SEMHF - Philips: A Healthcare Leader But A Very Risky Investment

2023-09-20 04:18:33 ET

Summary

- Philips faces significant challenges and controversies, including the results of a forced recall of ventilators and respiratory devices, leading to financial provisions and damage to its brand reputation.

- The company remains a major player in the healthcare equipment market, which should drive growth of mid-single digits through the end of the decade.

- It has ambitious financial targets and margin expansion goals, driven by its commitment to innovation and cost-efficiency improvements.

- Philips faces financial headwinds, with a weak balance sheet and ongoing lawsuits related to the recall issue.

- Despite its growth and margin improvement potential, the current risks and overvaluation suggest there may be more attractive investment opportunities in the market.

Investment thesis

I initiate my coverage of The Koninklijke Philips N.V. ( PHG ) with a Hold rating following my in-depth research of the company and the underlying healthcare equipment industry.

While once a prominent player in the market, Philips has faced significant challenges and controversies over the last couple of years, leading to a disappointing performance for its investors. The forced recall of ventilators and respiratory devices due to toxic foam issues has been a major setback, resulting in significant financial provisions and damage to the company's brand reputation. Furthermore, the case is still far from resolved, with more lawsuits hanging over Philips’ head, which brings with it significant financial risks, requiring a discount to peers.

Despite these challenges, Philips remains a major player in the healthcare equipment market through its Diagnosis & Treatment, Connected Care, and Personal Health segments. The company has ambitious financial targets and margin expansion goals, driven by its commitment to innovation and cost-efficiency improvements.

However, Philips faces financial headwinds, with a weak balance sheet and ongoing lawsuits related to the recall issue. The company's order intake growth has been lackluster compared to some of its peers, raising concerns about its ability to meet its growth targets.

While the company has a solid long-term growth outlook and potential for margin improvements, the current risks may outweigh the potential rewards for investors. The company's overvaluation by approximately 10% suggests that there may be more attractive opportunities in the market.

In this article, I will take you through my analysis of the company and the underlying industry, as well as the latest developments and financial projections.

Philips Koninklijke - An introduction

The once much larger Philips Koninklijke might not be a company investors hear from or see daily. With a market cap of slightly below $20 billion and operating in a massive industry with much larger players, it's hard to come across the company. Also, performance-wise, the company generates little headlines. 2022 revenue sat slightly below the 2009 level and its net income development does not offer much reason for enthusiasm either.

{kind=link}

Philips revenue (Statista)

The Philips we know today is a far cry from the size and broad portfolio it once had. Today, the company fully focuses on the healthcare equipment market through its Diagnosis & Treatment, Connected Care, and Personal Health segments. Philips is a leading player in the healthcare industry, providing a wide range of cutting-edge medical devices, solutions, and services. This ranges from state-of-the-art imaging equipment to telehealth solutions and patient monitoring systems.

Philips remains a company with innovation in its DNA. The company always pushes for innovations in the healthcare industry, and whereas this has put them at the forefront of the healthcare equipment industry, it also exposes them and their equipment to controversy. Philips has seen its fair share of operational issues and controversies over the last decade, which, with the addition of a number of spin-offs, has led to it turning out as a disappointing investment, with shares down over 30% over the last decade.

However, while financial growth was far from perfect, the real issues started in 2021. Up until that point, investors who had bought the shares at the start of the decade would have doubled their investment while receiving a decent dividend. However, after the COVID-19 pandemic, shares fell from an April 2021 high of $60 to a low of $12,60 back in October last year.

