PAXS - PFN: Best To Buy On Dips

2023-10-10 14:22:12 ET

Summary

- PIMCO Income Strategy Fund II offers a high yield of 12.90%, but this may indicate a potential distribution cut in the future.

- The PFN closed-end fund's performance has been lackluster, with a decline of 4.71% since July. Investors also lost money even after considering the distribution.

- The fund has taken steps to reduce the risk of default losses and has the flexibility to switch between floating-rate and fixed-rate debt securities.

- The forward trajectory of interest rates is difficult to determine right now, which makes the fund's ability to alter its interest rate risk quite useful.

- The fund failed to cover its distribution over the past year and is currently trading at a more expensive price than normal.

PIMCO Income Strategy Fund II (PFN) is a closed-end fund, or CEF, that has proven to be very popular among investors who are seeking to earn a high level of income from the assets in their portfolios. The fund proves its worth in that task fairly admirably, as it currently boasts a 12.90% yield. Unfortunately, as I have pointed out numerous times in the past, any time a fund achieves a yield that is this high, it tends to be a sign that the market expects that the fund may have to cut its distribution in the near future. However, the fund’s current yield is relatively in line with that of other PIMCO closed-end funds:

| Fund |

| Current Yield |

| PIMCO Income Strategy Fund II |

| 12.90% |

| PIMCO Access Income Fund (PAXS) |

| 13.01% |

| PIMCO Corporate & Income Opportunity Fund (PTY) |

| 11.43% |

| PIMCO Corporate & Income Strategy Fund (PCN) |

| 11.79% |

| PIMCO Dynamic Income Fund (PDI) |

| 15.55% |

The fund’s yield is also not completely out of line with that of fixed-income funds from various other fund houses. As such, it may not be as threatened as we would ordinarily think based on the yield. After all, the yield of just about everything has increased significantly over the past year or two as a direct result of the policies of the Federal Reserve.

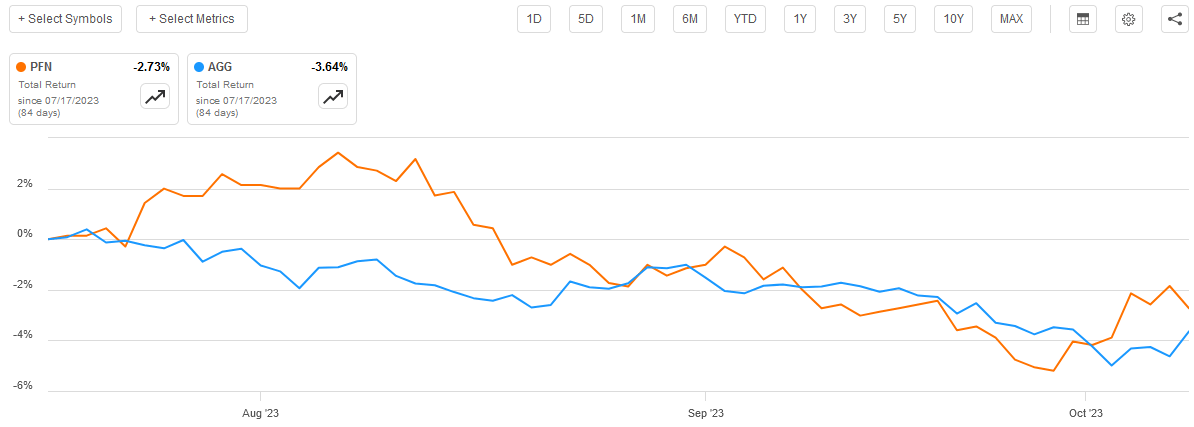

As regular readers may recall, we last discussed this fund back in the middle of July. It has, unfortunately, not delivered a particularly impressive return since that time. As we can see here, the shares of the fund declined by 4.71% over the period, which was a bit worse than the decline of the overall domestic bond market (AGG):

{kind=link}

However, in the case of this CEF, its high yield saves it somewhat. While investors in this fund still lost money during the period, the distributions that it paid out offset some of the declines. As such, investors who purchased the fund on the date of my last article have only lost 2.73% of their money compared to a 3.64% loss for those investors who invested in a broad-market bond index fund:

{kind=link}

This is certainly not a performance to write home about and, as we will see in this article, there is little reason to expect that things will improve in the near future. However, there are some signs that the worst may be behind us as most members of the Federal Open Market Committee expect that they will be able to cut interest rates slightly by the end of next year. That will benefit bond funds such as the PIMCO Income Strategy Fund II, but it is still a year away and a lot of things can happen in a year.

