RYLPF - Philips: I Was Wrong But Risk Remains

2023-04-25 11:39:59 ET

Summary

- Philips stock popped on Q1 strength but ignored continued cost growth in its Sleep & Respiratory Care unit.

- The market has ignored this cost growth altogether.

- The path ahead remains challenging for Philips, but I feel a Hold rating is more justified than a sell rating, granted that investors are aware of the challenging execution path.

In October 2022, I covered Philips (PHG) and I discussed the challenging environment for the company as the company's apnea devices had isolating foam particles that could end up in the respiratory tract, and the company faced macroeconomic headwinds.

Against my expectations Philips' stock has rebounded strongly gaining 67.2%. So, my sell recommendation would have been counterproductive for investors. In this report, I revisit Philips with an analysis of the first quarter results and a stock valuation based on the company's enterprise value.

My Bearish Thesis Explained

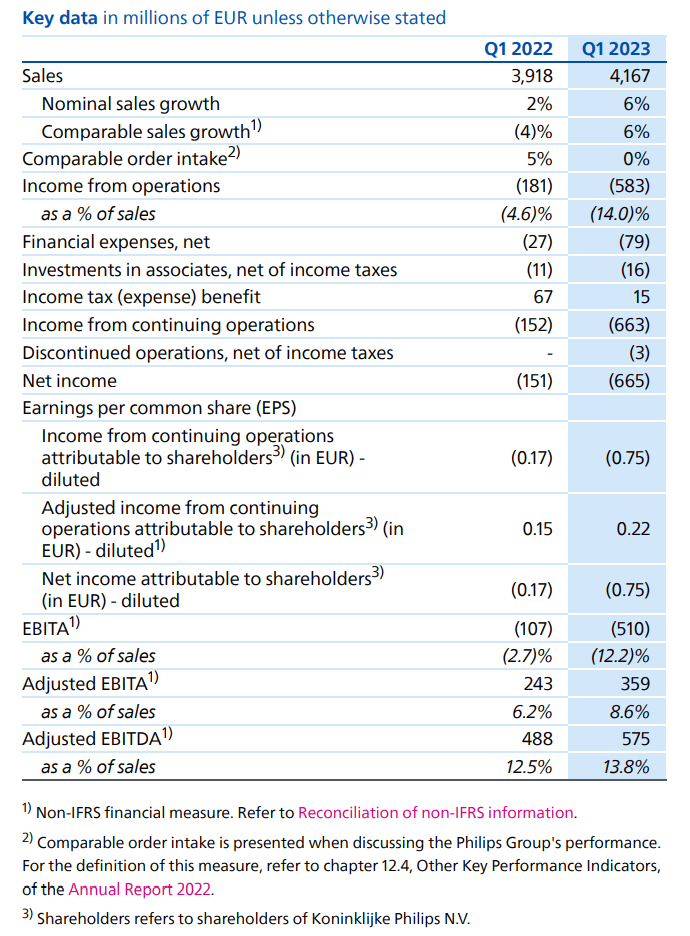

Before analyzing the first quarter results, it might be useful to explain why I was bearish on the stock. The obvious reason was that I expected the problems in the Sleep & Respiratory Care segment to persist, which also was the case with €575 million in litigation costs and €54 million in remediation costs. Furthermore, the Personal Health segment was expected to be under pressure due to reduced consumer spending and lower sales in Russia, which also was the case with 6% comparable sales growth decline. All of this would

However, as an analysis of the first quarter results will show there were positives in Philips' expectations as well as results that were a bigger driver for the stock price.

Philips Sales Grow And Margins Expand

{kind=link}

The positive for Philips was that sales grew by 6%, driven by double-digit growth in the Diagnostic & Treatment segment, while Connected Care which includes the troubled Sleep & Respiratory Care grew by 3% where decline in the Sleep & Respiratory Care unit was offset by strong Hospital Patient Monitoring sales. Another area of lower sales was Personal Health with 6% lower sales, but all combined, the 6% comparable sales growth was better than many had expected. Income from operations reflected the €575 million charge for litigation costs, but adjusted EBITDA showed an appreciable expansion in margins driven by 5.4 basis points margin expansion in Diagnosis & Treatment and a 2-percentage point increase in healthy part of the Connected Care business partially offset by a 3-percentage point contraction in adjusted EBITDA margins for the Personal Health segment. All with all, sales were up 6% and adjusted EBITDA was up nearly 18% and this expansion was driven by €190 million in cost reductions out of a €2 billion cost reduction effort.

The other positive was that Philips will start settling this year for economic damages related to the respiratory devices and next year for economic damages, which won't be cheap but the costs have already been incurred for that and the cash will flow out later and will give Philips a chance to leave the S&R debacle behind.

