PAHC - Phibro Animal Health: Vaccine App And Analysts' Expectations Imply Undervaluation

2023-11-20 20:53:35 ET

Summary

- Phibro Animal Health Corporation is expected to experience net sales growth and net income growth in the coming years.

- The company has a healthy balance sheet with little debt, which positions it well for successful expansion and innovation in its products.

- There are risks from changing regulations and competition, but overall, Phibro Animal appears undervalued.

Phibro Animal Health Corporation ( PAHC ) did not surprise the market in the last quarterly release , however most investors are expecting net sales growth and net income growth in the coming years. With a healthy balance sheet and little debt, I would expect that successful expansion of the life cycle of value-added products and further innovation in vaccines like the VAC Tracker App could bring net sales growth. There are obvious risks from changes in the changing regulations, the potential restriction of antibacterials in food-producing animals, and competitors. With that, I believe that Phibro Animal appears undervalued.

Phibro Animal Health Corporation: Recent Earnings And Beneficial Market Expectations

Phibro Animal Health Corporation is a leading global company in the field of animal health and mineral nutrition. Its commitment is to be a trusted partner for livestock producers, farmers, veterinarians, and consumers who are dedicated to the breeding and care of farm and companion animals.

{kind=link}

The company offers a wide range of products, with around 770 lines available in more than 80 countries, serving around 4,000 customers. Its products span diverse categories, from poultry, pigs, beef, and dairy cattle to aquaculture and dogs. These products are essential to prevent, control, and treat diseases as well as to support nutrition to improve the health and well-being of animals. Phibro Animal Health Corporation markets its products directly to integrated birds and through other channels.

Source: 10-Q

{kind=link}

{kind=link}

Phibro Animal Health Corporation operates in a diverse market, with approximately 4,000 customers, where the majority of the customers are served by its Animal Health and Mineral Nutrition segments. Its main clients are various livestock producers, covering poultry operations, swine, meat, and dairy farmers. The products are sold directly to the producers and distributors who resell them. For the pet segment, the company uses a distributor that reaches veterinary clinics. The company is not heavily dependent on a specific customer, and the loss of one would not have a material impact on its results. Furthermore, it does not usually enter into long-term contracts, operating mainly through purchase orders. Phibro did not really perform in the last quarterly earnings. The company reported lower revenue than expected, and EPS GAAP Actual was also lower than expected. Quarterly revenue stood at $231 million, and EPS GAAP was close to -$0.2. Having said that, investors are expecting a sales estimate of $240 million in the next quarter, so I believe that market estimates are optimistic. The new quarter is expected to be better than the previous one.

Source: SA

With that about the business model and recent earnings, in my view, it is a great moment to have a close look at the company given the recent long term expectations of other analysts. Analysts’ expectations include net sales growth, operating margin growth, and EPS growth. They are expecting 2025 net sales of $1.040 billion, with 2025 EBITDA of $116 million, EBIT of $85.8 million, and 2025 net income of $34.5 million.