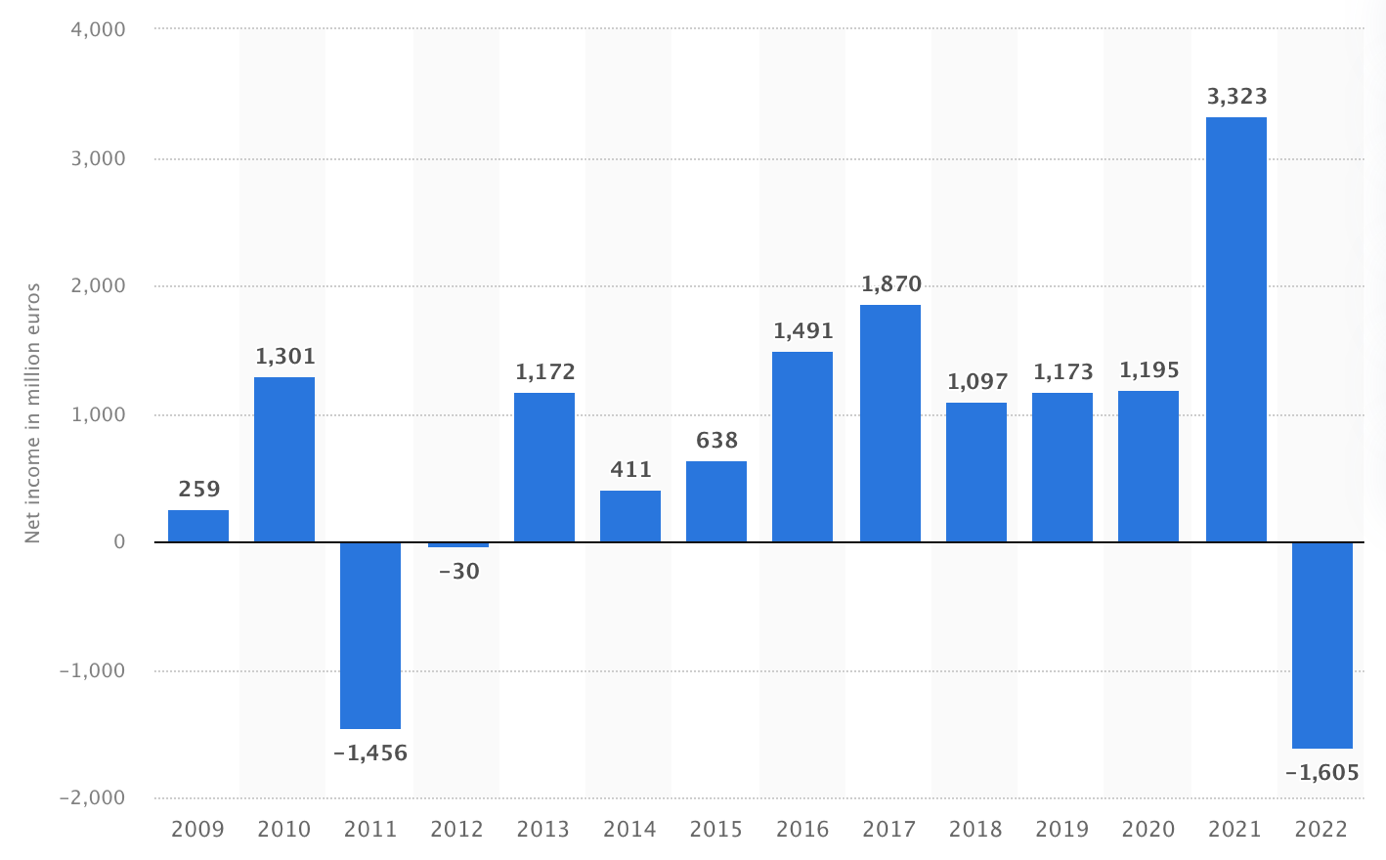

This significant share price decline can be attributed to two leading factors, which are the company’s operational struggles due to significant supply chain issues, inflationary pressures, and a very weak Chinese market due to COVID-19 lockdowns, resulting in an operational loss in 2022, and second, the massive forced recall (By the FDA) of ventilators and respiratory devices because of a toxic foam breaking off inside the machines, which cost the company over a billion dollars so far and damaged the company’s brand name. The combination of both of these factors has weighed heavily on the share price in recent years and for good reasons.

{kind=link}

Philips net income (Statista)

However, results from the past offer no certainties for the future, which is a positive in the case of Philips, and with the company working (and making good progress) on resolving the ventilators and respiratory devices issue and lawsuits, it might finally become more interesting to investors again, especially after the significant share price drop over recent years. So, let’s dive a bit deeper into the company’s growth potential, financial health, and opportunities that lie ahead in order to determine whether Philips is an interesting investment opportunity today or should still be avoided at all costs.

The respiratory recall issues are significant and far from being solved - The brand damage and financial provisions are significant

Let’s start with the elephant in the room for Philips, which is the forced recall of ventilators and respiratory devices because of a toxic foam breaking off inside the machines. The company has recalled around 5.5 million devices worldwide (of which 2.5 million from the US) used to treat sleep apnea in 2021 because foam used to dampen noise from the devices can break off and be inhaled by the user, becoming toxic and carrying potential cancer risks. According to Bloomberg, Philips had set aside $1 billion to cover these costs.

