PSX - Phillips 66 Has A Lot More In Store For 2024

2024-01-10 18:02:46 ET

Summary

- Elliott Investment Management sent a letter to the board of PSX to spur additional cost savings to be more in line with peers Valero and Marathon.

- The current initiatives will close the gap while also driving meaningful share appreciation. The discretionary FCF generated from these efforts will be returned to shareholders.

- I project a 7% dividend raise in 2024 as well as at least $3 billion in share repurchases.

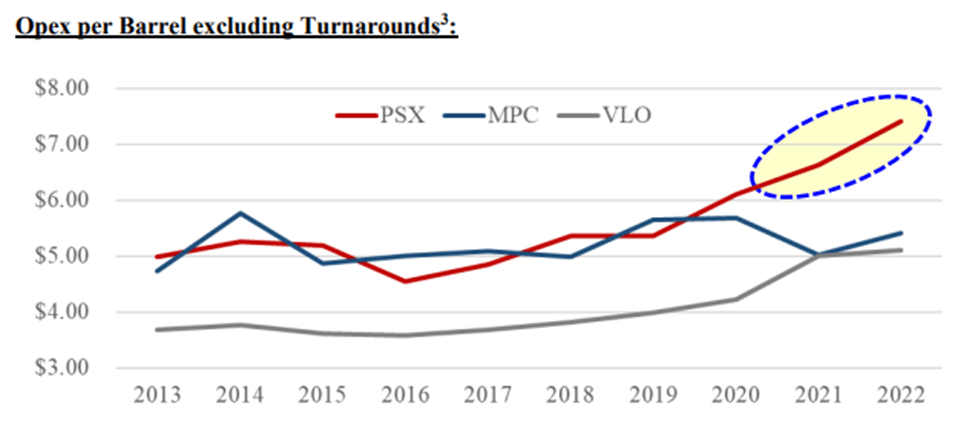

Phillips 66 ( PSX ) has seen a solid run up in share price thanks to the activity spurred on by the activist investor Elliott Investment Management. In a letter to the board , Elliott implied that PSX's refining assets can be run more effectively to drive costs out of the business. Elliott directly sited the growing gap in operating costs per barrel between PSX and peers Marathon and Valero.

The stock saw a 5% jump on the day of this announcement, adding to the 40% price appreciation since it bottomed in July of 2023. After an impressive run, does PSX have what it takes to follow through on its promises to shareholders and drive the share price higher?

This analysis will show that PSX does in fact have a run way to market beating returns in 2024. This is attributed to strong cost reduction efforts, startup of the Rodeo Renewed facility, and the stable performance of its midstream business.

This strong operational performance will be converted to shareholder returns as PSX executes on its goal of returning $13-$15 billion by the end of 2024. I project 2024 will see a 7% increase in the dividend while also returning at least $3 billion to shareholders in the form of share repurchases.

Driving Out Cost

Elliott Management's key point in advocating for change at PSX was an operating cost that was 50% on a per barrel basis. For companies that produce millions of barrels per day this can lead to significant loss in earnings. The letter references 2022 data, so PSX has 9 months of recorded performance in the books to gauge progress in this area.

