RYLPF - Philips: Compelling 5% Yield As Q4 Earnings Confirm Financial Turnaround

Summary

- Philips reported its Q4 earnings, which beat estimates.

- Several announced restructuring efforts and productivity initiatives are expected to support margins and profitability going forward.

- We like the stock, which has room to climb into an improving outlook while shares yield 5%.

Koninklijke Philips N.V. (PHG) has faced a challenging last couple of years going back to the disruptions during the pandemic followed by manufacturing bottlenecks as a theme in early 2022. The company was also caught up in a major safety recall and ongoing litigation related to its "Respironics" unit which added to financial setbacks. In response, a new CEO and management team announced a series of productivity initiatives which we covered in an article back in October. The update today highlights that many of those steps appear to be working.

Indeed, Philips just announced its latest quarterly results with sales and earnings both solidly beating market estimates. Our take is that the report goes a long way to confirm a real operating and financial turnaround. Even as management noted ongoing uncertainties at the macro level, the path is for a "leaner and more focused organization" that we believe is well-positioned to generate stronger profitability over the long run. The stock has gained momentum in recent months and we see more upside through 2023. We also see value in the stock's 5% dividend yield.

PHG Earnings Recap

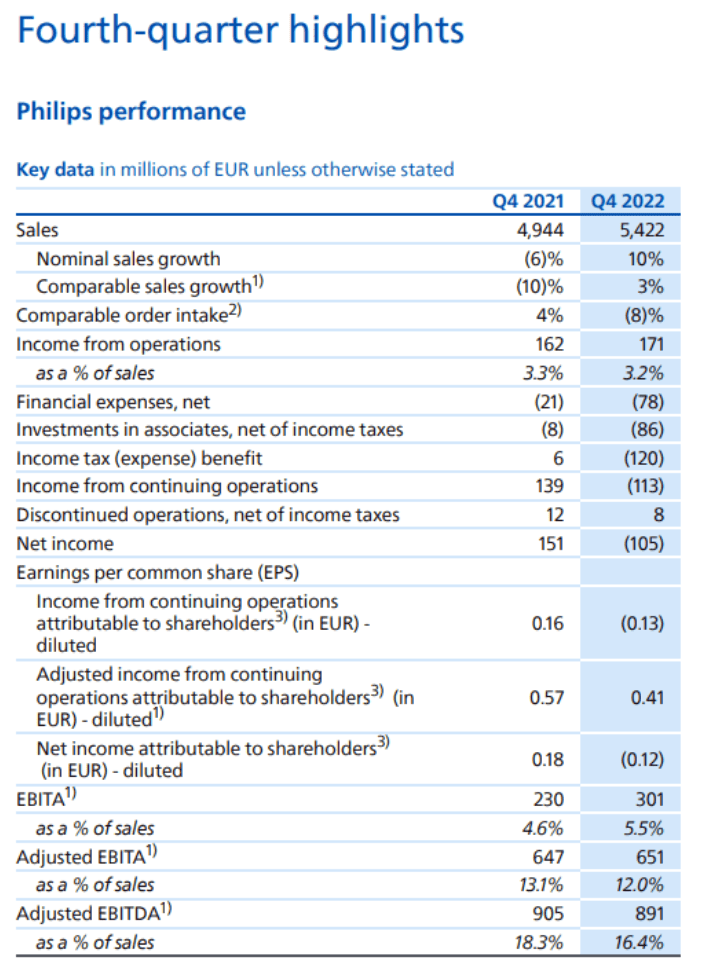

Philips reported Q4 non-GAAP EPS of EUR 0.41, which came in at EUR 0.23 ahead of estimates. Total revenue at EUR 5.4 billion, climbed by 9.7% year-over-year and was also EUR 390 million above consensus. As a Netherlands-based company, the results captured an FX benefit considering the strong Dollar and the proportion of sales outside the Eurozone. Nevertheless, group sales were also higher by 3% y/y on a comparable basis .

