PSX - Phillips 66: Attractively Valued Refiner With Quality Yield

2023-04-28 16:52:39 ET

Summary

- Phillips 66 has proven its mettle over COVID-19, has shown the sanctity with which management treats the dividend, and has strong buybacks.

- Midstream is strong and will likely remain so as the world continues to readjust to dislocations in global energy markets from Ukraine.

- Phillips 66 has credible efforts to boost the efficiency of the business and management's strategy is very shareholder centric.

- The company has made a lot of strides toward repairing their balance sheet since the depths of COVID and has a strong cash position.

- The company also has compelling investing in renewables that are based on delivering shareholder value, not 'greenwashing.'

The oil refining industry had an exceptional year in 2022. Across the world, there was a shortage of refining capacity that helped boost margins and led to record profits for many firms, including Phillips 66 (PSX). There have been years and years of underinvestment in Energy infrastructure. Phillips 66 has a lot of premier assets and relationships that ensure it will be poised to continue letting the good times roll. It is also a global firm, allowing it to benefit from profits in less stringent regulatory environments. Of course, you might be asking about what happens to an Energy firm in the upcoming 'most anticipated recession in history?'

Luckily, the refining industry is much less sensitive to the undulations in underlying commodity costs than much of the Energy complex. Also, while much of the upstream section of the complex can often become a political football, refining can help reduce carbon output when it is allowed to progress efficiently and technologically. Refinery technology advancements have led to dramatically more output per barrel of oil over the years. The management at Phillips 66 is dedicated to being the best refiner in the world. Luckily, the margin environment for the business is extremely favorable.

{kind=link}

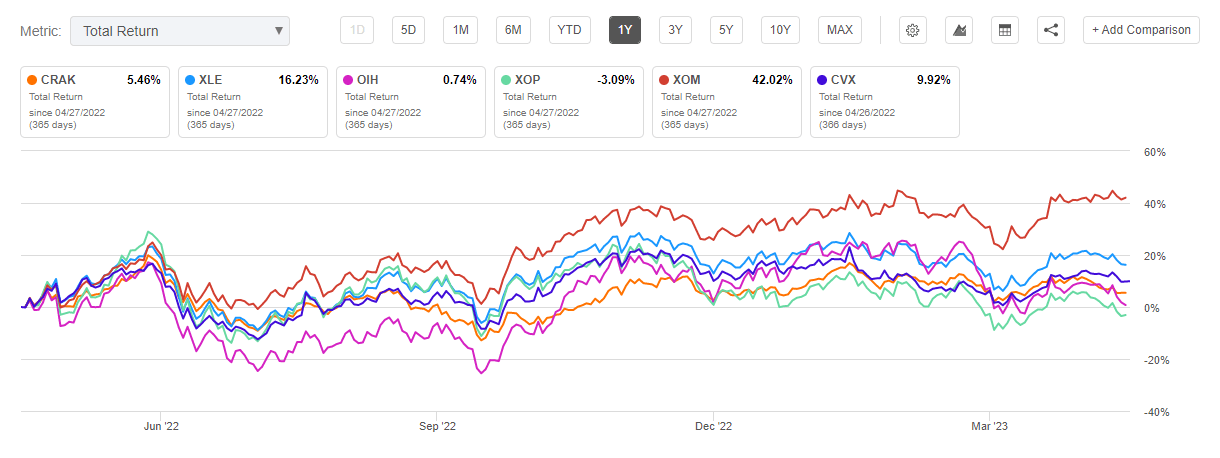

As you can see, the great performance of the Energy sector has been led by the two oil majors of the last year, particularly Exxon ( XOM ). You can see that upstream ( XOP ) and Oilfield services ( OIH ) have significantly lagged behind. However, ( CRAK ) representing oil refiners, has been relatively stronger. I suspect that its outperformance will begin to take off as strong margins that some thought to be a blip appear to be more sustainable.

{kind=link}

The company has also made aggressive moves to benefit from trends in NatGas. Overall, the company has a compelling strategy to maximize tailwinds in a way that delivers to shareholders. You have to be careful when picking dividend plays in the Energy sector. Still, I think Phillips 66 is a natural one to gravitate toward, given the economics of refining and management's militant focus on maintaining the dividend. Shareholder is the guiding light for this firm.

