PM - Philip Morris: The Smoke-Free Segment Future Looks Bright

2023-09-14 09:15:36 ET

Summary

- Philip Morris recently raised its dividend by 2.4% to $1.30, disappointing some investors accustomed to larger increases.

- Philip Morris and Altria Group are popular among dividend investors for their large payouts.

- Philip Morris has been shifting its focus to smoke-free products, such as vapes and IQOS, to adapt to the decline in traditional smoking.

- Philip Morris posted impressive revenue growth quarter-over-quarter after having two full quarters after the Swedish Match acquisition.

- Philip Morris earnings are expected to grow by double-digits from now until 2025.

Introduction

Recently, Philip Morris International ( PM ) raised its dividend by 2.4%, from $1.27 from $1.30. This left investors disappointed as many were accustomed to seeing larger increases from the tobacco company. Both PM and Altria Group ( MO ) are very popular amongst investors as they both pay out large dividends to their shareholders. MO also raised its dividend a month earlier from $0.94 to $0.98, so one can see why they're favorites with dividend investors.

Since its spinoff from the latter in 2008, PM has been rewarding its shareholders with steady dividend increases. But those increases have slowed in recent years. Considering the current state of the economy, I think a 2.4% increase is solid. With so much uncertainty right now, this shows the strength of not only the finances, but of the management team as well. In this article I discuss why I think PM deserves a spot in your dividend portfolio.

Who Is Philip Morris?

I look as PM and MO similarly to how I look at Realty Income ( O ) and Agree Realty ( ADC ). PM is the big brother to MO, just like O is the big brother to ADC. Although they spun-off from Altria in 2008, they actually have the larger market cap at $147.85 billion and operate in the international space. The company is headquartered in Stamford, Connecticut and has a global workforce of nearly 80,000. Their portfolio consists of cigarettes and smoke-free tobacco products, including heat-not-burn, vapor, and oral nicotine products under the IQOS and ZYN brands.