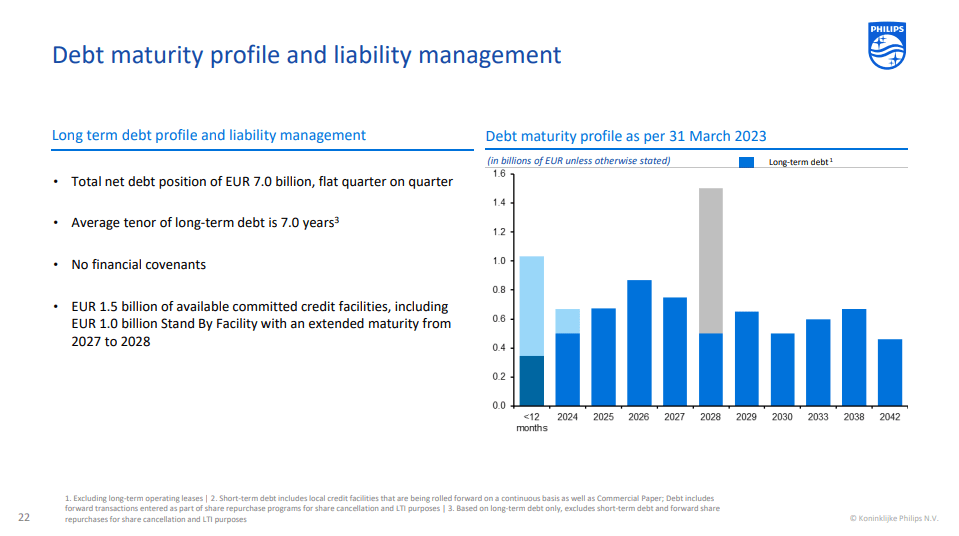

Cash and Debt Maturity

One of my main concerns last year was that with €776 million in cash, the dividend of €0.85 per share was not sustainable. The dividend strength remains something that I am not fully convinced of, as the company aims to pay 40 to 50 percent of its adjusted income to shareholders. For the first quarter, there was €0.75 in income attributable to shareholders indicating 9 to 11 cents in Q1 contribution towards the full year dividend payable in 2024 over 2023. For 2022, the adjusted income was €0.96 per share, indicating a dividend of up to €0.48. The company, however proposed a dividend in shares and keeping the dividend constant, which I believe will also be the most prudent path for 2023.

{kind=link}

During the first quarter, Philips had a free cash flow of €117 million which is a strong start of the year as the first quarter for many companies tends to be soft from sales and cash flow perspective. The company ended the quarter with €1.128 billion in cash and it will need that cash as it has €1 billion in short term debt. Philips will be able to pay that from its cash position, but it is likely it will utilize its €1.5 billion in remaining credit facilities for this as well. Either way, the company does not have an extremely strong cash position to service its debt, so it relies on improving cash flows and refinancing of debt as well as extending the credit facilities.

What Is Philips Stock Worth?

| Valuation Philips |

| Market Capitalization [$ bn] |

| $ 18.9 |

| Total debt [$ bn] |

| $ 9.0 |

| Cash and equivalents [$ bn] |

| $ 1.2 |

| Total Enterprise Value [$ bn] |

| $ 26.6 |

| EBITDA 2023 [$ bn] |

| $ 2.0 |

| EV/EBITDA |

| 13.1x |

| WACC |

| 6.7% |

| Current price |

| $ 21.72 |

| Median |

| Current |

| Industry |

| EV/EBITDA |

| 12.9 |

| 16.5 |

| 15.9 |

| Price target |

| $20.07 |

| $25.51 |

| $24.63 |

| Upside |

| -8% |

| 17% |

| 13% |

Philips has an enterprise value of $26.6 billion compromised of $18.9 billion in shareholders' equity, $9 billion in debt and $1.2 billion in cash and cash equivalents. For 2023, the revenue estimate by analysts is $20.18 billion and the EBITDA margin expected is 13.2%. I have assumed that this does not include the €575 million litigation provision announced during the first quarter. Accounting for this gives us an EBITDA estimate of $2 billion for 2023 with a 13.1x enterprise multiple. Compared to the median that is 8% lower than today's stock price when comparing it to the median but I could also see the stock starting to trade more in line with the industry in the case Philips is finally able to settle disputes which would provide 13% upside to the stock.

Conclusion: Philips Stock Is A Hold

Previously, I might have been too harsh on Philips stock assigning it a sell rating, but I think the reality was that charges continued into 2023 as I expected and the company continues face a challenging cash and debt maturity profile which requires significant cash generation. In the first quarter, the cash generation was strong and that creates expectations for the remainder of the year. I think that while the stock does show some upside, the path ahead remains risky for Philips. In some way, the limited upside to the share price is cause because I missed the run up in the stock price as I had a sell rating on the stock, but from fundamental point of view, I do think that Philips needs a very strong execution to manage its debt and realize the anticipated 2023 results. When the company manages to navigate the current challenges, I do think there is a lot of upside on continued sales growth for Patient Monitoring sales as well as overall margin expansion.

For further details see:

Philips: I Was Wrong But Risk Remains