Source: Market Screener Source: Market Screener

Healthy Balance Sheet

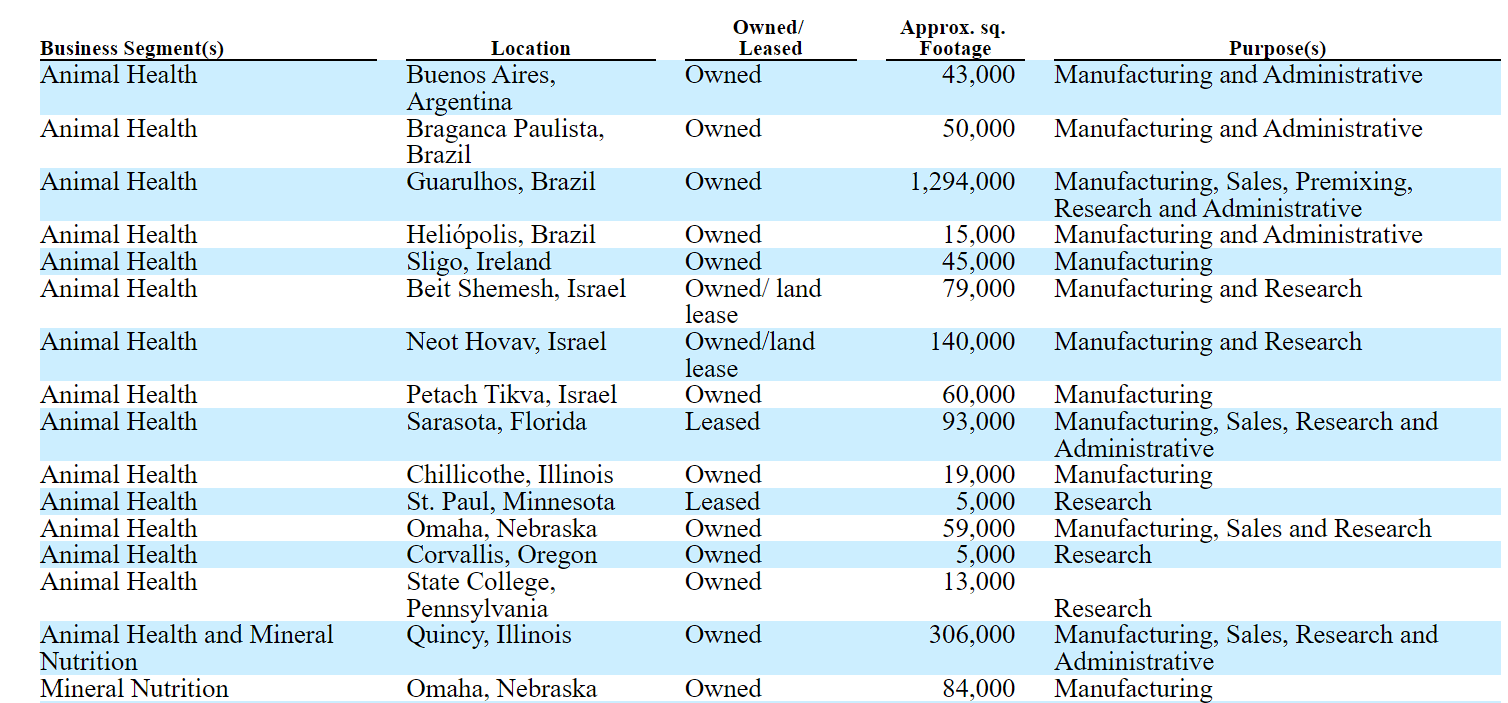

In the last report, the company noted cash and cash equivalents worth $43 million, short-term investments of about $48 million, and accounts receivable worth $149 million. Besides, with inventories of $279 million, total current assets were equal to $584 million. The current ratio appears significantly larger than 1x, so I am not really worried about a liquidity crisis.

Phibro also reports property, plant, and equipment of close to $193 million, with intangibles worth $52 million, goodwill of $53 million, and total assets close to $964 million. The asset/liability ratio stands at more than 1x, so I would say that the balance sheet remains stable.

Source: 10-Q

Current portion of long-term debt is equal to $24 million, with accounts payable worth $77 million and total current liabilities of close to $172 million. Finally, with a revolving credit facility of $154 million and long-term debt worth $304 million, total liabilities were equal to $691 million. It is worth noting that the long-term debt decreased a bit as compared to that reported in the last quarter, however the revolving credit facility increased. With that being said, I do not think that investors will be afraid of the total amount of debt. In the last ten years, financial leverage decreased.

Source: 10-Q Source: Ycharts

Debt Analysis, And Cost Of Debt

In April 2021, Phibro Animal Health Corporation entered into an amended and restated credit agreement that included a term loan and a revolving line of credit, with initial amounts of $300,000 and $250,000 respectively. In November 2022, the 2021 Credit Facilities were modified, increasing the revolving commitment to $310,000 and changing the interest rate from LIBOR to SOFR. In June 2023, an incremental term loan of $50,000 was obtained. These loans are based on the net leverage ratio, and will mature in April 2026. Additionally, in September 2022, a 2022 Term Loan was contracted for $12,000 to mature in September 2027.

{kind=link}

Interest rates vary, and derivatives are used to manage interest rate risk. According to the most recent quarterly report, the term loans and revolving facilities include interest rates of close to 6.23% and 7.42%. I also saw that the company is paying interest rates close to SOFR plus 2.0%.

Source: 10-Q

In September 2022, we entered into a credit agreement (the “2022 Term Loan”) in the amount of $12,000, collateralized by certain facilities. The 2022 Term Loan matures in September 2027. The interest rate per annum applicable to the 2022 Term Loan is based on a fluctuating rate of interest, at the Company’s election from time to time, equal to either one-month adjusted SOFR plus 2.0%, or a base rate determined by reference to the greater of the prime rate and the Federal Funds Effective Rate plus 0.5%. The 2022 Term Loan is repayable in monthly installments of $35, with the balance payable at maturity. Source: 10-Q

With these numbers in mind, I believe that the cost of capital of about 6.2%-7.4% would make sense for a DCF model.

Sector Median, And Trading Multiples

For the assessment of the exit multiples, I assessed the valuation of competitors in the same sector. According to SA, peers in the same sector report a median EV/EBITDA of 14x-12x, Price/Cash Flow of 15.99x-16.57x, and Price/Book of 1.8x. With these numbers in mind, I used a terminal valuation of around 12.5x-15.9x FCF.

Source: SA

Bearish Case Scenario, And Risks

Phibro Animal Health Corporation faces significant risks in its industry. Public perception of human health risks related to the consumption of foods derived from animals treated with their products could reduce sales.