Historically Favorable Conditions For Oil Refiners

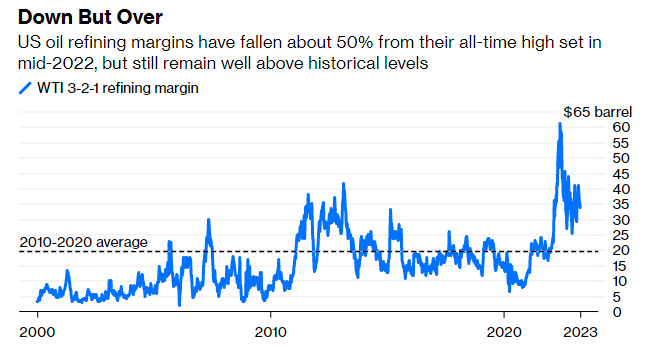

Crack spreads , which are the difference between what a refiner pays for oil and makes on the sale of the final product, have been elevated. When these spreads are high, refiners are particularly profitable. Evidence shows supply dynamics could keep them elevated for a long time, and Bank of America even proclaimed that a ' Golden Age ' for oil refiners has begun. I think Phillips 66 is a great way to get in on this opportunity.

One of the main reasons Energy firms tend to suffer during recessions is because the overall price of crude drops. However, Phillips 66 is specifically concentrated in the mid-stream of the Energy complex, meaning that it's less directly affected by the volatility of crude prices than many in its sector. So, while the company's profits are certainly correlated to the overall crude prices, it has a more stable business than many competitors in the Energy Industry. The relative stability of cash flows is nice for an industry that has burned many investors who thought they were getting high-flying yields that were less than rock solid.

{kind=link}

Even with Phillips 66, some of the more old-school dividend investors may scoff at a company with a somewhat unreliable dividend history compared to, dividend aristocrats like General Dynamics (GD) and Raytheon (RTX). Both of these stocks have A+ on dividend consistency Seeking Alpha grades compared to a C for Phillips 66. However, I'd say that the firm's valuation and increasing competitive advantage compensate for understandable turbulence over the last three years. The stock is currently on Seeking Alpha's Top Quant Dividend Picks .

The Refining Business Likely Has Bright Days Ahead

The Energy business is perhaps the most controversial on the planet right now. Climate change and government action around it cast a pall on the terminal value of the whole Energy sector, and valuations have been depressed as a result. However, the fundamental need of the economy for Energy is not going away, and the pace of innovation in renewables and other clean energy has not reached a level where it can yet replace fossil fuels. I think Phillips 66 can benefit from what I refer to as rhetorical arbitrage . In other words, the pessimism around the future of the energy that has been priced into markets is greater than reality justifies.

{kind=link}

The refining business is even more of a beneficiary of those willing to brave the rhetorical castigation of the Energy industry. It is relatively insulated from the reputational and regulatory risk for the following reasons. However, the business becomes particularly attractive when margins are above their long-term averages.

1. Refining as a business improves margins long-term through technological improvements that increase the efficiency per barrel of crude. They are an essential part of the Energy transition.

2. Refiners have natural technological expertise that can be helpful in key areas of the clean energy transition, such as biofuels.

3. As competition between global powers heats up and energy is at the center of that competition, the US government will likely increasingly see the Energy industry as a vital national asset. Refiners are vital to national infrastructure.

So, as the risk of recession rises, it might be wise to tilt your energy exposure to be more heavily weighted toward the refiners with more stable cash flows as the specter of recession rises. Obviously, the banking crisis puts a damper on economic expectations. This is one of the tactical reasons to favor refiners, but there are plenty of shareholder-friendly reasons to stay in this stock for the long term as well.

Good Prospects For Strong Buybacks And Enduring Dividends

This company has a healthy yield and a management that has expressed a fierce dedication to continuing to provide an attractive and growing dividend. One of the first things you need to do is check the track record of any company on dividends before considering making it part of your dividend portfolio. Despite some of the greatest curveballs in the history of the storied Energy industry, this company has continued to deliver. It has shown shareholders the management team is worthy of trust.