Elliott's Letter to the Board of PSX

{kind=link}

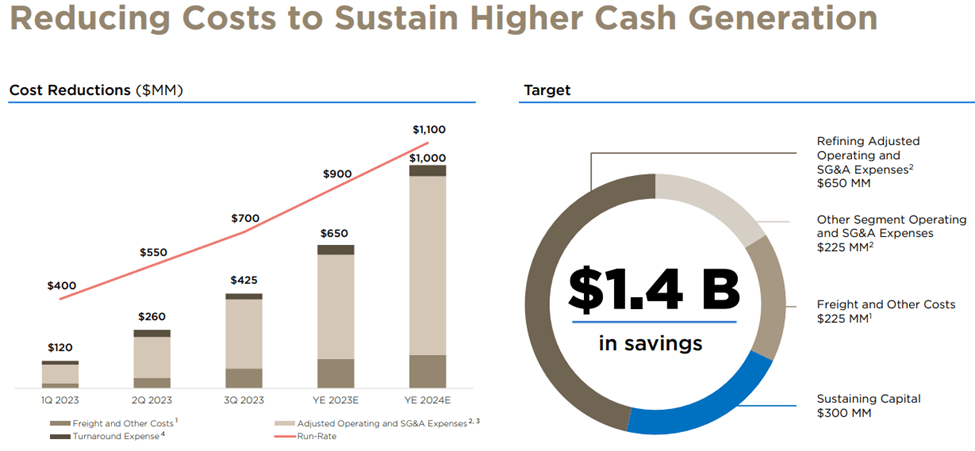

PSX has been able to realize savings of $650 million over the course of 2023 with another $350 being realized by the end of 2024. The full year effect of these savings is estimated to drive approximately $1.1 billion of costs out of the business on an annual basis.

At its current rate of production, PSX generates approximately 715 million barrels of product per year. This cost savings equates to a cost reduction of approximately $1.50/barrel. This will bring the 2024 exit OPEX/barrel down to the range of $6.00/barrel. Reductions in sustaining capital are projected to extract another $300 million in savings to drive PSX in the neighborhood of $5.60/barrel. While this would still make PSX the highest cost producer in the industry, it will no longer be such a ridiculous outlier from the pack.

Elliott believes that if management can reach its EBITDA goals of $9 billion in EBITDA by 2025, the company will be worth $205/share. This would be a 55% increase from today’s share price of $133.24/share. While there are some skeptics if PSX can achieve these goals, particularly given the challenges in CPChem (more on that later), improvements in its refinery position will generate a meaningful increase in shareholder value.

From Q3 exit, PSX expects to save $675 million annually between now and 2024 exit. Using the same valuation metrics (10% FCF) as Elliott Management, this would add $6.75 billion to the valuation of PSX, resulting in approximately 11.5% increase in the share price.

{kind=link}

Returns by the Numbers

Elliott's letter to the PSX board focuses on the profitability of the refinery segment. This makes sense as this segment generates nearly 60% of its income. However, it largely discounts the performance of its other two segments, Midstream and Marketing that generate the remaining 40%. Both of these groups are significantly less cyclical and provide a reliable earnings base.

In Q3, PSX revised its commitment to shareholders and raised the bar on shareholder returns. The company originally guided to return between $10-$12 billion over a time period stretching from mid-2022 to year end 2024. Now that we are at the midpoint of that program, PSX raised the guidance to between $13 and $15 billion, a sizable increase.

In my previous analysis of PSX in March of 2023, I projected that the company would likely exceed the $12 billion mark even with refinery margins falling from record 2022 performance. Now almost a full year later, and $6.7 billion into the program lets dive into what shareholders can expect.

By year end, PSX is on track to generate $7.7 billion in net income , a healthy reduction from $11 billion in 2022. This is not entirely surprising as crack spreads have declined after a record year. However, the company is continuing its efforts on cost control and projects to realize another $350 million in cost savings during 2024. Additionally, the Rodeo Renewed project is slated to come online in the first quarter and contribute $700 million of EBITDA for the company.

I have also modeled in further refinery margin decline for conservatism. In my base case scenario, refinery margins fall 20% from 2023 levels. I also model Rodeo Renewed as not contributing to the bottom line for added conservatism. To round out expenses, the company projects to spend $2.2 billion in CAPEX during 2024. All told, PSX stands to generate $7 billion in cash during the year.

| 2024e |

| 2023 Net Income |

| $7.7B |

| Cost Savings |

| $0.35B |

| Rodeo Renewed Startup |

| $0B |

| CPChem Startups |

| $0.1B |

| Changes in Refinery Margins |

| ($0.75B) |

| Depreciation |

| $2.0B |

| CAPEX |

| ($2.2B) |

| Net Cash Generation |

| $7.2B |

Now that we established a conservative earnings profile for 2024, it is possible to analyze how that cash is distributed to shareholders. The table below shows that PSX can still deliver $5 billion in 2024 back to shareholders and still generate a positive net cash position for the company.

| 2024e |

| Net Cash Generation |

| $7.2B |

| Dividend Cost |

| ($2.0B) |

| Debt Repayment |

| ($1.1B) |

| Share Repurchases |

| ($3.0B) |

| Net Cash Balance |

| $1.1B |

Under these projections, assuming $800 million in share repurchases in Q4 of 2023, PSX will deliver $13 billion back to shareholders as a base case scenario with $1.1 billion of margin remaining in the analysis.

