PFN - PFN: Earn Income With This CEF

2023-07-17 19:00:34 ET

Summary

- Investors today are desperate for any source of income as the cost of living continues to increase at a very rapid pace.

- PIMCO Income Strategy Fund II invests in a portfolio of bonds with the goal of providing its shareholders with a very high level of income.

- The market is expecting that the Fed will cut rates next year, and it will have a devastating effect on this fund if that does not happen.

- The PFN closed-end fund pays a 12.14% yield that is actually covered by net investment income and net realized gains.

- The fund is trading at a slight premium to the net asset value, so unfortunately the price could be better.

There can be little doubt that one of the biggest problems facing the average investor today is the rapidly-rising cost of living. This is evidenced by the consumer price index, which claims to measure the price of a basket of goods that is regularly purchased by the average person. As we can see here, the consumer price index has increased at a rate that exceeds the 2% year-over-year growth rate that is generally considered healthy for the economy:

{kind=link}

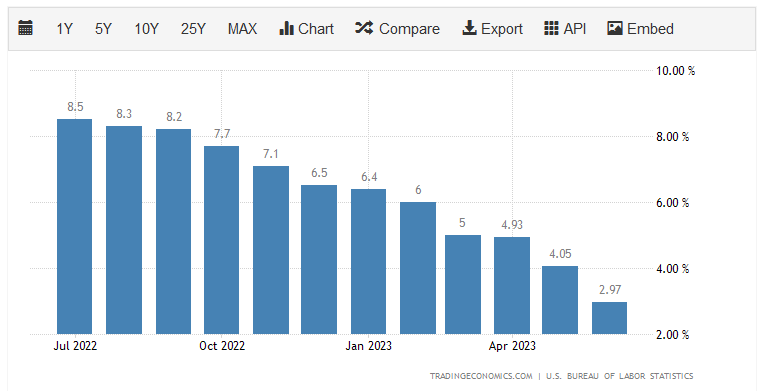

We can see that inflation has come down somewhat in recent months, which has the appearance of reducing the pressure on the average person. However, there are two flaws with this idea. The first of which is that inflation compounds so the recent 2.97% increase came on top of the 9.1% increase last year. This has the effect of increasing prices much more rapidly over a multi-year period than would be expected, just like we experience with our portfolios.

The second problem is that the majority of this improvement in the reported inflation rate is because energy prices are lower than last year. When we look at the core consumer price index , which excludes volatile food and energy prices, we see a very different story from the official narrative. I discussed this in a recent blog post . This has caused many consumers to resort to extreme measures in order to maintain their standard of living, including dumpster diving and pawning their possessions (see here ). The takeaway here is that the average American is in desperate need of additional sources of income.

As investors, we are certainly not immune to this. After all, we need food, fuel, and occasional luxuries just like anyone else. Fortunately, we do not need to resort to such extreme measures to obtain the extra money that is needed to survive in today's world. This is because we have the ability to put our assets to work for us to generate an income. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in income. These funds are unfortunately not very well-followed in the financial media and many investment advisors are unfamiliar with them so it can be difficult to obtain the information that we would really like to have to make an informed investment decision. This is unfortunate because these funds have a number of advantages over familiar open-ended and exchange-traded funds. In particular, a closed-end fund has the ability to employ certain strategies that have the effect of boosting their yields well beyond that of any of the underlying assets or indeed just about anything else in the market.

In this article, we will discuss the PIMCO Income Strategy Fund II ( PFN ), which currently boasts an impressive 12.14% yield. That is clearly enough to attract any income-focused investor to its shares. Unfortunately, whenever a fund obtains such a high yield, it is frequently a sign that the market expects a near-term distribution cut so we will want to investigate that. I have discussed this fund before, but several months have passed since that time so naturally a few things have changed. This article will focus specifically on these changes as well as provide an updated analysis of the fund's financial performance. Let us investigate and see if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the PIMCO Income Strategy Fund II has the objective of providing its investors with a high level of current income while still ensuring the preservation of capital. This is not particularly surprising considering that this is a PIMCO fund, and PIMCO is well known for its bond funds. This one is no exception, as the fund's portfolio is almost entirely invested in bonds, with only a small amount of exposure to both American and foreign equities:

Morningstar

The reason that the fund's objective is not surprising in this light is that bonds by their nature deliver all of their investment returns to their holders in the form of direct payments. After all, an investor will purchase a bond for its face value when it is first issued. The bond then makes a regular coupon payment to its holder over its lifetime and is redeemed at maturity for face value. Thus, the bond has no net capital gains over its lifetime and its entire investment return simply consists of the coupon payments that the bond pays out. This is due to the simple fact that a bond has no inherent link to the growth and prosperity of the issuing company.

