PSX - Phillips 66: Crack Level Normalization Expected In 2024 (Rating Downgrade)

2024-01-11 05:58:51 ET

Summary

- Phillips 66 might benefit from the conflict in the Middle East, and US refineries become a replacement for the disrupted diesel supply.

- We reported our pushback on Elliott's investment, with a downside protection on the disposal plan.

- Neutral rating due to a crack spread normalization level and a full valuation based on EV/EBITDA, EV/FCF, and P/E target.

Here at the Lab, we have a long-standing buy rating on Phillips 66 (PSX). We performed a comps analysis in our first publications, favoring Phillips 66 over HF Sinclair. Looking at the stock price performance, we arrived at a total return of +65% (including dividends payment), and our forecast on a better exposure to Europe, a potential buyback, further debt reduction, and an upside on CPChem proved correct.

{kind=link}

Mare Past Analysis

With this note, we update our Phillips 66 models and discuss key themes in 2024. Despite several headwinds, 2023 has been a resilient year for the company. Looking back, April was a momentum of a macroeconomic scare; in September, gasoline cracks collapsed, the 2023 winter was warmer than expected, and refinery productions are coming back from heavy yearly maintenance, which is coupled with new global capacity ramping up. On a positive note, inventory levels are better, and gasoline cracks have improved relative to seasonal norms. On a macro basis, looking ahead, our team's 2024 reasonable assumptions are set for a supportive fundamental environment on the mid-cycle crack spread. In our estimates, we forecast mid-cycle level but below 2023 results. In numbers, to put 2023 performance into perspective, the crack spread was around $26 per barrel, compared to a 2022 record level of $34 per barrel. In Q4, we forecasted that EC gasoline, EC diesel, and EC 321 spread at $9.5, $38, and $18.5 per barrel, respectively. Looking ahead, in 2024, for the above crack spread, our estimates are set at $16.5, $33, and $22.5. Diesel demand is strong, and we start with better inventories. In addition, in the past, the EU had an almost unlimited source of diesel within a week's sailing of Northern European ports. After the Russian invasion, the routes have become longer, and more ships are needed to transport an equal quantity of product. This CAPEX constraint favors US refineries. Moreover, sanctions imposed on Russia have deprived Europeans of their largest diesel supplier. To replace the Russians, Europe turned to the countries of the Middle and Far East. With the Israel-Gaza retaliation, diesel supply that usually passed through the Red Sea and crossed the Suez Canal is now almost interrupted . Here at the Lab, we believe that (once again) the United States refineries will benefit from this conflict, especially Phillipps 66, which has a strong EU presence and relationship.

Why are we now neutral?

Investors welcomed Elliott's involvement in Phillips 66 as they anticipated it would increase the chance of successfully implementing the new company's plan. Here at the Lab, we believe the company has established an operational program efficiency to unlock shareholder value. However, investors believe that Elliot can extrapolate an additional 75% return with a series of constructive dialogue. Well, we do not foresee this extra performance. Still, starting with the positive, we believe Elliot's involvement could provide downside protection on a potential SOTP valuation and might further unlock value with disposal if the CEO does not hit the company's goals.

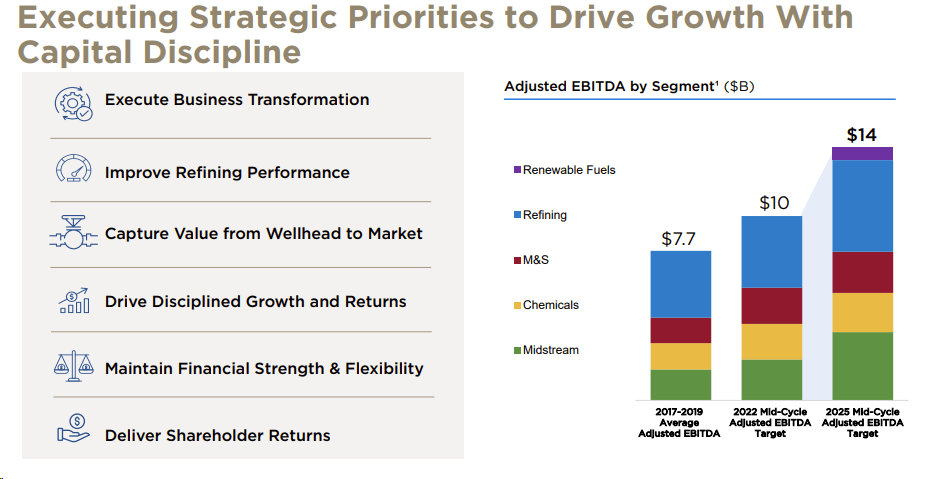

Our significant pushback is how the company will reach a $14 billion mid-cycle EBITDA target (Fig below). According to our calculation and reversing Phillips 66 EBITDA, the company should generate +$7 billion in a mid-cycle cracks environment. The company will likely achieve $6.5 billion EBITDA in 2023 with a composite crack spread above $30 per barrel. However, our estimates forecast a lower level for 2024, which could create significant headwinds for the refining business. Looking at Elliot's letter , if the CEO does not progress toward its 2025 financial targets over the next year, the best option is to sell non-strategic assets to unlock shareholder value. Elliott Management is confident of generating $15- $20 billion after-tax cash with a portion of its non-operated midstream stakes, European convenience stores, and CPChem stake. Here at the Lab, we arrived at an aggregate value of $10 and $12 billion. Based on a normalized chemical EBITDA of $1.5 billion and a 7.0x multiple (including $2 billion of debt), we arrived at net pre-tax cash proceeds of $9.0 billion. In the best case, the remaining assets could get $2.5/3.0 billion in value. Therefore, we are skeptical of the disposal plan and have a discrepancy valuation gap with Elliot of at least $3 billion.

We anticipate a 2024 EBITDA of $10.5 billion in our forward estimates. For 2024, the company is budgeting a total of $3.24 billion in investments, including a CAPEX of $2.23 billion at the operated level. We arrived at a forecast D&A of $1.7 billion and a core operating profit of $8.8 billion.

Phillips 66 adj. EBITDA target (Phillips 66 Jan Investor Update)

{kind=link}

Conclusion and valuation

We supported the company in the past thanks to a compelling valuation and upside from a shareholder remuneration story (on buyback). Currently, we see a limited stock price appreciation opportunity. Phillips 66 has invested much of the past several years underperforming the refining market, and the company's operation has been somewhat disappointing. Q1 2023 maintenance bodes well for Q1 2024 comps. The company has also increased its 2024 return of capital guidance pace. However, it trades at a 2024 EV/EBITDA of 7x with a P/E normalized of 10x. We arrived at a 2024 EPS of $14 per share in our estimates. In our long-term assumption, the 321 crack spread is forecasted at $11.5 per barrel with a crude differential of $3.5. WACC is at 8.0%, with a 22% corporate tax rate. Using an FCF/EV yield of approximately 8%, similar to large-cap refining peers, we arrived at a stock price of $139 per share and decided to move our Buy to a Neutral rating. In addition, even if we project a 5% dividend hike, the company's yield is at a low 3.3%. Global macroeconomic headwinds remain the most significant threat to this outlook, and we also believe that the company could face some short-term pressure. Downside risks include weaker Brent prices causing contraction in olefin margins, midstream margins not meeting consensus, weakening natural gas prices, and weaker-than-anticipated refining margins.

For further details see:

Phillips 66: Crack Level Normalization Expected In 2024 (Rating Downgrade)