However, the problem has by now become much worse than just a product recall as earlier this year, the FDA had classified the recall as the most serious type as the devices may cause serious injuries or death, which, according to Philips, is not the case. This exposes Philips to extensive legal problems. Furthermore, according to the NY Times , Philips was aware of this problem with the foam breaking off in 2015 but chose to ignore it. Also, the whole situation was miserably handled by the company, deceiving investors for over a year as it failed to properly inform them if it provided information at all.

Since April 2021, when Philips released the first warning of the problem, the FDA has received 98,000 complaints from Philips ventilators and respiratory device users. Some complaints included reports linking the devices to cancer, respiratory problems, pneumonia, chest pain, dizziness, and infections. The FDA even linked 346 deaths to the foam problems. Structural evidence for these accusations is hard to come by, but it sure does not make Philips look any good and it has led to several legal claims.

To avoid significant lawsuits, Philips recently announced an agreement to settle certain legal claims in the U.S. related to the recall of sleep apnea and respiratory care devices. The initial payment is $479 million but can rise further depending on how many claimants will take up the deal and how much the court will award as professional fees. Furthermore, this only resolves all economic loss claims in the U.S. Multidistrict Litigation, so any claims regarding personal injury or medical monitoring claims are excluded and still outstanding.

Philips has already recognized a provision of $615 million to cover the final settlement, so this agreement will not further hurt its financial results in future quarters. Crucially, Philips continues to deny “any admission of liability, wrongdoing, or fault by any of the Philips parties.”

According to Philips’ own assessment (through three independent testing laboratories) of the possible device flaws, 95% of the recalled devices showed no signs that these could pose any appreciable harm to the patients. The company confirmed that the foam inside the machine could get detached but, when inhaled, would unlikely cause appreciable harm to the patient.

Looking ahead, despite the recent settlement, the company still faces other legal actions over the recall, including personal injury claims, as well as an investigation by the U.S. Department of Justice. Lawyers working on the case have said they will continue to pursue personal injury and other claims against the company. Problems are far from over for Philips after already costing up to $1.5 billion so far. Some analysts believe these claims for injury and health damage could bring the total damage to €4 billion .

And the damages reach further than just immediate financial costs. Philips holds a 63% market share in the Respironics device market. Furthermore, the sleep apnea market is projected to grow at a CAGR of 5.9% through 2028, making it a very important and exciting market for Philips. However, recent controversy as explained above will almost surely hit its market share and growth potential in the market. A large number of patients will now opt to go with another brand for their apnea device. This will be a setback for Philips and the accusation of your devices causing cancer or even death is hard to overcome in terms of customer trust.

Today, the whole apnea device controversy is far from over for Philips and damage claims could run up much higher still. Eventually, it could cost Philips multiple billions while also damaging its brand reputation and trust, at least in the apnea equipment market. I am expecting this entire issue to remain a drag on the company's financial and share price performance due to market share losses and further legal settlements. Investors should closely monitor any developments.

