PSX - Phillips 66: The Shareholder-Friendly Cash Cow

2023-04-10 09:39:55 ET

Summary

- Phillips 66 is America's third-largest refining company, differentiating itself with a large footprint in chemicals.

- While the company's total return has lagged behind its peers, the company is a great source of relatively high and sustainable dividend income.

- The company is in a great spot to generate elevated free cash flow on a prolonged basis, and management is eager to distribute most of it to shareholders.

Introduction

Historically speaking, the best sources of wealth on the stock market are consistent dividend-growth stocks. More often than not, these come with subdued volatility and long-term outperforming total returns.

When picking volatile stocks in cyclical industries, investors need to get something in return. In the case of Houston-based Phillips 66 ( PSX ), investors are buying a source of relatively high energy income. This refining stock has a yield of more than 4.0% and a management team eager to maintain solid long-term dividend growth on top of high buybacks.

While PSX shares have lagged behind their competition, there is a compelling reason to put money into PSX, especially if recession fears provide a better valuation and juicier yield.

Now, let me walk you through my thoughts!

PSX Is A High Yield Cash Cow

With a market cap of $48 billion, Phillips 66 is the third-largest pure-play refinery company in the United States. In this case, I'm excluding Exxon Mobil ( XOM ) and Chevron ( CVX ), who have significant refining assets as well. However, these companies operate in the integrated oil and gas industry due to their upstream operations. Phillips 66 does not produce oil.

Founded in 2011 through a spin-off from CoconoPhillips, Phillips 66 is a combination of midstream and downstream operations.

In 2022, the company generated 81% of its revenue in the United States, followed by the United Kingdom with 10% of total sales. Sales were generated in the following segments:

- Marketing & specialties (66% of total sales).

- Refining (25%)

- Midstream (9%)

Essentially, the company produces gasoline, diesel, jet fuel, and other chemicals and sells these under various brand names to both wholesale and retail customers.