{kind=link}

source: company IR

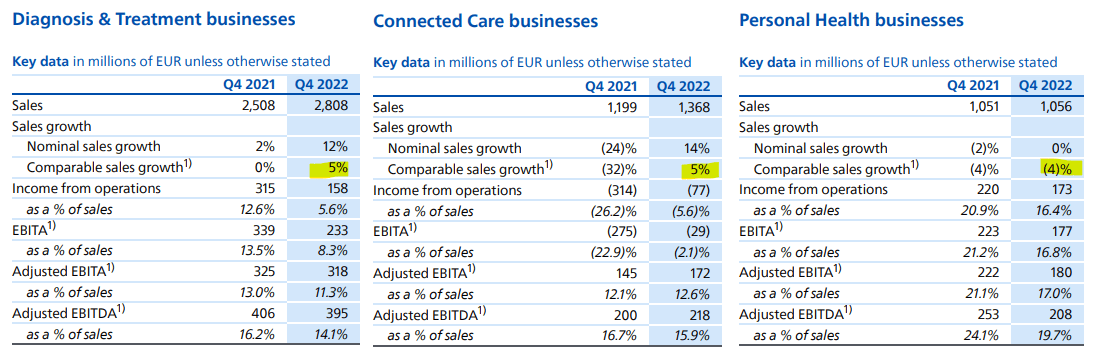

The relative strength was supported by "improved component supplies" for particular products including high-profile items like in-hospital patient monitoring, image-guided therapy, and ultrasound.

The North American market was a strong point, balancing softer trends from Europe. By segments, Diagnosis & Treatment along with Connected Care, both delivered 5% comparable sales growth. The Personal Health business faced a decline of -4% with Covid lockdowns in China limiting sales during the quarter.

Adjusted EBITDA at EUR 891 million was nearly flat from the EUR 905 million level last year, although significantly higher from EUR 461 back in Q2 which at the time drove a sharp selloff in the stock. On the other hand, the adjusted EBITDA margin of 12% was lower than 13.1% a year ago. Management noted ongoing cost pressures that are expected to continue, partially being balanced by recent price hikes.

{kind=link}

source: company IR

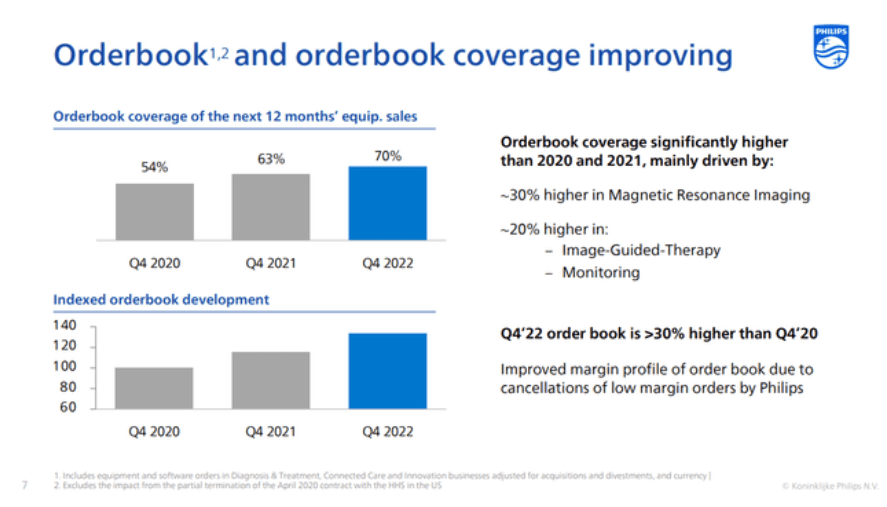

One of the main points of discussion during the earnings conference call was the trend from the order book. The headline confirms that the "comparable order intake" declined by -8% year over year. Management explains that some of that softness reflects the lower demand for Covid-19 acute care products as the emergency phase of the pandemic winds down.

The more important read is how it ties into the company's restructuring efforts. One of the steps is to streamline the product mix towards high-margin items. By this measure, management sees the order book as strong, focusing more on metrics like the "order book coverage" which improved to 70% from 63% at the end of last year, reflecting a tilt towards more valuable equipment. The trend is also evident in the "indexed order book development", which is 30% higher than in Q4 2020 with the elimination of low-margin orders.