About The Fund

According to the fund’s webpage , the PIMCO Income Strategy Fund II seeks to provide its investors with a very high level of current income while still ensuring the preservation of capital. This is a very common strategy for a bond fund, as bond investors who are willing to hold their assets until maturity are guaranteed not to lose money unless they are foolish enough to purchase a bond when it has a negative yield-to-maturity.

The exception to this rule is if the issuing entity defaults, but such events are fairly rare. This has certainly been the case during the “easy money” era that persisted over most of the past fifteen years. In fact, it was so easy to get money and avoid defaults that we saw a large number of companies that were unable to generate sufficient cash to pay the principal on their debt, although they were able to pay the interest expenses. Goldman Sachs estimated back in 2021 that about 13% of U.S. public companies were in this category.

These companies are naturally at risk of default now that higher interest rates will force their interest expenses up when they roll over their debt. As a result, we could see an increase in defaults in the near future that could result in investors in bond funds such as this one taking some losses.

Fortunately, the PIMCO Income Strategy Fund has taken some steps to reduce the risk that it will suffer from severe losses in the event of rising default rates. The fund primarily seeks to achieve this through diversification. It currently holds bonds from 433 unique issuers, which should ensure that its exposure to any individual company is limited.

Unfortunately, the fund does not make it easy to determine the weighting of the largest assets that it holds. There is no top holdings list provided either on the webpage or in the fund’s fact sheet . However, with 433 issuers represented in the fund, it is hard to believe that anything accounts for more than 2% or so, and indeed I cannot find anything in the annual report that stands out as an outsized bond position. As such, we can conclude that the fund’s losses due to a default by one of the issuers whose securities are in the portfolio are likely to be small enough that investors will not really notice.

As I have noted in various past articles, one of the biggest factors that influences bond prices is interest rates. This is unlikely to be a surprise to anyone, as it has been the reason why bonds were in a massive bull market from the 1980s until today, as the Federal Reserve was steadily reducing rates from the double-digit levels that they had in the early 1980s until just recently:

{kind=link}

Last year, we saw the reverse happen as the central bank started rapidly raising interest rates in order to combat the incredibly high level of inflation that has been dominant in the American economy. As of the time of writing, the effective federal funds rate is 5.33%, which is a 525-basis point increase over the 0.08% level that it had in February 2022. This represents one of the most rapid interest rate increases in history, and it is the primary factor that pushed bond prices down over the period. I explained why this is the case in my previous article on this fund:

This has naturally pushed down the price of bonds. This is because newly-issued bonds have an interest rate that corresponds to the federal funds rate. Thus, a brand-new bond will have a higher yield than any bond that was issued in the past two decades or so. In other words, a newly-issued bond will almost certainly have a higher coupon rate than pretty much any existing bond in the market. As such, nobody will buy an existing bond when they can get an identical brand-new one with a higher yield, so the price of the existing bond has to decline to the point where it has a similar yield-to-maturity as a brand-new bond that is otherwise identical.

As mentioned in the introduction, the members of the Federal Open Market Committee, which is the organization that sets the federal funds rate, have recently stated that the Federal Reserve is unlikely to raise rates again this year and that a 25-basis point cut is likely sometime next year. This is the reason why the stock market delivered such a strong performance yesterday. However, it is unlikely that the Federal Reserve will drop rates much more than that until at least 2025. This does relieve some of the strain on bonds, as the lack of further tightening means that the worst is probably over for bonds. However, as I noted in a few recent articles, such as this one , there is a very strong case to be made right now for higher energy prices going forward. This is mostly because underinvestment in crude oil production capacity has resulted in a situation where energy producers will not be able to supply sufficient oil to satisfy global demand starting within the next year or two.

In such a scenario, energy prices will drive inflation up and it may force the Federal Reserve to raise interest rates further as it attempts to combat the resultant inflation. After all, energy is a required input in pretty much everything that we use so producers will have to raise their prices in order to cover the extra costs. Thus, we could still see more pain in the bond market than the central bank is currently predicting.

Fortunately, the PIMCO Income Strategy Fund II has a way to protect itself from the effects of rising interest rates. From the fund’s webpage:

The Fund has the flexibility to allocate assets in varying proportions among floating- and fixed-rate debt instruments, as well as among investment grade and non-investment grade securities. It may focus more heavily or exclusively on an asset class at any time, based on assessments of relative values, market conditions and other factors.

