VLO - Phillips 66: Harvesting Juicy Energy Dividends

2023-05-30 17:13:18 ET

Summary

- Phillips 66 offers value and yield in the refining and chemical sector, with a strong long-term outlook and significant progress in its core business.

- The company's extensive chemical footprint, including the joint venture with Chevron Phillips Chemical Company LLC (CPChem), sets it apart from competitors and positions it well for the growing demand for advanced chemicals.

- With a healthy balance sheet and attractive valuation, PSX offers a potential upside of 28% to $120 per share and a longer-term target of $150.

Introduction

The global economy isn't in great shape. Germany officially entered a recession, Chinese reopening is sluggish, and economic growth indicators in the US hint at a recession.

Real Investment Advice

In light of these developments, I believe that tremendous value can be found in cyclical areas that offer good yields and capital gains the moment economic expectations bottom.

One of my favorite areas to look for these qualities is refining - or energy downstream. Phillips 66 ( PSX ) , one of America's largest refining stocks with a large chemical footprint, is currently trading 16% below its 52-week high after losing 9% of its value since the start of the year.

The company is now yielding close to 4.5%, which could turn into an even better yield due to the aforementioned economic challenges. This is what I wrote in my prior article :

While I believe that the stock is 50% below its fair value, I do not rule out another move lower in light of economic challenges and the odds of investors de-risking their portfolios.

Furthermore, the company's business is making great progress and seeing strong long-term demand.

In this article, I will make the case to add PSX shares on weakness if the market offers another opportunity.

So, let's get to it!