{kind=link}

source: company IR

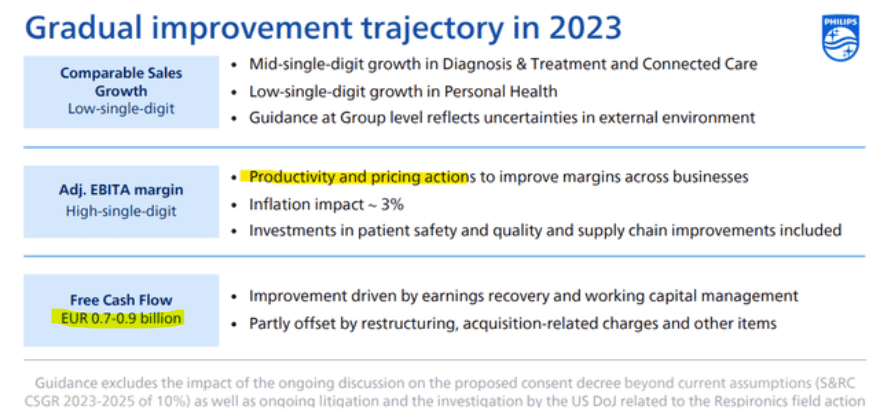

All these tie into an expectation for an improving operating and financial backdrop through 2023. Management is guiding for comparable sales growth in the "low-single-digits" while the adjusted EBITDA margin stabilizes in the "high-single-digit" with a stronger shift in the second half of the year. A headcount reduction of 4,000 employees along with improvements to its supply chain is expected to save EUR 500 million per year compared to 2021 levels.

{kind=link}

source: company IR

PHG Dividend

It's worth mentioning that the company proposed its latest annual dividend of EUR 0.85 per share, consistent with last year's payout. The gross payout for ADR shareholders of approximately $0.90 implies a 5% yield on the stock. A record date or payment date has not yet been announced. We believe the payout is sustainable at the current level for the foreseeable future looking out toward 2024.

What's Next For Philips

When looking at PHG, keep in mind that this was a distressed name just a few months ago with real concerns regarding its financial position. We mentioned the new CEO who took office in October. It might be too early to claim "Mission Accomplished", but it's clear there is a new sense of stability supported by the credible ongoing restructuring efforts based on these latest financials.

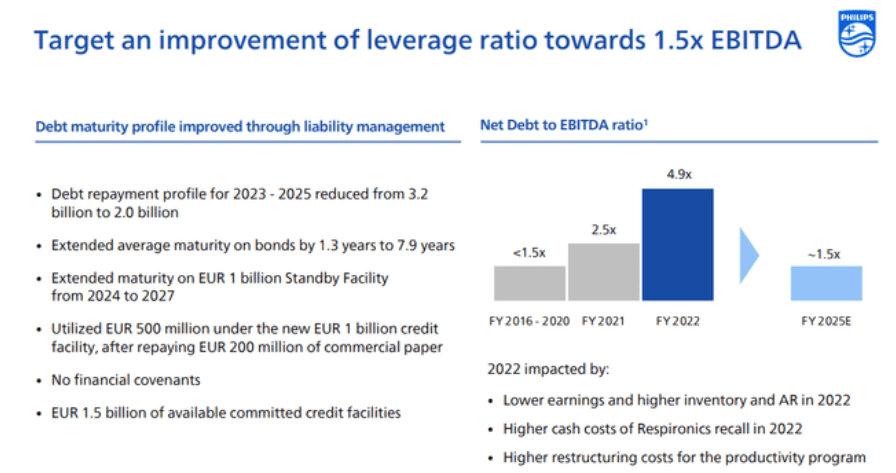

Philips ended the year with a net debt of EUR 7 billion with a leverage ratio of 4.9x, which nearly doubled since 2021. That said, if we simply annualize the Q4 adjusted EBITDA level to EUR 3.6 billion for the year ahead, the implied leverage ratio already improves to just under 2x. Management expects that to ultimately trend towards 1.5x through fiscal 2025. This is likely the most important development now compared to uncertainties during the first half of last year.

