PSX - Phillips 66: Growing Refiner Supply Inelasticity Drives Structural Profit Growth

2023-03-09 17:58:11 ET

Summary

- Phillips 66 and its peers had record profits in 2022 amid a massive increase in the spread between gasoline and oil prices.

- Declining global and US refinery capacity and low capacity utilization has caused diesel and gasoline prices to remain elevated compared to oil.

- Refinery capacity utilization plummeted in recent weeks amid a slight decline in fuel demand.

- Phillips 66 may benefit from a permanent rise in crack spreads due to extreme underinvestment in the refinery sector.

- PSX appears to be an attractive long-term opportunity at its current valuation, although a recession may cause a temporary correction.

One year ago, gasoline prices rose rapidly, with the national average retail conventional price nearing $5 per gallon. Gasoline prices have consolidated dramatically since then due to increased crude oil production, improvements in refinery output, and massive oil stimulus from the Strategic Petroleum Reserve withdrawal. This trend has hampered the value of many oil-producing companies; however, most refinery stocks, such as Phillips 66 ( PSX ), have maintained high valuations.

PSX is a fascinating stock today because it trades at a lower 7X "P/E" ratio and has had a strong performance over the past year despite headwinds in the energy market. Despite its elevated stock price, PSX's TTM earnings yield (inverse of "P/E") is near a record level, indicating the stock may be considered undervalued today. See below:

Phillips 66 fundamentally differs from most energy stocks since it focuses primarily on the energy market's midstream and downstream segments, giving it no direct exposure to crude oil prices. Instead, the spreads between oil and various oil products heavily influence PSX's income. Phillips 66 is also exposed to the overall demand for energy through its midstream and marketing segments. Today, energy demand is tremendous, and now that infrastructure growth is slowing, Phillips 66 is operating in a less competitive (or more stable) midstream and marketing environment.

Further, decades of no refining growth in the US (and most of the western world) are catching up with the market. A relatively large refining capacity gap will persist for many years as no new refineries are built. This situation appears to create "monopoly-like" conditions in the refining industry where massive barriers to entry (regulations, costs, etc.) limit refining capacity growth and point toward a long-term decline in capacity. With this in mind, Phillips 66 may benefit from elevated "crack spreads" indefinitely, keeping its profit levels much higher than they've been over the past decade. While PSX is a riskier and volatile stock, it may be a rare discount opportunity today.

Higher for Longer Crack Spreads?

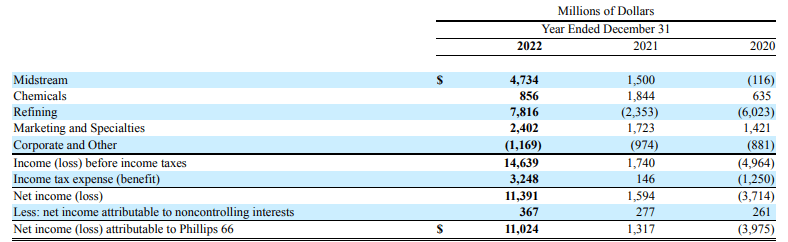

The cornerstone of Phillips 66's business is its refining segment. The company operates significant midstream, chemicals, and marketing businesses, but its refining business is the primary driver of volatility in its income. See Phillips 66's segment income below:

{kind=link}

The company's three non-refining businesses are less volatile, but offer lower potential income. The refinery business has been much more volatile since 2020, as lockdowns created a significant decline in gasoline demand that caused Phillips 66 to reduce production and investment levels . The company, and its peers, have been prolonged to restore output levels due to high costs and labor shortages . Of course, fuel demand returned to peak levels very quickly in 2020, creating a substantial deficit. Accordingly, the company faced massive losses in its refinery segment in 2020 and equally abnormal profits last year as "crack spreads" skyrocketed.

Crack spreads differ between oil product prices, such as gasoline, diesel, and jet fuel. This figure drives Phillips 66's profit margin since the company buys oil and turns it into various petroleum products. Typically, spreads are around $10-$30 per barrel but have been over $30 for most of the past year. See below:

Late last year, Phillips 66 appeared to be a questionable investment as crack spreads were falling and seemed likely to return to normal levels . The company's EPS would be much lower than the past year if the crack spreads normalized. However, the spreads have shown excellent resistance to falling below the $30-$40 range, indicating there may be long-term issues in the refining industry that are causing permanent increases in production margins.

Crack spreads are elevated due to a decline in refinery capacity and low utilization of existing capacity. US and global Refining capacity slid in 2020 and 2021, falling back to ~2010 levels despite high demand (see "products supplied"). More recently, refining capacity utilization has nosedived amid a slight decline in demand. See below:

The rebound in refining capacity utilization last year indicated that crack spreads were likely to normalize. However, the recent significant decline in capacity utilization and refining net input means refiners may struggle to maintain production levels. At the end of last year, refiners were consistently operating at breakneck speeds, with capacity utilization consistently above 90%. However, demand levels have declined slightly (see "products supplied" above), potentially due to an economic slowdown or recession. Refiners have matched the decline with a substantial reduction in inputs and capacity utilization, indicating a conservative position that may ensure high crack spreads even with lower demand.

