SWMAY - Philip Morris: Not As Attractive As The Competition

Summary

- Philip Morris is the largest company in the tobacco sector with a market cap of $159B.

- Shares are near fair value today just above $100. With an earnings multiple over 17x, shares don't have a margin of safety for new investors.

- The acquisition of Swedish Match and its very popular ZYN product line is going to be a boost for the company long term.

- I find Altria and British American Tobacco to be more attractive due to their single digit P/E ratios and yields over 7%.

I wrote a couple articles in 2022 on Philip Morris ( PM ), the tobacco giant focused on international markets. My opinion on the stock at the time was that it didn’t offer the same margin of safety as other tobacco giants like Altria ( MO ) and British American Tobacco ( BTI ). While other companies in the tobacco sector have single digit P/E ratios, Philip Morris has a more expensive valuation, which is why I think forward returns won’t be as attractive over the next couple years.

Investment Thesis

Over the last year, shares of Philip Morris have bounced between the mid-80s and $110. Shares now sit in near the middle of that range just over $100. This is right around fair value in my opinion, and shares have a P/E over 17x right now. That is why I prefer the cheaper alternatives like Altria or British American Tobacco, which I expect to experience multiple expansion in the next couple years unlike Philip Morris. They also have larger yields than Philip Morris’s 5% dividend.

One thing that I do like Philip Morris is their smoke free transformation. Altria has had several false starts on this front, and after the acquisition of Swedish Match ( SWMAY ), Philip Morris now controls the very popular ZYN brand. After the company digests the acquisition, I expect the company will resume their buybacks and increase the dividend in the mid-single digit range moving forward. However, with the valuation that is rich relative to the sector, I think most of the returns for investors will be from dividends instead of share price appreciation.

Swedish Match & Reduced Risk Products

The biggest event for Philip Morris in 2022 was their acquisition of Swedish Match. They plan to remove the listing from exchanges after retiring the remaining shares. I think that the acquisition will be a huge benefit for the company long term, but it will take some time to digest the acquisition. One thing I will say about Philip Morris is that they seem to have been more successful with their investments in reduced risk products than Altria.

{kind=link}

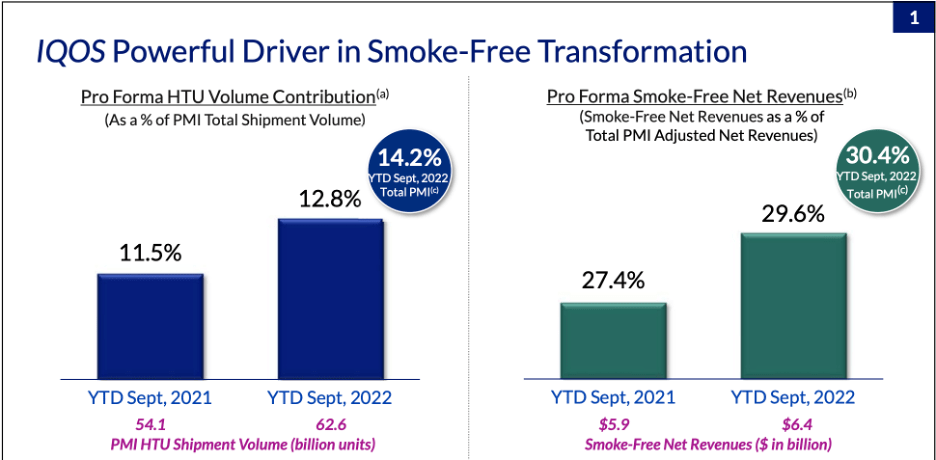

The company has seen continued growth of the combustible alternatives like IQOS. The IQOS products continue to grow as a percentage of Philip Morris’s volumes, and now make up nearly 30% of the company’s revenues. Altria has had several misfires with their reduced risk products, and Philip Morris now owns the popular ZYN line of smokeless tobacco, which is the market share leader in the segment. With their continued execution I understand the relative valuation premium to Altria, but I don’t think now is an opportune time to buy shares.

