate & Income Strategy Fund ( PCN ) |

| 29.00% |

| PIMCO Dynamic Income Fund ( PDI ) |

| 20.00% |

| PIMCO Dynamic Income Opportunities Fund ( PDO ) |

| 17.00% |

| PIMCO Income Strategy Fund II ( PFN ) |

| 33.00% |

These values are significantly higher than the 6% or so annual turnovers that we see from other fund houses on their fixed-income funds. The PIMCO Income Strategy Fund, for its part, has an annual turnover of 35.00%, which is clearly higher than many other PIMCO bond funds. I explained why this is important in a recent article :

This could be important because it costs money to trade bonds or other assets. These costs are ultimately billed to the shareholders and create something of a challenge for management. After all, management needs to generate sufficient returns to both cover these added costs and still deliver a return that is comparable to a similar index fund. This is a task that very few management teams manage to achieve and as such most actively managed funds underperform their benchmark indices.

As we might expect, the PIMCO Income Strategy Fund's portfolio is heavily weighted toward bonds. As we can see, 176.94% of its net assets are invested in bonds, with minimal allocations to anything else:

CEF Connect

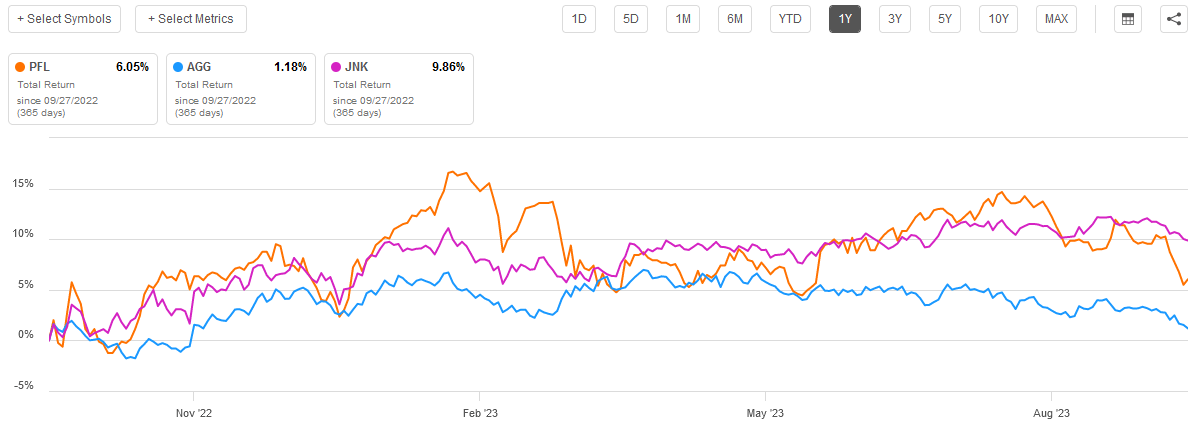

The reason that this is possible is that the PIMCO Income Strategy Fund employs leverage as a method of boosting its returns, much like all of PIMCO's other closed-end bond funds. We will discuss this in more detail later. The fact that this fund invests mostly in bonds though means that the two most relevant indices to compare it to are the Bloomberg U.S. Aggregate Bond Index ( AGG ) and the Bloomberg High Yield Very Liquid Index ( JNK ). The PIMCO Income Strategy Fund only delivered a middling performance compared to these two indices over the past year. It managed to beat the aggregate bond index, but underperformed junk bonds:

{kind=link}

Please note that the chart above shows the total return of all three assets, so it takes the distributions into account. This is important because bonds provide a significant percentage of their investment return to their owners in the form of direct payments. In fact, bonds have no net capital gains over their lifetimes, which I explained in my previous article on this fund:

A bond investor purchases a bond at face value, receives regular coupon payments that serve as income, and then receives the face value back when the bond matures. Over its lifetime, the only investment return that is delivered by the bond is the coupon payments. There are no net capital gains over time because bonds have no inherent link to the growth and prosperity of the issuing company.

As the fund invests in bonds, the same applies to it as applies to the bond indices. With that said, funds do tend to provide capital gains to their investors because they engage in bond trading to exploit price changes, as well as have no maturity dates. The best metric to use when evaluating the performance of a bond fund (or indeed anything that delivers a significant part of its investment return through dividends, distributions, or coupon payments) is total return. As we can see here, this fund pretty consistently beats the aggregate bond index, as the orange line is almost always above the blue line. However, it struggles somewhat against the junk bond index, which is probably due to its leverage.