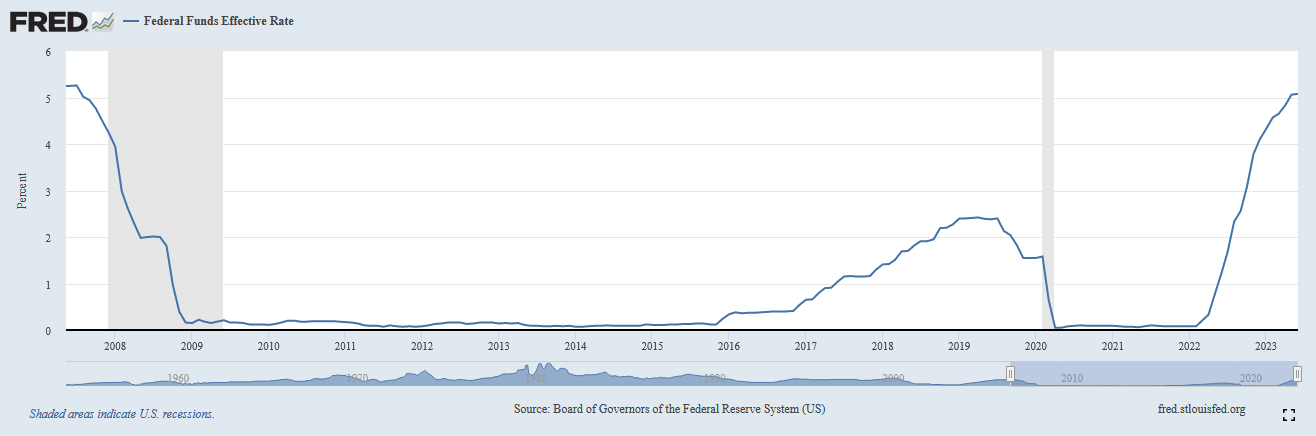

With that said, bonds do offer the potential for profiting from price swings by trading them prior to maturity. This comes from the fact that bond prices vary with interest rates. It is an inverse relationship, so when interest rates go up, bond prices drop. As everyone reading this is certainly well aware, the Federal Reserve has been very aggressively raising interest rates in an attempt to combat the high inflation that has been plaguing the economy. We can see this quite clearly by looking at the federal funds rate, which is the rate at which the nation's commercial banks lend money to one another on an overnight basis. As we can see, this rate has skyrocketed and is now at the highest level that we have seen since 2007:

{kind=link}

As of the time of writing, the effective federal funds rate is 5.08%. This is the highest that it has been since the 5.26% rate that was witnessed in July of 2007. Curiously, I can recall how everyone back then was complaining about how the "low-interest rate environment" led to the financial crisis. Today, all I hear is commentators calling today's rate "high" despite the fact that this same rate was deemed low sixteen years ago. Regardless, the current rate is a very steep increase from the 0.08% effective federal funds rate of February 2022.

This has naturally pushed down the price of bonds. This is because newly-issued bonds have an interest rate that corresponds to the federal funds rate. Thus, a brand-new bond will have a higher yield than any bond that was issued in the past decade-and-a-half. In other words, a brand-new bond will almost certainly have a higher coupon rate than pretty much any existing bond in the market. As such, nobody will buy an existing bond when they can get an identical brand-new one with a higher yield so the price of the existing bond has to decline to the point where it has a similar yield-to-maturity as a brand-new bond that is otherwise identical.

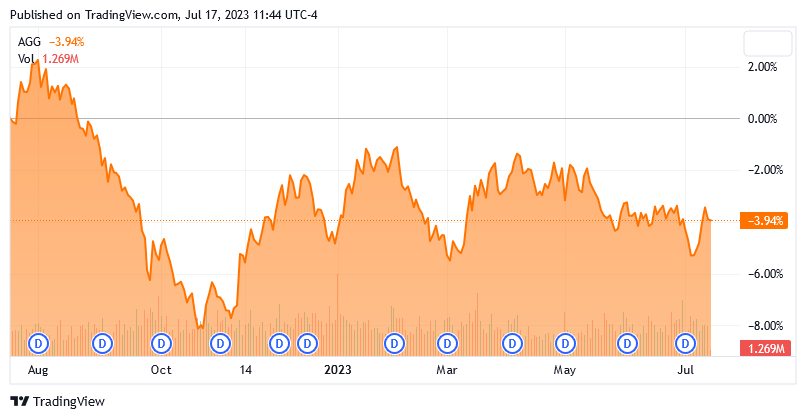

We can see this effect quite clearly by looking at the Bloomberg U.S. Aggregate Bond Index ( AGG ), which is down 3.94% over the past twelve months:

{kind=link}

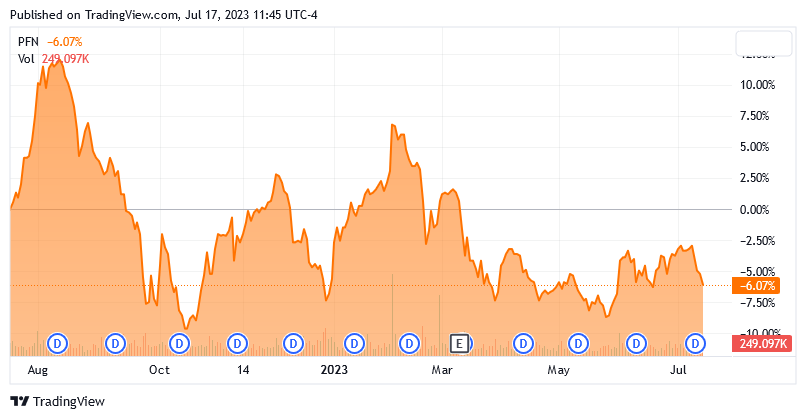

The PIMCO Income Strategy Fund II has fared no better, as it is down 6.07% compared to a year ago:

{kind=link}

With that said, though, the PIMCO fund did manage to deliver a positive return over the period due to the fact that its yield is so high. As of July 14, 2023 (the most recent date for which data is currently available as of the time of writing), the PIMCO Income Strategy Fund II delivered a 6.77% total return over the past twelve months:

{kind=link}

Please note that in order to actually achieve this return, an investor will have needed to reinvest all of the fund's distributions. This sort of defeats our thesis of using this fund as a way to get extra income to cover our regular expenses. However, it will always be the case that reinvesting dividends or distributions will result in more money overall due to the distributions compounding and earning more money. However, it is still true that someone that went and spent all of the distributions ended up getting more money in distributions than they lost from the share price decline. Thus, everyone that held this fund for the full trailing twelve-month period came out ahead. That is much better than we can say for many other funds, including most bond funds.

The biggest question for investors considering this fund today is where interest rates will be going from here on out. The Federal Reserve may have paused on rate hikes for June, but it still expects that there will be two more before the end of the year. The market right now appears to agree with analysts that the Federal Reserve will then begin cutting rates over the course of 2024, albeit slower than it increases them. The median estimate is that the federal funds rate will be at 3.60% at the end of 2024. However, there is a very real risk of reigniting inflation if this is done.

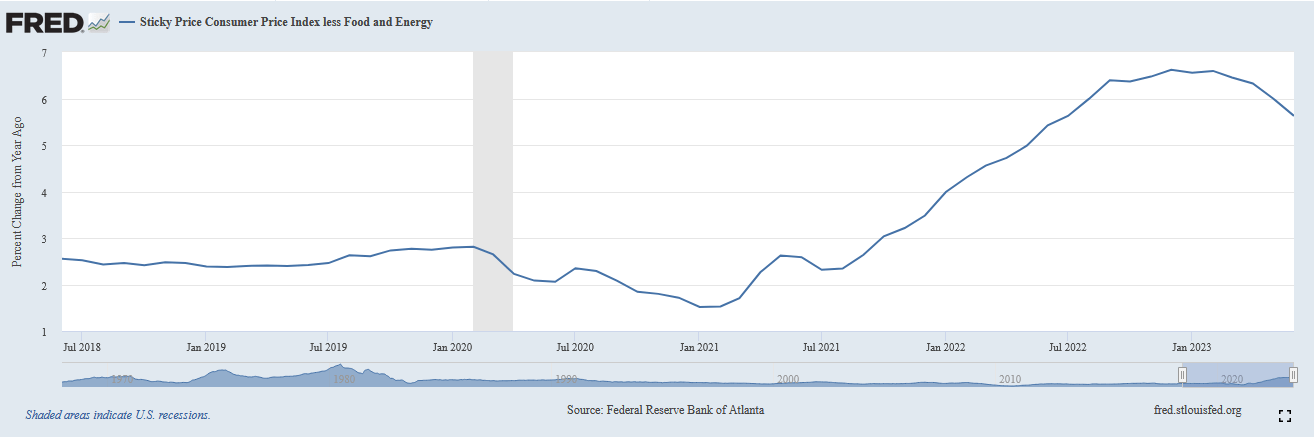

As mentioned in the introduction to this article, the biggest reason for the improvements in the headline inflation number has been the fact that energy prices are lower than a year ago. This is evident in the fact that other measurements of inflation that exclude energy prices are tracking well over 5% year-over-year even today. For example, the sticky price consumer price index showed an increase of 5.63% year-over-year in June:

{kind=link}

Thus, an increase in energy prices would almost certainly reignite the headline inflation numbers and undo all of the so-called "progress" that the Federal Reserve has made in the fight against inflation. We are already seeing the balance between supply and demand in the global oil market begin to tighten and OPEC+ appears willing to keep cutting production until oil is back over $100 per barrel. Such an event would start pushing the inflation numbers up again and ensure that the market is wrong about rate cuts in 2024. As the bond market is currently pricing in these cuts, it would have a devastating effect on the bond market if the Federal Reserve does not cut rates. The PIMCO Income Strategy Fund would be affected as well, and would see its share price drop accordingly.

In my last article on the PIMCO Income Strategy Fund II, I mentioned that the fund heavily invests in below-investment-grade securities. These are what are colloquially known as "junk bonds," and they are quite commonly held by closed-end funds due to the fact that their yields tend to be much higher than the yield of investment-grade securities. This was a very big deal in years past due to the fact that investment-grade bonds were yielding next to nothing. It is still the case today that the fund heavily invests in these securities, as we can see by looking at the credit quality of the bonds that comprise its portfolio:

Morningstar

A speculative-grade security is anything rated BB or lower. As we can see, that represents 40.02% of the portfolio. This is much lower than the percentage of the portfolio that consisted of junk bonds the last time that we discussed it. It is not necessarily surprising that this is the case as the interest rates on investment-grade securities are much higher than they were only a few months ago. In fact, as of the time of writing, the Bloomberg U.S. Aggregate Bond Index yields 2.83% compared to a 5.67% yield of the Markit iBoxx USD Liquid High Yield Index ( HYT ) so the difference between speculative-grade securities and investment-grade securities is not as great as it once was. As such, there is less reason to favor speculative-grade securities when seeking out a high level of income.

The fact that the fund's allocation to junk bonds went from 71.14% to 40.02% over the course of a few months could lead one to expect that this fund has a very high annual turnover. In fact, the fund reported a 45.00% annual turnover in its most recent annual report. This is higher than many fixed-income funds, but it is not especially high among the entire closed-end fund universe. The reason that this matters is that it costs money to trade bonds or other assets, and these expenses are billed directly to the fund's shareholders. This creates a drag on the portfolio's performance and makes management's job much more difficult. After all, the fund's managers need to generate sufficient returns to cover these extra expenses and still have enough left over to satisfy the shareholders. That is something that very few management teams manage to accomplish on a consistent basis, and thus it contributes to the fact that most actively-managed funds end up underperforming their benchmark indices.

This fund is a notable exception to that, as it has substantially outperformed the Bloomberg U.S. Aggregate Bond Index during just about any period that one cares to mention. Here is the index's performance history over time:

{kind=link}

Now compare that to the performance history of the PIMCO Income Strategy Fund II over the same time period:

{kind=link}

As is immediately apparent, the PIMCO fund substantially outperforms the index during every multi-year period in question. While past performance is no guarantee of future results, it appears that PIMCO's management team has a very strong track record of meeting their performance goals. This probably explains why the fund is very popular among fixed-income investors as it seems likely that management will be able to continue to beat the index going forward.

Leverage

In the introduction to this article, I stated that closed-end funds like the PIMCO Income Strategy Fund II have the ability to employ certain strategies that can boost their effective yields beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. With that said though, the beneficial effects of leverage are nowhere near as strong today with rates at 5% as they were early last year when rates were at 0% so the fund will not be able to boost its yield as much today as it used to be able to do.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since this would expose us to too much risk. I generally like a fund's leverage to be less than a third as a percentage of its assets for this reason. Fortunately, this fund appears to meet this requirement. As of the time of writing, the fund's levered assets comprise 28.78% of the overall portfolio:

Morningstar

Thus, it appears that the fund is striking a reasonable balance between risk and reward. It does not appear that we have anything to worry about here.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the PIMCO Income Strategy Fund II is to provide its investors with a high level of current income. In order to achieve this goal, the fund invests in a portfolio of bonds and similar assets that boast fairly respectable yields. It then applies a layer of leverage to boost these yields well above those of any of the underlying assets. The fund then pays out its income to the shareholders via distributions. As such, we might assume that this fund would boast a very high yield itself. That is certainly the case as the PIMCO Income Strategy Fund II pays a monthly distribution of $0.0718 per share ($0.8616 per share annually), which gives it a 12.14% yield at the current price. The fund has generally been consistent with its distributions over the years, although there have been a few variations:

{kind=link}

In particular, we see that the fund cut its distribution from $0.08 per share monthly to $0.0718 per share monthly back in 2021. This is not exactly unexpected though since the distributions of most fixed-income closed-end funds tend to vary somewhat with interest rates. After all, the returns of bonds and other fixed-income securities are highly correlated with interest rates. For the most part, this fund's distribution has been much more consistent than most other closed-end funds in the same category, which may appeal to those investors that are looking for a safe and secure source of income to use to pay their bills or finance their expenses.

As is always the case, it is critical that we ensure that the fund can actually afford the distribution that it pays out. After all, we do not want to be the victims of a distribution cut since that would both reduce our incomes and almost certainly cause the fund's share price to decline. Let us investigate the fund's finances to determine how sustainable the current distribution is likely to be.

Unfortunately, we do not have an especially recent document to consult for the purposes of our analysis. As of the time of writing, the fund's most current financial report corresponds to the six-month period that ended on December 31, 2022. As such, it will not provide any insight into the fund's performance so far this year. That is quite disappointing as the bond market has been remarkably strong this year and the fund may have been able to exploit this by trading bonds for capital gains. The latest financial report should still give us a pretty good idea of how well the fund weathered the turbulent and challenging conditions in the bond market during 2022. During the six-month period, the PIMCO Income Strategy Fund II received $37.304 million in interest and $307,000 in dividends from the assets in its portfolio. This gives the fund a total investment income of $37.611 million over the period. It paid its expenses out of this amount, which left it with $30.358 million available for the shareholders. This was, unfortunately, not enough to cover the $34.497 million that the fund actually paid out in distributions to its investors, although it did get very close. At first glance, this is likely to be concerning as the fund is paying out more than its net investment income.

However, a fund like this has other methods that can be employed to obtain the money that is needed to cover the distributions. For example, the fund might be able to earn capital gains and then use that money to finance the distributions. Fortunately, the PIMCO Income Strategy Fund II did have some success at that task during the period. The fund was able to generate $14.371 million in net realized gains, although this was partially offset by $30.746 net unrealized losses.

Overall, the fund's assets declined by $6.499 million over the six-month period after we account for all inflows and outflows. The decline in the fund's asset base would have been larger had it not conducted a $12.888 million capital raise during the period. We usually like to see a fund completely cover all of its distributions and slightly increase its asset base during a given period without resorting to capital raises.

This one failed to accomplish that, but it is worth noting that the net investment income and net realized gains together were sufficient to cover the fund's distributions with money to spare. Thus, the real problem here is the net unrealized losses. We will really need to see how well the fund performed in the first half of this year to make a determination about the sustainability of its distribution, but it still did as well or better than most other fixed-income funds during one of the most challenging periods for bond markets in recent memory.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the PIMCO Income Strategy Fund II, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. This is, unfortunately, not the case with this fund today. As of July 14, 2023 (the most recent date for which data is available as of the time of writing), the PIMCO Income Strategy Fund II had a net asset value of $6.82 per share but the shares currently trade at $7.02 each.

This gives the fund's shares a 2.93% premium to the net asset value at the current price. While this is certainly better than the 4.95% premium that the shares have averaged over the past month, it is still a premium and it indicates that anyone buying today is overpaying for the fund based on the value of its assets. Thus, it might be a good idea to wait for the price to come down before buying into the fund. However, PIMCO funds almost always trade at a premium to the net asset value so it might not be possible to acquire this one at a discount for a long time.

Conclusion

In conclusion, the PIMCO Income Strategy Fund II is a very good fixed-income fund, as is the case with most funds that bear the PIMCO name. The fund has a long history of outperforming its benchmark indices, which explains its high price and apparent popularity. The biggest concern here is that the market may be wrong about the course of interest rates over the next eighteen months, which would have a devastating effect on every bond fund. That is, admittedly, not something that is a unique risk to this fund but it is worth considering before buying shares. Overall though, PIMCO Income Strategy Fund II is a very solid choice for anyone seeking a bond fund for income.

For further details see:

PFN: Earn Income With This CEF