PSX - Phillips 66: Impressive Fundamentals Provide For Long-Term Value

2023-06-06 04:35:57 ET

Summary

- Phillips 66 has made a strong financial comeback since the pandemic, with impressive Q1 2023 earnings and a positive outlook from institutional investors.

- The company offers an attractive blend of value and income through dividends and share buybacks, with a current dividend yield of 4.16%.

- Despite potential risks from macroeconomic factors and regulatory pressures, Phillips 66's diversified portfolio and strong ESG ratings make it an appealing stock for investors.

Editor's note: Seeking Alpha is proud to welcome REC Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Phillips 66 (PSX) is a multi-national energy company with operations in oil & chemicals refining, marketing, and logistics. After a tough couple of years during the pandemic, the company's financial profile has made a roaring comeback, which is yet to be reflected in today's stock price. Based on the fundamentals and institutional positioning, I believe there is good value in the forward outlook. In the meantime, there is also notable income to be gained through dividends and share buybacks, creating an opportunity for your portfolio with an attractive blend of income and value.

Phillips 66 stock has underperformed the S&P 500 year-to-date, but one can see significant positive support from institutional players, both on the sell side and the buy side of the market.

On the sell side, a Bloomberg survey of research analysts at banks and brokers demonstrates the positive consensus around the stock, as 57% of analysts issued a "Buy" rating, whilst 43% issued a "Hold" rating. None of the surveyed analysts issued a "Sell" rating. In addition, the 12-month estimate target price of $120 represents a forecast return potential of 23% based on the current price level, illustrated below.

Analyst Recommendations (Bloomberg)

{kind=link}

On the buy side, we can analyze the historical holdings of the major shareholders to identify any buying or selling patterns. From the Top 10 investors, one can see a positive picture, as big players such as BlackRock (BLK), Wells Fargo (WFC), and Wellington Management have increased their stakes in Phillips 66 significantly in recent quarters. At the same time, investors that have reduced their number of shares have generally seen relatively small reductions, likely due to portfolio rebalancing.

Phillips 66 Institutional Holders (Bloomberg)

{kind=link}

From a Management Insiders' perspective, the stock outlook also appears well supported by management team purchases year-to-date as presented on Bloomberg Insiders page, with the majority of transactions being buy operations and increases in shareholdings. Management purchases are often viewed as a promising signal that the stock is currently undervalued and demonstrates a vote of confidence to the market that insiders have a positive take in their own company's current prospects and are willing to bet further skin in the game.

Phillips 66 Management Team Transactions (Bloomberg)

{kind=link}

So, what is warranting this positive perception on the institutional side? Let's dive into the fundamentals.

Financial Performance

Phillips 66 has released impressive financial results, most recently in their Q1 2023 figures, which boasted earnings per share of $4.20 , significantly higher than the consensus estimate of $3.56 expected by the market and presented on Bloomberg. Zooming out to the fiscal year 2022 and last twelve months ('LTM') results, we see encouraging trends in margin growth, both in EBITDA and net income, which is an impressive feat given that the earnings call indicated that recent quarters have seen significant refining maintenance . In 2022, revenues increased to $170 billion , as compared to $111 billion in 2021, whilst net income increased to $11 billion , as compared to $1.3 billion the prior year. With guidance in the recent earnings call that refining maintenance and capex should be lower in coming quarters, I expect further bottom line growth, which should translate into greater free cash flow and in turn an increasingly positive outlook for the stock.

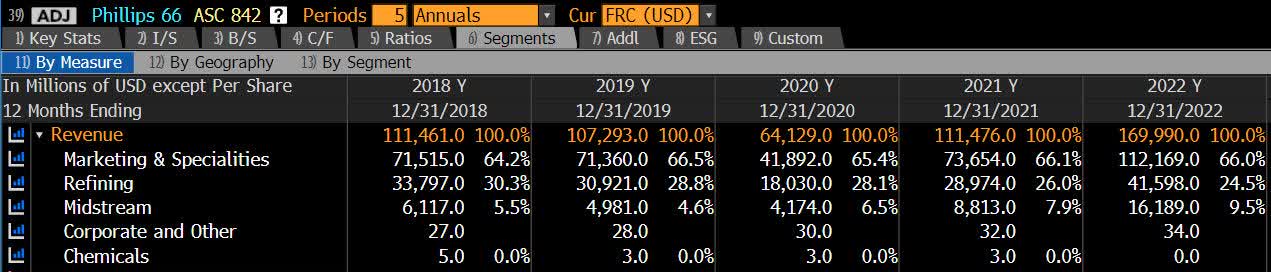

In addition, Phillips 66 is positioned well compared to direct peers due to its greater diversification when looking at both the product mix and geographic mix, according to the Bloomberg financials below. In FY '22, the Marketing & Specialties segment accounted for 66% of revenues, whilst Refining made up 24% and Midstream represented 10%. US operations accounted for 80% of revenues, whilst International operations made up 20%. This diversified portfolio of business should continue to act as a source of strength.

