PSX - Phillips 66: An Equity-Rich Refiner Facing Earnings Headwinds

2024-01-10 18:28:24 ET

Summary

- Phillips 66 is given a Hold rating, which is more cautious than the bullish consensus.

- Double-digit top and bottom line declines in Q3, as we await Q4 results in a few weeks.

- The share price is at a double-digit premium vs. the long-term moving average.

- The downside risk of falling oil prices has been discussed, as well as this company's diversification into chemicals.

Stock & Industry Snapshot

As we approach the middle of the trading week, my eyes are back on the energy industry, so I'll be covering Phillips 66 ( PSX ) , a well-established Houston-based firm in the oil and gas refining segment.

A few quick facts from its website are that its business is focused on refining, midstream operations, chemicals, and emerging energy, among others.

The firm emerged from energy giant ConocoPhillips ( COP ) to spin off as its own company traded on the NYSE in 2012.

What we know from key market segment data is that the energy sector has underperformed a bit in the last year, however it also has staged a triple-digit performance vs. 3 years ago, when this sector was hit hard during the global pandemic.

PSX - market segment data (Seeking Alpha)

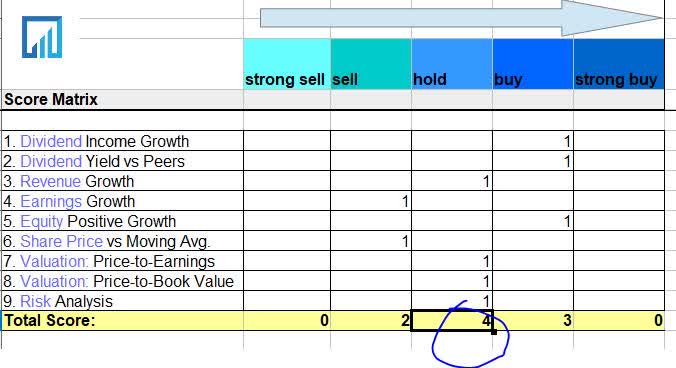

Scoring Matrix

We use a 9-point scoring method that looks at this stock holistically and assigns a total rating score, using a score matrix. Our approach focuses heavily on accounting statements, and follows a logical progression to find relationships between earnings data, share price, and valuation.

{kind=link}

Today's Rating

Based on the score total in the score matrix , this stock is getting a rating of hold.

Compared to the consensus rating on Seeking Alpha, my rating is somewhat more cautious than the overly bullish sentiment it seems.

PSX - consensus rating (Seeking Alpha)

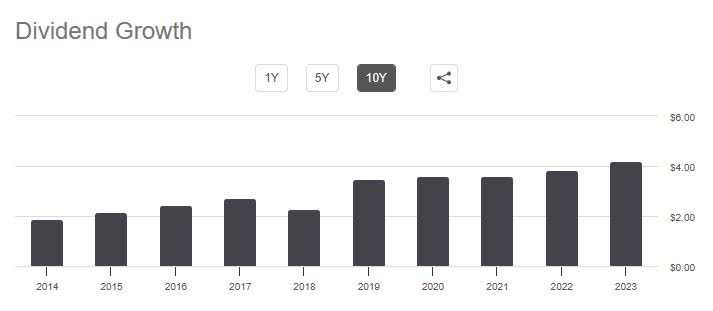

Dividend Income Growth

From the 10-year dividend chart , we see that this company has grown its dividend steadily in 10 years, despite the 2021/2022 pandemic headwinds.

{kind=link}

Going from $1.89/share/annually in 2014 to $4.20/share/annually is a nice 122% growth over a decade.

In fact, in its Q3 remarks , the company boasted of how it "returned $1.2B to shareholders through dividends and share repurchases."

Also, notably is that its quarterly payouts have tended to be relatively steady for years.

However, I am cautious about the likelihood they hike dividends again just yet, considering that its earnings took a YoY decline in Q3, however it has been consistently generating positive cash flow .

This rating category justifies a buy, rather than a strong buy.

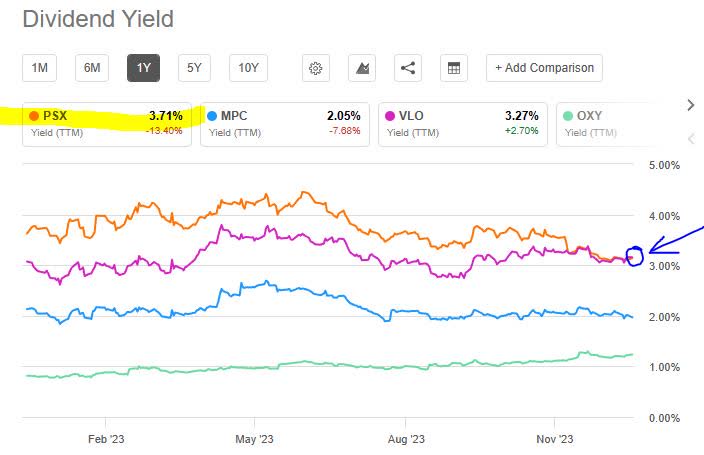

Dividend Yield vs. Peers

From dividend yield data we can see that the company leads the way on dividend yield among a peer group of similar energy-sector companies.

