PSX - Phillips 66: Buy The Drop And Secure A 3.9% Dividend Yield

Summary

- Investors have the opportunity to take advantage of a minor, post-earnings selloff for PSX.

- Refining strength is driving Phillips 66’s profit growth.

- Phillips 66 has an attractive P/E ratio of below 5x.

Phillips 66 ( PSX ) is an integrated energy company with significant midstream, refining, and chemical assets. The company's stock plummeted after it reported fourth-quarter earnings that fell slightly short of expectations.

Having said that, Phillips 66, in my opinion, is an appealing addition to a passive income portfolio because the market overreacted to the earnings release and Phillips 66 can be expected to continue paying a solid dividend.

The company's low earnings multiple of 4.6x, which implies a high margin of safety, makes PSX particularly appealing.

Profit Miss Creates Opportunity

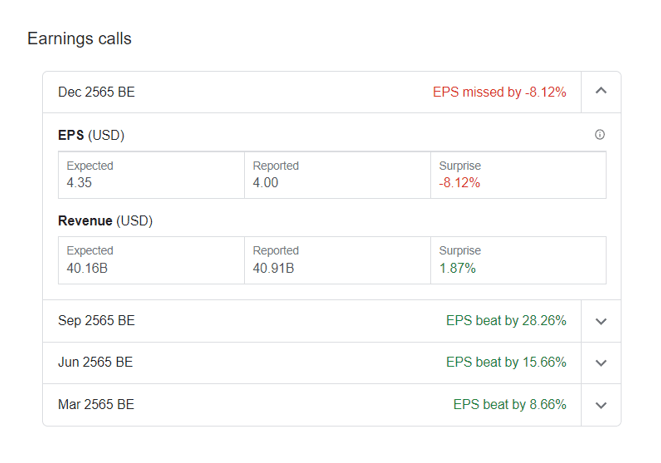

Phillips 66 reported fourth-quarter profits yesterday, and the company fell short of expectations, but only by a small margin. The refinery behemoth earned $4.00 per share in adjusted profits for the fourth quarter, falling short of the $4.35 per share profit estimate, resulting in a profit miss of about 8%.

As a result, the refinery's stock price fell 5.78%, creating an opportunity for passive income investors to consider the refinery play at a lower earnings multiple and a higher dividend yield.

{kind=link}

Refining Gains Drive Phillips 66's Financial Results

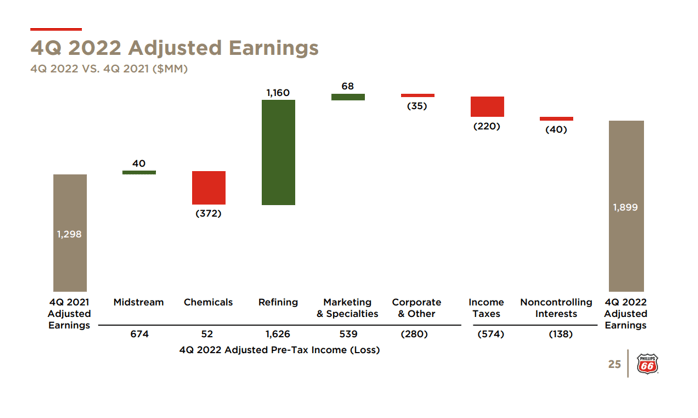

Phillips 66 owns pipelines, chemical manufacturing and refining facilities, and over 8.8K marketing/specialty outlets where the company's products are sold. Phillips 66's refining business is by far the most profitable, accounting for $1.63 billion in adjusted earnings in the fourth quarter. Refining profits increased 249% YoY due to a broader fallout from the Ukraine war as well as a chronic shortage of refinery capacity in the United States.

Adjusted Earnings (Phillips 66)

{kind=link}

Refining capacity fell in the United States for two consecutive years, and a lack of refining capacity explains why companies that operate refineries have done well recently.