Fundamentally, the company is not in horrible shape

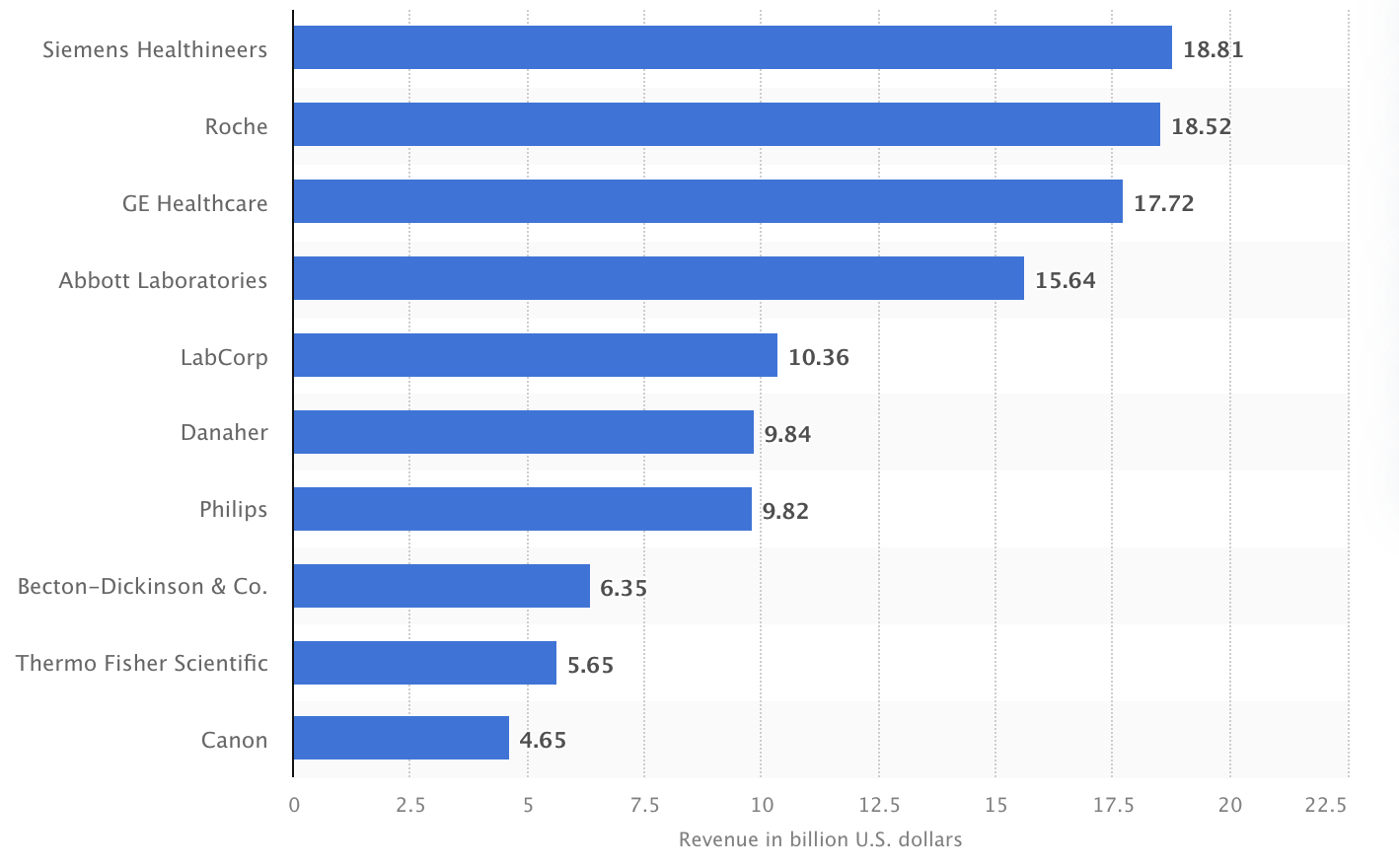

Despite the above-explained legal issues and damaged brand reputation, the company is still one of the largest medical equipment makers worldwide, as it plays an important role in the very lucrative healthcare market. The medical equipment market is projected to grow at a CAGR of around 6% through 2030, driven by global trends like an aging population, increasing costs, and a growing need for data insights.

{kind=link}

Sales peer comparison (Statista)

To better understand the company’s operations, Philips operates three segments: Diagnosis and treatment, Connected Care, and Personal Health. The Diagnosis & Treatment segment is the largest, accounting for 49% of its sales. The goal of this segment is to “support precision diagnosis and minimally invasive treatment in a growing number of therapeutic areas such as cardiology, peripheral vascular, neurology, surgery, and oncology,” through diagnostic imaging, ultrasound, and image-guided therapy equipment.

The second largest is the Connected Care segment, which accounts for 29% of sales and focuses on “ambulatory, home-based and in-hospital monitoring and workflow solutions fueled by advanced interoperability and patient data insights.” The segment designs and manufactures equipment for health monitoring and sleep & respiratory care.

Finally, the Personal Health segment accounts for 20% of sales and consists of a broad range of consumer products like shaving equipment and many other products. This is the only consumer-focused part of the business remaining after spinning off its light business in 2018.

According to Statista , this gives Philips a market share in the global MedTech market of around 3% as of 2021. However, this share is expected to drop slightly by 2028 due to faster-growing competitors and Philips operating in healthcare equipment segments that are projected to grow slightly slower. Still, according to Philips, its segments should report 3-6% annual growth. Looking at the company’s products, I expect this growth to sit slightly more on the low end of the range guided by Philips. Positively, Philips does hold the #1 or #2 market position in most of its product segments, giving it an edge over the competition in terms of pricing.

