PFO - PFO: A Near-Term Correction Is Likely (Rating Downgrade)

2024-01-19 11:27:05 ET

Summary

- Flaherty & Crumrine Preferred Income Opportunity Fund has a lower yield compared to its peers due to recent distribution cuts and high leverage.

- The PFO closed-end fund has performed well in recent months, outperforming the iShares preferred stock index fund.

- The fund's exposure to the banking sector and high leverage pose risks, and recent economic reports suggest that interest rate cuts may not be as likely as currently expected.

- The fund is poised to decline if the Federal Reserve does not cut at the March meeting, so profit-taking is probably a good idea here.

- The PFO fund's price is reasonable, and it can probably sustain the distribution, although a steep asset price decline could still be problematic.

The Flaherty & Crumrine Preferred Income Opportunity Fund ( PFO ) is a closed-end fund, or CEF, that investors can employ in order to generate a relatively high level of income from the assets in their portfolios. As is the case with many of the closed-end funds from this fund house, this one has a relatively low yield compared to many of its peers.

As of the time of writing, the fund has a 6.59% yield, which is lower than the 6.67% yield of the iShares Preferred and Income Securities ETF ( PFF ). In other words, this fund has a lower yield than an unleveraged fund that is investing in very similar assets. It is likely that this is caused by the fund’s numerous recent distribution cuts as a result of fairly large losses due to the high level of leverage employed by Flaherty & Crumrine’s preferred stock funds. That same high level of leverage has also made this fund a fairly risky way to play a cut in interest rates that may not even be coming to the degree that is currently priced into its shares.

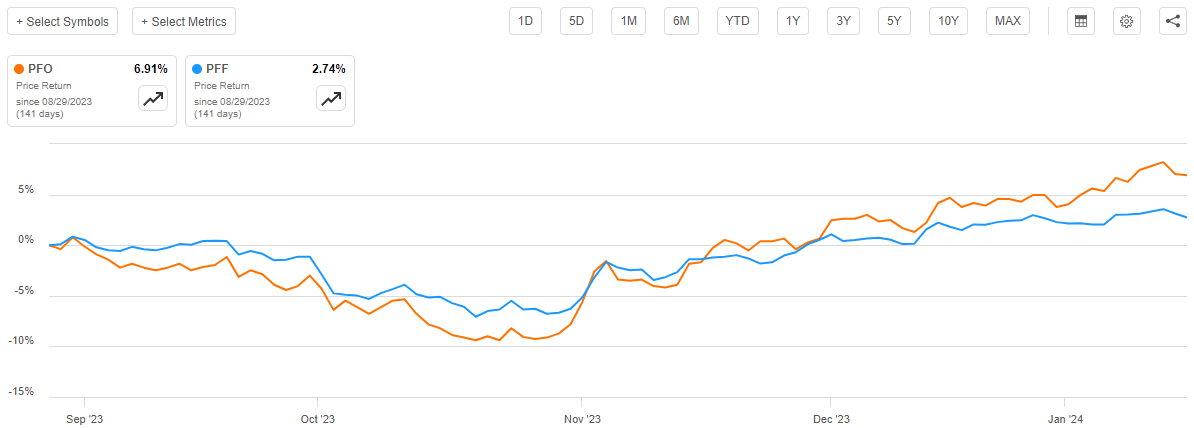

As regular readers can likely recall, we previously discussed this fund in late August 2023. The market was rather pessimistic at that time, with many market participants beginning to accept that the Federal Reserve was serious about interest rates remaining “higher for longer.” Today, many investors are optimistically expecting that interest rates will be sharply reduced in the very near future and have bid up fixed-income prices accordingly. That has naturally benefited the shares of this fund, as they are up 6.91% since the date that my previous article was published. This is substantially better than the 2.74% gain of the aforementioned preferred stock index fund:

{kind=link}

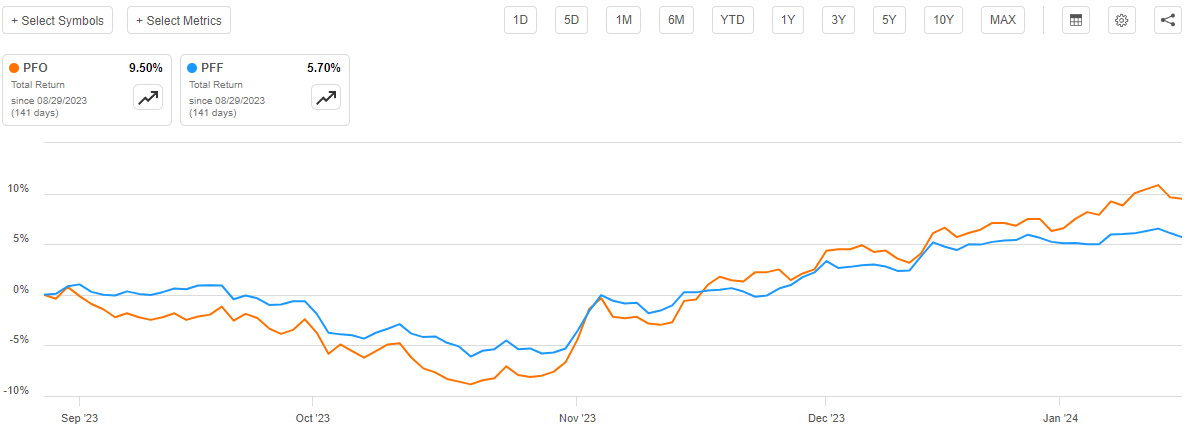

This outperformance relative to the index is exactly what we would expect from a leveraged preferred stock fund. However, both of these funds deliver a significant percentage of their investment returns in the form of direct payments to their investors. As such, it is important that we consider the distribution in our analysis as that provides a better idea of what investors actually received. When we do that, we see that investors in the Flaherty & Crumrine Preferred and Income Opportunity Fund received a 9.50% return over the past five months or so. That is much better than the 5.70% total return that investors in the preferred stock index earned:

{kind=link}

That is certainly the sort of performance that might impress any potential investor, despite the fact that this fund’s distribution yield is lower than the preferred stock index. Unfortunately, there could be some reasons to expect that the fund will soon surrender some of its gains, and in fact we have started to see that over the past few days as a slew of positive economic reports have made it clear that near-term rate cuts are unlikely and thus the pricing of the fund’s assets is too high.

About The Fund

According to the fund’s website , the Flaherty & Crumrine Preferred and Income Opportunity Fund has the primary objective of providing its investors with a very high level of current income. This makes a great deal of sense considering the fund’s strategy, which is explained on the website:

The Fund’s investment objective is to provide its investors with high current income consistent with preservation of capital.

…

Under normal market conditions, the Fund invests at least 80% of its Managed Assets in a portfolio of preferred and other income-producing securities. Preferred and other income-producing securities may include, among other things, traditional preferred stock, trust preferred securities, hybrid securities that have characteristics of both equity and debt securities, contingent capital securities, subordinated debt and senior debt. “Managed Assets” are the Fund’s net assets, plus the principal amount of loans from financial institutions or debt securities issued by the Fund, the liquidation preference of preferred stock issued by the Fund, if any, and the proceeds of any reverse repurchase agreements entered into by the Fund.

The website goes on to state that at least 25% of the fund’s assets will be invested in banks and other financial services companies. That is not unusual as most preferred stock funds are very heavily invested in that sector. We will discuss this later in this article. For now, the most important thing is that the fund’s website claims that it will invest primarily in preferred stock and similar securities. CEF Connect confirms that this is the case, although it puts the fund’s preferred stock allocation at 61.47% of the fund’s total assets:

CEF Connect

That is well below the 80% that the website would seem to imply will be invested in preferred stock. However, a closer reading of the description above reveals that the fund actually only has to invest 80% of its portfolio into preferred stock or other “income-producing assets.” Bonds certainly qualify as an income-producing asset as, like preferred stock, they deliver the bulk of their total investment return in the form of direct payments to their holders. The dividends or coupon payments thus provide income to the fund that allows it to provide current income to its shareholders. Thus, it does appear that the fund’s objective matches the portfolio.