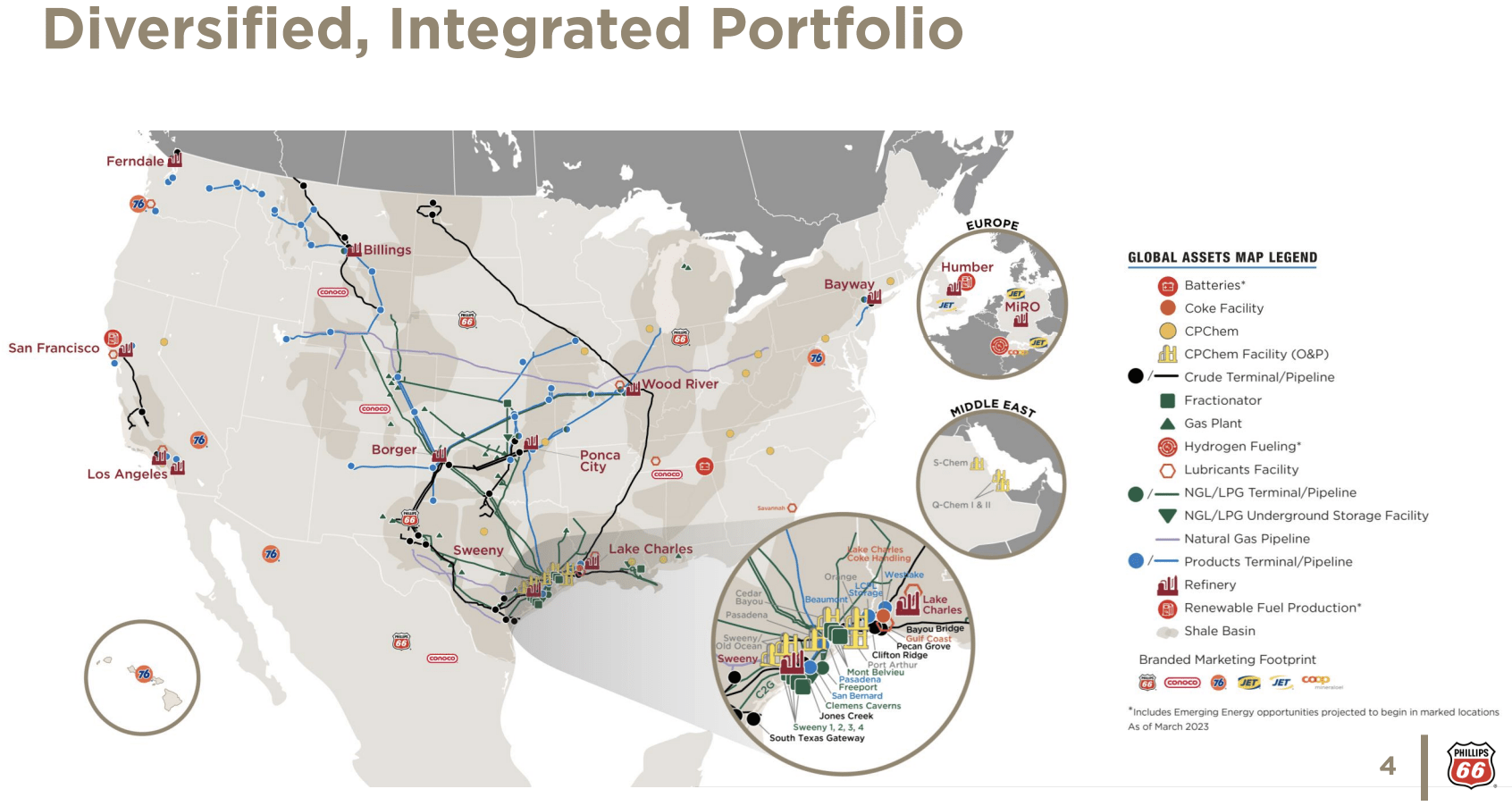

What Sets Phillips 66 Apart

Established in 2011 as a result of a spin-off from ConoccoPhillips, Phillips 66 embodies a fusion of midstream and downstream operations.

{kind=link}

Phillips 66

Last year, the United States accounted for 81% of the company's revenue, while the United Kingdom contributed 10% to its overall sales. The revenue was generated across the following segments:

- Marketing & specialties, constituting 66% of total sales.

- Refining, contributing 25%.

- Midstream operations 9%

Phillips 66 oversees the operation of 12 refineries, boasting a combined net crude throughput capacity of 1.9 million barrels per day.

Phillips 66

What distinguishes Phillips 66 from its competitors is its extensive chemical footprint. A pivotal aspect of this is the company's 50-50 joint venture with Chevron, known as Chevron Phillips Chemical Company LLC (CPChem).

Headquartered in Texas, CPChem specializes in the production and marketing of ethylene and other olefin products utilized in industrial processes.

Ethylene, a key component produced primarily through the cracking of hydrocarbon-based raw materials such as ethane, propane, butane, naphtha, and gas oil, is used in the production of plastics like polyethylene and polyvinyl chloride. As an observer in the chemical industry, I have witnessed a notable surge in demand for advanced, high-quality chemicals such as ethylene.

Additionally, CPChem manufactures and markets aromatics, styrenics, and specialty chemical products, including benzene, cyclohexane, styrene, polystyrene, organosulfur chemicals, solvents, catalysts, and chemicals used in drilling and mining.

In the United States alone, the company sold over 30,000 million pounds of chemicals last year.

Over the past five years, PSX shares have returned just 0.3%. Both its peers Valero Energy ( VLO ) and Marathon Petroleum ( MPC ), have outperformed the energy sector by a substantial margin.

The problem is that PSX isn't as efficient as its peers. It also has a much larger footprint in chemicals. Since the pandemic, the biggest profits were made in refining, which benefited from shutdown capacities and a rebound in demand. Hence, more money went into MPC and VLO than PSX.

Now, these tailwinds are turning into headwinds.

Headwinds Are Mounting

Earlier this month, Bloomberg reported that US refiners are increasingly turning to financial hedging strategies to secure profits amid the diminishing likelihood of a summer fuel demand boost and the potential for run cuts.

Commercial players, including refiners, have raised their bearish short positions in gasoline to at least 200,000 contracts this year, up from an average of 180,000 in the second half of the previous year.

The decline in refiners' profit margins (as seen below), driven by economic weaknesses in the US and China, has resulted in increased hedging activity.

Bloomberg

Global demand for diesel, often considered a measure of industrial activity, is also weakening. Recessionary fears have caused a significant drop in US gasoline demand, reducing hope for a strong summer season.