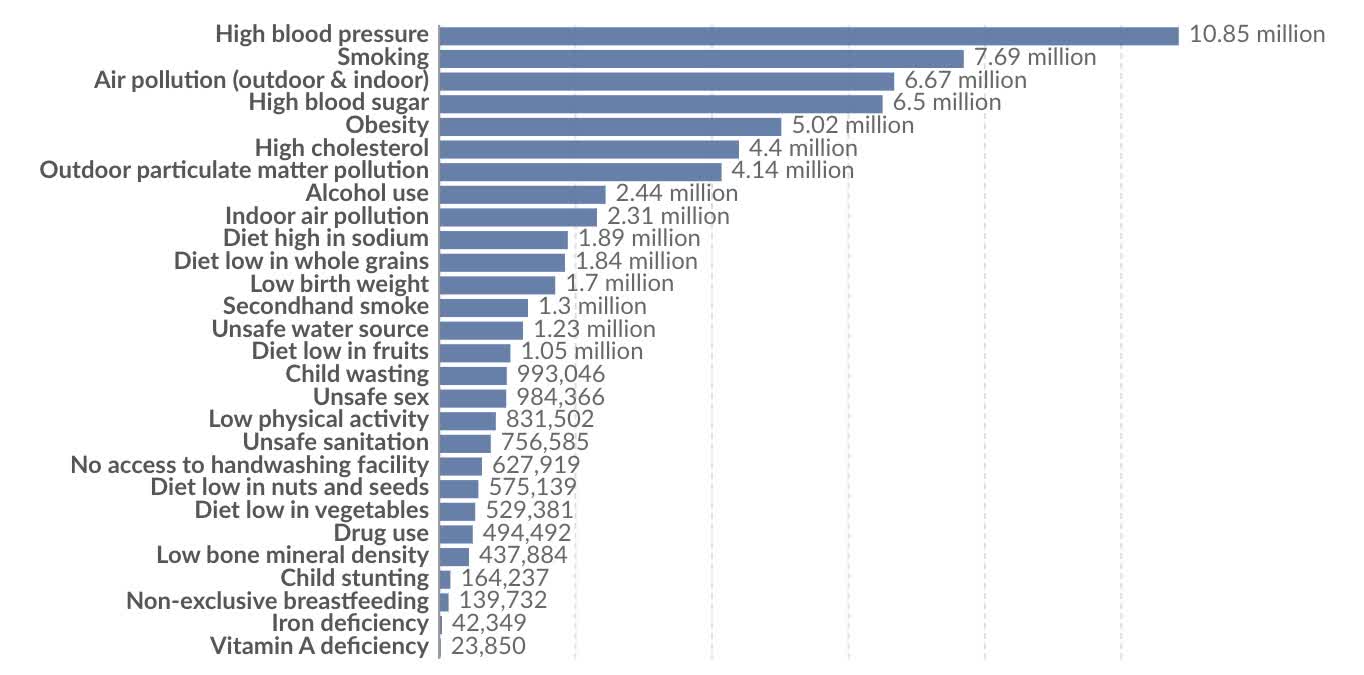

Similar to Altria, the company has been shifting its products away from the traditional smoking sector due to its decline. Over the last several years, smoking has declined and the use of E-cigarettes has risen over the same period. In the last year alone, the use of electronic cigarettes rose to 6% from ~4.5% the year before. A contributing factor for this is that smoking has been linked to a large number of health problems. Below are the leading causes of death from 1990-2019. In 2022, the leading cause of death worldwide was coronary artery disease, also known as heart disease. According to researchers, 40-60% of cases are linked to genetics. And what's also a significant contributing factor? You guessed it: smoking.

{kind=link}

Because of this, it has caused many tobacco companies to shift their focus on alternatives to smoking, largely E-cigarettes. Supposedly this was a less harmful alternative to traditional smoking, but emerging data suggests otherwise. Another reason is the reduced smell and added flavors of tobacco making it socially acceptable. The flavor combined with the lack of smell led to its popularity amongst teenagers. This caused the FDA to step up its campaign against the alternative, citing the use of nicotine in many of the products. This has been a constant fight between the FDA and many tobacco companies over the last several years, and many continue to try to find innovative ways to keep their businesses going.

Slowed Dividend Increases

As previously mentioned, tobacco companies are popular amongst investors because of their generous dividends. Investors looking for income usually look here first when searching for high-yielding investments for their portfolios. Admittedly, the dividend raises have not been as prominent in recent years as investors are used to, but like I always say, "some growth is better than no growth."