Reaching the Top

To reach or exceed the top end of the guided returns, PSX will need to see stable or increasing crack spreads. Management has projected for a relatively stable supply and demand outlook for the next three years. The currently scheduled capacity additions and retirements appears to be fairly balanced with a slight skew to the undersupplied side of the scale.

I think as we look at capacity growth, there was about 1.5 million barrels a day of net capacity added in 2023. That compares to global demand growth of 2.2 million, 2.3 million barrels a day. As we look at 2024, we've got another, call it, net 1.4 million barrels a day of capacity being added. And as you look at the IEA, EIA and OPEC, demand expectations are pretty broad for next year, between 1 million barrels a day and 2 million barrels a day.

But as we look at 2025, 2026, the capacity growth is relatively modest and we do have a continuation of rationalization that's occurring Lyondell, Houston. We've got Grangemouth, UK, recently announced. Japanese refinery shutting down as well. So only about 1 million barrels a day of growth in 2025, 2026. So, not an overwhelming amount of capacity coming into the market.

If refining margins are flat this will re-inject $1.3 billion back into the cash flow model that can be deployed for additional share repurchases. This will easily drive PSX into the middle-to-top end range of its projected shareholder return program. Any benefit from Rodeo Renewed (which I expect to contribute at least $500 million) will drive PSX to the top of their range and possibly beyond.

A 7% increase in the Dividend

PSX has been a faithful steward of its dividend. In March of this year, CEO Mark Lasher gave a very promising outlook for how the company intends to treat the dividend.

And we had a hiatus from share repurchases during COVID. We consistently grew our dividend throughout COVID, so we didn't back off our dividend. We -- that's the promise we make. And we tend to view our dividend as an irrevocable promise. And so we're cautious about increasing that dividend. But at the pace of share repurchases we're making today, we see that incremental dividend cash being fairly consistent. So we'll increase the dividend per share over time. But as we repurchase shares, take those off the table. That will be a consistent amount at about right at $2 billion a year. And so that's the near-term shareholder return commitment that we made

Using the framework of a constant dividend cost allows the company to drive dividend growth through share retirement. This helps longtime shareholders to realize both appreciation and income.

PSX has spent an average of $950 million in share repurchases per quarter thus far in 2023. As of the end of Q3 it has retired nearly 25 million shares and is on track to retire an additional 7.5 million in Q4 for a total of 32.5 million shares. The savings from these retired shares will be reallocated back to the existing shares to drive the dividend cost back up to $2 billion a year or $500 million quarterly.

This equates to a 7.9% increase in the dividend if taken exactly to the $2 billion mark. I believe investors will see a quarterly dividend raise to approximately $1.13/share for 2024.