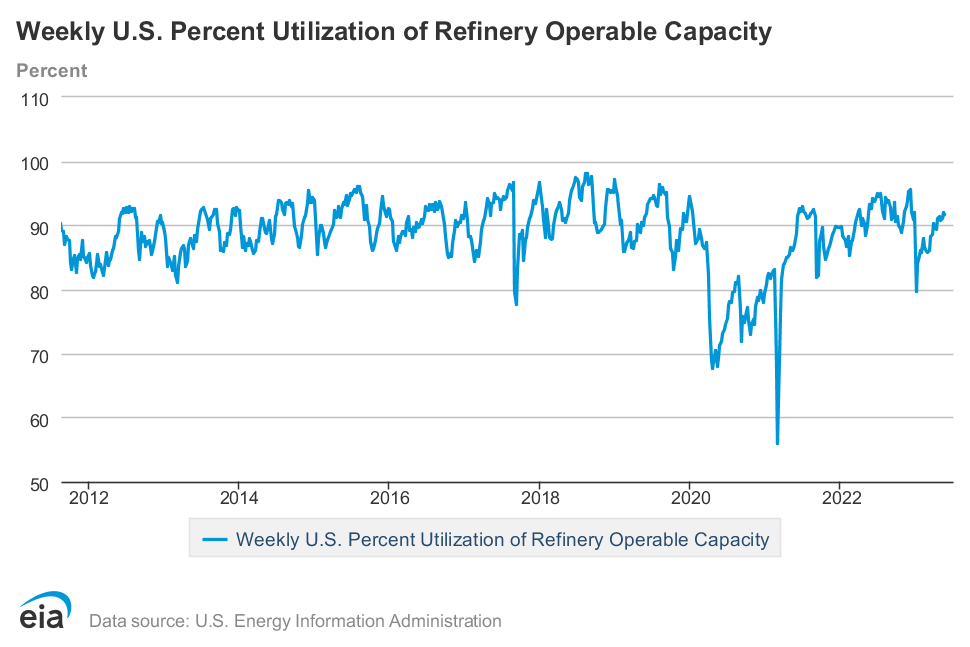

Refining utilization rates remain healthy in the low 90% range, which is accompanied by above-average maintenance operations, according to my sources.

{kind=link}

Energy Information Administration

The good news is that despite headwinds, Phillips 66 is doing well and is expected to see great improvements in its core business.

Phillips 66 Remains In A Good Spot

The company had a great start to this year. In the first quarter, PSX reported impressive financial and operating results, achieving adjusted earnings of $2 billion or $4.21 per share, marking a record first quarter.

According to the company , and in light of the aforementioned comments from Bloomberg, its refineries are currently operating at high utilization to meet demand and take advantage of market opportunities during the summer driving season.

The company also provided outlook information for the second quarter, including expectations of a mid-90s global O&P utilization rate in the Chemicals segment and a mid-90s worldwide crude utilization rate in the Refining segment.

Furthermore, heading into the gasoline driving season, US gasoline inventories are at their lowest level in roughly ten years. According to the company, octane spreads have also shown strength. On the diesel side, early in the year, demand was weaker due to a warmer winter, but it has firmed up, especially in the Mid-Continent planning season.

Turnaround expenses in the Refining segment are expected to be between $100 and $120 million. Corporate and Other costs for the second quarter are projected to be between $260 and $290 million, reflecting higher interest costs associated with recent financing activities.