{kind=link}

Of this peer group, Phillips can boast 3.71% trailing dividend yield, (3.14% forward yield), and a healthy payout of $1.05/share/quarter. Others, like Marathon Petroleum Corporation ( MPC ) are trailing behind at 2.05%, Valero Energy Corporation ( VLO ) at 3.27%, and Occidental Petroleum Corporation ( OXY ) came in last.

The goal of this exercise is to pick just one of these to buy and add to a dividend income portfolio and gain exposure to the energy sector.

With a yield below 4%, which is decent, and leading this peer group, I would give this stock a buy in this category.

Revenue Growth

We can see from income statement data that total revenue fell to $39.64B in Q3, vs $44.95B in Sept. 2022, an 11.8% YoY decline.

However, we also see an improvement vs. Q2 figures, and a major improvement vs. its low of $21B in March 2021.

In addition, this company continues to expand its projects, and besides oil refining keep in mind it has a significant chemicals business too. Here is what the company said about its growth plans there:

CPChem recently completed construction and began operations of a 586 million pounds per year 1-hexene unit in Old Ocean, Texas. CPChem expects to start up its 1 billion pounds per year propylene splitter project at its Cedar Bayou facility in the fourth quarter.

Incidentally, 1-hexene is widely used as a solvent, paint thinner, and chemical reaction medium, according to the Natl. Library of Medicine .

In this rating category I call it a hold, on the basis of double-digit YoY revenue declines but also revenue improvements vs. 2021 and potential added strength in the chemicals space.

Earnings Growth

Also, from the income statement, we know that net income (earnings) fell on a YoY basis to $2.09B, vs $5.39B in Sept. 2022, a 61.2% YoY decline.

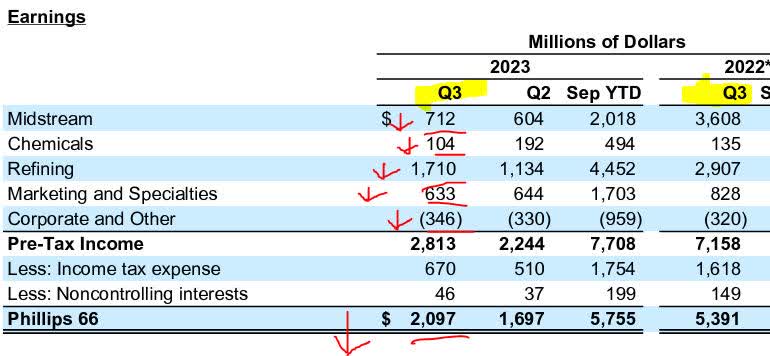

Here is a look at the business segments contributing to earnings:

{kind=link}

As it appears, on a YoY basis all segments declined however refining improved vs. Q2.

Specifically regarding refining, the company stated in its remarks the following:

The increase was primarily due to higher realized margins supported by strong utilization. Realized margins increased from $15.32 per barrel in the second quarter to $18.96 per barrel in the third quarter.

In the chemicals segment, "this decrease was mainly due to lower margins, partially offset by higher volumes."

From the income statement it is also evident that interest expenses climbed in Q3 to $221MM, vs $158MM in Sept. 2022. Operating expenses also climbed somewhat in Q3.

In the larger context, the company has still come far from its nearly $600MM net loss in March 2021.

Notable to mention is a Reuters article from 5 days ago mentioning the company's plans to raise money and lower costs through the sale of assets, which is on the table but has not materialized just yet:

The company said it would monetize $3 billion in non-core assets in 2024 as part of a plan to boost returns by cutting costs and assets.

In this rating category, I am compelled to say sell, on the basis of double-digit earnings declines, the climbing costs, and unclear certainty over earnings growth sustainability in the near future, considering the volatile nature of oil prices and their effect on the energy sector.

Equity Positive Growth

This is a company with a lot of equity, in my opinion, with the balance sheet data showing $31.98B of total equity in Q3, vs $33.3B in Sept. 2022, a nearly 4% YoY decline.

One impact on equity is long-term debt, and at this firm, it grew in Q3 vs. Sept 2022.