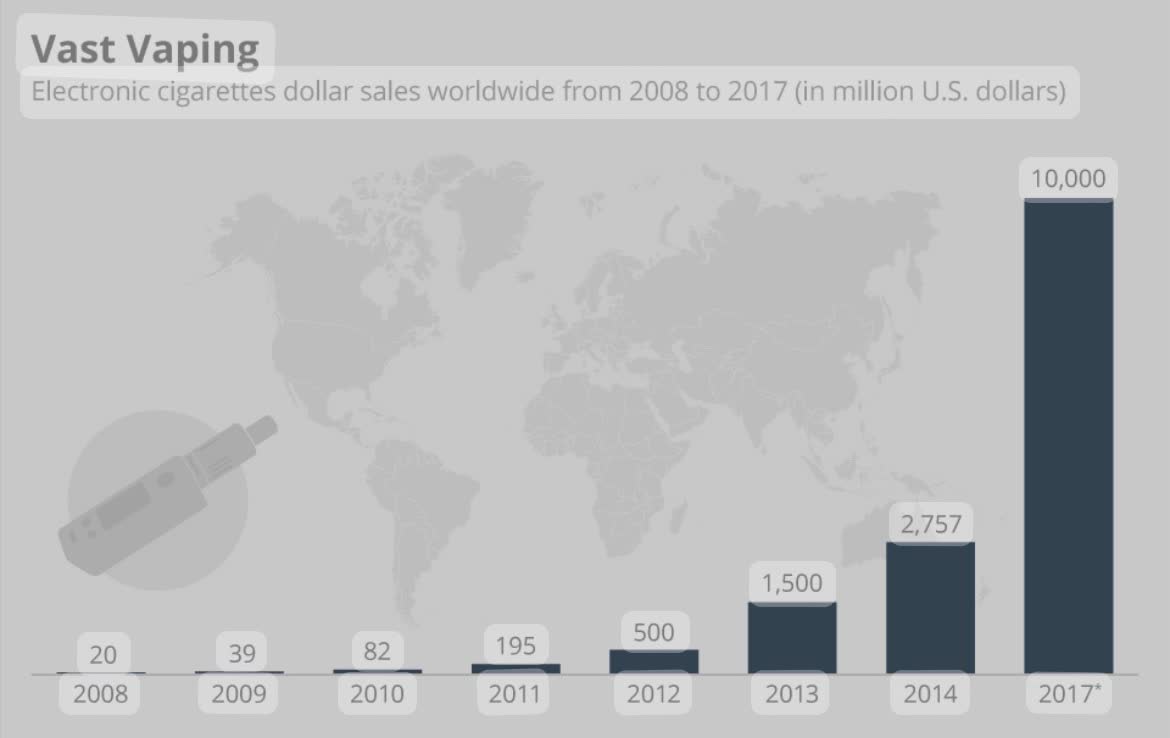

With so much uncertainty and talks of a recession, a pandemic, and a constant battle with the FDA, I think PM has done very well navigating the rough seas. From 2008 to 2014, PM increased its dividend by almost 117%. Since then, the increases have slowed down significantly to just 30% over the last 9 years. Below you can see when vaping really started to become popular worldwide. In 2014, vaping numbers almost doubled from the year before and tripled in 2017. Notice something in common? That's about the time when PM's dividend increases started to slow down, in 2014.

{kind=link}

Like all good businesses, the company had to find innovative ways to move away from traditional smoking. And for a business to invest in its future, that takes cash flow. And cash flow is where those dividends come from, so PM had to make a choice: continue rewarding shareholders with huge increases, or invest in its business while rewarding them with smaller increases along the way. And this has continued into 2023.

Philip Morris' aim is to become a growth company and they made this apparent by raising their organic net revenue forecasts to +7.5 to +8.5. This reflects the momentum of IQOS and the ongoing growth of ZYN. We'll talk about this expected growth a little later in the article.

Impressive Smoke-Free Growth

The company's goal is to fundamentally transform its business to deliver a smoke-free future and to achieve it as quickly as possible. One of the ways the company has been doing this is making accretive investments into the smoke-free segment and distributing those products. PM recently amended its distribution deal with Kaival Brands for the distribution of its vapes. During Q2 earnings , the company posted total cigarette and HTU shipment volume growth of 3.3% for its third consecutive quarter of positive volumes. This contributed to top-line growth and adjusted EPS growth.