Phillips 66 Product Mix (Bloomberg) Phillips 66 Geographic Mix (Bloomberg)

{kind=link}

{kind=link}

Shareholder Remuneration

Due to the stronger financial position, management is making a significant effort to maximize shareholder returns, which should support and boost the stock in coming quarters. In Q4 2022, the company announced plans to perform share buybacks worth between $10-12 billion by the end of 2024 . These buyback programs have a positive impact on the outstanding shareholders as earnings per share increase. In addition, the stock has a long history of consistently paying dividends, even during the COVID downturn years. Since 2022, it has stepped up the dividend amount to $1.05 per share , representing a current dividend yield of 4.16% (Bloomberg), which compares favorably versus peers. Dividend yield is a key metric for income investors, as it represents the stock's annual dividend payments as a percentage of the stock's current price. The total return for investors is then the price performance plus the dividend yield, which in the case of Phillips 66 could make a large positive impact on your portfolio. Ultimately, the consistency and growth in shareholder remuneration make this a key income stock to hold.

Peer Analysis

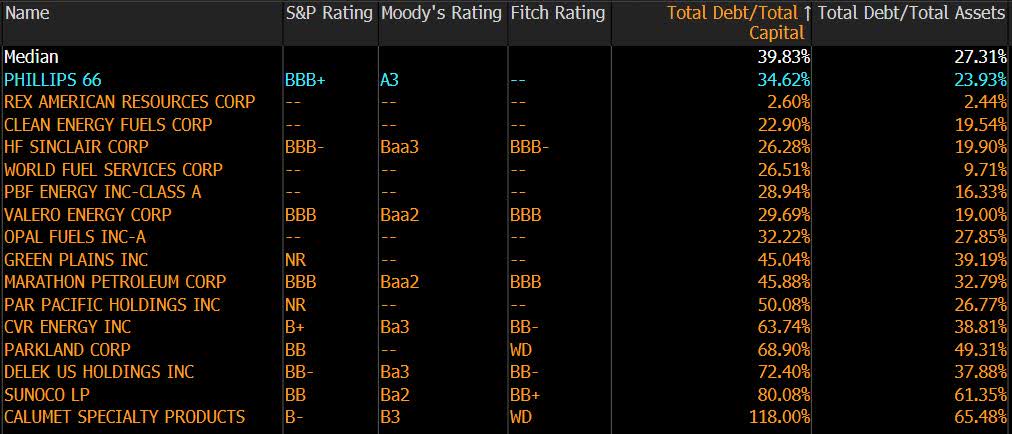

Looking across the direct global peers hand-picked by Bloomberg on the Relative Valuation screen, we can see Phillips 66 has an edge over its competitors across key verticals that are under growing scrutiny from investors, such as in credit and ESG. Credit-wise, Phillips 66 has a superior credit profile, as illustrated by the assigned credit ratings by the top three rating agencies. This is partly driven by their leverage ratios, which currently sit below median levels versus its peers. This is a notable achievement given the relative size of Phillips 66 in terms of total capital, assets, and market cap. As corporates continue to adjust to a higher interest rate environment, it will become increasingly critical to maintain manageable levels of debt and interest cost.

Peer Analysis - Debt (Bloomberg)

{kind=link}

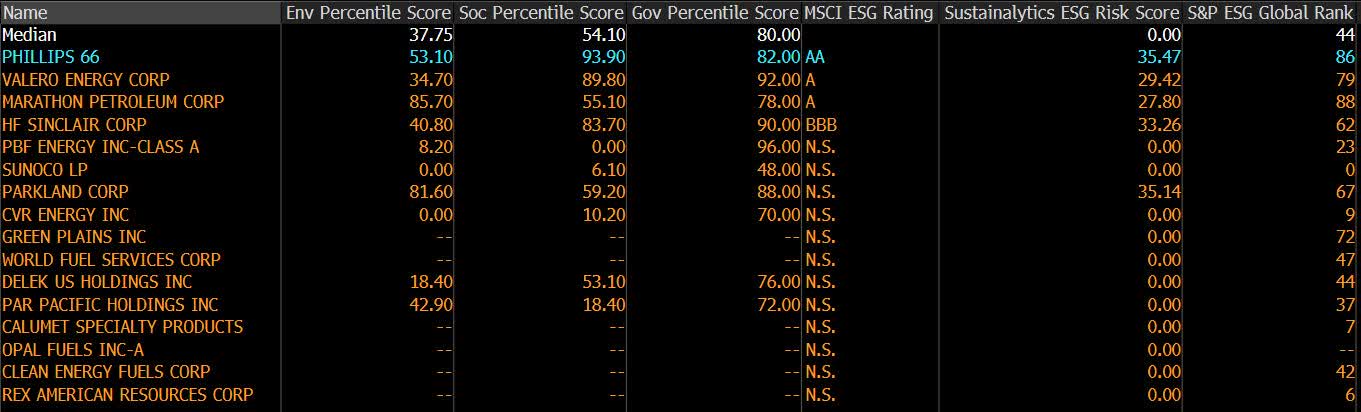

Environmental, social, and governance considerations continue to become a growing part of the investment criteria process, especially for institutional investors assessing sectors such as commodities refining & marketing. Across the board in assessments undertaken by Bloomberg, MSCI, Sustainalytics, and S&P, Phillips 66 has showcased top tier ratings relative to its peers. This places the stock in a strong position, as investor, governmental, and regulatory scrutiny intensifies in this age of decarbonization and sustainability.