Curiously, the fund’s third-quarter 2023 holdings report states that 77.8% of the fund’s assets are invested in preferred stock or preferred hybrid securities. This report shows the fund’s assets as of August 31, 2023, which is the same date that CEF Connect is using for its data. Thus, there appears to be a discrepancy between the two sources. It is possible that CEF Connect is actually considering anything with a maturity date as a bond, regardless of where it fits in the issuing company’s capital structure. While most preferred stocks do not mature, there are some that do have a maturity date. There is really not a significant difference between a preferred stock that matures and a bond, which could explain the discrepancy in the data sources. The holdings report provides this allocation for the fund:

| Asset Type |

| Percentage Of Portfolio |

| Preferred Stock & Hybrid Preferred Securities |

| 77.8% |

| Contingent Capital Securities |

| 17.0% |

| Corporate Debt (Bonds) |

| 2.1% |

| Money Market Funds |

| 2.1% |

Anytime there is a discrepancy between data sources, it is typically best to use the information provided by the fund’s sponsor as the authoritative data source. However, in this case, the data from CEF Connect can certainly be informative because preferred stock with a maturity date and convertible preferred securities behave a bit differently in terms of price movement than straight perpetual preferred stock. In particular, the maturity date on some preferred stock affects the duration (the sensitivity of the security to interest rates) and convertible preferred stock will have a greater correlation to the common stock of the issuing company than ordinary preferred issues. However, we can still see that the majority of the holdings in this fund should behave like ordinary preferred stock and will go up when interest rates decline and vice versa.

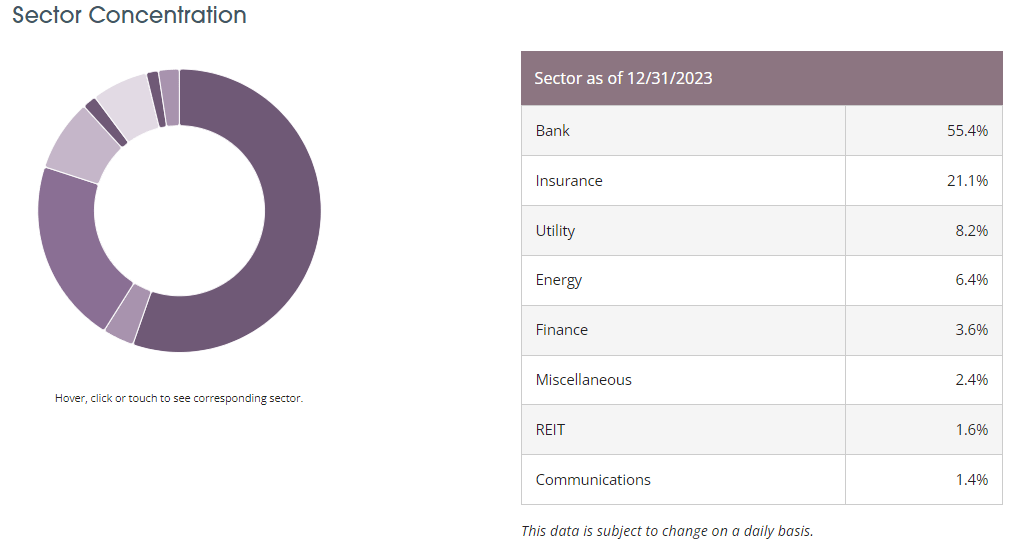

Earlier in this article, I pointed out that it is common for preferred stock funds to have a significant percentage of their assets invested in securities issued by banks or other financial institutions. The Flaherty & Crumrine Preferred and Income Opportunity Fund is certainly not an exception to this, as its own website states that it will always have at least 25% of its portfolio invested in such securities. The weighting to the financial sector is currently much higher than this, though. As we can see here, the fund currently has 55.4% of its assets invested in the banking sector and another 21.1% invested in insurance companies:

{kind=link}

This is higher than the 73.87% weighting that the preferred stock index has to the financial sector. Unfortunately, the index fund that was mentioned in the introduction does not differentiate between banks and insurance companies. Its literature only states that 73.87% of the assets are invested in “Financial Institutions.” The Flaherty & Crumrine Preferred & Income Fund has 76.5% between banks and insurance companies, so it is clearly overweight to the sector.