What we do know is the company has the financial strength to return capital back to shareholders. This is what they said on that topic in their Q3 release:

Phillips 66 returned $6.7B through share repurchases and dividends since July 2022 and is on pace to exceed the original $10 billion to $12 billion target. The company is now increasing this target to a range of $13 billion to $15 billion and plans to return at least 50% of operating cash flow to shareholders.

Further, the firm seems to have lots of liquidity to tap into if needed:

As of September 30, 2023, the company had $3.5B of cash and cash equivalents and $6.3B of committed capacity available under credit facilities. The company's consolidated debt-to-capital ratio was 38% and its net debt-to-capital ratio was 33%.

Despite the single-digit equity decline, which I think is insignificant for a firm with this level of book value, due to continued double-digit positive equity and liquidity strength, as well as a continuation of returning capital to shareholders, I would call it a buy in this case.

Share Price vs. Moving Average

The following is the chart with the most recent price as of this article:

What we see is a share price of $133.22, which is a +21% premium to its 200-day moving average, as the chart shows.

When considering the overly bullish share price, up over $43 from its October lows, while at the same time, the company revenue and earnings are showing double-digit declines lately, and a dividend yield less than 4%, this stock makes a good case for a sell at this point, at least in terms of share price.

Now, for readers who would argue that this stock will continue to be bullish in 2024 and the bulls will take that share price further, I think the tie-breaker here will be a closer look at valuation and risk, in the next few sections.

Valuation: Price-to-Earnings

Here, we'll briefly look at valuation metrics such as the GAAP-based forward P/E ratio.

The data shows the forward P/E multiple is now 8.66, below the sector average of 10.45x earnings.

What we discussed earlier is that the share price is double-digits above its 200-day SMA, while earnings are on a double-digit decline. So, even though this valuation is below its sector average, it still appears that a major rift exists between share price and earnings.

What I found is that its energy-sector peer Valero Energy actually presents a better valuation case than Phillips does. For instance, they only had a 7% YoY earnings decline, but their share price only rose a few points above its moving average, so a much lower rift between share price growth and earnings. Also, its valuation is around 5.4x earnings.

My sentiment on Phillips in this case to say hold, because although the valuation is below its sector it still could use improvement and not quite justified at a multiple of +8x earnings.

Valuation: Price-to-Book Value

Also, from valuation info , we see that the forward P/B ratio is now at a multiple of 1.92x book value, somewhat above its sector which is around 1.6x.

When comparing this to the share price and equity discussion earlier, we know that there is a very bullish share price and an equity growth that is practically flat although equity remains at +$30B, certainly no small number.

This would be more of a hold, since there was no significant decline in book value.

Risk Analysis

The risk I want to bring up is the trend in oil prices, and the potential downside impact on a stock like this since low oil prices can lead to less investment in drilling as it becomes unprofitable to do so.

Let me turn your attention to today's article by the Canadian Broadcasting Corp/CBC which highlighted that 2024 oil prices will be sluggish:

A new report forecasting energy trends estimates global oil prices will be stuck at low levels for the next couple of years.

The analysis from Deloitte released Tuesday predicts an average West Texas Intermediate ((WTI)) price - typically regarded as the benchmark for crude oil - of $72 US per barrel this year.

That depression in price is because of cuts from major producers, record production in the United States and slowing growth in demand, according to the report.

Another data point pointing to downside potential in oil is the latest chart from Statista, which shows a downward trend in oil prices going into 2024:

{kind=link}

The low oil price forecast seems more driven by oversupply, rather than lack of demand. Lately I wrote in another article covering an airline about a spike in travel demand going into 2024. In fact, this thesis is also supported by this week's analysis from Goldman Sachs :

While demand for crude oil held up over the past year, the growth in oil supply has been surprisingly robust. The result has been softer oil prices, and that phenomena may continue in 2024.

So, I am on the fence when it comes to this risk because on the one hand there is anticipated oil demand but also oversupply. There are also continuing geopolitical conflicts going on in the world, which may or may not impact oil prices. In addition, Phillips does not only do oil but also has a robust chemicals business, as I mentioned earlier.

In the big picture, I think the case is for a hold right now.

Quick Summary

To summarize, from a holistic perspective I'm calling this stock a hold, being more cautious than the consensus.

The evidence shows declining revenue and earnings, book value growing flat, and a decent dividend yield just under 4%.

My portfolio strategy here would be to hold and continue earning the $1.05/share quarterly dividend income, and wait out the situation with oil prices some more.

What I think could drive the upside in share price on energy stocks is a combination of demand growth for oil in 2024 (fueled mainly by travel growth) and a supply shock or pullback, such as an OPEC decision or a larger geopolitical conflict in global oil regions.

For further details see:

Phillips 66: An Equity-Rich Refiner Facing Earnings Headwinds