PSX - Phillips 66: A Diversified Way To Benefit From A Strong Refining Environment

2023-11-04 06:56:49 ET

Summary

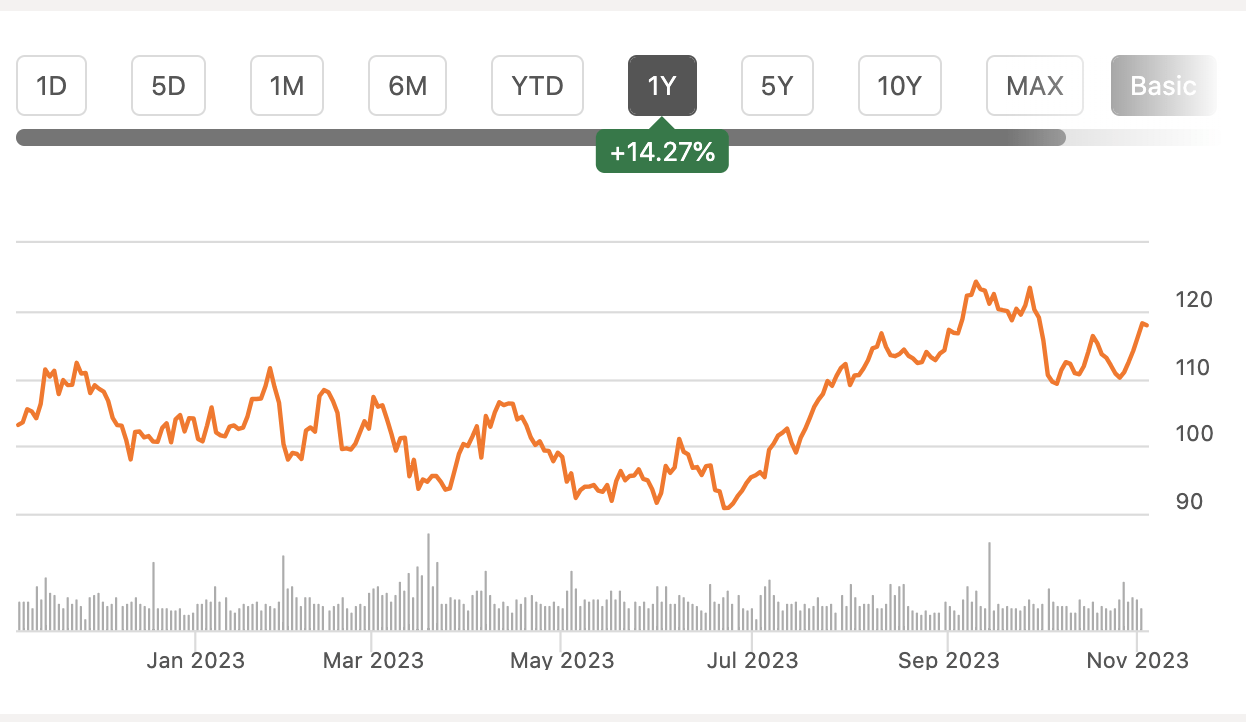

- Phillips 66 shares have risen 14% in the past year and are up 6% since reporting Q3 earnings results.

- Refining results were soft, but long-term guidance was encouraging, and the company's diversification provides stability.

- The company generated $2.4 billion in operating cash flow and has been aggressive in buying back its own stock, with its share count down 25% the past decade.

Shares of Phillips 66 ( PSX ) have been a strong performer over the past year, rising about 14%. Shares are also up 6% since reporting Q3 earnings results, aided in part by a broad market rally. While refining results were a little soft, long-term guidance was encouraging. I view shares as attractive.

{kind=link}

In the company's third quarter , PSX earned $4.62 in adjusted EPS, which missed expectations by $0.10. Adjusted revenue declined from $45.7 billion to $40.3 billion; however, for refiners, revenue is not the ultimate driver of earnings as it can move dramatically with oil prices. Refiners are relatively price agnostic as they earn money based on the spread between crude oil and refined products. If that spread stays the same, crude oil moving up or down has essentially no cash flow impact.

Relative to the second quarter, earnings rose $304 million to $2.07 billion. Refining was up $592 million while midstream and chemicals were down $57 and $88 million respectively. PSX is somewhat unique among the US refiners in that it is not a pure-play refinery with 50% ownership in a chemicals joint venture (CP Chem) and extensive midstream operations. The company has also been diversifying, going against the trend of de-integration with its purchases of its MLP, Phillips 66 Partners, and DCP Midstream over the past two years.