{kind=link}

source: company IR

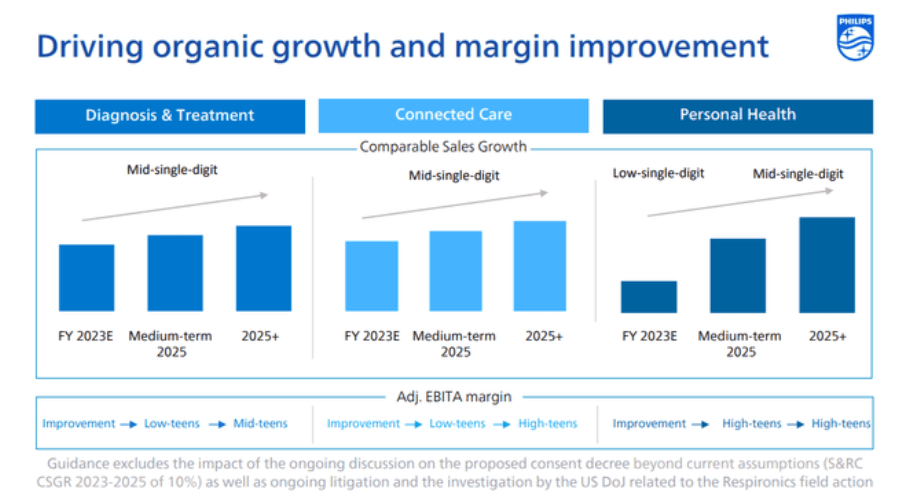

Going forward, the expectation is for stronger organic growth and firming margins through the next decade. For each of the three major operating segments, the plan is to reach sustainable long-term growth in the mid-single-digits while the adjusted EBITDA margin improves toward the high teens.

{kind=link}

source: company IR

What we like about Philips is that the company is a clear market share leader in several categories. High-level themes like an aging global population and an ongoing digitalization of healthcare globally represent key tailwinds that will remain in play beyond the current economic cycle.

The company also sees drives like growth in Cardiac workflow and demand for integration of equipment into cloud platforms as supporting investments towards its products worldwide. On the personal health side, Philips benefits from a reputation for quality and name recognition that we expect to continue.