Additionally, reliance on a healthy livestock industry is subject to changing regulations and the potential restriction of antibacterials in food-producing animals. This could adversely affect company’ operations and financial results.

Concerns about antibacterial resistance and government restrictions may impact the sales. Reputation and public perception can also influence the use of the company’s products.

Under the previous detrimental assumptions, my expectations include 2032 net income of about $53 million, depreciation and amortization worth $43 million, but no amortization of debt issuance costs, no gain on sale of investment, or stock-based compensation. Under this case scenario, I used a median net income growth close to 1.28%, which I believe is quite conservative.

{kind=link}

Additionally, with 2032 changes in accounts receivable of about $67 million, changes in inventories worth $46 million, and changes in other current assets of about -$38 million, I also included changes in accounts payable of about -$19 million. Finally, with changes in accrued expenses and other liabilities close to -$45 million, 2032 net cash provided by operating activities would be $122 million. Taking into account 2032 capital expenditures of -$44 million, 2032 FCF would be $78 million.

Source: DCF Model

If we assume a WACC of 7.42% and an EV/FCF of 12.5x, the total implied enterprise value would be $814 million. Adding cash and subtracting equity, the implied forecast price would be close to $9.7 per share, and the IRR would be close to -0.58%.

Source: DCF Model

My Best Case Scenario Includes Successful Expansion Of The Life Cycle Of Value-added Products And Growth In Emerging Markets.

Phibro Animal is pursuing a number of strategic initiatives critical to its long-term success. Under this scenario, I assumed that some of these strategies could bring net sales growth and FCF growth. Strategies include increasing sales in emerging markets, growing revenue through new product development, and expanding the life cycle of value-added products.

I also believe that improving operational efficiency and expanding its complementary products and services along with a continued investment in animal products could bring business growth. Given the balance sheet, cash in hand, and lack of debt, I think that Phibro is well positioned to pay for new product design or increases in sales and marketing for geographic expansion. I also believe that further investments in vaccines could also significantly accelerate the net sales growth of the group. The animal vaccine market is growing at close to 10%, and in the last quarter, vaccine net sales increased by close to 14% as compared to the same quarter in 2022.

Source: 10-Q

A study published by Towards Healthcare states that the animal vaccine market is estimated to grow from $14.27 billion in 2022 at 10% CAGR to reach an estimated $ 36.91 billion by 2032, as a result of a rising focus on food safety and security. Source: Animal Vaccine Market Size USD 36.91 Billion by 2032 with a CAGR of 10%

With regards to the vaccine efforts, it is worth noting the new technological tools designed by Phibro. More specifically, the VAC Tracker App is, in my view, a useful tool that could bring significant data about clients, and create new relationships. I encourage investors to have a quick look at it.

{kind=link}

The global animal healthcare market size is expected to grow at close to 4.7%, however I tried to be as conservative as possible, and used a median net income growth of 2.8%.

The global animal healthcare market size was estimated at US$ 54 billion in 2022 and is expected to surpass around US$ 85.07 billion by 2032, poised to grow at a compound annual growth rate of 4.70% from 2023 to 2032. Source: Animal Healthcare Market Size, Growth, Trends, Report 2023-2032

{kind=link}

More in particular, under this scenario, I assumed 2032 net income of close to $69.55 million, 2032 depreciation and amortization of $53.055 million, and changes in accounts receivable of about $67.055 million.

Besides, with changes in inventories of $39 million, changes in other current assets close to -$13 million, and changes in accounts payable of -$18 million, net cash provided by operating activities would be close to $165.55 million. Finally, with capital expenditures of about -$54.055 million, 2032 FCF would be close to $112.055 million.

Source: DCF Model

If we include a WACC of 6.2055% and the implied enterprise value of $1.03975 billion, the implied equity forecast would be close to 1.0055 billion, and the fair price may be close to $25 per share. Besides, we would be talking about an IRR of about 13.955%.

Source: DCF Model

Highly Competitive Industries

In my opinion, Phibro operates in highly competitive industries, facing rivalry from global and regional competitors with diverse resources. Its competitive position is supported by product records, customer service, product line breadth, quality, manufacturing technology, location, and pricing. Consolidation in the animal health market can strengthen competition. Competitors continue to innovate and launch competitive products.

My Opinion

In my opinion, Phibro is a leading company in the animal market, providing a wide range of essential products for the prevention, control, and treatment of diseases in farm and companion animals. I expect growing revenue through expansion of the life cycle of value-added products, the development of the vaccine business, and further technological innovations like that of the vaccine tracker. There are obvious risks from changes in the regulation of antibacterials in livestock production and competition, however I believe that the stock appears a bit undervalued.

For further details see:

Phibro Animal Health: Vaccine App And Analysts' Expectations Imply Undervaluation