PGZ - PGZ: CMBS CEF 40% Upside Once It Bottoms

Summary

- The Principal Real Estate Income Fund is a closed-end fund in the fixed-income space.

- The CEF focuses on below-investment-grade CMBS tranches and REIT Equity.

- In 2022, PGZ had a total return very much in line with the better-known Cohen & Steers Quality Income Realty Fund (RQI).

- PGZ is a high beta, high-leverage vehicle.

- Currently, there is significant distress in the CMBS market with a maturity wall on the horizon, but we are not experiencing the same Armageddon scenario in commercial properties as during Covid.

Thesis

The Principal Real Estate Income Fund ( PGZ ) is a closed end fund in the fixed income space. The vehicle focuses on mezzanine Commercial mortgage-backed securities ('CMBS') and REIT equity. As per its literature:

The Principal Real Estate Income Fund seeks to provide high current income, with capital appreciation as a secondary objective, by investing in higher-yielding debt and equity commercial real estate-related investments.

The current collateral split is 65% CMBS bonds and 35% REIT equity. Commercial mortgage-backed securities are a leveraged play on commercial real estate, and depending where they sit in the capital structure (investment grade or junk) they can carry a significant amount of default risk, with larger gap-down traits when compared to pure corporate credit. The reason behind this occurrence is the collateral pool, which is generally composed of a few large properties. Once a loan on a property defaults and incurs a loss in the structure, it can wipe out a number of debt tranches. But more of that in the 'Holdings' section below, as well as a deep dive into one of the CMBS bonds in this fund.

The CEF has lost value in the past year due to higher interest rates. Higher rates are bad all across the capital stack in the fund, especially when considering the leverage in the name. The fund has an outright 36% leverage ratio, but more importantly through its CMBS mezz holdings it has embedded leverage as well. High leverage equates high volatility, and the propensity for the fund to lose value fast.

This is a high beta fund that has not bottomed yet, but once it does we will see a slow recovery similar to what we witnessed post Covid, with an upside potential of 40% plus.

Holdings

The current collateral split is 65% CMBS bonds and 35% REIT equity. Its top holdings are CMBS bonds:

Top Holdings (Fund Fact Sheet)

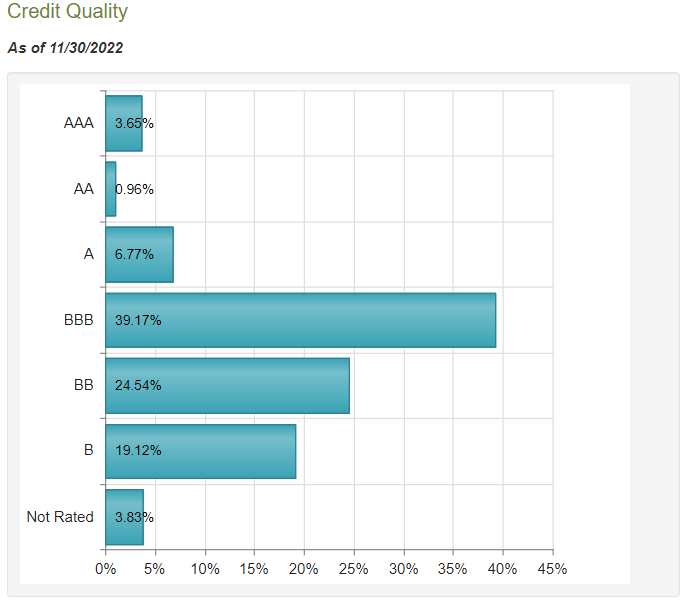

We can see that from a ratings stand-point the fund has a chunky exposure to non-investment grade names:

{kind=link}

We can see that 'BB' and 'B' names account for almost 65% of the CMBS portfolio. That is a fair amount of risk, with leverage on top.

Let us do a deep dive into one of the bonds in this fund so that an investor can have a better understanding of the CMBS market. For starters, please notice the record near term debt maturity wall in commercial lending:

Commercial Debt Maturity Wall (SLGreen Presentation)

{kind=link}

This has translated into lower prices for mezz CMBS bonds. One of the names in the collateral pool is COMM 2013-CCRE6 (Commercial Mortgage Trust 2013-CR6).

This CMBS bond was issued back in 2013 with 80 properties securing the commercial loans:

Deutsche Bank Securities and Cantor Fitzgerald & Co. have filed a prospectus for COMM 2013-CCRE6, a $1.49 billion CMBS conduit deal for 48 commercial mortgage loans secured by 80 properties.