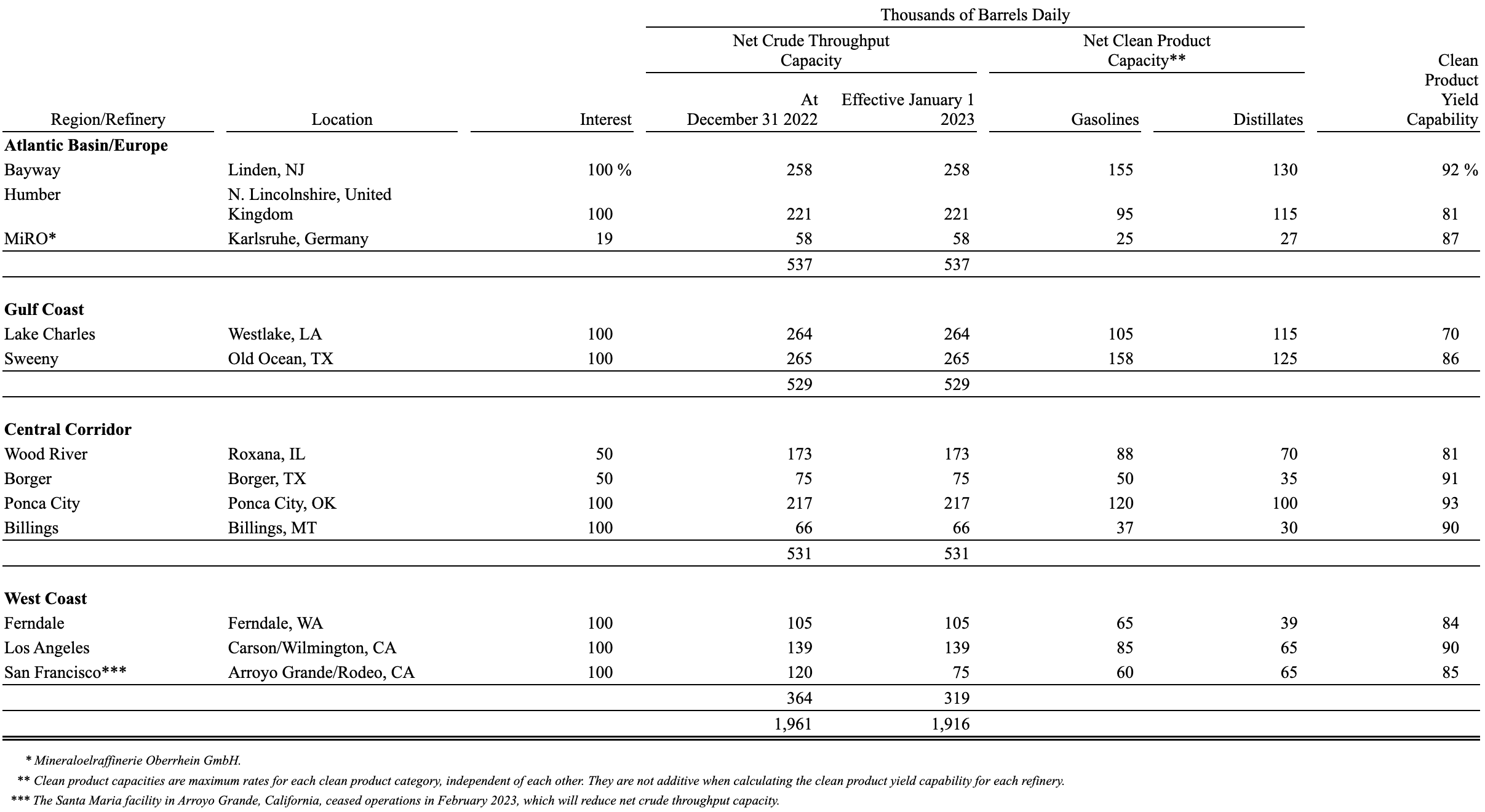

Phillips 66 operates 12 refineries in the United States and Europe. These assets have a net crude throughput capacity of 1.9 million barrels per day. In 4Q22, the company had a utilization rate of 91%.