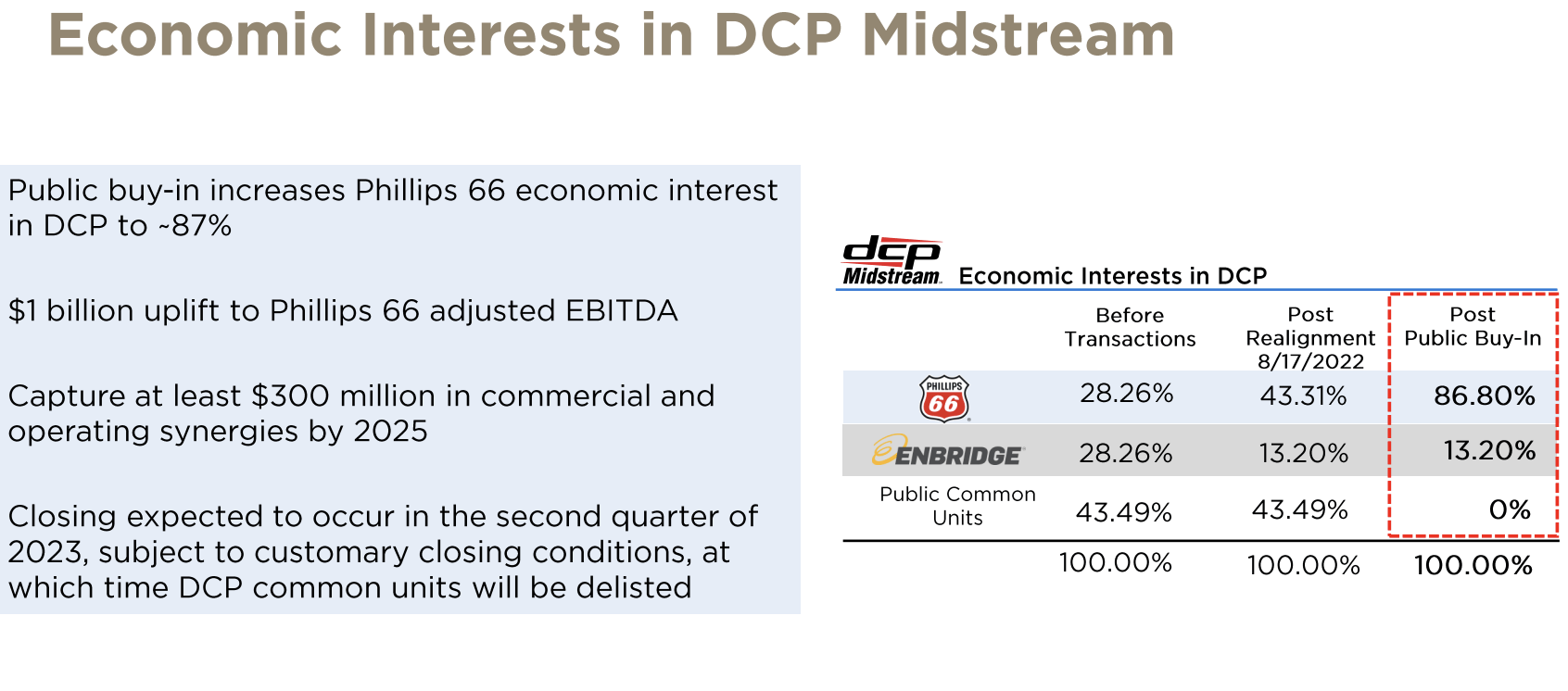

The pending buy-in of DCP Midstream's publicly held common units is expected to close during the second quarter, supported by senior unsecured notes and a delayed draw term loan.

By buying DCP Midstream, the company expects to generate at least $300 million in synergies by 2025. The company owns this project with midstream giant Enbridge ( ENB ).