The largest loan in the transaction is for The Federal Center Plaza, a fixed rate loan with a principal balance of $130 million. The loan is secured by the fee simple interest in two adjacent office buildings totaling 725,317 square feet and a controlling interest in a connected, 912-space parking garage in downtown Washington, DC. The Federal Center Plaza Loan has a 10-year term and interest only payments for the term of the loan. The Federal Center Plaza Loan accrues interest at a fixed rate equal to 4.1405 percent.

Source: CRE Newsletter

The Federal Center Plaza loan is now coming due, but it seems that there will be a default here:

This month the maturity defaults and imminent maturity defaults were led by several large office loans including:

$327.7 million Wells Fargo Center (MSC 2019-NUGS)

$243.6 million Republic Plaza (WFRBS 2012-C10 & WFRBS 2013-C11)

$130.0 million Federal Center Plaza (COMM 2013-CR6)

Source: KBRA

We are not aware of the loan to value on the Federal Center Plaza property, but once it defaults any losses will be passed to the COMM 2013-CR6 securitization, which in turn will absorb losses based on subordination. This is basically in a nutshell how the commercial mortgage market distress translates into a tangible result for a CMBS CEF like PGZ, which holds one of the tranches of the COMM 2013 securitization.

Performance

In the past year the CEF has lost around -25% of its value:

{kind=link}

We are comparing PGZ here with a premier REIT CEF, namely the Cohen & Steers Quality Income Realty Fund ( RQI ) and the CMBS ETF ( CMBS ). CMBS is composed of only AAA tranches of CMBS bonds, hence we will always expect this name to have a low volatility. We can see that PGZ and RQI had very similar performances last year.

A longer time-frame brings into focus de-leveraging issues during Covid:

{kind=link}

We can see how PGZ and RQI had very similar total return profiles until the Covid crisis. Both vehicles lost a substantial amount during the pandemic, but PGZ never really recovered to the same extent as RQI. We are assuming some forced deleveraging here and maybe some impairments. Interesting to note that now, on a 5-year timeframe, CMBS and PGZ have very similar total returns (obviously with very different volatility profiles and drawdowns).

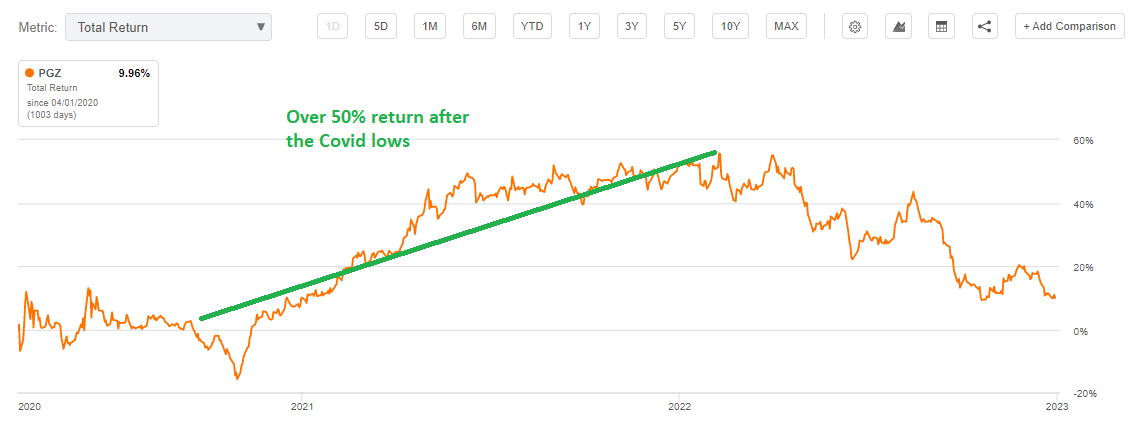

PGZ is a very cyclical fund due to its build - it contains many mezz CMBS tranches. After the Covid crash the fund took its time to build a bottom, but then proceeded to post a 50% plus gain:

Return after Covid (Seeking Alpha)

{kind=link}

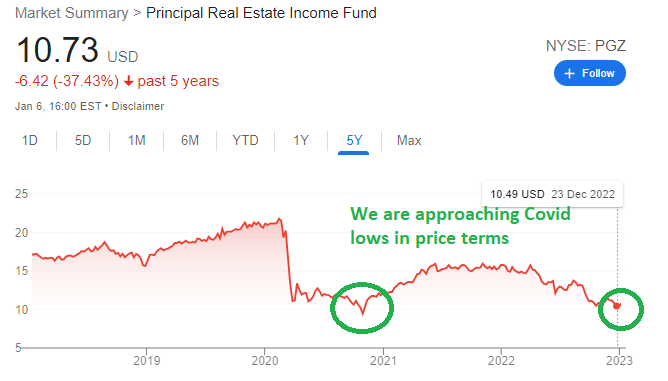

We are now starting to approach the Covid lows in price yet again:

{kind=link}

This fund will take a while to bottom and it will not have a "V" shaped recovery, but the price is closing in on Covid lows, when the world was about to end.