{kind=link}

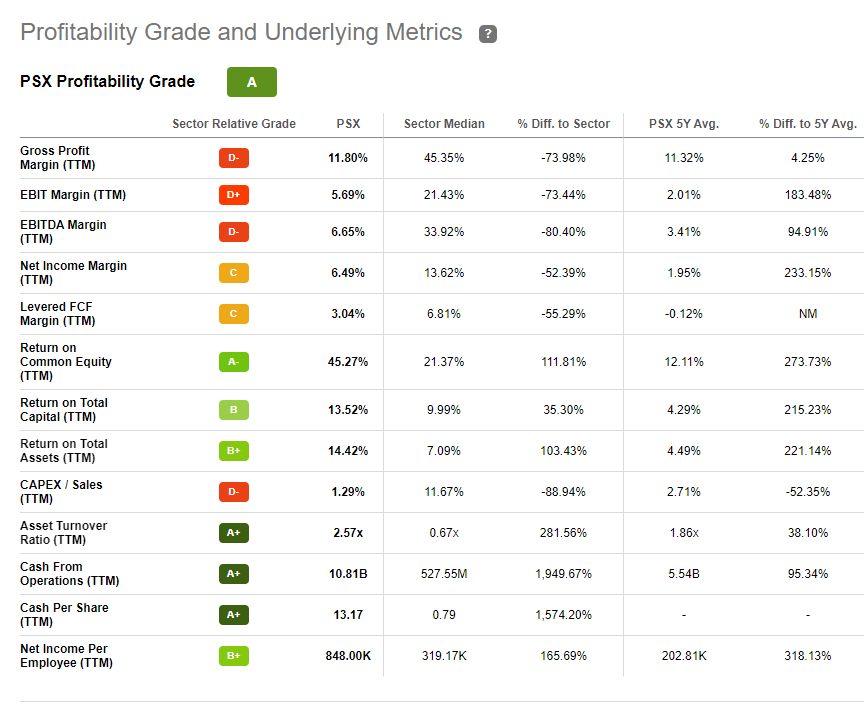

When considering the dividend, you always want to consider debt levels and profitability. Suppose a company's profitability is declining or is stagnant at the same time as slowing revenue growth, then a healthy growing dividend could be at risk. So, I'm encouraged when I see the high profitability scores Phillips 66 receives from Seeking Alpha. Sometimes a higher-than-historic dividend can be an alarm bell.

However, in the case of the Energy industry and in Phillips 66 specifically, I believe the higher dividend is reflective of a management imperative that has changed as fortunes have for the Energy sector. Companies that used to be cowboys are now as clean as preacher's sheets from a shareholder's perspective and must remain that way in the new environment. Let the new cult of shareholder interest serve your long-term interests. Peak liquid energy demand is still at least a decade away, and there are many dividends to be paid.

{kind=link}

This company also has a strong competitive position. It solidified its position as the second largest US refiner after its recent accretive merger with DCP Midstream . The company is now firmly in a leading position in the US refining market, and aside from its growing strength in this area has a premier chemicals segment.

