VLO - Phillips 66: A $4.20 Dividend (4% Yield) To Celebrate 420 Day

2023-04-20 12:03:47 ET

Summary

- In celebration of April 20 (i.e. "420 day"), my stock of the day is Phillips 66, which currently pays out a $4.20/share annual dividend (a 4% yield).

- As we exit the shoulder season and into the summer driving season, PSX is perfectly positioned after recently completing major refinery turnaround projects on both coasts.

- After completion of Sweeny Frac-4 in Q4, and the upcoming close of the DCP acquisition, PSX is expecting the combination will deliver an incremental $1.3 billion uptick in annual EBITDA.

- While crack spreads have fallen year-over-year, they're still relatively healthy and PSX should have another strong year after earning $11.0 billion or $23.27/share in 2022.

Phillips 66 (PSX) is my stock of the day considering it is April 20 (i.e. "420 day"). That's because PSX pays out a $4.20/share annual dividend obligation and that's good enough for a very attractive 4% yield. Meantime, PSX is expected to achieve an estimated $1.3 billion incremental EBITDA increase this year due to two midstream developments: The completion of Sweeny Frac-4 in Q4 and the pending DCP Midstream acquisition - which is expected to close this quarter (Q2). And, as we exit the "shoulder season," PSX is perfectly positioned for the summer driving season after completing major refinery turnarounds on both coasts. Bottom line: PSX is a buy.

Refining Crack Margin

It's true that the U.S. 3:2:1 refining crack spread has fallen from the last year's super-strong level, but refining margins are still very healthy from an historical perspective, and I expect margin to strengthen in the second half of the year:

Macro Micro

Turnarounds

I also expect PSX's upcoming Q1 results to be relatively weak driven by a relatively low refining utilization rate. I say that because, as we learned from CEO Mark Lashier on the Q4 conference call , Q1 was expected to have the majority of PSX's annual refinery maintenance expense:

So our first quarter turnaround, you can tell by our guidance there that ... our annual guidance is in the 550 to 600 (million) range. And our first quarter is a majority of that spend. So we are heavy centric first quarter on our turnaround. And those are primarily related in just a couple of sites ... I see that as really impactful to our Atlantic coastal operations there as the biggest part of that impact on the turnarounds. There is also some Gulf Coast turnaround activity as well that is less impactful. So although there is a heavy spend, it's centric really in one primary facility.

The good news is that, after refinery maintenance operations in the latter part of 2022, and the Q1 turnaround, PSX should be ideally positioned to benefit from what's expected to be another strong summer driving season.

Midstream Developments

However, what PSX may lose in yoy refining profits, it's likely to make up with a big uptick in its midstream operations. I say that because Sweeny Frac-4 came online in Q4 of last year. Frac-4 is an additional 150,000 bpd of capacity. That brings its total Sweeny Hub capacity to 550,000 bpd - making it the second largest fractionation hub in the country.

Also in Q4 of last year, and as expected, Phillips 66 announced an agreement to acquire all the publicly held units of DCP Midstream for $3.8 billion (see PSX Grows By Swallowing DCP Midstream ). That deal is expected to close this quarter and to deliver an incremental $1 billion of EBITDA on an annual basis. That equates to an estimated $2.74/share based on the 473,728,000 shares outstanding at the end of 2022.

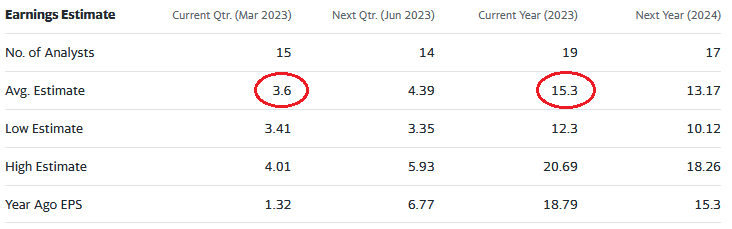

Q1 Earnings Estimates

PSX is scheduled to release its Q1 FY23 earnings on May 3. The graphic below shows current consensus earnings estimates from Yahoo Finance :

{kind=link}

As you can see, analysts are expecting $3.60/share in Q1 earnings and $15.30/share for the full year. Obviously, the back half of the year is expected to be stronger for the reasons given earlier. While the $15.30/share for full-year FY23 is obviously down significantly from $23.27/share the company earned last year due to exceptionally strong crack margins, note that at pixel time the stock is currently trading at only $101.80. That equates to a forward P/E of only 6.7x. Combined with a current yield of 4%, PSX is - in my opinion - a strong value here.