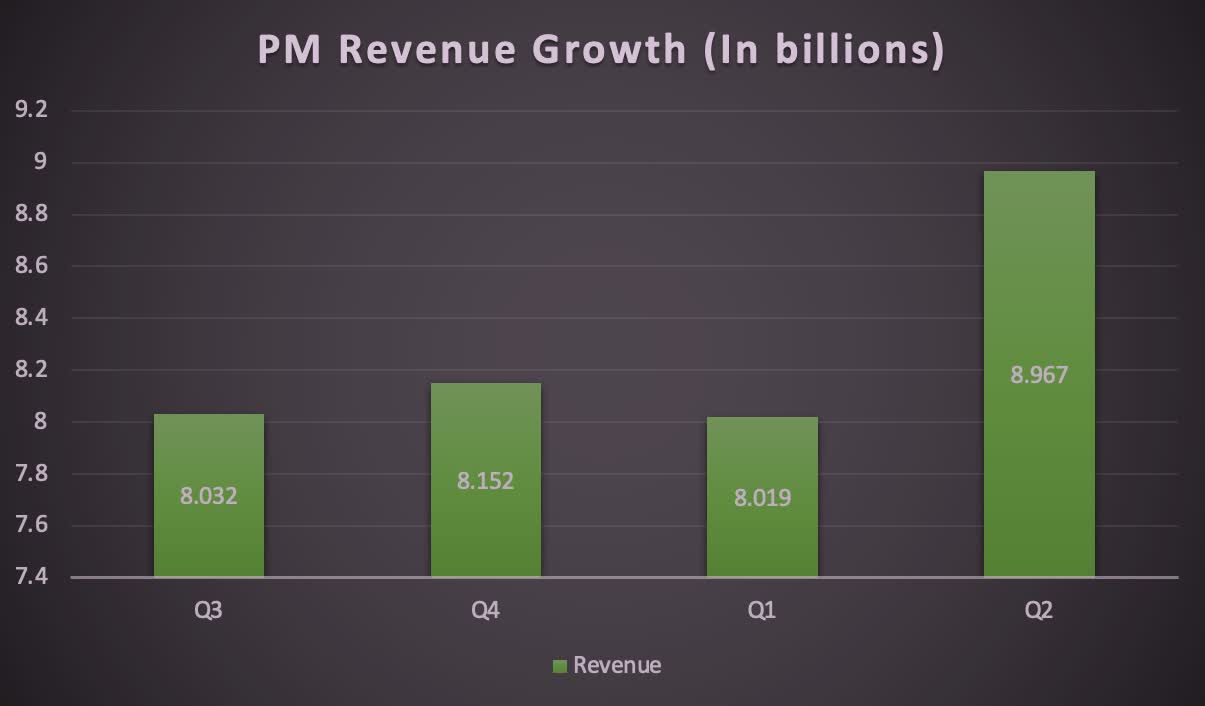

Besides vapes, another growth driver for its smoke-free segment has been its ZYN and IQOS products. U.S. volumes grew over 50%. Organic net revenue also grew 7%, driven by the increasing proportion of IQOS HTUs in the sales mix and combustible pricing. As seen in the chart below the company has posted some strong growth after the Swedish Match acquisition two full quarters ago. Additionally, you can see a slight decrease in revenue from Q4 to Q1. This was because of headwinds due to timing & comparison effects, and the annualization of 2022 excise tax increases in Japan and Germany, but they have since bounced back, posting 11.82% revenue growth quarter-over-quarter.

{kind=link}

Strong Forecasted Growth

Although the tobacco industry is seemingly always in a battle against the FDA, PM and its peers always find new ways for growth. Part of this is due to the inelasticity of the business. With smoking rates on the decline, it's easy for the business to raise prices on its products. Being in the military the last 21 years and having been stationed on many ships, I've seen this first hand. And even though times have changed with the emergence of vapes, I remember non-smokers buying large sums of cigarette cartons to sell to the smokers when we ran out of cigarettes. On deployment, it seemed like 99% of the time we would always run out. And smokers would lose it as they would have to wait for the next port visit before they could pick up their favorite brands. And people would pay big bucks for them. I've personally know someone who paid $50 for a pack of cigarettes on deployment, so saying the business is inelastic is an understatement.