The takeaway from this quote is that the PIMCO Income Strategy Fund II can switch between floating-rate and fixed-rate debt securities. In a recent article , I pointed out that floating-rate securities do not have the same interest-rate sensitivity that ordinary fixed-rate bonds possess. This is because the coupon that is paid by the securities changes based on the prevailing interest rate in the market. As such, they will always deliver a competitive yield to other bonds in the market and their price tends to be almost perfectly stable. Thus, the fund can invest exclusively in these bonds during rising rate periods, which should allow it to outperform funds that do not have this flexibility. However, the downside to floating-rate securities is that they will typically underperform during periods in which interest rates decline. This is because the coupon payments from these securities are getting smaller in such an environment, and they do not benefit from price appreciation.

Unfortunately, the PIMCO Income Strategy Fund II does not specify the percentage of its assets that are invested in fixed-rate versus floating-rate securities so there is no way to be certain of the degree to which the fund is using these securities to reduce its interest-rate risk in the current market. The fund’s annual report states that 44.4% of the fund’s assets are invested in bank loan participations, some of which are floating-rate:

Fund Annual Report

Anything that lists an interest rate of LIBOR+XXXX or EUR003M+XXXX where XXXX is a percentage is a floating rate security. We can see these too in some of the corporate bond positions that show a T-Bill 1MO + XXXX figure for the interest rate. We can see though that these do seem to be a minority of the portfolio overall, but there are quite a few of them listed under the bank loan participations. It would be nice if the fund gave us an actual breakdown of the percentage of its portfolio that consists of floating-rate versus fixed-rate notes, however. The Apollo Tactical Income Fund (AIF) does this and it is a big help for investors that are attempting to determine their interest rate risk from a given fund.

Leverage

As is the case with most closed-end funds, the PIMCO Income Strategy Fund II employs leverage as a method of boosting the effective yield of the bonds in its portfolio. I explained how this works in my last article on the fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. With that said though, the beneficial effects of leverage are nowhere near as strong today with rates at 6% as they were early last year when rates were at 0% so the fund will not be able to boost its yield as much today as it used to be able to do.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since this would expose us to too much risk. I generally like a fund’s leverage to be less than a third as a percentage of its assets for this reason.

As of the time of writing, the PIMCO Income Strategy Fund II has levered assets comprising 29.36% of its portfolio. This is a fairly reasonable amount of leverage that is well below the one-third level that we typically like to see. As such, it appears that the fund has a reasonable balance between risk and reward. This is reinforced by the fact that this fund’s leverage is considerably less than some of the other fixed-income closed-end funds that we have discussed in recent weeks, and it seems likely that it will probably not suffer more outsized losses, although I am hesitant to truly predict that interest rates have peaked. Overall, though, we probably do not really need to worry too much about this fund’s leverage right now.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the PIMCO Income Strategy Fund II is to provide its investors with a very high level of current income. In pursuance of this objective, the fund invests in a portfolio of both investment-grade and junk bonds and then applies a layer of leverage to boost the effective yield of the portfolio. When we consider that bonds of all types have much higher yields than most of us are accustomed to, and the effects of the leverage, we can assume that this fund is probably generating a fairly high yield from its strategy. It collects all of the money that it receives from the assets in the portfolio, as well as any capital gains that it manages to achieve by trading bonds whenever interest rates change, and pays it out to the shareholders, net of the fund’s own expenses. As such, we can probably assume that this will result in the fund boasting a very high effective yield.