This is something that may concern investors, particularly because of the risks that the media has been screaming about with respect to the banking sector in today’s high interest-rate environment. At least some of these concerns may be overblown, as the banking sector’s net interest margins actually soared in 2023 on the back of high-interest rates. In fact, banks are warning that their profits would be hurt if the Federal Reserve does cut interest rates in 2024. That is very different from the usual story that we hear about banks being hurt by high-interest rates. In fact, the biggest problem that banks have when interest rates rise is that fixed-rate securities on their balance sheet fall in price, resulting in unrealized losses. That is only a problem if a bank run forces it to sell its fixed-rate loans and realize the losses, and the Federal Reserve put a program in place to prevent that problem following the collapse of Silicon Valley Bank. The only other problem that banks face comes from the fact that interest rates have been far too low over the past twenty years, resulting in consumers and businesses becoming so indebted that they cannot carry their existing debt in today’s environment. For the most part though, banks are not hurting as much in the current high interest-rate environment as the news headlines may lead one to believe. As such, there should not be a huge amount of risk from the banking sector exposure, although it is important to ensure that your portfolio is properly diversified using other assets to ensure that you do not have too much exposure to the sector.

The Rationale For The Downgrade

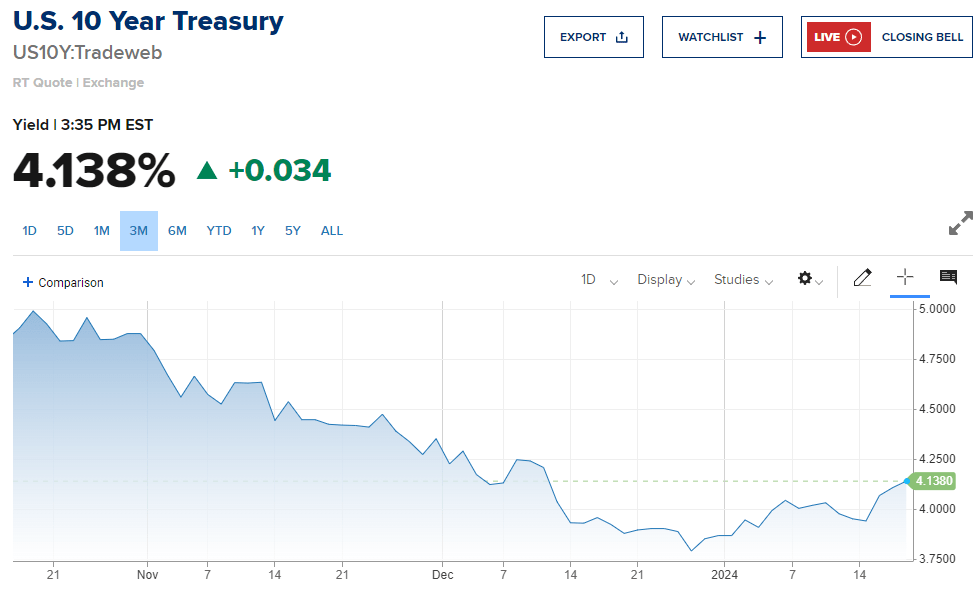

As mentioned in the introduction, the Flaherty & Crumrine Preferred and Income Opportunity Fund delivered very strong gains during the final few months of 2024. This was due to falling long-term interest rates and a general perception that the Federal Reserve would rapidly reduce interest rates in 2024. We can see this perception reflected very well in the pricing of the ten-year U.S. Treasury note. As of right now, this note is yielding 4.138% annually. This is down from the peak of 4.988% on October 19, 2023:

{kind=link}

The market is currently expecting that the Federal Reserve will cut interest rates six times in 2024, which strongly implies that the economy will enter into a severe recession within the next two or three weeks. There has only been one time in history (in the 1980s) that the central bank has cut rates by 125 basis points or more during a single year in the absence of a recession:

Zero Hedge/Data from Bloomberg

The market is currently projecting that the first rate cut this year will come at the March meeting of the Federal Open Market Committee, but that seems rather optimistic. Recent economic data has been coming in above expectations, which does not support the idea that the economy is on the cusp of a recession. In fact, most of the data shows that things have improved since October 2023, which was when the market first began to predict a near-term pivot by the Federal Reserve. Thus, the economy appears to be handling the 5.50% Federal Funds rate with a great deal of resilience and that reduces the need for near-term rate cuts.

The market appears to be waking up to this reality, which is why the ten-year U.S. Treasury rate has been inching up over the past few days. The Flaherty & Crumrine Preferred and Income Opportunity Fund is also down 1% over the past five days, so it is naturally being affected by investors beginning to digest the idea that they were wrong. However, the fund will probably keep declining for a while if the Federal Reserve does not cut interest rates in March. That is still priced into preferred stock right now, as are the six rate cuts over the course of the year.

Investors may want to unload their shares of this fund today, as the underlying securities still look overpriced. This was confirmed by Fed Governor Chris Waller at the Brookings Institution earlier this week. While he did suggest that there will be interest rate cuts this year, he suggested that they would not begin until the second half of the year. He also reinforced the idea that the Federal Reserve will cut three times, not six. That strongly suggests that this fund will suffer significant share price declines over the next few weeks.

Leverage

As stated in the introduction to this article, the Flaherty & Crumrine Preferred and Income Opportunity Fund employs leverage as a method of boosting its effective yield. I explained how this works in my previous article on this fund:

In short, the fund is borrowing money and using that borrowed money to purchase preferred stock, bonds, and other income-producing securities. As long as the yield of the purchased assets is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses.

As of the time of writing, the Flaherty & Crumrine Preferred and Income Opportunity Fund has leveraged assets comprising 39.75% of its portfolio. This is quite a bit less than the 41.13% leverage that the fund had the last time that we discussed it, but it is still considerably higher than the leverage that is possessed by similar funds. For example, the John Hancock Preferred Income Fund II ( HPF ), which we discussed a few days ago, only has 38.48% leverage at its current share price.

This fund’s very high leverage is a real risk, as it amplifies the fund’s losses and is probably a major reason why the fund cut its distribution as severely as it has over the past few years. After all, this fund’s leverage resulted in it taking much larger losses on its preferred stock portfolio than comparable funds that do not employ such high levels of leverage. This may reduce this fund’s appropriateness for risk-averse conservative investors as it is employing a high-risk, high-reward strategy.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Flaherty & Crumrine Preferred and Income Opportunity Fund is to provide its investors with a very high level of current income. In pursuance of that objective, the fund invests in a portfolio of preferred stock and other income-producing assets. As the phrase implies, these securities primarily deliver their investment return via dividend and coupon payments made to their owners. In this case, that owner is the fund that collects these payments on behalf of its own investors. This fund adds a layer of leverage to allow it to collect payments from more securities than it could using its equity capital. That should allow it to have a higher effective yield than an unleveraged fund with similar assets. The fund pools all the payments that it receives together and then distributes them to its investors after deducting its own expenses. We might expect that this would give the fund’s shares a fairly high yield.