{kind=link}

Phillips 66

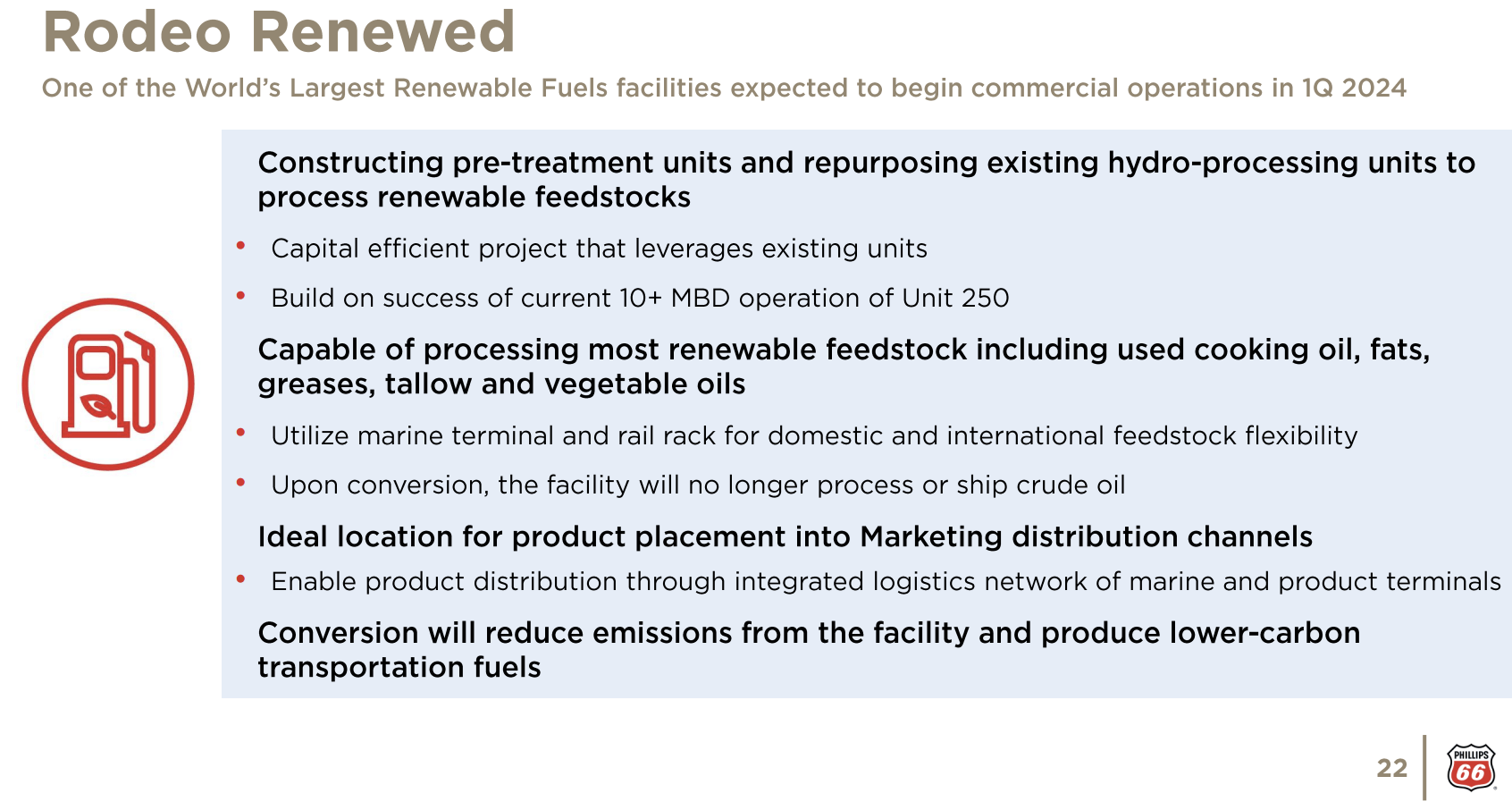

PSX also made tremendous progress in its renewable fuel and chemical businesses. For example, the San Francisco refinery is being converted into one of the world's largest renewable fuel facilities. This conversion will substantially reduce emissions from the facility and enable the production of lower carbon-intensity transportation fuels. The Santa Maria facility was safely shut down in February to advance the project, with commercial operations expected to begin in the first quarter of 2024.

The Rodeo facility, upon completion, will have a renewable fuel production capacity of over 50,000 barrels per day.

{kind=link}

Phillips 66

Furthermore, In the Chemicals segment, CPChem is pursuing a portfolio of high-return projects, including the construction of a second world-scale 1-hexene unit in Texas and the expansion of propylene splitting capacity at the Cedar Bayou facility.

These projects are anticipated to start in the second half of 2023. Additionally, CPChem and Qatar Energy are jointly building world-scale petrochemical facilities on the US Gulf Coast and in Qatar, with start-up expected in 2026.