Premium / Discount to NAV

The fund usually trades at a discount to net asset value:

Premium/Discount (Morningstar)

{kind=link}

We can see that historically the vehicle has traded at a -10% discount to NAV, which got more pronounced after the Covid crash. CMBS bonds are more on the illiquid side, and commercial real estate is now under pressure on the back of higher rates. We expect the discount to persist.

Distributions

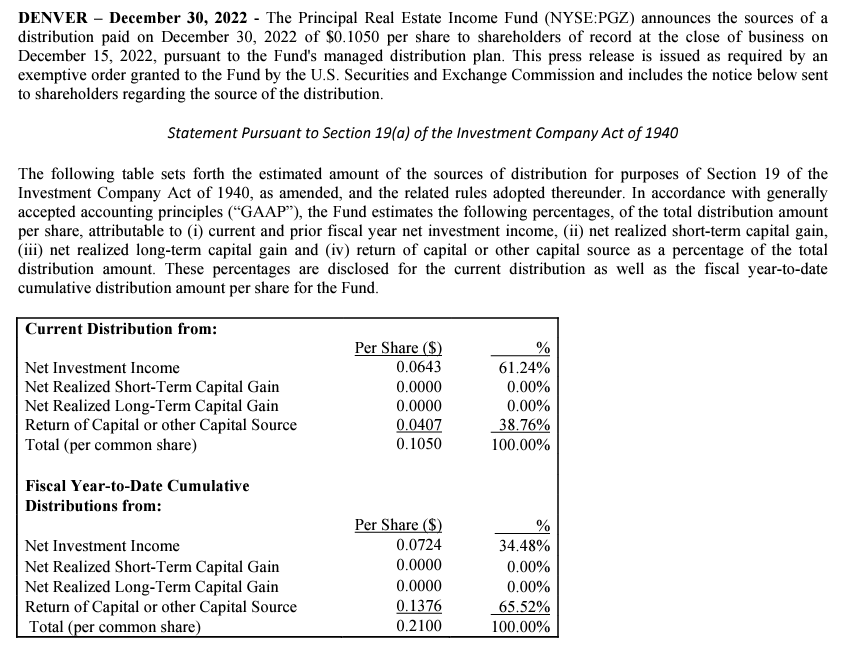

Due to the underperformance in the Equity REIT collateral, the fund's distribution is not currently covered:

{kind=link}

As we can see from the above table the fund utilizes a substantial amount of REIT equity capital gains to cover its dividend. When the market is down, the fund uses ROC instead. Expect this to continue until we see a recovery in REIT equity prices.

Conclusion

PGZ is a CMBS and REIT equity closed end fund. The current collateral split is 65% CMBS bonds and 35% REIT equity. On the CMBS side the fund is overweight below investment grade names, which are experiencing distress on the back of higher rates and a maturity wall in the commercial debt market. The fund is trading with a -15% discount to NAV, which we expect to persist. In 2022 PGZ had a total return very much in line with the better known Cohen & Steers Quality Income Realty Fund ( RQI ).

PGZ is a high beta, high leverage vehicle. The fund is not a true buy and hold, with an investor needing to pick it up after it bottoms out, and sell it when the market recovers. CMBS prices have come down on the back of higher rates and an expected liquidity crunch in 2023/2024, with over $ 1 trillion of commercial debt coming up for re-financing. The realities of the underlying collateral and leverage have translated into a price for PGZ which is approaching its Covid lows. This is not a CEF for the faint of heart, and once it bottoms it will not have a "V" shaped recovery (we do not expect the Fed to pivot to 0% rates in 2024). However, do expect a price action similar to the post-Covid one, with the fund slowly recovering and posting healthy total returns in the years after. We expect a 40% total return in the name after the bottoming process is over and the ironing out of debt re-financings in the CMBS market.

For further details see:

PGZ: CMBS CEF, 40% Upside Once It Bottoms