PGX - PGX: Duration And Deglobalization Aren't A Great Combo

2023-08-30 10:13:02 ET

Summary

- Invesco Preferred ETF is mainly a financial ETF exposed to preferred shares, with a dominant exposure to the banking sector.

- The condition of national banks is pretty good in the U.S., especially as they absorb deposits from regional banks with relatively better ability to offer attractive rates.

- While short-term interest rates may be settling down, long-term rates are a concern for preferred investors, as changes in these rates can significantly impact the value of preferred shares.

- We think that long-duration exposures are at risk from further deglobalization, where we think the markets are thinking wishfully about the matter.

The Invesco Preferred ETF ( PGX ) is a primarily financial exchange-traded fund, or ETF, exposed to preferred shares. Duration is a consideration with preferred share ETFs, which means the situation with rates and their likely evolution will be critical. We think that long-term interest rates could remain elevated to a degree where current preferred yields would be insufficient to compensate shareholders for the risks of being preferred shareholders, which ultimately is like being a very subordinated debtholder. At least the rates are settling down for more upfronted maturities, but there is risk in preferred stocks due to their long duration.

Deglobalization is the primary concern, which we believe will be the global economic regime indefinitely, and will worsen. On top of the lacking risk premium in PGX to current rates, there is price risk if markets are thinking wishfully about deglobalization.

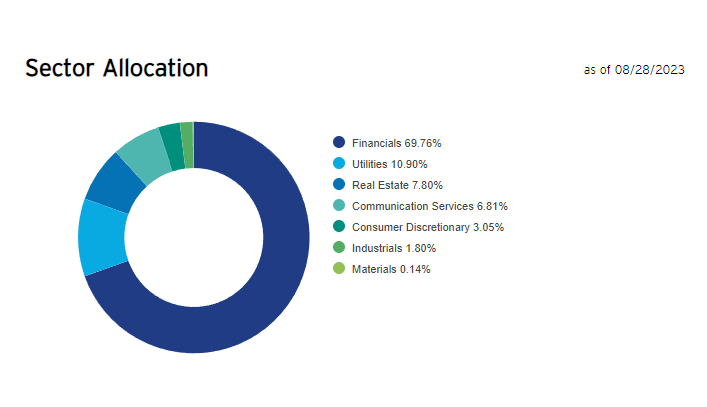

PGX Breakdown

Below are the sectoral exposures:

PGX Sectoral Exposures (Invesco.com)

{kind=link}

The financials exposure dominates the ETF and includes exposures to preferred shares from JPMorgan Chase ( JPM ), Wells Fargo ( WFC ) and Bank of America ( BAC ). Communications services is mainly AT&T ( T ).

While the credit rating of these companies are generally pretty high, the preferreds aren't rated highly due to their subordinated nature relative to the average issue in the debt stack. Preferreds have liquidation preferences but only after all the other claimholders before equity get what they're owed.

Liquidation is altogether pretty unlikely for the vast majority of this portfolio. While the banking system was under pressure in the beginning of the year, the large, national banks ultimately became beneficiaries of the failures of regional banks, and while deposit beta is eating into margins on the savings and deposits business, this is a problem for equity holders, not preferred shareholders, whose dividends are quite easily covered. Moreover, there are green shoots in other aspects of these businesses such as IB. Things are looking up, especially as markets and economic actors become more comfortable with where rates currently are. The national banks are going to be pretty resilient, and given that the Fed is beginning to signal an end to rate hikes, the sort of unemployment that could really rocket reserves and put banks in trouble does seem increasingly unlikely.

Bottom Line

While, in the short term, you can be somewhat confident in that rates are arriving at a top, you cannot be confident about long-term rates, which have actually been quietly revised upwards for the past several months. These long-term rates are what should concern preferred investors, because the bulk of the PV of preferreds is being discounted on the long-term horizon. These discount rates are compounded for many years, so changes in long-term rates are a problem.

The short term rates really don't matter all that much. And while long-term rates are estimated based on evolutions from short-term rates, factors like deglobalization, which could reverse the cost benefits from the economic reliance on China, are going to be an issue for the underlying inflation rates 5 and 10 years out from now, as well as the underlying interest rates.

Net of expenses on the ETF, the yield is only around 6% from the PGX. That's less than a 2% rate premium over the longer-term rate forecasts, which we believe markets are probably still underestimating due to wishful thinking around globalization as a trend and the actually substantial lead that China has relative to other economies in terms of the quality of their manufacturing.

Banking, which dominates the exposures in PGX, is quite safe for the time being. But deglobalization, higher costs, and potentially higher unemployment are risks that could turn the fortunes of major banks quite substantially. While preferred shares would be safer than equities in a situation like that, they still carry risk.

A 2% risk premium is quite simply not even close to enough considering that the average credit spread on a corporate bond would be close to that amount. Corporate bonds are going to be less risky than a preferred. At least the equities offer an earnings yield above 10%, of course with all the added risk but still a much more commensurate level.

Even just on a price basis, the long-duration makes preferreds unattractive if wishful thinking around deglobalization is in fact the consensus in markets. Insufficient compensation here for both price and credit risks. PGX isn't very compelling.

For further details see:

PGX: Duration And Deglobalization Aren't A Great Combo