PSX Shareholder Distributions

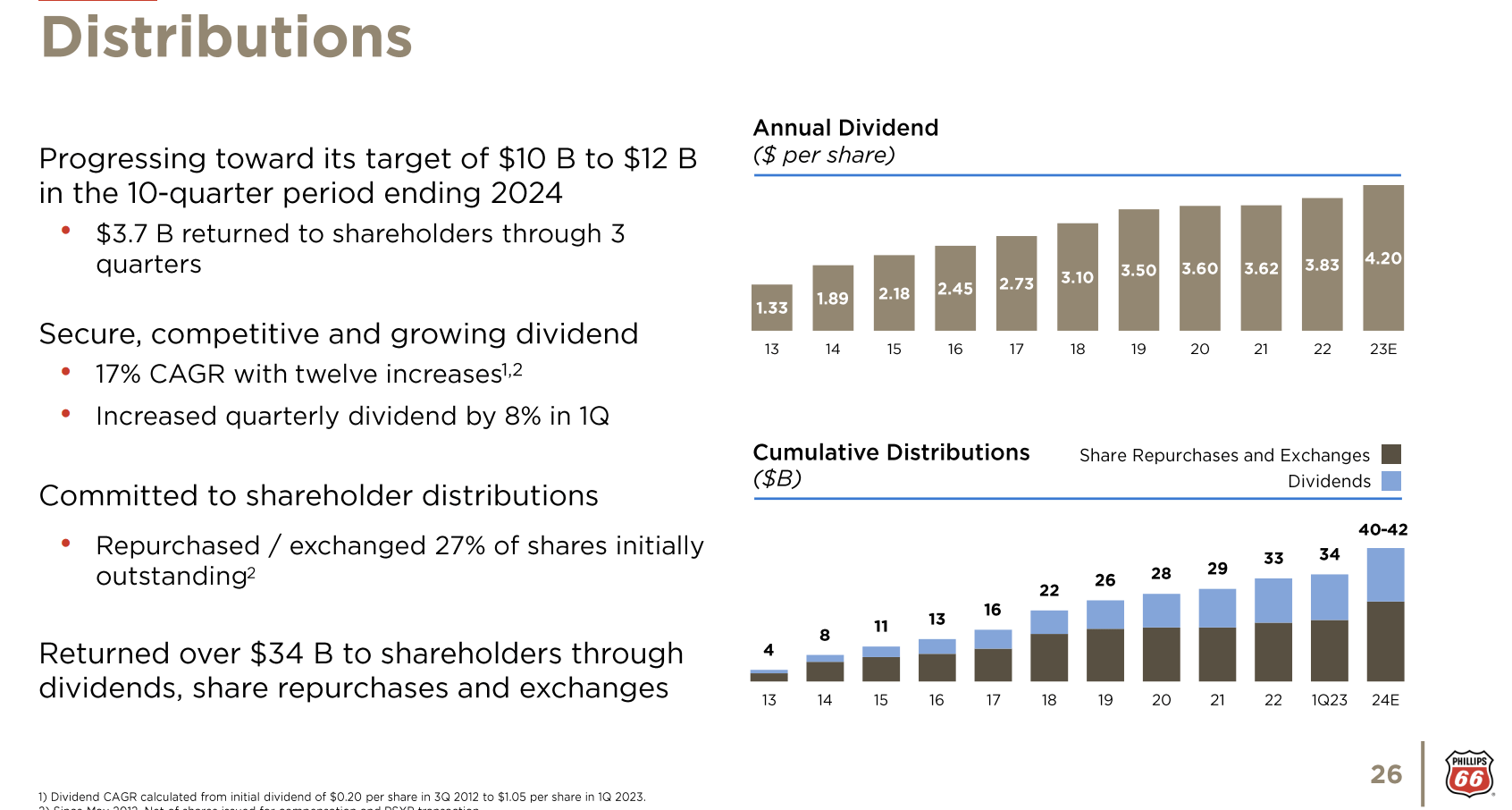

Since July 2022, Phillips 66 has returned $3.7 billion to shareholders through share repurchases and dividends. The company remains on track to achieve its target of returning $10 to $12 billion over the 10-quarter period between July 2022 and year-end 2024.

Since 2013, the company has grown its dividend by 17% per year. Over the past five years, that number has declined to 6.9%, which is still impressive, given that we're dealing with a current yield of 4.4%. In February, the company hiked its dividend by 8.2%. The payout ratio is at just 18%.

{kind=link}

Phillips 66

According to the company:

Our integrated diversified portfolio provides us with the ability to generate strong cash flow, return substantial cash to shareholders and invest in the most attractive projects. We remain committed to operating excellence and disciplined capital allocation as we execute our strategy.

