PSX - Phillips 66: Maintain Buy Recommendation Following Solid Q2 Results

2023-08-08 01:36:45 ET

Summary

- Phillips 66 released solid Q2 results, beating market estimates in EPS, Revenues, and Net Income.

- The company increased their diversified mix of earnings across product segments, reducing reliance on volatile refining margins.

- PSX continues to offer attractive income benefits with consistent dividend growth and a higher dividend yield compared to peers.

Investment Thesis

Phillips 66 ( PSX ) released solid Q2 results last week, beating the market estimates in several financial metrics. Despite the stock's recent rally in the last couple of months, I believe PSX still demonstrates good value for a long-term play, whilst also satisfying income investors thanks to their favorable dividend yield relative to peers.

Company Summary & Performance

Phillips 66 is a multi-national energy company with operations in oil & chemicals refining, marketing, and logistics. The firm's main business segments are:-

- Marketing & Specialties - purchase and sale of refined petroleum products, as well as the manufacturing and marketing of specialty products such as base oils and lubricants.

- Refining - refines crude oil into petroleum products such as gasoline, distillates, and aviation fuel.

- Midstream - transportation, storage, and marketing of crude oil, refined products, and natural gas liquids.

PSX stock is up ~9% year-to-date, outperforming the S&P 500 Energy Index, as per the normalized chart below. The stock has underperformed the broader S&P 500 Index, but we can see the strong recovery rally from PSX in recent months, narrowing the performance spread between the two. As discussed further below, I believe this performance trend will continue as PSX financial fundamentals continue to show positive elements and investor positioning remains constructive, with the stock also looking undervalued compared to peers.

Phillips Benchmark Performance 2023 (Bloomberg)

{kind=link}

Solid Financials

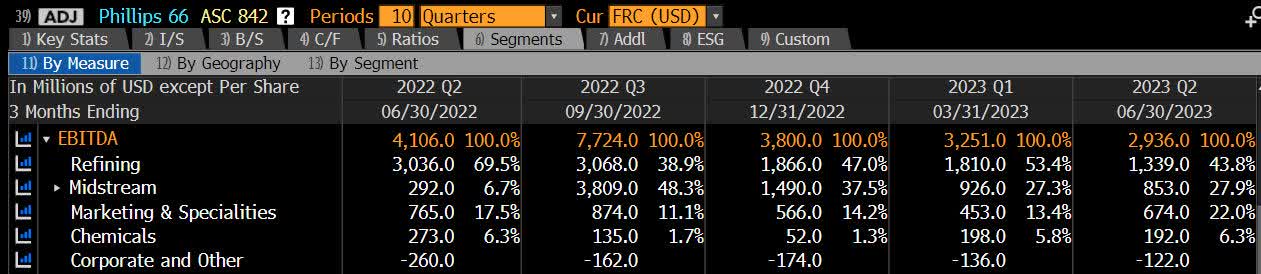

Before diving into the latest quarterly earnings, one positive to highlight is the EBITDA breakdown by product. In this year's results, we can observe a more balanced and diversified mix of earnings across product segments, as the historic reliance on the main Refining segment has reduced, which is the business line most exposed to volatile refining margins. This is a positive development that should bring a more stable and diversified earnings base for PSX leadership to better manage the company's financial profile and dividend programme.

EBITDA - Product Breakdown (Bloomberg)