Still, refining accounts for over half of the company's EBITDA and is the biggest driver of quarterly variances. Still, particularly its midstream operation provides some stability to cash flows. This means when refining spreads widen, PSX will not enjoy as much or a windfall as a more pure-play operator like Valero ( VLO ) but that during refining downturns, its results should be able to hold in better, all else equal. In my view, PSX can offer investors a smoother ride over-time because of the diversification within its business.

Refining results were a bit soft in the quarter, driving the headline EPS miss. This segment earned $1.7 billion in pre-tax income, which was down from $2.8 billion last year. Some of this was due to the fact that last year was an unsustainably good year for refining. Russian sanctions led to tightness in product markets, like diesel, which meant the crack spreads refiners earn were very wide. They have come down with the 321 crack spread at $28.64 in the quarter, down about $8. That is a macro headwind out of the company's control. However, PSX realized only 66% of this spread, or about $19, which was down from 73% last year. Configuration and secondary products were a $10 headwind from just $7 last year.

Now, management has reiterated it expects to see 1.3% capture improvement this year and is undertaking about a dozen projects a year to continue improving this 1-2% per year. On the positive side, the refineries ran at a crude oil utilization rate of 95%, which is the highest since 2019. So, the efforts to modernize its facilities is helping to reduce downtime. Particularly considering management raised long-term guidance (more below), I am inclined to view this as a one-quarter disappointment from what was an outstanding quarter last year.

Midstream transportation pre-tax income was stable at $285 million, but NGLs were down by about 17% sequentially to $293 million. While transportations revenue is generally fee based, the NGL unit does have some commodity price exposure. Underlying margins there were actually higher, but cargo freight cost timing was unfavorable. Relative to last year, midstream income rose by about $100 million or 16%, excluding one-time items. Management also raised its synergy estimates to $1.4 billion from $1 billion from its past midstream M&A.

Chemicals pre-tax income of $104 million sequentially was down over 40% due to lower margins amid weak pricing. Profits were also down ~22% from $135 million last year. This was actually a more modest decline than seen at some standalone chemical companies like Dow ( DOW ), aided by low-cost feedstocks and limited exposure to the Chinese construction market.

Even though profits were down due to difficult comparisons in refining and a lower capture this quarter, the company still generated $2.4 billion in operating cash flow excluding working capital. With $855 million in cap-ex, free cash flow was over $1.5 billion in the quarter. With this, PSX did $1.2 billion in capital returns last quarter, reducing the share count by about 2%. Over the past year, the share count has fallen by 7.5%. Alongside this, there was $500 million in debt reduction. PSX carries $19.4 billion in debt and $3.5 billion in cash, and that debt load is sufficiently supported by its underlying cash flow.

Phillips 66 has generated $5.1 billion of free cash flow ex working capital this year. This provides healthy coverage of its 3.6% dividend yield (the dividend costs about $1.8 billion per year). With its free cash flow, it has been an aggressive buyer of its own stock. Even with its equity issuance to acquire Phillips 66 Partners, PSX has repurchased over one-quarter of the company over the past decade.

{kind=link}

Alongside this quarter, PSX added $5 billion to its buyback authorization, taking it to $8.1 billion. The company also sees an additional $1 billion of EBITDA growth beyond last year's expectations by 2025 as it benefits from increased midstream synergies and investments to improving refining capture margins. As a consequence, PSX targets $13-$15 billion in capital returns by the end of next year from its initial $10-12 billion goal rolled out last year. That should translate to another ~8% reduction in the share count over the next twelve months,

This steady share count reduction should support EPS growth. I also am of the view that refining margins are likely to stay wider than their pre-COVID norms as I have outlined previously because the world has underinvested in increasing refining capacity even as oil demand continues to slowly rise. That lack of supply should keep refining margins elevated. At the same time, its midstream operations provide fairly steady cash flow to support the dividend and interest payments.

Even assuming a further 10% narrowing in crack spreads, PSX has over $3.50 in quarterly earnings power, or about $14 per year on a run-rate basis. With each share it buys back, that underlying EPS power continues to rise, as well. Given the stability offered by its more diverse operations, I do believe shares deserve a somewhat wider multiple than peers and believe they can trade to about 10x earnings, pointing to fair value of $140, or over about 20% above current levels. In the meantime, PSX is able to buy back more shares at a discount, making the purchases even more accretive.

I believe investors should seek out refining exposure given the favorable supply/demand dynamics, and with its midstream and chemical businesses, PSX provides a relatively safe way to benefit from this theme.

For further details see:

Phillips 66: A Diversified Way To Benefit From A Strong Refining Environment