MO - Philip Morris Stock: Cheaper And Stronger

2023-09-29 07:13:21 ET

Summary

- Philip Morris International has experienced stronger-than-expected growth in its reduced-risk product range, making it more attractive to investors.

- The company's iQOS brand has been highly successful, achieving significant revenue growth and profitability.

- Philip Morris aims to generate at least two-thirds of its overall revenue from reduced-risk products by 2030.

- PM stock is not expensive, and promises attractive total returns.

Article Thesis

Philip Morris International Inc. ( PM ) is a leading tobacco company that is heavily active in the reduced-risk product range via its brands such as iQOS. The company's valuation has recently come down, while growth has been stronger than expected. With the dividend yield also having risen over the last couple of months, Philip Morris International looks more attractive than it did at the beginning of the year.

Philip Morris: The King Of Reduced-Risk Products

Traditional tobacco usage, via smoking, comes with major health risks, as (almost) everyone knows. Of course, there are still many who decide to smoke anyway, but more health-conscious consumers are hard to reach with a product such as cigarettes. That is why many tobacco companies, including Philip Morris International, have been investing heavily in new product categories that come with (at least from what we know today) fewer health risks. Products such as heat-not-burn devices, vapes, and so on are among the categories experiencing growth, and that is also where tobacco companies have made investments -- both when it comes to R&D, and when it comes to marketing.

Not all companies have been equally successful in shifting their product mix towards these lower-risk products, however. Some have had a harder time, others did better. Philip Morris International, with its iQOS brand, has been highly successful and has experienced compelling growth both in terms of sales volumes as well as in terms of revenues and profits.

Philip Morris' revenue growth has been better than that of Altria ( MO ), British American Tobacco ( BTI ), and Japan Tobacco ( JAPAY ). Philip Morris achieved roughly twice the growth rate of MO and BTI, while JAPAY fell behind even further. The fact that Philip Morris was able to generate this kind of growth in US Dollars, despite selling its products outside of the US only, is even more remarkable -- a strengthening US Dollar was a headwind for PM, but not for MO, and yet, PM grew faster.

To some degree, this is due to PM's exposure to faster-growing markets in some developing and emerging countries, where anti-smoking laws can also be less severe compared to the US, for example. But Philip Morris' attractive business growth was also driven by its very successful reduced-risk portfolio, which has been gaining more revenue share compared to the other major tobacco companies.

In a recent presentation, a summary of which is available here , Philip Morris International lays out its past success and its goals for the future:

{kind=link}

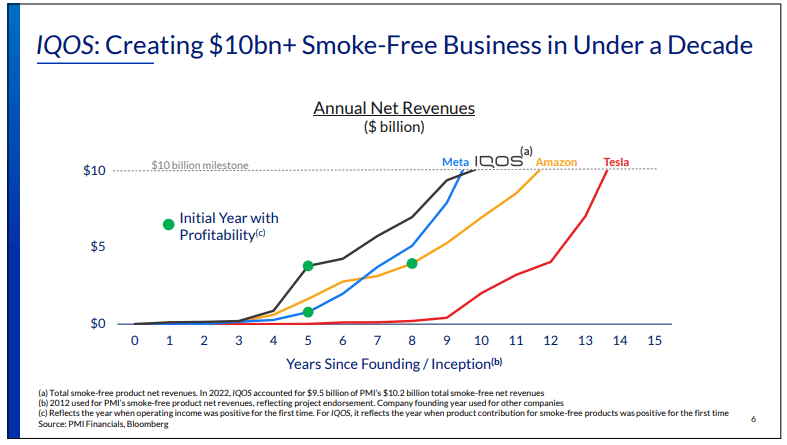

We see that iQOS sales have risen to $10 billion a year in around one decade, despite the fact that the business was doing very small revenues only for the first couple of years. That's when Philip Morris ran smaller tests in single countries in order to get feedback, in order to optimize marketing, and so on. Once the company pushed into more markets, revenues began to soar, and it does not look like growth will slow down any time soon.

In the above chart, the company also compares iQOS's growth in the first couple of years to the growth that major companies such as Meta Platforms (META), Amazon (AMZN), and Tesla (TSLA) have achieved. iQOS hit the $10 billion mark a lot earlier than AMZN and TSLA and around the same time as Meta. iQOS also was pretty early in achieving profitability. Hitting profitability early is a good thing for shareholders, as it means that the legacy smoking business doesn't have to subsidize the iQOS brand any longer, while the early profitability also suggests that iQOS, overall, is a highly profitable product in itself. Some investors have feared that reduced-risk products wouldn't be as profitable as traditional cigarettes, but this chart could help ease their fears. Of course, it is important to note that iQOS was, unlike META, AMZN, and TSLA, not a standalone company -- iQOS was part of a very profitable company, while the others were startups.