{kind=link}

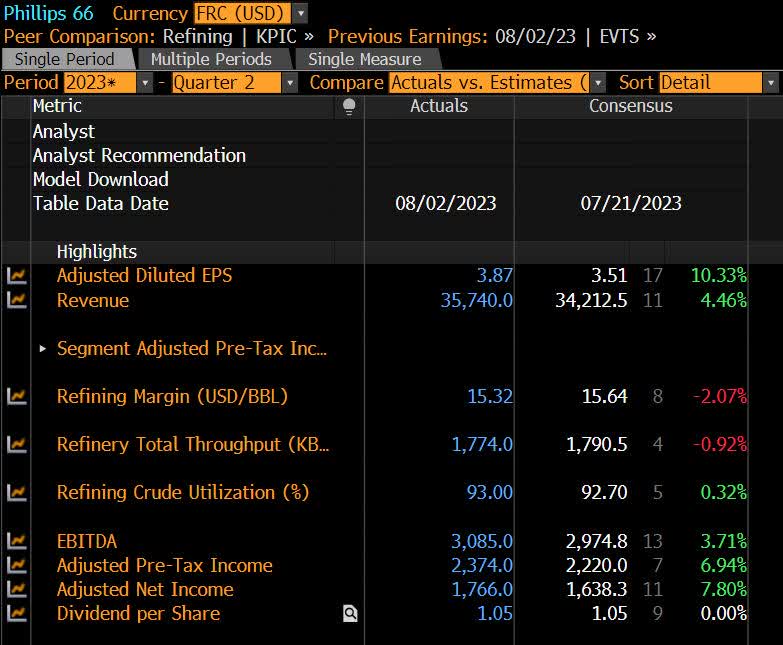

In terms of Q2 results released last week, PSX reported better than expected results. Quarterly adjusted EPS was $3.87, beating the Bloomberg consensus of $3.51 by over 10%, and Revenues were $35.74 billion, exceeding the consensus of $34.21 billion. Adjusted Net Income came in at $1.77 billion, comfortably above the $1.64 billion consensus figure.

Q2 Actuals vs. Estimates (Bloomberg)

{kind=link}

On a quarter-on-quarter basis, the results were slightly mixed. Revenues were marginally higher than Q1, whilst both Net Income and EPS dropped slightly. Looking ahead, Q3 estimates are forecasting a stable outlook in terms of Revenues and Net Income, as well as a significant pick up in Free Cash Flow. This gives me enough assurance that PSX is well positioned to maintain a positive outlook on their long term value story.

Quarterly Financials (Bloomberg)

