CVX - Phillips 66: The Importance Of The Chemicals Segment

2023-05-02 11:26:27 ET

Summary

- Phillips 66's Chemicals Segment is frequently overlooked due to its bigger Refining & Midstream Segments. Today, I'll discuss why PSX's Chemicals Segment is so important for shareholders.

- PSX's Chemicals Segment primarily consists of a 50/50 joint-venture with Chevron called CPChem.

- Today, I'll take a look at PSX's Chemicals Segment's recent performance and what to expect from CPChem going forward.

- Phillips 66 is due to release Q1 earnings on Wednesday, May 3rd, so I'll also review consensus earnings estimates.

Years ago, Phillips 66 ( PSX ) unveiled a strategic plan to grow shareholder value by investing heavily in its higher-margin Midstream and Chemicals Segments in order to diversify away from and smooth out its cyclical Refining Segment results. The thought process was that PSX's mid-cycle margins would be higher than a pure-play refiner and therefore the market would reward the stock with a premium valuation. If that has happened, it hasn't been overly impressive. I say that because compared to its primary refining peers - Valero ( VLO ) and Marathon Petroleum ( MPC ) - the jury is still out (see below). Today, I'll discuss why PSX's Chemicals Segment is so important to shareholders and what to expect going forward. I'll also review current consensus Q1 EPS estimates prior to the release on Wednesday before the market opens.

| TTM P/E |

| Forward P/E |

| Yield |

| PSX |

| 4.23x |

| 6.81x |

| 4.24% |

| Valero ( VLO ) |

| 3.29x |

| 5.05x |

| 3.56% |

| Marathon Petroleum ( MPC ) |

| 4.38x |

| 5.78x |

| 2.46% |

As you can see in the chart above, PSX has a significantly higher yield than either VLO or MPC, and actually has a lower TTM P/E than does MPC. However, PSX's forward P/E is significantly higher than either VLO or MPC.

Chemical Earnings

First off, for those that are not aware, PSX's chemicals operations consist primarily of a 50/50 joint venture with Chevron ( CVX ) called "CPChem".

The chart below was taken from PSX's Q4 EPS report and summarizes the company's earnings by Segment over the past two years:

Phillips66

As you can see, while PSX's Refining Segment bounced back strongly last year from a dismal 2021, it was just the opposite for the Chemicals Segment. Indeed, pre-tax earnings from CPChem for FY2022 was only $856 million - down almost $1 billion yoy (-53.6%). That's a drop of an estimated $2.21/share based on the 466 million PSX shares outstanding at the end of the year, and obviously looms large relative to the company's $4.20/share annual dividend obligation.

The point is that CPChem's results have been volatile and, as most commodities are, affected not only by global economic growth but also by supply. Indeed, companies like CPChem (i.e., PSX and CVX) and Exxon Mobil ( XOM ) have been growing their chemicals capacities so fast, sometimes it seems as though they are already spending on the next big project before they have made any earnings on the last big project. Granted, U.S. chemical plants have strong feedstock advantages due to shale's producers' abundance of natural gas and NGLs production (i.e., low prices), but the extra added capacity on the global market of these massive petchem projects ends up lowering realized prices due to over-capacity.

So this is one big reason (the other being lower refining margin) that the returns of PSX have lagged its peers VLO and MPC over the past few years: Phillips 66 has invested in expensive world-class chemicals projects yet the returns on those investments have, arguably, not come to fruition as expected. Sure, it's a commodities business and it's all about mid-cycle margin over the long term, but still, at some point investors' should question these very large cap-ex expenditures on huge global petchem projects.

CPChem Going Forward

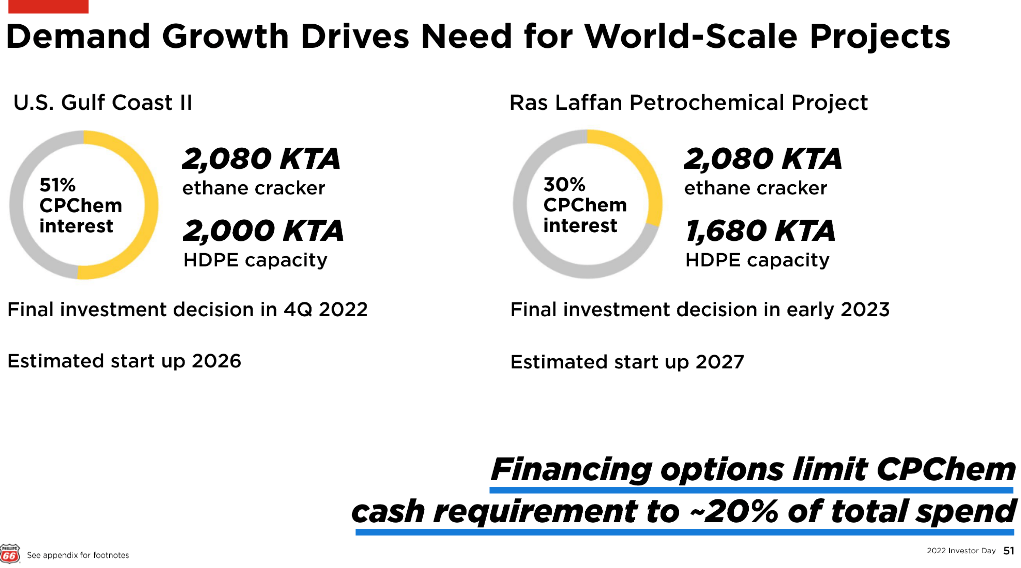

With that as background, note that in the Q4 EPS report referenced earlier, PSX announced that CPChem and Qatar Energy have reached FID to move forward on both of the major growth projects that Phillips 66 said it was considering during the Investor Day 2022 Presentation:

{kind=link}

The U.S. Gulf Coast II project is a $8.5 billion integrated polymers facility in which CPChem will own a 51% equity share in a joint venture with Qatar Energy owning 49%. The project includes a 4.6 billion pounds per year ethane cracker and two high-density polyethylene ("HDPE") units with a combined annual capacity of 4.4 billion pounds. Operations are expected to begin in 2026.