Peer Analysis - ESG (Bloomberg)

{kind=link}

Relative Valuation

We can analyze Phillips 66's multiples versus its industry peers in order to build a view on the stock's fair value in terms of being undervalued or overvalued at current levels. One can see in the Bloomberg Relative Valuation page that both the current and forward-looking Price/Earnings Ratio of the stock is currently below the industry median, consolidating the view that an uplift to the stock is justified as indicated earlier in this text by the Bloomberg Analyst Survey. We can also see a similar undervalued picture when looking at the EV/EBITDA multiples.

Peer Analysis - Valuation (Bloomberg)

{kind=link}

Market Fundamentals

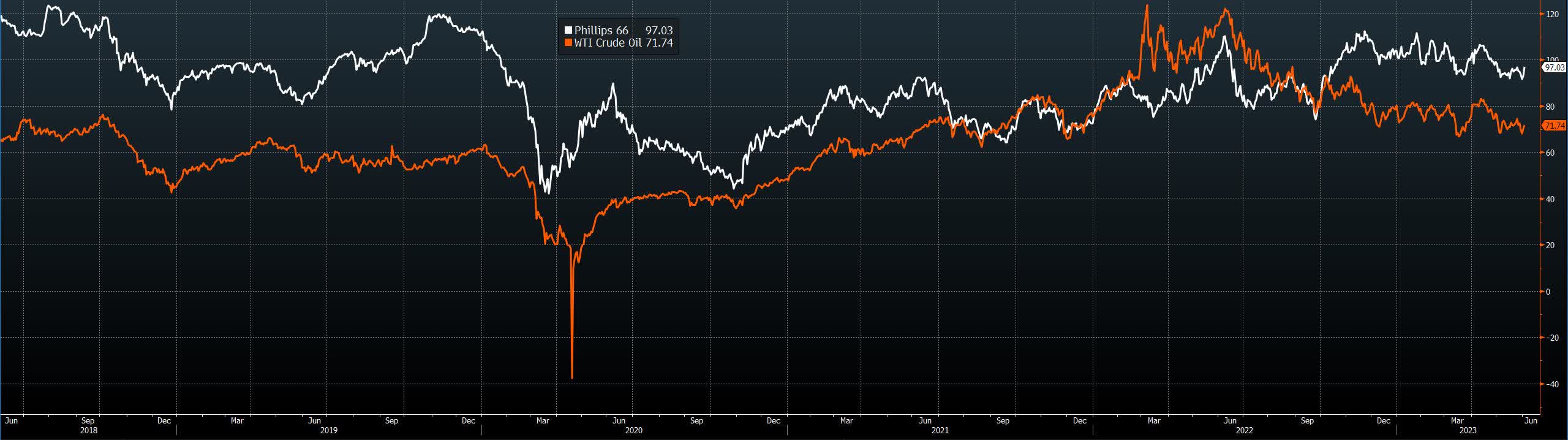

When analyzing the stock performance of Phillips 66 with that of WTI crude oil, we can see a strong correlation in recent years in the below historical chart. Oil has dropped in previous quarters to relatively low levels, currently trading around the $70 per barrel mark. However, banks and commodity brokers are forecasting a positive recovery and an uptick in crude prices in the next year, driven by a combination of low inventories, a resilient US economy, and growing demand from a resurgent China. This outlook is presented in the Commodity Price Forecasts page on Bloomberg, with the median consensus target price for WTI of $90 by the end of Q3 '24, which should further support the stock outlook for Phillips 66.

Phillips 66 & WTI Crude (Bloomberg) WTI Crude Price Forecasts (Bloomberg)

{kind=link}

{kind=link}

Risks

Whilst the company's management seem to be executing on all fronts, there are downside risks to the thesis to highlight, both on the macro front and company specific.

If the Federal Reserve and the US economy do end up facing a hard-landing and prolonged recessionary period, we would see a significant drop in US domestic GDP and demand for energy products, which would hit key products and markets for Phillips 66. Falling demand would depress energy prices, which would impact the stock.

On the company specific side, higher than expected refining maintenance, unplanned downtime, and larger than expected capex would impact the financial profitability and possibly derail shareholder remuneration exercises. Also to consider, increasing regulatory and governmental pressure on sustainability reform and decarbonization could also lead to headwinds for the company and likely cause a negative hit to the bottom line.

In conclusion

Phillips 66 is an exciting stock that has recovered strongly since the pandemic and is exhibiting attractive characteristics from both income and value perspectives. The company management's execution in shoring up and growing the financial profile and profitability of the firm is paying dividends (literally!) and creating significant passive income for shareholders. At the same time, the fundamentals of the company and the wider outlook for this segment of the energy sector are yet to be fully priced in the current stock price, as demonstrated by the institutional supports that Phillips 66 currently holds.

For further details see:

Phillips 66: Impressive Fundamentals Provide For Long-Term Value