Since 2020, refinery companies have changed their business goals from growth to "shareholder value." Despite massive profit increases, Philips 66, Marathon ( MPC ), and Valero ( VLO ) (the most prominent US refiners) have all reduced Capex levels to extreme lows. Further, these firms' "cash from financing" levels have fallen to immensely negative levels, indicating a combined goal to return cash to stakeholders (through debt reduction, dividends, or share repurchases). See below:

All three of these refiners and virtually all large energy companies I've seen (including Chevron and Exonn) have made the same changes since 2020. From around 2014 to 2019, most energy companies were chronically unprofitable amid substantial growth in US oil and natural gas production and overgrowth of the midstream transportation sector. This "glut era" was driven by the development of the US shale production industry. However, during the "lockdown era," there was no effort by energy producers to continue to expand production or downstream infrastructure. Indeed, as evidenced by stagnating oil production , a falling rig count , and declining refining capacity, major US energy companies may not even be spending enough in CapEx to maintain current output levels.

Refinery Capacity Faces Terminal Decline

There are a few reasons for this fundamental shift away from growth. For one, more than half of workers in the oil and gas sector want to leave, creating an ongoing shortage across the energy sector. While pay issues may be an aspect of poor labor sentiment, frustration after massive job cuts in 2020, an aging skilled workforce, and high job stress are also crucial factors. The increase in energy prices and materials costs also has limited energy companies' willingness to invest in new infrastructure. Of course, the massive rise in interest rates is also critical in discouraging borrowing for growth and encouraging debt reduction.

The most significant factor limiting energy output growth is likely the lack of refining capacity after decades of no refining growth in the US. Regardless of oil supply and energy demand, all segments of the energy pipeline are tied to refining capacity, as it is the primary bottleneck. Refineries are tremendously expensive, with 10-year capital investment commitments.

With the US and most of the developed world looking to transition away from fossil fuels, it makes little sense for refiners to make significant long-term investments since the payback time is limited (or perceived to be limited). While many may argue that clean energy is not growing nearly quickly enough to replace fossil fuels soon, this perception has limited interest in the energy sector for younger people ("why pursue a dying career"?). It also discourages financial investment in the industry (leading to higher debt costs) and is backed by political and regulatory efforts.

In my opinion, there is a large gap between the reality of the fossil fuels energy sector and the perception that it will be replaced by clean energy. In the long run, the fossil fuels sector will inevitably be replaced (since supplies are inherently limited). Still, that change may be many decades away (at the current rate of "clean" infrastructure growth). However, in the immediate term, negative fossil fuel perceptions are creating substantial declines in infrastructure growth to the extent that capital investment appears to be below maintenance levels. Indeed, even if gasoline prices and crack spreads remain abnormally high, I doubt refiners will make significant infrastructure investments due to this perception and the immense time-value costs of making investments. Further, I believe refinery capacity utilization may remain constrained by labor shortages, as over two-thirds of refiner workers are over 40, and only 5% are below the age of 30 - indicating a vast long-term labor shortage issue.

What is Phillips 66 Worth Today?

Due to the immediate and long-term factors facing the energy sector, specifically the refining industry, I believe there may be a structural increase in energy crack spreads. Fundamentally, now that infrastructure investment levels have collapsed, Phillips 66 is backed by a very attractive business economy. Gasoline is historically "demand inelastic," wherein a price rise does not cause demand to fall dramatically (since it is used to transport virtually everything). This attribute also means the market can maintain high prices even with a recession if production does not continue to grow.

More importantly, the "supply curve" of petroleum products has become highly inelastic, wherein refiners are essentially unwilling to pursue capacity growth regardless of profit margins. Indeed, production has declined since 2019 despite a significant increase in profitability. This situation is uncommon but logical, considering most refiners are concerned that transportation fuel will be replaced by clean energy alternatives over the next two decades. Higher debt costs and a lack of skilled workers also significantly limit their ability to increase capacity.

In the past, Phillip 66's profits were constrained by output growth from competitors. This is a particularly crucial factor for its refining business, but also its midstream and other segments. Crack spreads may fluctuate dramatically over the coming years but remain above the $30-$40 range permanently due to the many refinery supply constraints. Many factors could influence Phillip 66's profits, but I believe its EPS may average in the $15-$20 range over the coming years due to this change, above the $10-$15 consensus target. A recession this year could cause its EPS to fall below my target, but in the long run, I believe a recession could benefit the sector by further constraining infrastructure investment.

Even at the $10-$15 long-term annual EPS target range, PSX would be cheap today with a long-term forward "P/E" of ~7-10X. However, assuming crack spreads create a new stable range at or above current levels, PSX's long-term forward "P/E" would likely be closer to 5-7X today. In my view, that is extremely low, with a $150+ share price more reasonable given a $15+ expected long-term EPS.

I am moderately bullish on PSX today and believe it is a solid long-term value investment. Over the next five to ten years, I suspect it will continue to deliver excessive profits as refining capacity and utilization falters due primarily to significant underinvestment. The stock appears significantly undervalued, even based on more conservative EPS targets. PSX may be a better "dollar-cost-average" investment because it could decline materially in the short term in energy demand declines due to a recession. Given "petroleum products supplied" levels are falling, it may be best to wait for a correction before investing heavily in PSX.

For further details see:

Phillips 66: Growing Refiner "Supply Inelasticity" Drives Structural Profit Growth