The Ras Laffan PetChem Project is a $6.0 billion integrated polymers complex located in Ras Laffan, Qatar. The JV will be majority owned by Qatar Energy (70%) with CPChem holding a 30% stake. The Ras Laffan Petrochemical Project is almost a copy-cat version of the U.S. Gulf Coast Project with the exception that its annual HDPE capacity is "only" 3.7 billion pounds. Ras Laffan PetChem is expected to start up in late 2026.

Global Newswire

As can be seen in the graphic above as reported by GlobalNewswire .com, the global HDPE market is expected to grow to 78 million tons by 2028, but will be closer to ~65 million tons in 2026 when these two new HPDE projects, with a combined capacity of 3.68 million tons come online (or an estimated 5.7% of total global demand).

Doing the math on PSX's share of cap-ex on these two projects, in aggregate, comes to an estimated $3.07 billion. At the same time, note that these two large-scale petchem plants will produce a combined HDPE capacity of a whopping 8.1 billion pounds. That's got to impact the global market, and thus the margin that CPChem will realize - at least in the short term, and maybe even the mid term. Which begs the obvious question: why construct both at the same time such their combined production will hit the global market at the same time? I mean as a long-term investor, I'm all about mid-cycle margin, but am I the only one to make the observation that these overlapped project schedules seem to practically insure lower short-term chemicals margin?

I should note that CPChem is also currently constructing a second world-scale unit to produce 1-hexene in Old Ocean, Texas and expansion of propylene splitter capacity at its Cedar Bayou facility. Both of these projects are expected to go online in the back half of this year.

Q1 Earnings Estimates

The current Q1 and FY23 consensus earnings estimate trends for PSX are shown below, courtesy of Yahoo Finance :

Yahoo Finance

As you can see from the chart, estimates for Q1 have risen by 11 cents/share over the past 90 days to $3.56/share. Note also that PSX is expected to deliver Q2 earnings of $4.32/share. If that comes to fruition, PSX would cover its entire current $4.20 dividend obligation in Q2 alone. The fact that PSX is expected to earn $15.16/share this year bodes very well for another substantial dividend increase going forward after an 8% boost in February .

Back to chemicals for a second. Note that Chevron typically does not break out its Downstream Earnings into Refining/Chemicals results. However, Chevron released its Q1 report last week and total downstream after-tax earnings - boosted primarily by strong refining profits - were $1.8 billion, up slightly from Q4 but up 5x+ from the $331 million in Q1 of last year. This information came from Chevron's Supplemental Q1 document, available here .

Meantime, Exxon Mobil also reported Q1 results last week that showed strengthening Chemical Segment results in Q1 on a sequential basis:

ExxonMobil

However, as can be seen, XOM's chemical products results were down significantly on a yoy basis. Exxon said the results were driven by "improved margins from strengthening of the North American ethane feed advantage partly offset by higher scheduled maintenance".

The point here is that the read-across from Chevron's and Exxon's earnings reports last week bode well for a relatively strong report from PSX.

Risks

Longer term, it remains to be seen if Phillips 66's large cap-ex spend on expanding its Chemicals Segment will eventually deliver the strong mid-cycle margin it was supposed to. So far, I am not impressed. One thing that would help is if PSX would finish one world-class Chemicals expansion project, and start seeing some good returns on it, before spending more cap-ex building on yet another big expansion project. I certainly see no reason whatsoever to build two world-class petchem projects at the same time . That "strategy" seems to be baking in terrible short-term margin after start-up due to over-capacity.

Plastics are becoming an increasing environmental and human body pollutant . This is causing pressure on governments to take action , various groups to press for filtered water versus bottled water, and several states - including California, Maine, New Jersey, New York, Oregon, Rhode Island, Vermont, and Washington - to ban single use straws .

Summary & Conclusion

All things considered equal, but acknowledging that they never are, shareholders in PSX can expect a relatively strong Q1 report Wednesday morning. Both Chevron and Exxon beat consensus estimates, and that bodes well for PSX. I say that because even though PSX obviously does not have the upstream operations that XOM and Chevron have, their downstream refining and chemicals operations delivered strong results. So should PSX.

Meantime, PSX's Frac-4 went online in Q4 of last year, the price of natural gas - a primary feedstock for PSX's refining and chemicals operations - has been declining, and PSX has a larger share of DCP Midstream earnings this quarter over the year ago quarter. Point being: yoy comparisons should be easy for PSX this quarter and this year. However, I doubt PSX's Refining Segment will replicate last year's super-strong results.

PSX still appears to be quite a bargain here. With a strong and safe yield of 4.24%, low valuation level, and with the outlook for another strong year of earnings combined with the new CEO's desire to Boost Shareholder Returns, shareholders should expect a strong dividend increase - perhaps as high as double-digits. As a result: I reiterate my BUY rating going into the Q1 report Wednesday morning.

I'll end with a 5-year total returns chart of PSX versus its primary refining peers as well as integrated majors Exxon, Chevron, and the Energy SPDR ETF (XLE) for additional perspective:

Note that PSX is the worst performer - by far. In my opinion, one reason is because of the large cap-ex spend on massive global petchem projects and the relative lack of decent returns on that investment.

For further details see:

Phillips 66: The Importance Of The Chemicals Segment