{kind=link}

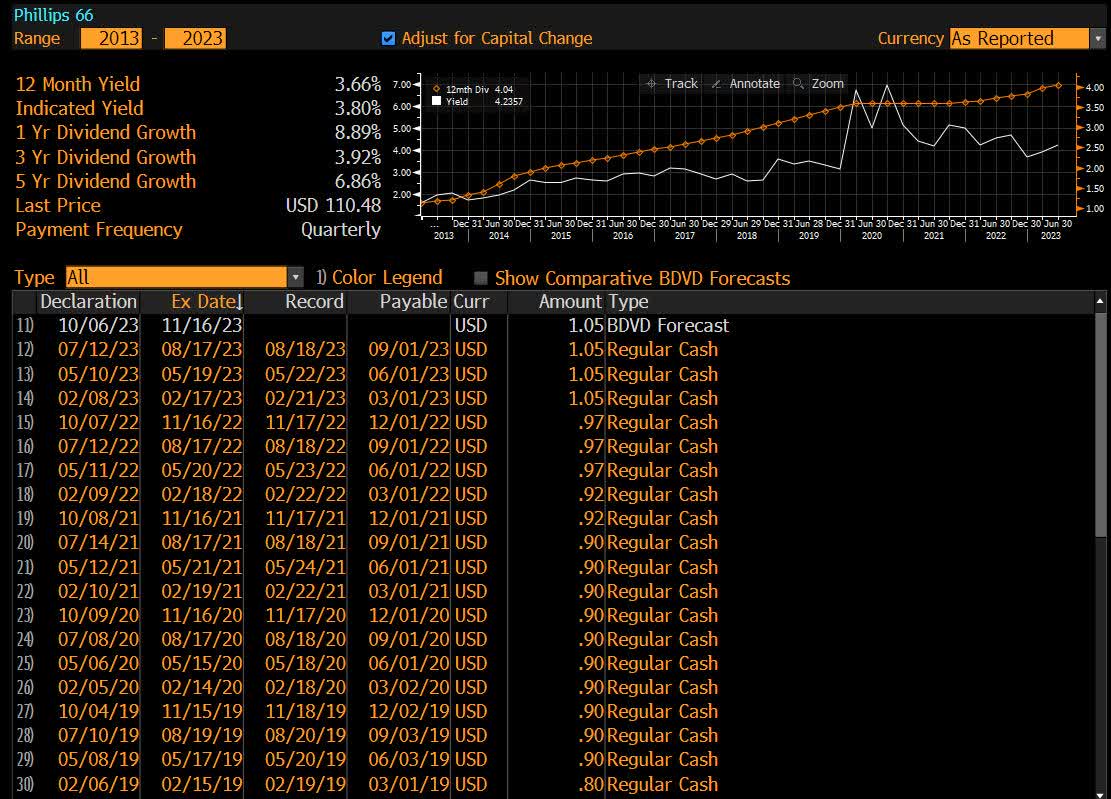

From a shareholder returns perspective, I believe PSX continues to demonstrate great income benefits. The management team have prioritized delivering shareholder returns from both share buybacks and a consistent dividend plan. The company boasts $5.4 billion in shareholder distributions since July 2022, and is on track to meet $10 - 12 billion by year-end 2024.Specifically on the dividend side, PSX is well-known for its consistent and growing dividend story. The stock has a 1 year dividend growth of nearly 9%, with the most recent quarterly dividend at $1.05 per share. The annualized dividend yield is respectable at 3.80% , higher than its peer group.

{kind=link}

Overall, I believe PSX represents one of those rare hybrid stories of demonstrating attractive performance from both income and value perspectives, and this trend is well-positioned to continue in coming periods thanks to the solid financial results.

Valuation & Analyst Forecasts

In terms of relative valuation, we can look at the Price-to-Book Ratio to compare PSX to their peers. Using the FY 2023 BPS estimate of 71.52 from Bloomberg, and the forward-looking sector median P/B Ratio of 1.70x from Seeking Alpha, we obtain a target price of ~$121, which implies a return potential of ~10%.

Price-to-Book Valuation (Bloomberg, Seeking Alpha)