Future Outlook

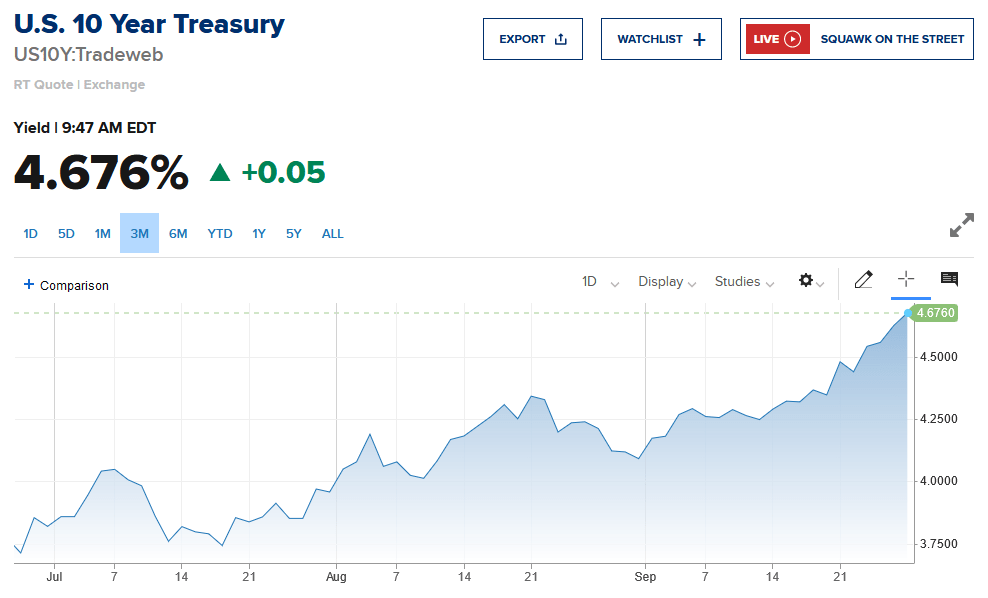

As I mentioned in the introduction, the market has started to wake up to the reality that the Federal Reserve's fight against inflation is nowhere near finished. This has dashed much of the optimism that near-term rate cuts may be on the agenda. We can see this quite clearly by looking at the ten-year U.S. Treasury yield. For most of the past year, the ten-year U.S. Treasury had a lower yield than short-term Treasuries (an inverted yield curve) because the market was expecting the Federal Reserve to cut rates. However, for the past few weeks, the yield of the de facto risk-free asset has been trending up:

{kind=link}

As we can see here, the ten-year Treasury is now at a 4.676% yield, which is the highest yield that it has had since the collapse of Lehman Brothers in 2007. The ten-year is hardly alone in its yield increase, as the two-year U.S. Treasury is now at 5.11%, which also represents a much higher yield than it has had during the current rate hike cycle:

{kind=link}

This currently indicates that the market no longer expects that rates will decline in the near future. This supports recent predictions by the Federal Reserve. As I pointed out in a recent article , the members of the Federal Open Market Committee are expecting that it will take until 2027 or later until rates get down to the 2% or lower rate that the market has become accustomed to over the past twenty years. In fact, the median prediction among Fed members is that the federal funds rate will be at 4% or higher at the end of 2025, which is well above the rate that the market was predicting earlier this year.