Diving further into the company data, we can see Philips generated €18.4 billion in sales in the last four quarters. 40% of sales came from recurring revenues, which increases company stability and resiliency. This is a big plus and makes it an interesting defensive play. For clarification, these recurring sales mainly consist of service revenues.

The company is still active in over 100 countries. Philips generates 43% of its sales in North America, followed by Western Europe in which it generates 20% of its sales. Furthermore, the company generates 28% of its revenues in emerging regions, boosting its overall growth. I believe this revenue diversification is strong as the company is not overly dependent on a single region and has solid exposure to faster-growing economies to boost growth—another positive.

Furthermore, the new CEO could possibly provide a new wind at the company after 12 years under CEO Frans van Houten, who was held responsible for the respiratory debacle as Philips stayed silent on the problem for too many years and poorly informed investors on the size of the issue in recent years. The company handled the whole situation in a miserable way, deceiving investors for over a year. The situation had given investors little confidence in management’s capabilities, so the CEO switch was inevitable and highly necessary.

Many investors and analysts hoped for an outsider to come into the company to restructure it and help it recover from issues in recent years. This would make a lot of sense after management bluntly completely failed in recent years. However, in October last year, Philips appointed Roy Jakobs to succeed Frans van Houten.

Roy Jakobs has worked at Philips for 13 years and prior to its appointment as CEO he was the Chief of the connected care segment. He looks well suited for the job but an experienced CEO to righten the ship could have been a better choice at this point in time. Still, I am glad about the CEO change and believe it could bring new opportunities to Philips. However, it will take some time and dedication from the new CEO to win over investors’ confidence again.

Finally, the company currently employs approximately 72,000 employees, but after already announcing the reduction of its workforce by 4,000 roles in October 2022, it aims to streamline the business further and cut another 6,000 by 2025, of which 3,000 in 2023. This should meaningfully help Philips save costs and make the business leaner—another positive development to drive improved cost efficiencies, which the company definitely needs.

On that note, let’s look closer at the growth expectations, recent results, and the company’s financial health.

Ambitious financial targets and significant margin expansion potential but a weak balance sheet