During the most recent quarter, Philip Morris' smoke-free revenues made up more than 35% of total revenues, which shows how far the company has already come in expanding its new businesses. In more than 20 markets, Philip Morris is already generating more revenues with its reduced-risk products compared to its legacy products. And thanks to iQOS' ongoing strong growth, we can expect that the number of countries where this holds true will continue to grow.

In fact, the company plans to hit that target -- at least 50% of revenue coming from reduced-risk products -- on a company-wide basis over the next couple of years. By 2030, i.e. seven years from now, Philip Morris plans to generate two-thirds of its overall company-wide revenues from its reduced-risk portfolio.

iQOS is the most important revenue source in that category, but Philip Morris's more recent introduction Zyn is also well-received and growing fast. Zyn is a nicotine pouch that is, among other countries, also sold in the US, even though Philip Morris doesn't sell its other products there. This gives the company some exposure to the major US market, which Philip Morris believes will be beneficial for its profit performance going forward.

Strong Growth And A Solid Valuation

Philip Morris' attractive business growth rate in the reduced-risk product space translates into attractive financials. While the core legacy business isn't much of a growth driver, it still continues to generate attractive profits and cash flows as well.

For the coming three years, i.e. for the 2024 to 2026 period, Philip Morris International is forecasting revenue growth of around 6% to 8% on an organic basis. Since Philip Morris generates most of its revenues outside of the US, forex rate movements can have a major impact on the company's reported revenues once denominated in US Dollars. But since the USD will, I assume, not strengthen forever, this should not be a long-term headwind. Once/if the US Dollar heads lower, Philip Morris's ex-USD exposure could turn into a currency rate tailwind .

Due to operating leverage, Philip Morris believes that its profits will grow considerably faster than its revenues. That makes sense, as price increases and optimization will allow for margin growth -- the same has held true for many years for Philip Morris and other tobacco companies. The company thus targets an operating income growth rate of 8% to 10% for the next three years. With some debt reduction that should result in lower interest expenses, net profit and earnings per share are forecasted to grow at an even faster rate of 9% to 11% per year in the 2024 to 2026 time frame. Note that this forecast does not account for buybacks, as Philip Morris plans to spend most of its free cash flow on dividends and debt reduction.

While currency rate movements could result in ups and downs in these numbers as the forecast is based on currency-neutral assumptions, I believe that, generally, the forecast seems relatively realistic. But in order to be conservative here, let's assume that Philip Morris grows at just two-thirds of the forecasted pace. This would translate into a revenue growth rate of 5% per year, while earnings per share would grow by 7% per year in 2024, 2025, and 2026. Since Philip Morris has also updated its earnings per share guidance for the current year, now forecasting ~$6.50, this would translate into earnings per share of around $7.95 to $8.00 in 2026. If Philip Morris is able to hit its goals, earnings per share would come in at $8.65. Even the lower one of these numbers, the more conservative $8.00 estimate, would be a nice feat for the company, I believe. Put a 15x earnings multiple on that, and Philip Morris would trade at $120 per share at the end of 2026. That would represent an upside potential of 29% over a little more than three years, or around 8% per year. On top of that, investors would be receiving a dividend yield of 5.5%, which would make for 13%-14% annual returns.

Even if PM were to grow its earnings per share at just half the forecasted rate, and if the earnings multiple in 2026 would be just 13 , then total returns over the next three years would still be in the 6%-7% range -- which wouldn't be a disaster at all. And I believe that this is a very conservative estimate, actual performance should be well ahead of that.

Takeaway

PM used to be more expensive than other tobacco companies, and that still holds true to some degree. But the strong growth from the reduced-risk portfolio remains very convincing, the forecast for the current year and beyond is great, and since PM has seen its shares drop so far this year, the valuation has gotten cheaper as well. Meanwhile, the price decline has also resulted in a higher dividend yield. While not the highest-yielding tobacco company, Philip Morris looks attractive at current prices, and I will likely establish a position soon.

For further details see:

Philip Morris Stock: Cheaper And Stronger