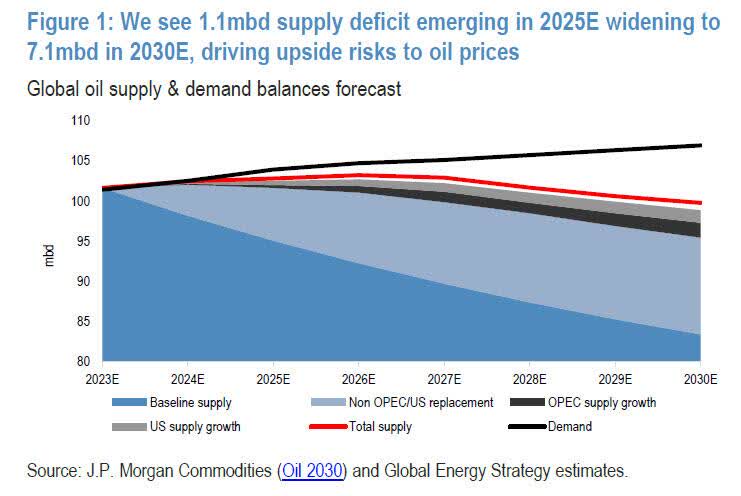

One reason for this is that inflation is not slowing down, despite the media narrative to the contrary. The most recent headline consumer price index figure showed a 3.7% year-over-year increase, which was higher than the 3.2% number in August and the 3.0% number in July. Thus, inflation is not slowing down but rather appears to be getting worse. This is because inflation never really came down. As I pointed out back in April, all the improvements that we saw in inflation came from the Federal Government selling crude oil from the Strategic Petroleum Reserve to push down energy prices. That is no longer an option as the Reserve is now at "tank bottom" and the production of crude oil is less than global demand. In fact, JP Morgan ( JPM ) is now predicting a 7.1-million-barrels per day global shortage by 2030:

{kind=link}

When we consider that crude oil is an input into pretty much everything that we purchase, it is hard to see how the inflation fight can be declared over in such an environment. As such, interest rates will probably remain a lot higher going forward than the market still thinks.

Eventually, the bond market will adapt to a world in which interest rates will be higher than we have become accustomed to. After all, today's federal funds rate is not particularly high by the standards of any period prior to 2001. However, bonds will probably be a pretty painful place to have your money until then.

Leverage

As mentioned earlier in this article, the PIMCO Income Strategy Fund employs leverage as a means of boosting its effective yield and returns. I explained how this works in my previous article on this fund:

In short, the fund will borrow money and then use that borrowed money to purchase bonds and other debt securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case. With that said though, the beneficial effects of leverage are not as great today as they were two years ago when interest rates were at 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not taking on too much leverage because that would expose us to too much risk. I generally do not like to see any fund have leverage exceeding a third as a percentage of its assets for that reason.

As of the time of writing, the PIMCO Income Strategy Fund has leveraged assets comprising 26.13% of its portfolio. This is a considerably lower leverage than the fund had the last time that we discussed it, which is quite nice to see. This reduction in the fund's leverage could be a sign that the fund is trying to be a bit more cautious with respect to the market right now, which is probably a very good idea for the reasons that we just discussed. As such, the balance between risk and reward seems reasonable here.

Distribution Analysis

As mentioned earlier, the PIMCO Income Strategy Fund has the primary objective of providing its investors with a very high level of current income. In pursuance of this objective, the fund has assembled a portfolio of bonds that deliver the majority of their investment returns in the form of direct payments made to investors. As the yield on most bonds is considerably higher than the yield on even traditionally high-yielding stocks like utilities and real estate investment trusts, we can assume that the fund's portfolio provides it with a reasonably high level of income. However, this fund goes one step further and applies a layer of leverage to boost its effective yield well beyond that of any of the underlying assets. The fund collects all of the payments made by these bonds along with any profits that it manages to make from trading bonds prior to maturity and pays them out to its shareholders, net of any expenses. As such, we might expect that this fund will be able to pay out a high yield to its shareholders.