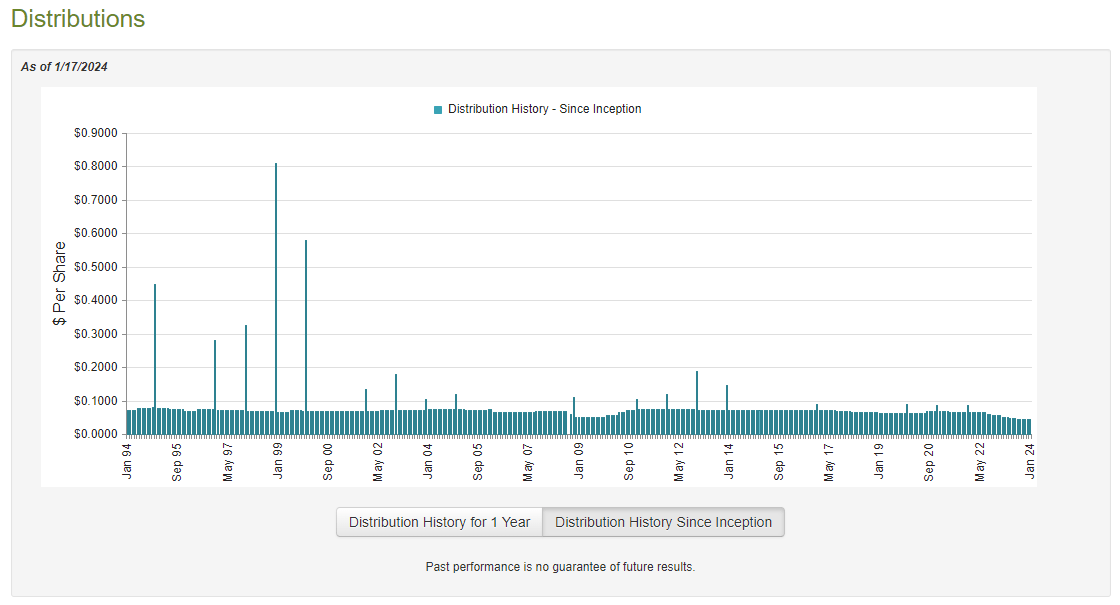

This is indeed the case, as the Flaherty & Crumrine Preferred and Income Opportunity Fund pays a monthly distribution of $0.0450 per share ($0.54 per share annually), which gives it a 6.59% yield at the current price. This is actually lower than the preferred stock index and is quite a bit lower than other preferred stock funds are able to deliver. The fund’s distribution history also leaves a lot to be desired, as it has both raised and reduced the distribution several times over its history:

{kind=link}

With that said, the fund did have a reasonably consistent track record until 2022 when it began cutting the payout numerous times as the fund’s leverage amplified its losses and forced it to take steps to preserve its net assets. That event almost certainly reduced the goodwill that this fund had previously managed to build up among income-focused investors. The distribution cuts were even more painful for those investors who are trying to support themselves from the income produced by their portfolios because inflation has caused all of us to need more income to support ourselves. The distribution cuts had exactly the opposite effect and amplified the loss of purchasing power.

As I have pointed out numerous times in the past though, the fund’s history is not necessarily the most important thing for anyone purchasing the fund today. This is because a new investor will receive the current distribution at the current yield and will not be impacted by actions that the fund has taken in the past. The most important thing for such an investor is how well the fund can sustain its current distribution. Let us investigate this.

Unfortunately, we do not have an especially recent document to consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. As such, this report will not include any information about the fund’s performance over the past seven months. That is very disappointing as it will not provide us with any insight into how well the fund handled the very challenging period for preferred stocks that existed during the summer of 2023. It may have taken losses during that period, although some of these losses might have been erased during the strong market rally that began in mid-October. We unfortunately will have to wait until the fund releases its annual report before having any insight into its performance during both of these periods. That is a shame, but we have to work with what has been publicly released right now.

During the six-month period, the Flaherty & Crumrine Preferred and Income Opportunity Fund received $2,498,502 in dividends along with $4,287,948 in interest. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $6,805,841 over the period. The fund paid its expenses out of that amount, which left it with $3,695,058 available for shareholders. That was, unfortunately, not enough to cover the fund’s distributions during the period. The fund paid out a total of $4,027,816 during the period so it was just a little bit short. We normally prefer that a fixed-income fund fully cover its distribution out of net investment income, so this is very disappointing. However, the fact that it did get so close to fully covering the payout improves our confidence somewhat.