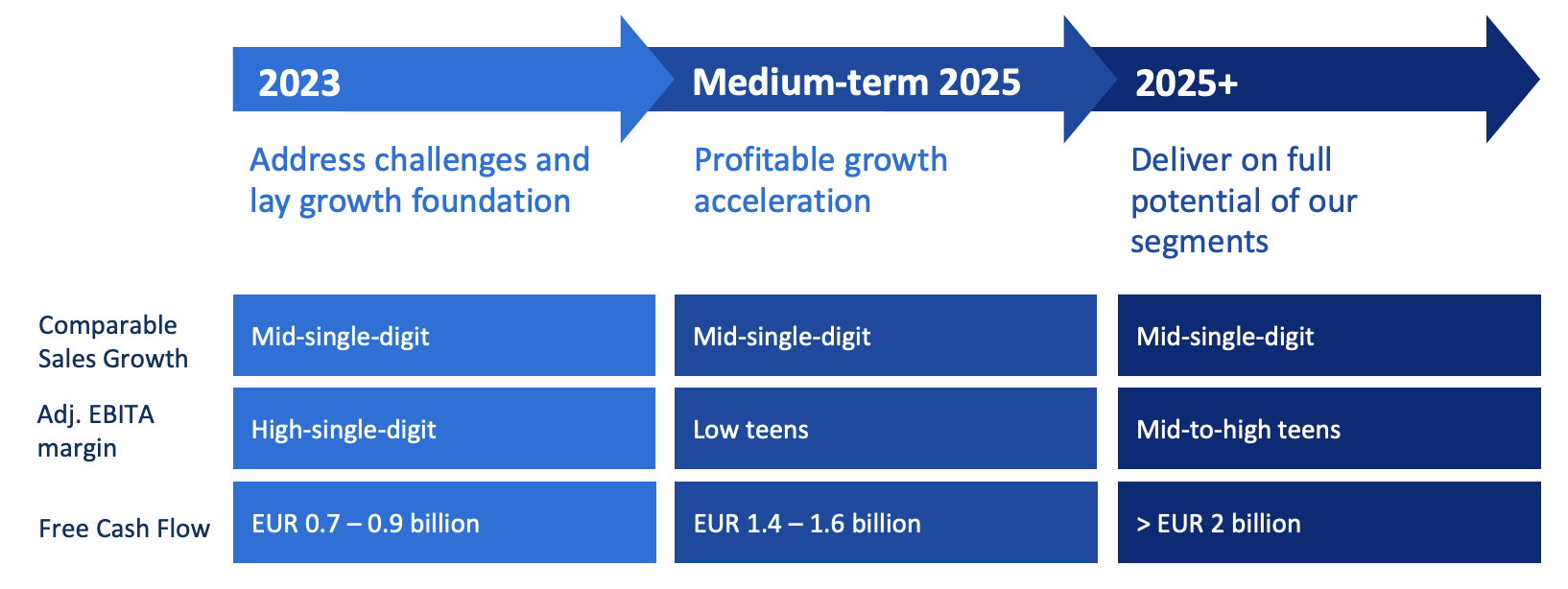

Cutting right to the chase, Philips aims to improve its performance to mid-single-digit comparable sales growth with a low-teens adjusted EBITA margin by 2025 and the EBITDA margin to improve to mid-to-high-teens beyond 2025. Also, the company remains committed to its innovative nature and wants to invest a minimum of 9% of sales into R&D, of which 90% will be focused toward product development to drive technological innovations.

{kind=link}

Financial targets (Philips)

These financial targets highlight management’s goal of significantly improving its financial profile over the next few years. Supporting its growth potential is management’s conviction in improving its supply chain in order to make it more reliable. An unreliable supply chain has been massively impacting Philips over recent years and has been a leading factor in its disappointing performance. Its supply chain was a mess and this caused a shortage in electronic components. As the supply chain has been improving over recent quarters, so has the financial performance. However, looking at the latest financial results, not everything indicates a strong outlook.

For its latest quarter, Philips reported sales growth of 9% YoY, which is a strong quarter sales-wise. Also, in terms of profitability, Philips had a strong Q2 as it saw improvements in profitability and cash flows. A Q2 EBITDA margin of 10.1% was a significant improvement YoY of 490 basis points and net income turned positive from a negative €20 million reported last year to a positive €74 million in Q2. So far so good, right?

However, Philips reported an order book, which was up by only 3% YoY. The order intake was down 8% YoY. Even when excluding the impact of the company leaving Russia, this was down 4%, which is not boosting my optimism for future growth. There are few excuses for negative growth in orders as the industry remains resilient and supply chain struggles do not impact the order intake.

One of the possible reasons that Philips does point to is cautious buying behavior by hospitals and healthcare systems in the US and other mature geographies due to cost inflation, a shortage of staff, and general macroeconomic conditions. Furthermore, according to Philips, its order intake remains healthy, and the low YoY change is mainly due to a higher sales conversion and growth in sales, as well as a tough comparison to last year. However, this last point is hard to agree with, as the 2Q22 order intake was only up 1%.

The other excuses from management I can get behind and I can see why this might pressure orders up to a point. However, looking at peer results in Q2, these saw a much better order intake as Siemens Healthineers ( OTCPK:SMMNY ) reported a book-to-bill of 1.21 and GE HealthCare ( GEHC ) organic order growth of 6% YoY , while both also reported solid sales growth. Again, this is a negative indication of future growth and of lower demand for the company’s products. The order book and order intake are essential for 40% of Philips’ sales, as the other 60% comes from recurring revenue. On a slightly more positive note, Philips believes it should be able to accelerate the order intake in the second half of the year to once again start reporting positive growth.

Overall, I believe the company’s financial targets are really respectable and, considering the company’s portfolio, also highly likely. However, this will demand a better order intake in the next few quarters. If the order intake remains suppressed, it will be tough for Philips to match its growth targets.

As explained before, the healthcare equipment sector is incredibly interesting, with a lot of potential for stable and reliable growth due to several global trends. Philips, as one of the leading suppliers of medical devices and through its recurring service revenues, should be well-positioned to benefit. Therefore, mid-single-digit sales growth should be achievable, although the range will be sitting slightly lower at 3-5%. Still, I believe this is nothing to complain about for a company like Philips, although I also want to add that there might be better opportunities out there as several of its peers have a meaningfully better growth outlook.