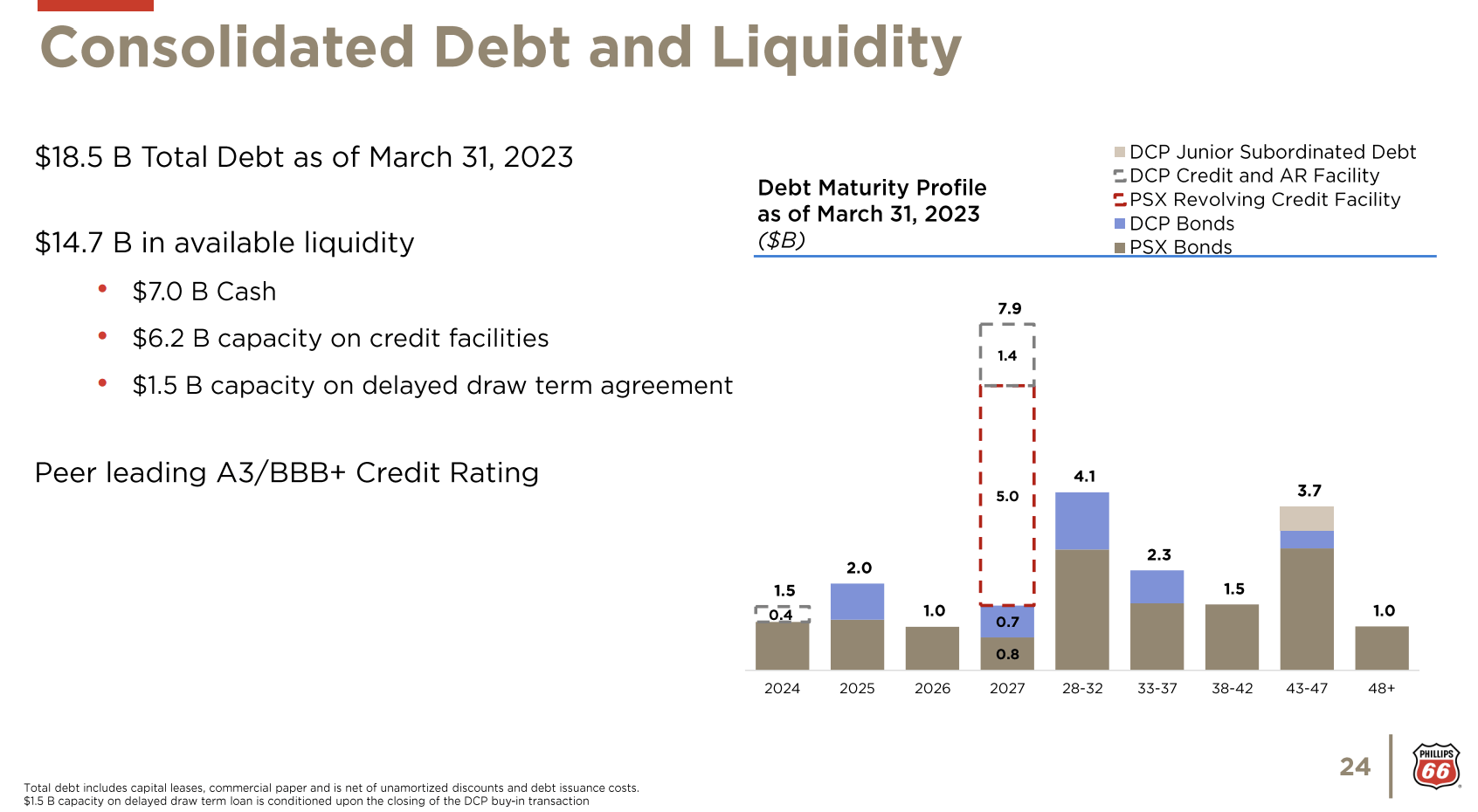

One reason why PSX is able to distribute so much cash to shareholders is its healthy balance sheet. The company has an A3/BBB+ rated balance sheet, $14.7 billion in available liquidity, and no major maturities until 2025. Its 2023E net leverage ratio is 1.0x EBITDA.