{kind=link}

source: company IR

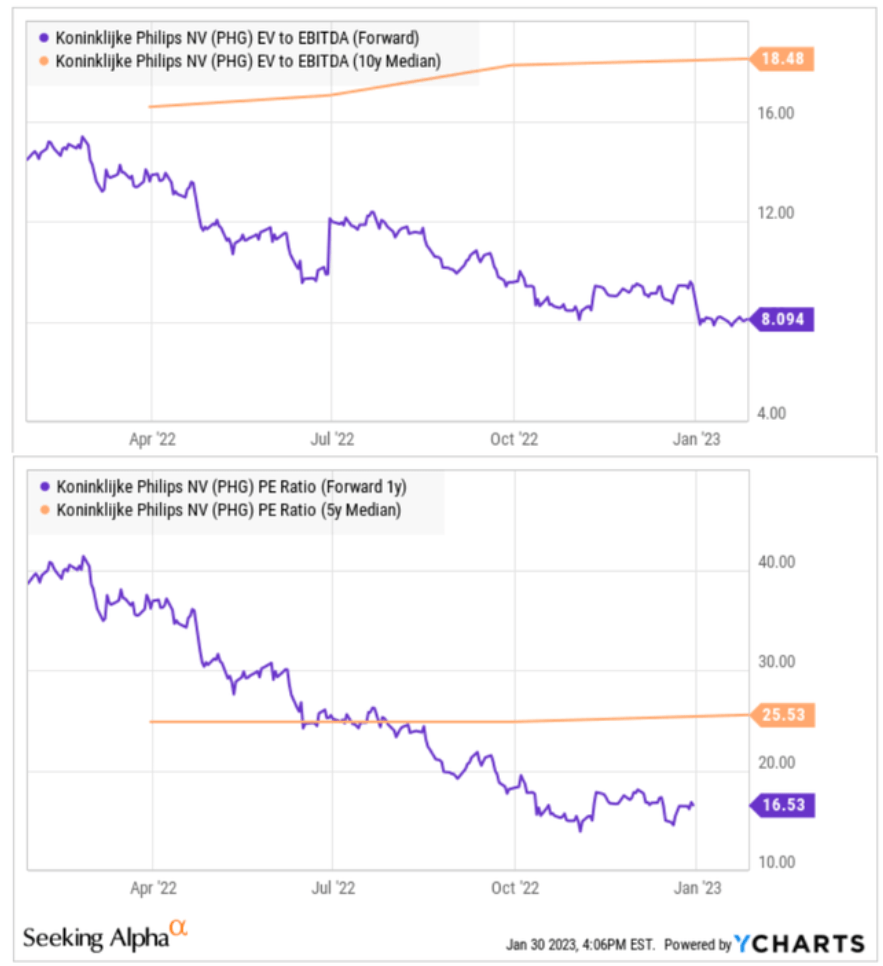

As it relates to valuation, we have to go back to that theme of PHG being distressed. The metrics were looking at between an EV to forward EBITDA multiple of 8x or forward P/E of 16.5x suggesting the stock is trading at a deep discount compared to its historical average. While some of that spread is justified based on the soft top-line momentum and higher debt, the bullish case is that there is room for a repricing higher as the company confirms a turnaround and the market recognizes the new outlook.

{kind=link}

source: company IR

PHG Stock Price Forecast

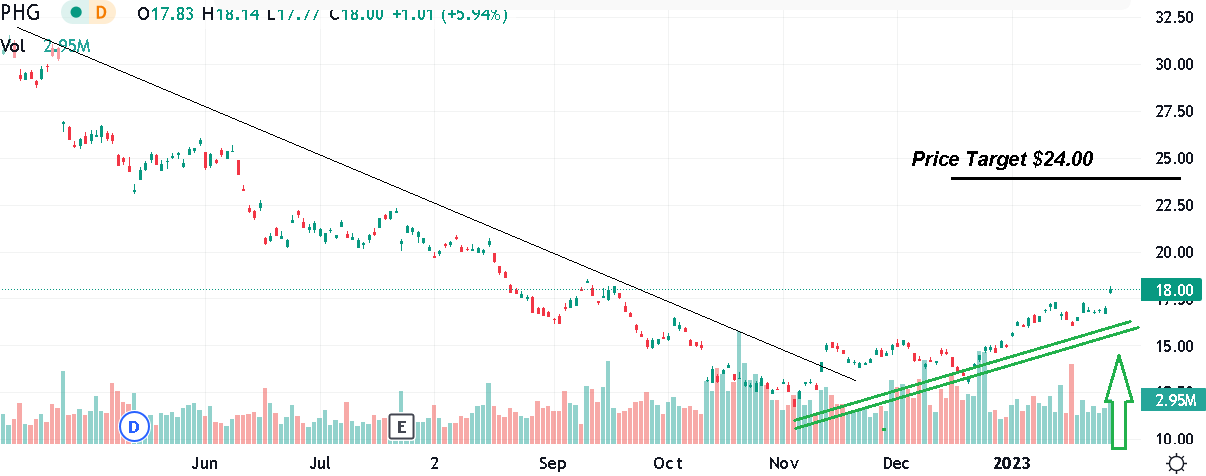

We rate PHG as a buy, with a price target for the year ahead at $24.00 implying a 25x multiple on the current 2023 consensus EPS for the stock at $0.98. The way we see it getting there is that stronger earnings over the next few quarters can support some revisions higher to estimates as shares gain momentum. Getting into 2024, against the long-term financial target for the company, PHG could start to appear cheap as the cost savings efforts drive margins higher.

In terms of risks, the company remains exposed to financial market volatility and macro conditions. A deterioration of the economic environment defined by a deeper recession would impact demand, opening the door for weaker-than-expected results. The ongoing " Respironics " litigation has been addressed by management with over EUR 1.5 billion in write-offs but still poses the potential for headline risks related to a potential expansion of the recall. We want to see the stock remain above $15.00 as an important level of support.

{kind=link}

Seeking Alpha

For further details see:

Philips: Compelling 5% Yield As Q4 Earnings Confirm Financial Turnaround