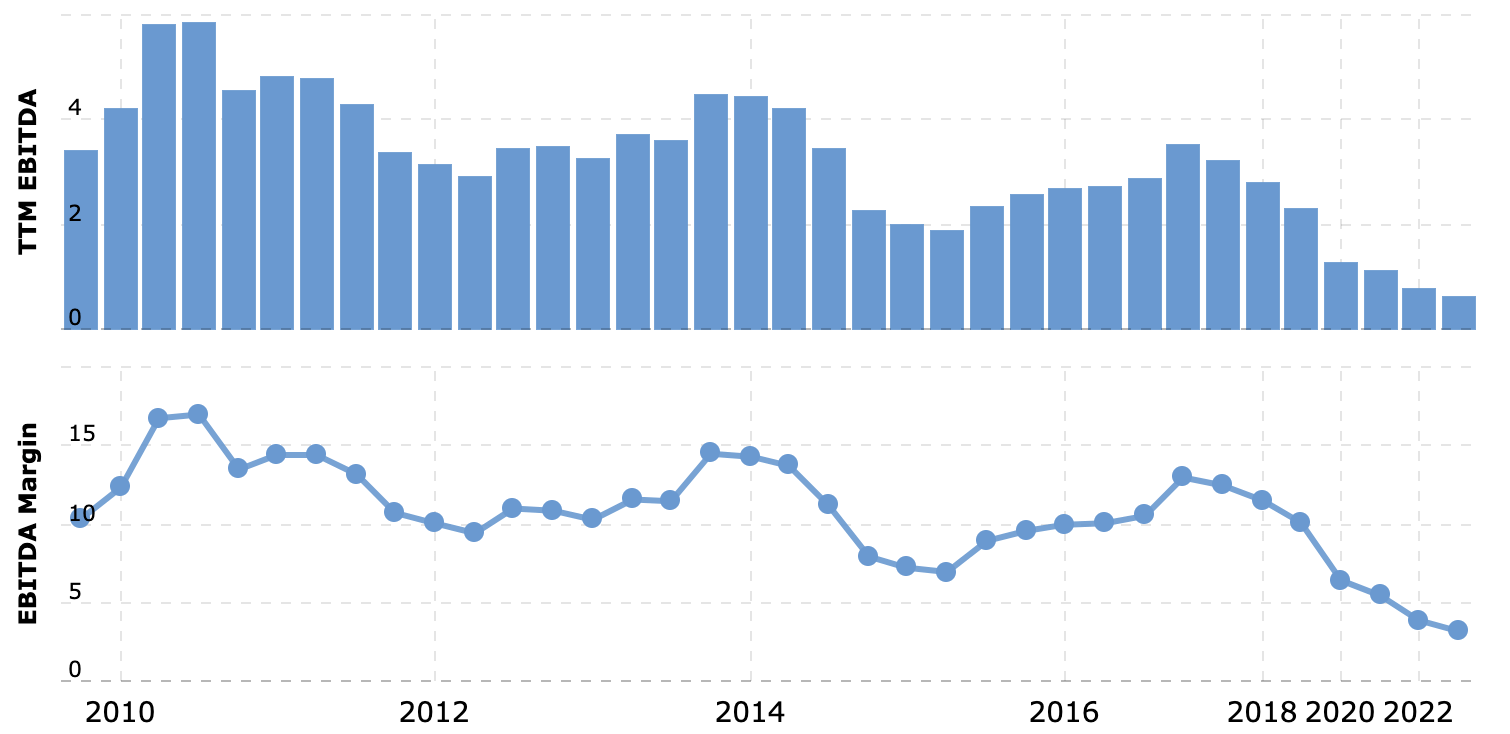

In terms of margins, the company is quite bullish on its potential margin developments. Its EBITDA margin over the last couple of years has been significantly below its historical average, which should not come as a surprise as sales were also down considerably.

{kind=link}

EBITDA development (Macrotrends)

Philips’ EBITDA target in the low teens by 2025 would put the margin on par with its average over the last decade, which indicates significant improvement from recent levels but is still far from impressive for long-term shareholders. However, the EBITDA target of high teens after 2025 sounds much more promising and points to significant margin improvements in the future.

Whether Philips can achieve this is, of course, hard to say today, but looking at its current operating cost structure, I do see plenty of room for efficiency improvements. Over the last decade, Philips management has had little focus on improving cost efficiencies, but this looks to be changing under the current CEO, which is a promising sign. These margin targets by Philips are realistic if management executes them correctly. The incoming personnel changes through significant layoffs are a good start. As a result, in terms of efficiency and margin potential, I am quite bullish, in part driven by new management.