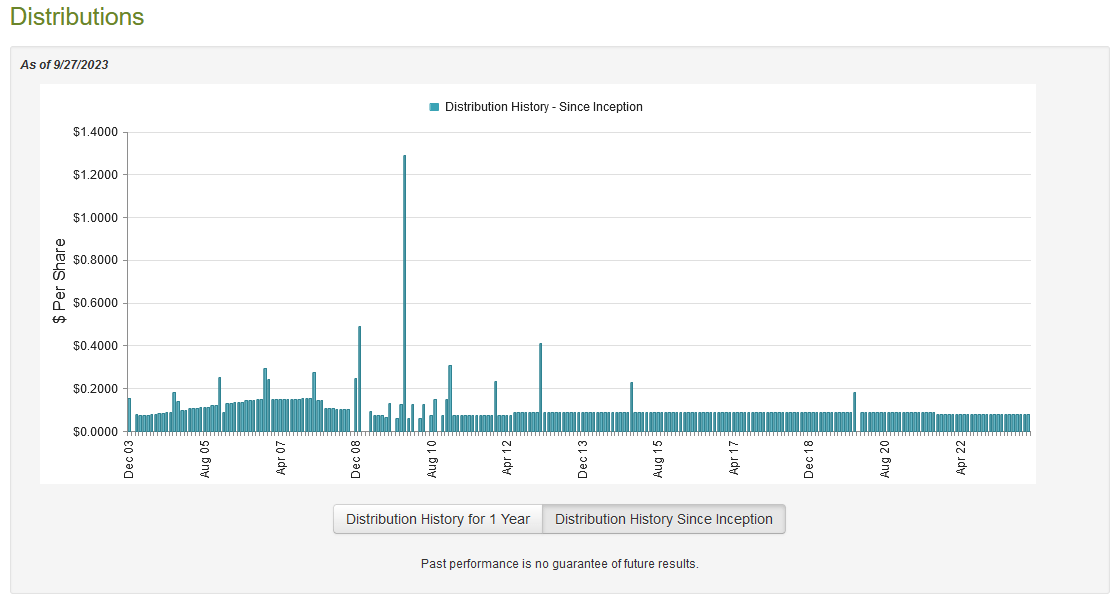

This is certainly the case as the PIMCO Income Strategy Fund currently pays a monthly distribution of $0.0814 per share ($0.9768 per share annually), which gives it a 12.92% yield at the current price. The fund has been more consistent with respect to its distribution over time than most other fixed-income funds, but it has certainly not been perfect as the distribution has varied over time:

{kind=link}

As we can see, the fund has been reasonably consistent with respect to its distribution over the past ten years, as it only cut the payout once and has otherwise never changed it. Thus, overall, it might be appealing to those investors who are seeking a safe and secure source of income to use to pay their bills or finance their investments despite not having a perfect track record. However, this consistency also raises some questions. In particular, how is this fund able to maintain such a stable distribution when its peers have been unable to achieve the same thing? As such, we want to investigate the fund's distribution in order to determine how sustainable it is likely to be.

Fortunately, we have a very recent document that we can consult for this purpose. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on June 30, 2023. This is a much newer report than the one that we had available to us the last time that we discussed this fund. That is very nice to see as this report should give us a good idea of how well the fund was able to take advantage of the optimistic conditions that existed in the market over the first half of the year. After all, the market widely expected that the Federal Reserve would quickly cut interest rates and so was driving up bond prices and generally pricing them in line with these expectations. The aggregate bond index bounced in January and remained strong for a few months, which could have given the fund some opportunities to sell bonds into the market for a profit.

During the full-year period, the PIMCO Income Strategy Fund received $40.115 million in interest and $328,000 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund reported a total investment income of $40.471 million during the period. It paid its expenses out of this amount, which left it with $31.979 million available for shareholders. This was, unfortunately, not enough to cover the $36.222 million that the fund actually paid out in distributions during the period. At first glance, this is likely to be quite concerning, as we normally would like to see a fixed-income fund fully pay its distributions out of net investment income.

Fortunately, the fund does have other methods through which it can obtain the money that it needs to pay its distributions. For example, the fund might have been able to sell appreciating bonds into an overly optimistic market during the first half of this year. Unfortunately, it generally failed at this task as it reported net realized losses of $7.689 million and had another $9.012 million in net unrealized losses.

Overall, this fund failed to cover its distributions out of its investment profits. The fund issued new shares in the market and raised $19.502 million, but even this was not enough to offset the losses on the portfolio.

The fund's net assets declined by $1.265 million over the full-year period after accounting for all inflows and outflows. When we consider that the newly issued shares will also receive the distribution, it is difficult to see how this fund can sustain its distribution in a bear market for bonds.

Valuation

As of September 27, 2023 (the most recent date for which data is available as of the time of writing), the PIMCO Income Strategy Fund has a net asset value of $7.58 per share but the shares currently trade for $7.56 each. This gives the fund's shares a 0.26% discount on net asset value at the current price. This is much better than the 3.29% premium that the shares have had on average over the past month. Honestly, this is an incredibly cheap price for any PIMCO fund as offerings from this fund house almost always trade at a premium. As such, the current price is certainly a reasonable entry point for this fund.

Conclusion

In conclusion, the PIMCO Income Strategy Fund is a reasonably decent way for an investor to earn a high level of income from their portfolio. There are some risks, though, as bonds have a reasonably high probability of being in a bear market that lasts for quite some time. As such, it might be best to stay on the sidelines until conditions improve. While things will eventually sort themselves out, bonds will probably decline until inflation really is under control and that seems very unlikely to happen in the near future given the importance of energy as an input for pretty much everything else. The fund is straining to maintain its distribution already and it seems unlikely that it will be able to sustain it indefinitely at the current level.

For further details see:

PFL: Good Bond CEF But Bond Bear Market Is A Big Risk