Valuation

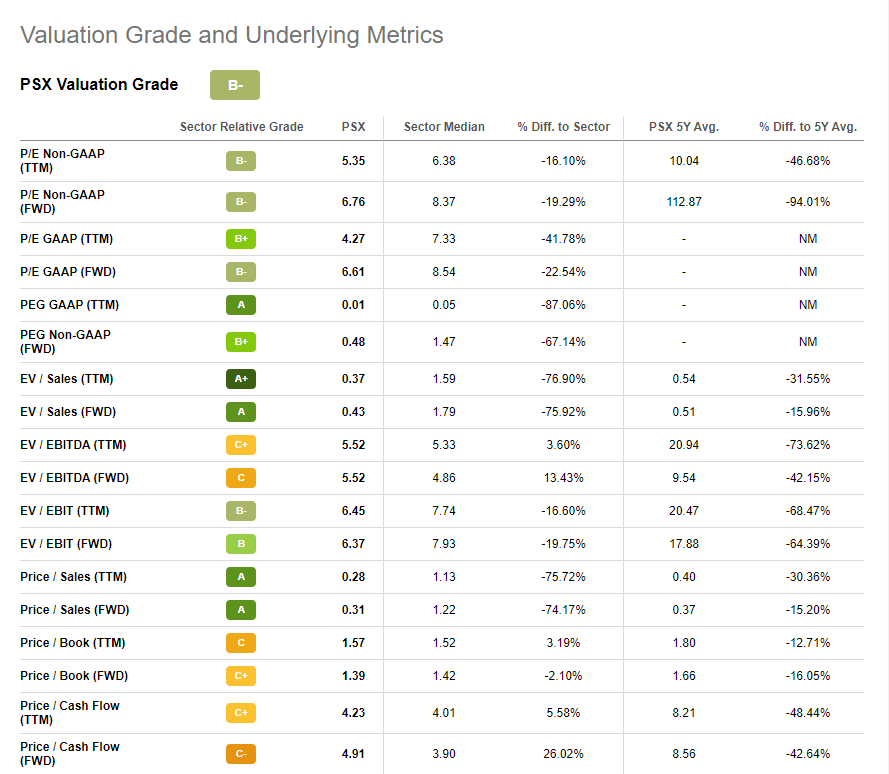

Phillips 66 is very appealing from a valuation standpoint across most metrics. It is pretty much significantly lower than the sector across the board, with a few exceptions. What's even more notable about this is that it is measured against an extremely undervalued sector. Not only is the sector undervalued, but when you compare the characteristics of Phillips 66 to the rest of the sector, its stable mid and downstream cash flows should be more resilient to recession than other areas. When you throw in the strong dividend yield, this stock has a great margin of safety for those who want to buy and hold.

{kind=link}

As you can see, Phillips 66 is trading at bottom-of-the-barrel multiples. Its TTM GAAP P/E ratio is 4.27. Given the supply and demand dynamics in oil refining, you are getting what seems like very cheap growth in earnings. And the great yield gives you an additional margin of safety. Refining is an essential and mature industry, and given the favorable dynamics, you might be able to get some attractive yield.

Given how undervalued the stock is, the potential total return is advantageous. If you have time and don't like checking the stock daily, why not try buying shares directly through Computershare and signing up for the dividend re-investment program ((DRIP))? One advantage is owning stocks outside the brokerage account. You won't likely sell on a whim or on a bad day. I think the total return potential for this stock over the next 5-10 years is very attractive. The company's management is making real investments in renewables, which helps increase the terminal value for any Energy firm.

Phillips 66 2022 Sustainability Report

Of course, aside from some of the traditional valuation methods that put Phillips 66 in an attractive light that I mentioned above, there are also valuation methods that strictly use dividends to determine intrinsic value. The Gordon Growth Model ((GGM)) is a simple model that has some flaws, but it has stood the test of time as a useful valuation metric, especially for those who make dividends central to their investing process. My Gordon Growth model inputs are below:

1. Next Year's dividend: $4.20

2. Phillips 66 Equity Cost of Capital: 11.85% (Source: Valueinvesting.io )

3. Phillips 66 5-year Dividend Growth Rate: 10.12% (Source: Seeking Alpha)

The intrinsic value is the dividend divided by the equity cost of capital minus the dividend growth rate (4.20/1.73%)= $242.77. This represents about a 150% premium from the price on 4/27/23 around 2 pm. Obviously, this broad metric suggests that the stock's current price is a bargain when using the GGM.

Of course, this metric shouldn't be used alone, and the output price I get should not be construed as a price target. It is simply one method of valuation that suggests, based on the next year's dividend yield and the long-term growth rate of the dividends, that the stock is very undervalued.