In terms of financial health, Philips has looked better. The company currently holds a net debt position of €7.3 billion. It has a total debt of €8.2 billion, of which €1 billion is short term and total cash of €1 billion. Normally, I would be fine with this balance sheet as it should cover the company’s obligations just fine. However, in the case of Philips, which is facing further financial headwinds through the earlier discussed lawsuits hanging over its head, the current financial position is very tight, as also highlighted by the fact that the company now pays its dividend in shares.

Yes, the company has already put $1.5 billion aside, but it simply does not have the financial resources to cover further financial settlements. These would have to be financed through more debt, which is also far from ideal in the current high-interest climate.

From that perspective, Philips is not in terrific financial health, and further financial settlements to avoid lawsuits could hurt it quite a bit. A reported FCF of €5 million in Q2 is also not helping in the slightest to improve this. However, the situation for Philips regarding cash flow is improving rapidly.

In the period 2016-2019, prior to the COVID crisis and financial struggles for Philips, the company was able to generate FCF of around €1.5 billion , which could be an indication for the next couple of years. If the company is able to report such cash flows over the next couple of years again, this could improve its financial health, but if not, I see little room for positivity here.

Also, this will leave very little room for shareholder returns. The company can simply not afford it. I expect it to increase its debt position significantly over the next couple of quarters/years, depending on the financial pain it suffers from the sleep apnea lawsuits.

Outlook & PHG stock valuation

Following the solid Q2 results, Philips raised its FY23 outlook, albeit from an extremely low estimate. Therefore, the FY23 increase was expected, and there is no particular reason for enthusiasm. Management now expects FY23 sales growth of mid-single digits, in line with its long-term growth targets, and the EBITDA margin to sit at the high end of the high-single-digit guidance. Management expects the positive sales momentum to continue in the year's second half.

Following the Q2 results, management’s long-term growth targets, and my in-depth research of the company and the underlying industry, I expect the company to report the following financial results through 2026.

{kind=link}

Financial projections (By Author)

These estimates mean Philips is currently valued at a forward P/E of approximately 15.5x, which sits 43% below its 5-year average of 22. Generally, healthcare stocks tend to trade at a premium to the index as these offer incredible stability and resilience no matter the state of the economy or the rate of inflation. The same could be said for Philips and its peers, as demand for its products should always remain solid and its service activities highly necessary.

However, in the case of Philips, it is hard to award such a valuation premium today considering its economic health and the risks of further financial damage following the apnea devices recall factors that have come into play or deteriorated over recent years, explaining the difference to its 5-year average valuation. Also, these factors are the reason why shares are valued below peers GE Healthcare (18x) and Siemens Healthineers (22x), and rightfully so.

So, while the sales, EPS, and margin outlooks might be looking solid, the financial profile of the company, its large debt position, the overhang of more lawsuits, and negative order intake growth require a significant discount to peers and its averages.

Considering the company’s current position and financial risks, I believe shares should be valued no higher than 14x earnings in order to create a sufficient risk-reward profile. Based on this belief and my FY24 EPS estimate, I calculate a target price of €21 ($22.50) per share. Going with an annual return of 10% per year, I believe the current fair value sits around €17.90 per share, meaning shares are currently 10.5% overvalued.

Conclusion

While Philips might not have been a very strong investment over the last decade and while I view the respiratory issues as far from resolved and possibly hitting it quite significantly financially, I do believe the company’s long-term growth potential in the healthcare equipment market is looking quite solid as the company’s competitive positioning is looking good. The same can be said about potential margin improvements over the remainder of the decade, for which there seems to be plenty of room.

However, despite this solid outlook, I believe the risks of an investment are currently simply too high for investors, mainly due to the remaining financial risks involved with the apnea device recall and remaining lawsuits, especially when considering the company’s weak balance sheet, which leaves little room for further setbacks.

Taking all these factors into consideration, shares seem to be overvalued by around 10% as I believe investors could consider taking on the risks at a share price of below €18 per share. At current prices, I see many more attractive opportunities in the market and, therefore, see no reason to buy Philips shares today. However, as the overvaluation is limited and the outlook solid, I rate shares a hold for now but recommend existing shareholders to keep a close eye on any developments.

For further details see:

Philips: A Healthcare Leader But A Very Risky Investment