{kind=link}

Phillips 66

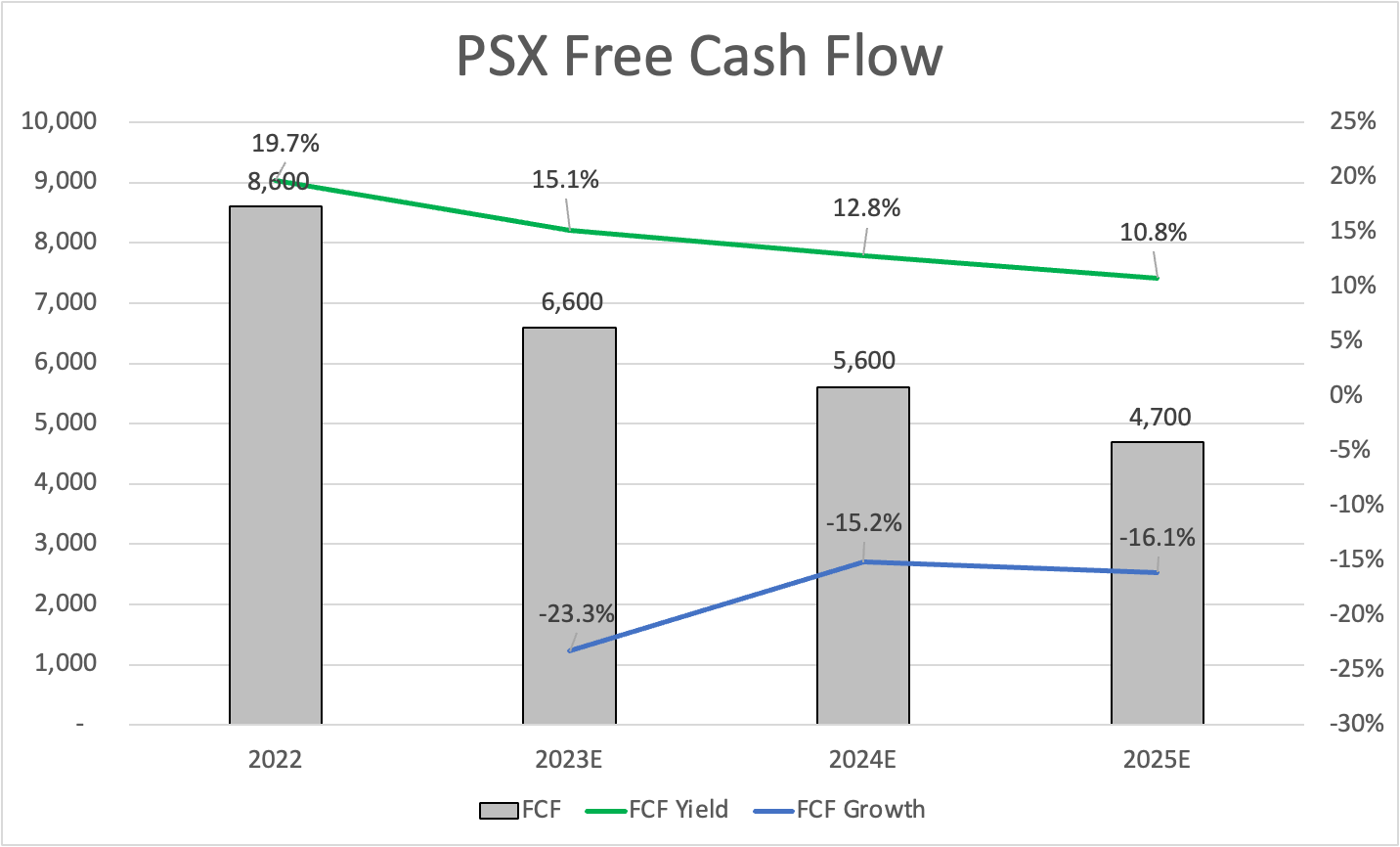

With that in mind, analysts expect Phillips 66's free cash flow to moderate in the years ahead as global margins come down due to new capacity additions.

Nonetheless, even according to these estimates, the company is expected to maintain a double-digit free cash flow yield, which paves the way for continuous dividend growth and buybacks.

{kind=link}

Leo Nelissen

It also indicates that the valuation remains attractive, as PSX shares are now trading at roughly 8x 2024E free cash flow.

Conservatively speaking, I would apply a 10x multiple, which indicates a 28% upside to $120 per share. $120 is the current analyst consensus estimates.

My longer-term target is $150, which - I believe - is a fair target the moment economic growth expectations bottom.

If I were in the market for more high-yield energy exposure in the refining/chemical business, I would be a buyer below $90.

As I wrote in my prior article, the stock could fall to the $70 to $80 area if economic conditions deteriorate further.

Takeaway

Phillips 66 presents a compelling opportunity for investors seeking value and yield in the refining and chemical sector. Despite economic challenges and headwinds in the industry, PSX has a strong long-term outlook and is making significant progress in its core business.

The company's extensive chemical footprint, including the joint venture with Chevron Phillips Chemical Company LLC (CPChem), sets it apart from competitors and positions it well for the growing demand for advanced chemicals.

While PSX has faced efficiency and profitability challenges compared to its peers, recent financial and operating results indicate positive momentum.

The company's commitment to shareholder distributions, demonstrated by share repurchases and growing dividends, further sweetens the deal.

With a healthy balance sheet and attractive valuation, PSX offers a potential upside of 28% to $120 per share and a longer-term target of $150.

Investors interested in high-yield energy exposure in the refining/chemical sector should consider buying below $90 while being aware of the potential for further downside if economic conditions worsen.

For further details see:

Phillips 66: Harvesting Juicy Energy Dividends