The chart below, which highlights refinery capacity between 2013 and 2022, is based on information and data provided by the United States Energy Information Administration. Due to a lack of investment in new refineries over the last decade, annual refinery capacity in the United States is now at the same level as it was in 2014.

Distillation Capacity (U.S. Energy Information Administration)

{kind=link}

This is good news for Phillips 66, which is raking in cash from its refining operations. The refining segment benefited from the highest fourth-quarter earnings growth and was the primary driver of Phillips 66's adjusted profit growth in 4Q-22.

4Q'22 Adjusted Earnings (Phillips 66)

{kind=link}

PSX Is A Distribution Play

Phillips 66 has a decade of consistent dividend growth, which is probably the most appealing aspect of owning the company's stock in a dividend-oriented portfolio.

Phillips 66 increased its dividend from $1.33 per share in 2013 to $3.88 per share in 2022, representing a 192% increase in total dividend growth.

Passive income investors can secure a very good 3.9% dividend yield from one of the largest refinery companies in the United States, based on a current pay-out of $0.97 per share per quarter.

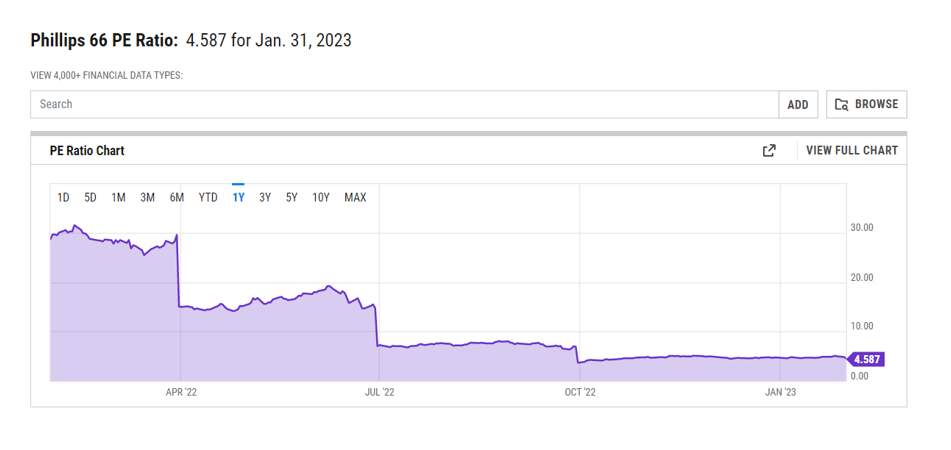

PSX's Valuation Reflects A High Margin Of Safety

Phillips 66 is currently trading at an unreasonably low earnings multiple of 4.6x. In my opinion, the valuation reflects a very high margin of safety.

According to Morningstar , the 5-year average earnings multiple is 15.7x. Considering the company's low earnings valuation, I believe the refinery company offers attractive total return potential to passive income investors over the next 12 months.

{kind=link}

Why Phillips 66 Could See A Lower Valuation

Sanctions on Russian oil imports have boosted refining margins in the sector, as have under-investments in U.S. refinery capacity, which has been driving Phillips 66's profit growth.

Because the refining business is the most important part of Phillips 66, anything that affects refining margins, such as the supply of refining capacity in the United States or the availability and cost of feedstocks, will have a disproportionate impact on Phillips 66's profit trends.

A decline in refining margins is therefore a potentially significant headwind for Phillips 66, even though I do not believe the dividend will be jeopardized.

My Conclusion

Phillips 66 is a consistent dividend payer with a lot of long-term potential.

Even though the company did not meet profit expectations for the fourth quarter, I believe investors will quickly forget about the relatively minor profit miss and return their attention to Phillips 66's positive supply-demand situation, strong dividend yield, and low earnings valuation.

The 3.9% dividend yield is appealing, and Phillips 66 is likely to increase its dividend in the coming years.

For further details see:

Phillips 66: Buy The Drop And Secure A 3.9% Dividend Yield