Opportunities for Additional Value Creation

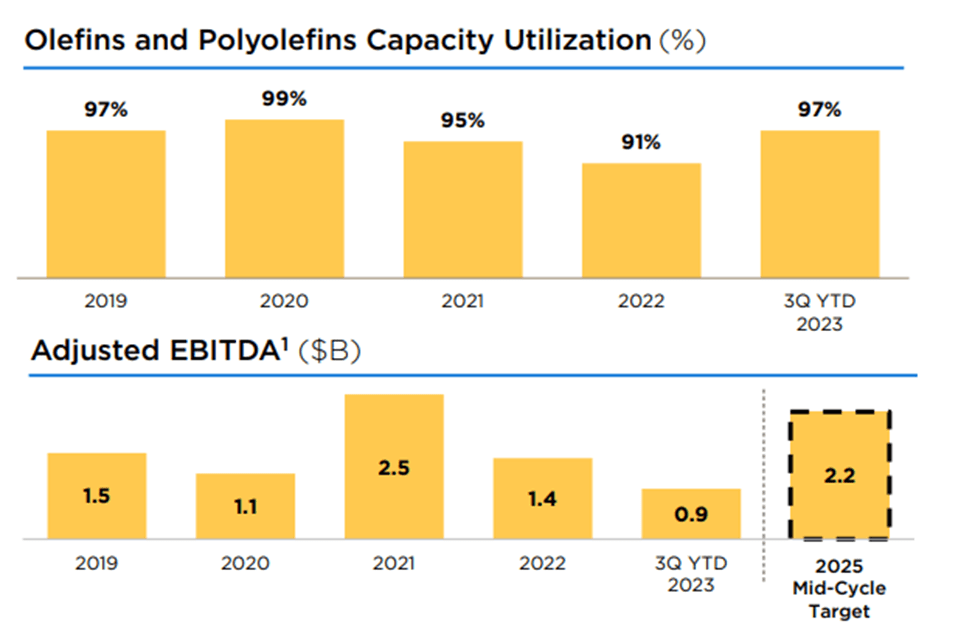

Beyond closing the gap in refining operating costs, Elliott Management also identified the opportunity to monetize non-core assets to boost the capital return program for PSX. Elliott has aligned with many Seeking Alpha readers in that PSX should sell is CPChem stake as it is a very large capital investment for PSX with very little profit to show for it. The annual net income creation from this segment is currently in the range of $600-$800 million annually .

Since sale of this group would only slightly detract from the entire enterprise's earning potential, this seems like an obvious source to harvest capital. Unfortunately, at this time, PSX's management seems content to play the long game with CPChem .

But CPChem is well positioned to endure those kinds of conditions. They have a strong competitive position. 95% of their feedstock is advantaged. And so they've been able to run flat out and create good bottom-of-the-cycle value, almost $1 billion of EBITDA back to us at the bottom of the cycle is a pretty good story. But we see fundamentals continue to improve. It's going to be a function, though, of what's going on in the global economy.

And so we continue to be bullish in the long term around CPChem, around their value chain, but the ultimate outcome is going to be driven by global economics.

It's fair to be skeptical on the prospects of CPChem. Management expects a mid-cycle target of $2.2 billion in EBITDA if the industry can achieve "mid-cycle" margins by that time. With two multi-billion dollar cracker plants under construction to commence operations in 2026, it calls into question the return of invested capital from these projects.

{kind=link}

I hate to be near sighted, but I fear it's a tall task for one management team to appropriately manage business in refinery, retail, midstream, and a JV chemicals unit. It's hard to be good at everything. Therefore, on this premise, I would be in favor of selling the CPChem unit for redeployment of capital.

Risks

The most obvious risk would be a decline in crack spreads leading to a rapid decline in refinery profitability. The oil and gas industry is notorious for being cyclical and investors do not want to be caught on the wrong side of the cycle. My analysis baked in an overall 20% reduction in refinery margins and reduced income growth to provide some conservatism. In this base case, PSX is still able to meet the minimum of $13 billion in returns it has promised to shareholders.

An additional risk would be a further delay with the Rodeo Renewed project. Since this is largely a regulation play, the overall direction of the project could be changed with the stroke of the pen. There is the potential for margin compression in this sector as multiple renewable projects are entering the market.

If both of these scenarios pan out simultaneously, I believe sufficient margin exists to deliver the base case of shareholder returns as cost savings in both the refinery and midstream segments can mitigate most of these losses.

Summary

In this article I analyzed the impact of PSX's cost reduction program as well as the cumulative impact of its shareholder return program. I reviewed how improvements in the refinery business could generate an 11.5% increase in share price using a FCF based evaluation.

I also presented a base case projection that allows PSX to reach its minimum threshold to return $13 billion to shareholders by the end of 2024 assuming a 20% compression in refinery margins. If refinery margins are maintained, the top end of the return guidance of $15 billion can be achieved.

I believe patient investors will be rewarded with a hefty 7% dividend raise in 2024 as well as significant share appreciation as the cumulative effects of cost reductions and share repurchases are realized. I continue to rate PSX as a buy under $135/share.

For further details see:

Phillips 66 Has A Lot More In Store For 2024