Valuation

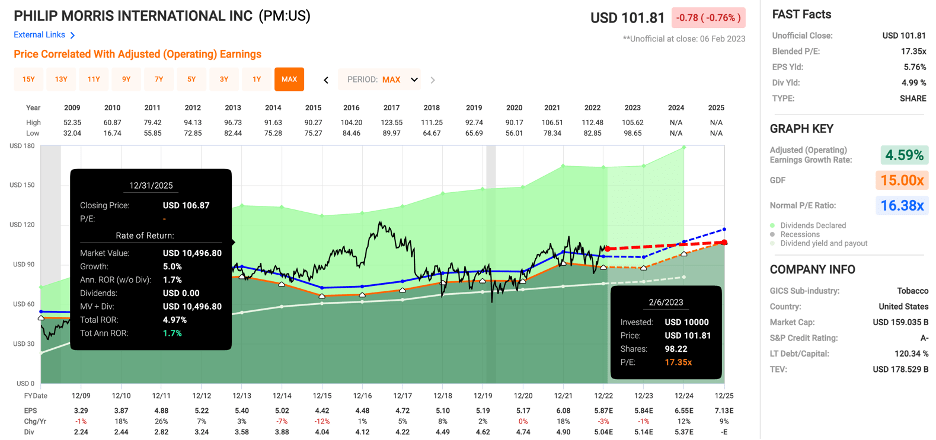

Philip Morris stock now has a blended earnings multiple of 17.4x. This is one turn higher than the average multiple of 16.4x. Despite excise taxes, the large tobacco companies have impressive margins, which is why I think the other companies in the sector are too cheap. Philip Morris is close to fair value in my opinion with shares near $100.

{kind=link}

While earnings are projected to grow next year and in 2025, I don’t think long term investors should expect any multiple expansion from here. When you look at alternatives like Altria or British American Tobacco with single digit P/E ratios and larger dividends, I don’t see why investors putting money to work today would choose Philip Morris. This doesn’t mean it’s time to sell for long term investors, but if you are looking for an investment in the tobacco sector with an attractive valuation and large dividend, I would choose Altria or British American Tobacco. While I’m not a huge fan of the current valuation, Philip Morris does have a history of consistently providing dividend hikes for investors.

Dividends & Buybacks

Since the spin off, Philip Morris has consistently raised their dividend. Their most recent increase was a 1.6% increase from a quarterly payout of $1.25 to $1.27. This is a smaller increase than recent years, but this is likely due to the Swedish Match acquisition. The yield currently sits just under 5%, but I would expect the dividend growth to speed up again after the company digests the acquisition.

The other thing that investors in the tobacco industry have come to expect in recent years is a consistent share buyback program. While Altria and British American Tobacco have continued to plow money into buybacks, that is not the case for Philip Morris in recent quarters. After announcing the Swedish Match acquisition, Philip Morris paused their buyback program, except to offset shares for employee stock options. I think the buybacks will start back up sooner or later, but the current valuation means that I would rather see dividend increases (or other acquisitions) if I were an investor.

Conclusion

I chose Altria as my conservative pick for 2023 , and I plan to write an update on British American Tobacco soon. The biggest reason I prefer those two stocks is simply the valuation. With single digit P/E ratios and yields over 7%, I think their risk/reward is better than Philip Morris. I think most of the returns for investors in Philip Morris will come from the 5% dividend, while I think the other companies have meaningful upside from multiple expansion. I do like the Swedish Match acquisition which should be good for the company and its long-term investors.

One of the questions I ask myself when making new investments is this: do I think this has the potential to provide double digit returns over the next three to five years? I’m not going to pretend I have a 100% hit rate, but it does help screen out stocks where I don’t find the risk/reward to be that attractive. I don’t see double digit returns for Philip Morris in coming years, primarily due to the starting earnings multiple over 17x. I wouldn’t be a seller here, but for investors putting new cash to work in the sector, I would recommend a closer look at Altria or British American Tobacco.

For further details see:

Philip Morris: Not As Attractive As The Competition