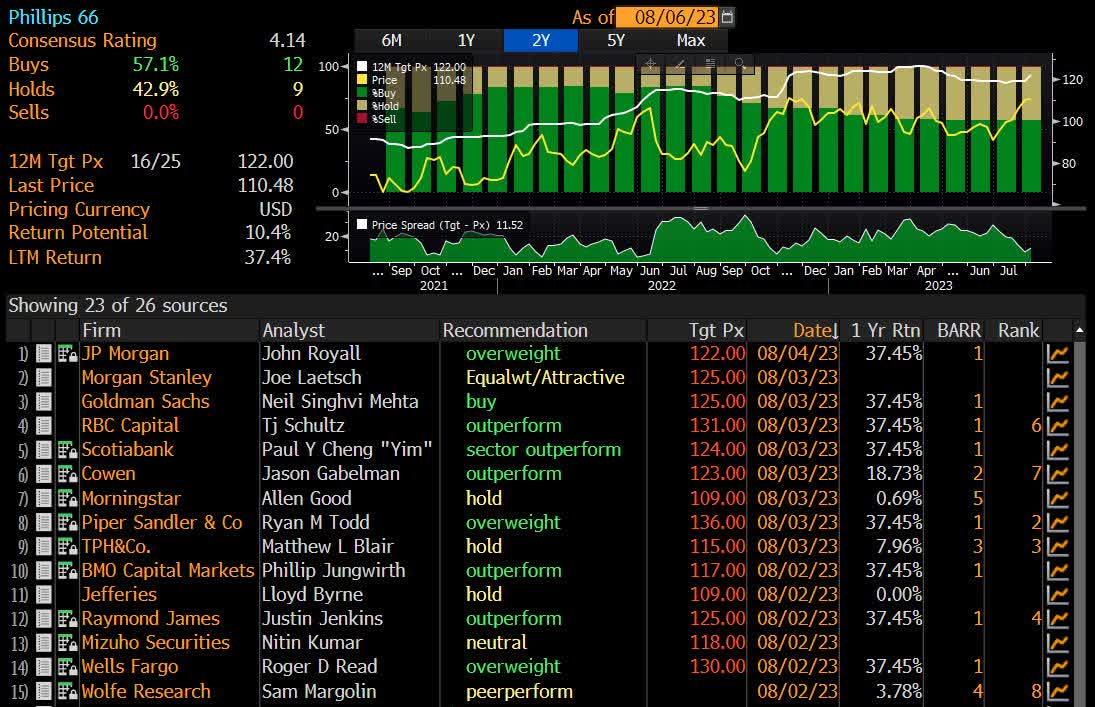

Looking at the Bloomberg Analyst Recommendations page for affirmation of our value outlook, we can see a positive picture. There are currently no analysts with a "SELL" recommendation on the stock, as 57% have issued a "BUY" rating, whilst 43% are recommending a "HOLD" rating. Based on the median consensus 12 month target price, it is also implying a return potential of ~10%, in-line with the P/B valuation above.

Bloomberg Analyst Recommendation (Bloomberg)

{kind=link}

Investor & Management Positioning

I always look to affirm my long-term outlook on the stock by looking at the buying and selling patterns of major shareholders and the management team. In the case of the Top 10 shareholders of the stock, we can see a positive picture, as large institutional shareholders such as BlackRock, Wellington, and Barclays have substantially increased their positions in PSX. This would not be the case if we were approaching overvalued levels in their eyes.

Top 10 Shareholders (Bloomberg)

{kind=link}

From a management insiders perspective, the stock is also well supported from net buying activity from the company executives. Since the start of the year, there have been ~133K shares purchased, with ~32K shares being solid. The net purchase position of ~101K shares by insiders gives me confidence that the management team still see good long term value in their stock based on current levels.

Management Transactions (Bloomberg)

{kind=link}

Bullish Options Sentiment

An additional technical factor from the options market that can signal whether traders see the current price as over or undervalued is the Put/Call Ratio, which compares the current open interest for put options versus call options. A value below 1 indicates that there is a greater amount of open interest in call options versus puts. If there were greater market concerns for a fall in the stock price, there were would be greater demand for put options, both for speculative reasons to take advantage of expected lower prices, as well as protective purposes in terms of hedges. The current value of 0.85 demonstrates that there is still strong positioning in the market to take advantage of upward moves in the stock through call options.

Put/Call Ratio Open Interest (Bloomberg)

{kind=link}

Risks

Looking at the wider macro picture, PSX is highly correlated to the price of WTI crude. So far this year, oil has had a decent year, currently trading back above the $80 mark per barrel. If we were to see a drawn out period of lower economic growth or even negative growth in the major economies such as the US, we could expect reduced energy demand and a hit to PSX's topline earnings. The company is also exposed to the crack spread, the pricing differential between crude oil and petroleum products refined from it, essentially representing a processing margin for companies such as PSX. A tightening spread would hit PSX's profitability in their Refining segment.

Despite this wider risk, the US economy in particular has shown resilience in its macroeconomic indicators despite the aggressive monetary tightening by the Federal Reserve. US quarter-on-quarter GDP growth for Q2 was 2.4%, a strong number and well above the median estimate of 1.8%, which gives me sufficient comfort that PSX should not be impacted significantly by the current state of their largest geographic revenue market.

In Conclusion

Following the Q2 results, I believe Phillips 66 continues to be a strong player in any portfolio, and I maintain a long-term value outlook on the stock. I think the solid financials and perceived valuation are well supported by the current positioning of top shareholders, as well as from the implied outlook of the options market. At the same time, PSX continues to demonstrate favorable income elements as well, with an attractive shareholder return outlook of buybacks and a stable dividend programme.

For further details see:

Phillips 66: Maintain Buy Recommendation Following Solid Q2 Results