Risks And Where I Could Be Wrong

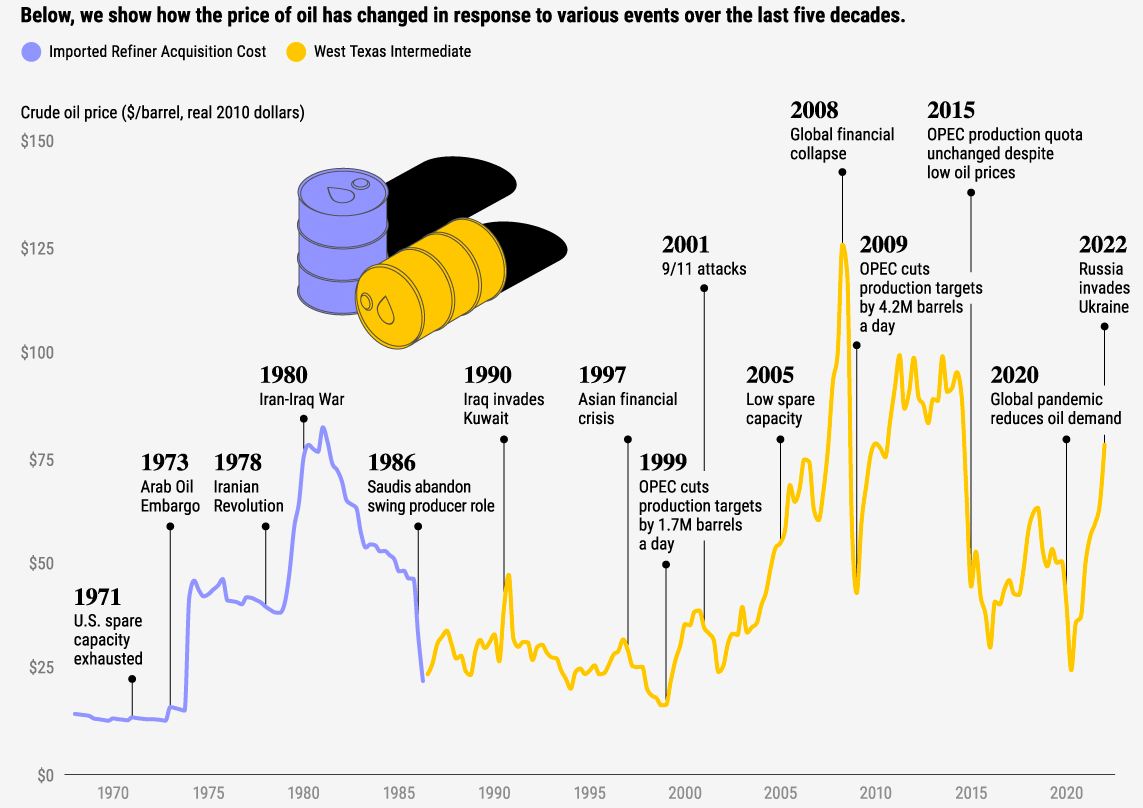

The Energy sector is a volatile one. Making money drilling holes in the ground and all the associated refining and such that goes with it certainly isn't for the faint of heart. Geopolitical risk is elevated in our current environment. There are increasing signs that the global energy market of the last four decades might be splintering due to the War in Ukraine and increasingly assertive non-aligned members of OPEC.

Environmental and safety regulations are also a major concern for oil refiners. Luckily for Phillips 66, it has a pristine safety record that is the envy of many in the industry. However, there has been some pushback on one the company's major green initiatives in Rodeo, CA that could probe problematic reputationally. Overall though, I see the risk of environmental externalities as relatively lower than many other Energy sector companies.

The volatility in spreads for refining is always a risk for these companies. It is somewhat mitigated for Phillips 66 by its strong chemicals segment. Refining is roughly two-thirds of the business. It's nice to have some diversification, but anything that causes crack spreads to diminish materially could hurt profitability and threaten the dividend.

EIA, Refinitiv, Visual Capitalist

{kind=link}

Overall, the largest risk to this firm is the general commodity price risk that can occur during recessions. If there is a severe economic contraction and demand is severely curtailed, this firm will suffer with the rest of the industry, even given its relative resilience.

Conclusion

There are both tactical and long-term reasons to be an owner of Phillips 66. This name has many positives, including its strong dividend, shareholder-oriented management, leading refining assets, and robust chemicals segment. The Energy sector has had to become more shareholder-friendly as the externalities of fossil fuels have come front and center in the public consciousness. Refiners are advantaged because their business models give them economic characteristics that mitigate some of the coarser parts of Energy investing.

Phillips 66 has been boosting efficiency across the organization by lowering headcount, improving the balance sheet, and making technological strides in refining itself. The company's focus on delivering to shareholders is admirable, and it continues to refine and improve its organization and assets to ensure it can continue to for the long-haul. I suspect this name will be a coveted compounder in the coming years. Get in while the valuation is still attractive.

For further details see:

Phillips 66: Attractively Valued Refiner With Quality Yield