Returns

However, investors should acknowledge that PSX has significantly lagged its peers Valero ( VLO ) and Marathon Petroleum ( MPC ) over the past few years:

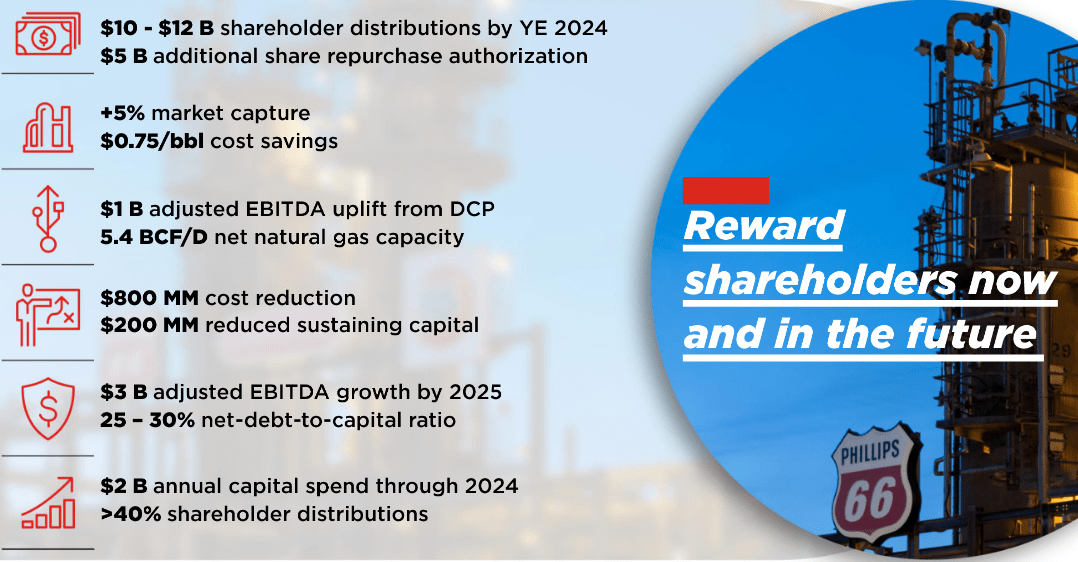

However, and as I reported previously on Seeking Alpha, at the company's Investor Day Presentation last fall, relatively new CEO Mark Lashier unveiled a strategy to address the company's relative under-performance by a combination of efficiency initiatives, a reduction in headcount, primary growth projects, and by improving the company's refining performance by boosting market capture by 5%.

The result is a goal to deliver $10-$12 billion to shareholders by year-end 2024:

{kind=link}

Summary and Conclusion

While it remains to be seen if PSX's new CEO Mark Lashier can deliver on the goals shown in the Investor Day Presentation, he does seem intent on leaving his mark on the company and improving the company's relative lack of performance as compared to peers. Time will tell. However, the market appears to be overly skeptical in my opinion. I say that because the current EPS estimates imply a forward P/E of only 6.7x. Given the company's strong balance sheet and the relatively clear line of sight to a big uptick in midstream EBITDA this year due to Frac-4 and the DCP acquisition, PSX - and its 4% yield - look very attractive here. Even if the company falls short of its $10-$12 billion shareholder distributions by year-end 2024, dividend growth should be strong. PSX is a buy.

For further details see:

Phillips 66: A $4.20 Dividend (4% Yield) To Celebrate 420 Day