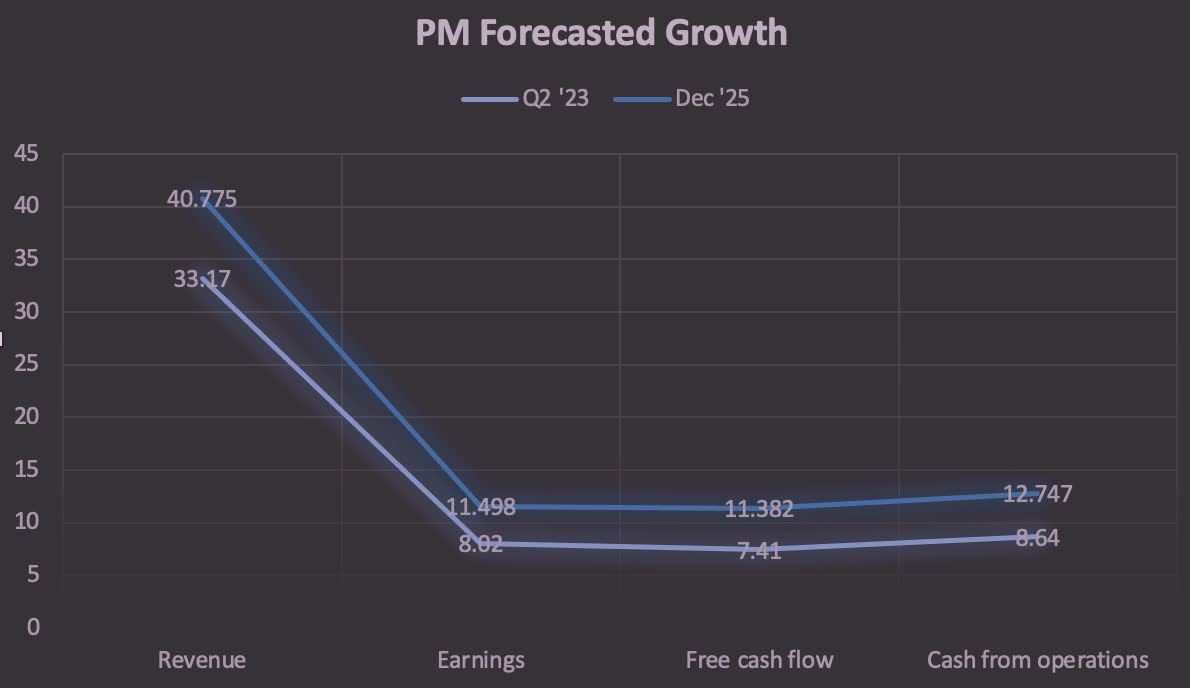

PM is expecting double-digit growth over the next two years. Revenue is expected to grow by nearly 23% from $33 billion to $40.7 billion and earnings are expected to grow 43% from $8 billion to $11.5 billion by 2025. Furthermore, cash from operations & free cash flow are expected to grow by double-digits as well to $12.7 billion and $11.4 billion, respectively during the same period.

{kind=link}

PM Stock Valuation

Alright let's calculate PM's intrinsic value to get an acceptable buy price using the Dividend Discount Model ((DDM)). Due to the current macro environment and uncertainty with interest rates, I decided to be slightly conservative. Over the past 5 years PM has an average annualized total return of 11.3% and a dividend growth rate of 4% over the same period. With interest rates to remain high and the threat of a recession I decided to go with an annualized dividend for next year of $5.28 or a $0.02 increase to next year's dividend. Again I'm being conservative here. Expecting a 10% annual return and a 5% DGR, I have a price of $105. The stock is currently trading at $95.25 at time of writing, making it a buy. Analysts have an average price target of $113 offering investors roughly 19% upside from here.

Risks

Tobacco companies will face continual pressure from the FDA, their biggest risk. With vaping and smoke-free products popular amongst the younger generation, this will be a constant uphill battle. There's also the risk of a healthier environment. Consumer trends are constantly shifting towards health & wellness. There's also the threat of a recession. Recently, oil prices have surged and CPI has risen at an annual rate of 2.4% in the last 3 months. Some are reporting the chances of a recession at 33%, a drop from 50% earlier this year. Although the market is pricing in more than a 90% chance the Fed holds rates at the next meeting, another hike or two could be the final tipping point to push the economy into a recession. This will cause consumer spending to be even tighter which could have an effect on PM's earnings going forward.

Conclusion

Although PM's dividend growth in the last few years hasn't been what investors are used to, the company's smoke-free segment posted impressive growth as seen in their Q2 earnings report. Earnings are expected to grow by double-digits by December 2025 and the company remains focused on transforming the business to deliver a smoke-free future. I believe the company is currently undervalued and offers investors great upside to its average price target.

Due to their inelastic business model and innovations, I rate Philip Morris stock a buy and think it offers investors stable income for the long-term. For now, I own its peer Altria but think PM is a great alternative and may consider opening a position in my retirement portfolio due to its valuation.

For further details see:

Philip Morris: The Smoke-Free Segment Future Looks Bright