There are other ways through which a fund can cover its distributions, however. For example, the price of preferred stock changes with interest rates, so the fund might be able to take advantage of this by trading the securities in its portfolio. Unfortunately, it failed miserably at this task during the period in question. The fund reported net realized losses of $3,063,665 and had another $6,304,129 net unrealized losses. Overall, the fund’s net assets declined by $9,700,552 after accounting for all inflows and outflows during the period. This comes on the heels of a $33,796,766 decline in net assets during the preceding full-year period. Thus, the fund has been seeing its net assets decline for at least eighteen months as of the time of the most recent report.

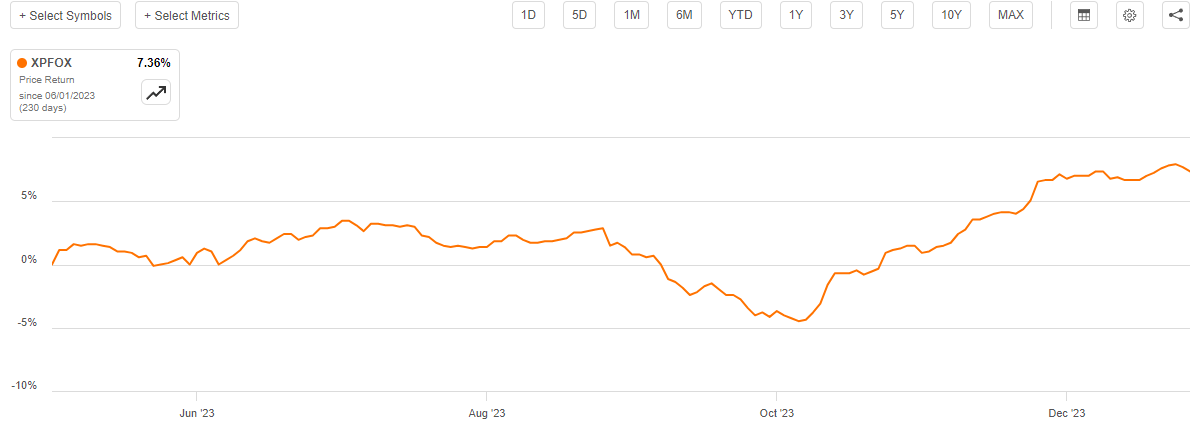

Fortunately, it does appear that the fund has managed to solve the problem of declining net assets. This chart shows the fund’s net asset value since June 1, 2023 (the first day following the release of its most recent financial report):

{kind=link}

As we can see here, the fund’s net asset value is up 7.36% since the most recent financial report was released. This suggests that the fund has covered all of the distributions that it has paid out over the past seven months. While it is uncertain whether or not it will be able to hold onto this performance if the Federal Reserve fails to cut interest rates, for now, it looks okay.

Valuation

As of January 17, 2024 (the most recent date for which data is currently available), the Flaherty & Crumrine Preferred and Income Opportunity Fund has a net asset value of $9.34 per share but the shares currently trade for $8.22 each. This gives the fund’s shares an 11.99% discount on net asset value at the current price. While that is not an especially attractive selling price, it is a smaller discount than the 14.32% discount that the fund’s shares have had on average over the past month. As such, the current price could be a reasonable level to take some profits.

Conclusion

In conclusion, the Flaherty & Crumrine Preferred and Income Opportunity Fund is a highly leveraged fixed-income closed-end fund that appears to have been run up too far in recent weeks. It seems very unlikely that the interest rate cuts necessary to justify the current price of the fund’s shares are going to be forthcoming anytime soon. As such, the fund is primed for a near-term price decline. The fund’s leverage will likely work against it here, so investors might want to take their recent profits and wait for a correction in order to reduce risks right now.

For further details see:

PFO: A Near-Term Correction Is Likely (Rating Downgrade)