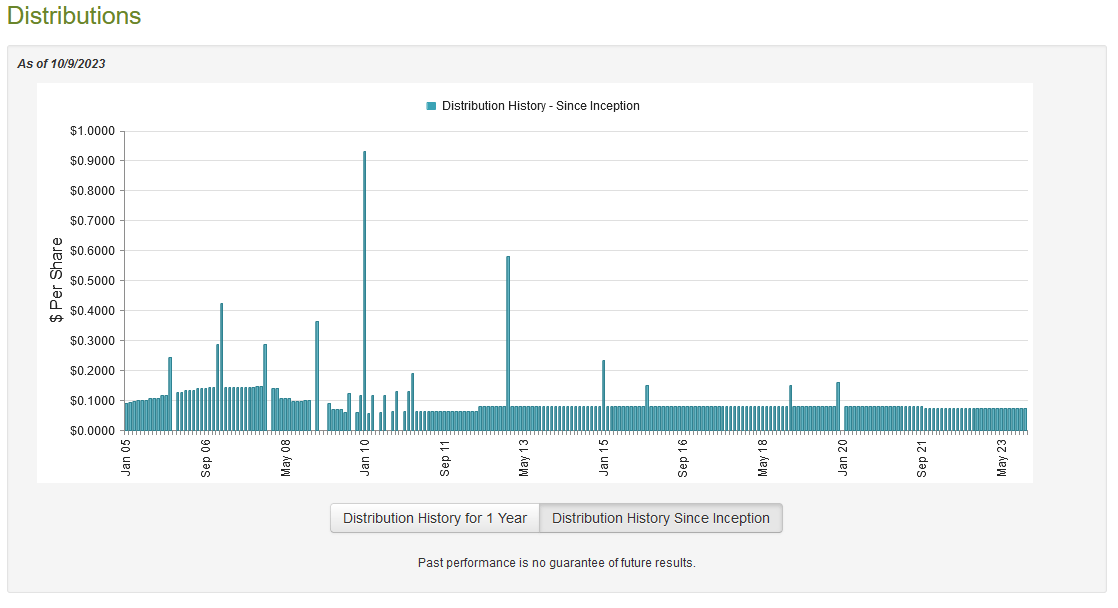

That is certainly the case as the PIMCO Income Strategy Fund II currently pays a monthly distribution of $0.0718 per share ($0.8616 per share annually), which gives it a whopping 12.90% yield at the current price. Unlike most fixed-income funds, this one has been remarkably consistent with its distribution over the years:

{kind=link}

One thing that regular readers will likely recall is that many of the fixed-income closed-end funds that we have discussed have changed their distributions fairly often over the years. These changes tend to correlate with interest rates, which makes sense considering that interest rates have an outsized impact on the returns provided by bonds. The PIMCO Income Strategy Fund II has proven to be much more stable with respect to its distribution, although it has not been perfect. This will probably make the fund rather appealing to those investors who are seeking a safe and consistent source of income to use to pay their bills or finance their lifestyle. However, it does mean that we need to take a very close look at the fund’s finances, as it seems odd that this fund has been able to accomplish a task that its peers have not.

Fortunately, we do have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report is the full-year report for the period that ended on June 30, 2023. This report was linked to earlier in this article. This is a much newer report than the one that we had available to us the last time that we discussed this fund, which is nice as it should give us a good idea of how well the fund was able to take advantage of the incredibly optimistic market that existed during the first half of this year. After all, investors were wildly optimistic that the Federal Reserve would quickly pivot and cut rates, and they were bidding down bond yields and driving up prices. This environment could have allowed for some opportunistic trading on the fund’s part.

During the full-year period, the PIMCO Income Strategy Fund II received $76.457 million in interest along with $603,000 in dividends from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $77.126 million during the period. It paid its expenses out of this amount, which left it with $62.080 million available to shareholders. Unfortunately, this was not nearly enough to cover the $70.331 million that the fund actually paid out during the period. This is concerning because we usually like a fixed-income fund to be able to completely fund its distribution out of net investment income.

However, there are other methods through which the fund can obtain the money that it needs to cover the distribution. For example, it might have been able to take advantage of rising bond prices at certain points during the first half of the year to conduct opportunistic asset sales. Unfortunately, the fund failed miserably at this task. It reported net realized losses of $19.897 million and had another $10.669 million net unrealized losses. Overall, the fund’s net assets declined by $4.675 million after accounting for all inflows and outflows during the period.

Obviously, the fund failed to cover the distributions that it paid out during the full-year period. However, the actual decline in the fund’s net assets was not as large as we might have expected. This is because the fund conducted a capital raise during the year that brought in $33.369 million of new money from investors. It also brought in another $7.385 million from shareholders who were reinvesting their distributions. Despite this, the fund’s net assets still declined. This is not sustainable over any sort of extended period, so we need to keep a very close eye on this fund to ensure that it manages to correct this problem, or it will almost certainly have to cut its distribution.

Valuation

As of October 9, 2023 (the most recent date for which data is currently available), the PIMCO Income Strategy Fund II has a net asset value of $6.59 per share but the shares currently trade for $6.70 each. This gives the fund’s shares a 1.67% premium at the current level. This is a very small premium for a PIMCO fund, but it is incredibly expensive for this fund. The PIMCO Income Strategy Fund II is one of the few PIMCO funds that tend to trade at a discount, and the fund had a 1.35% discount on average over the past month. As such, it may be best to wait for the fund’s price to decline somewhat before purchasing shares.

Conclusion

In conclusion, there are still considerable risks for bond funds despite some recent dovish rhetoric from a few officials at the Federal Reserve. In particular, the inflation problem is far from being solved and the Federal Government’s demand for money is forcing rates up due to the inability of the private sector to keep up. However, it does seem that the worst is behind us, and this fund has some ways that it can protect itself against unfavorable swings in interest rates.

The biggest problem here is that PIMCO Income Strategy Fund II failed to cover its distribution over the past year, which is a problem that it will need to correct in the very near future. In addition, the shares look rather expensive compared to their typical price. It might be best to wait and buy on dips so that you can at least get the fund at a discount.

For further details see:

PFN: Best To Buy On Dips