{kind=link}

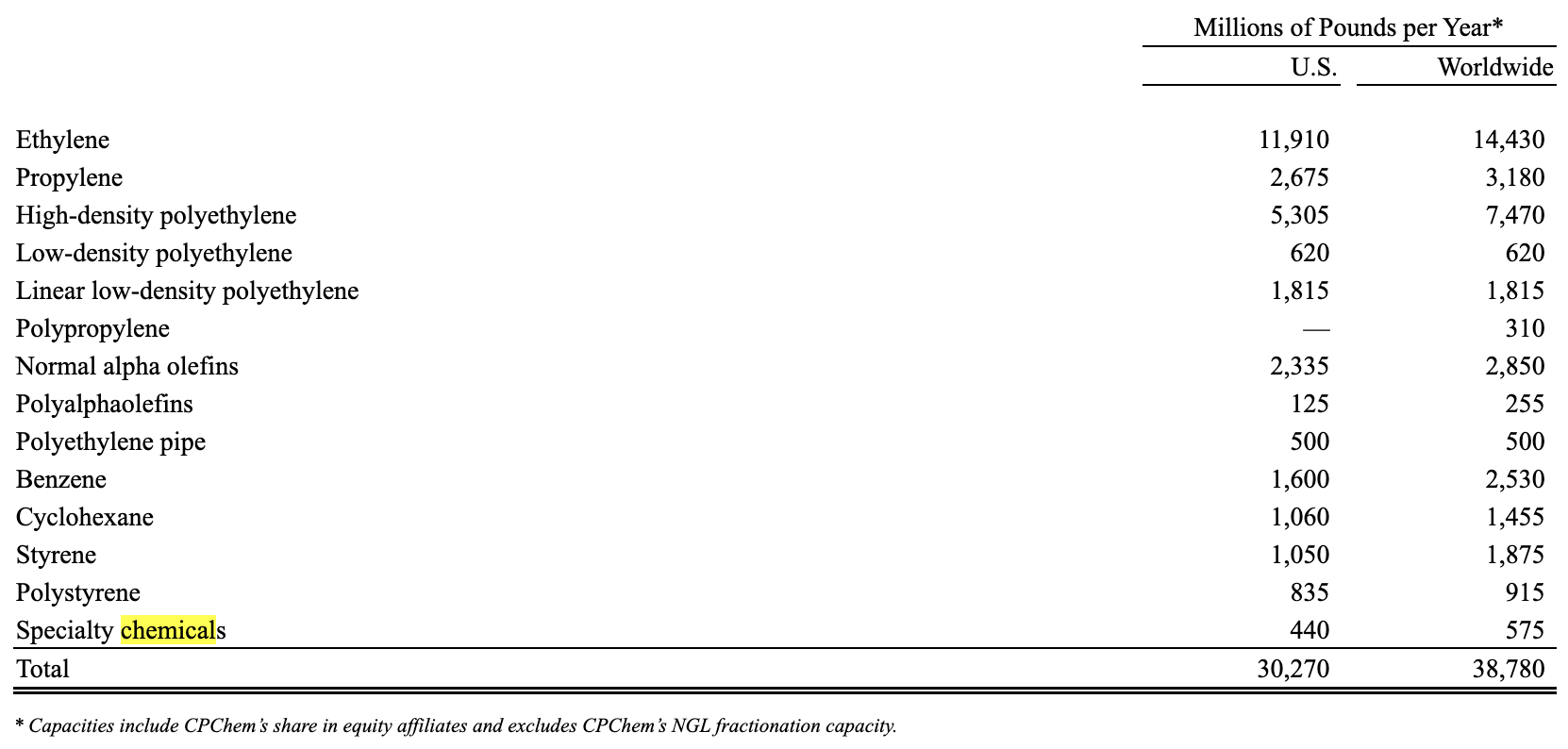

What sets Phillips 66 apart from its peers is its huge chemical footprint. The company has a 50-50 joint venture with Chevron called the Chevron Phillips Chemical Company LLC (CPChem).

This Texas-based corporation is engaged in the production and marketing of ethylene and other olefin products used in industrial processes.

Ethylene, which is primarily produced by cracking hydrocarbon-based raw materials such as ethane, propane, butane, naphtha, and gas oil, is used to manufacture plastics such as polyethylene and polyvinyl chloride. After having spent some time in the chemical industry (I'm not an expert, but an observer), I noticed a rapid increase in demand for advanced and high-quality chemicals like ethylene.

CPChem also manufactures and markets aromatics, styrenics, and specialty chemical products, including benzene, cyclohexane, styrene, polystyrene, organosulfur chemicals, solvents, catalysts, and chemicals used in drilling and mining.

In the US alone, the company sold more than 30,000 million pounds of chemicals last year.

{kind=link}

In the second half of this year, the company is expected to bring two major projects online. According to the company :

In Chemicals, CPChem is pursuing a portfolio of high-return projects, enhancing its asset base as well as optimizing its existing operations. This includes construction of a second world scale unit to produce one hexene in Old Ocean, Texas, and the expansion of propylene splitting capacity at its Cedar buying facility. Both projects are expected to start up in the second half of 2023.

With that said, the stock has failed to keep up with its peers Marathon Petroleum ( MPC ) and Valero Energy ( VLO ), which I own.

While the company has beaten the Energy Select Sector ETF ( XLE ) over the past ten years, it has underperformed the aforementioned peers by a rather wide margin - both on a price and total return basis.

While its peers have performed better, PSX has a juicier yield.

The company currently pays $1.05 per share per quarter, which translates to a 4.1% yield. This rather high yield is backed by a 21% payout ratio and a balance sheet with a BBB+ rating.

While the company has kept its dividend stable during the pandemic, it has never cut its dividend in its relatively short history as a standalone company.

These are the latest hikes:

- February 2023: 8.2%

- March 2022: 5.4%

- October 2021: 2.2%

During the pandemic, the company faced a massive headwind, worse than anything we've seen during the Great Financial Crisis. After all, lockdowns caused an implosion in traffic and industrial chemical demand.

Back then, the company didn't have enough operating cash flow to pay for capital expenditures ("CapEx"), let alone distribute a dividend. Yet thanks to its balance sheet, the company was able to use new debt to support the dividend and investments in both maintenance and growth projects.

However, it resulted in an increase in net financial debt.

Since 2021, however, the industry has experienced huge tailwinds. Because of refinery shutdowns during the pandemic, rebounding demand caused a steep increase in margins, allowing PSX (and its peers) to quickly reduce debt.

In the past four quarters, PSX generated more than $8.6 billion in free cash flow.

This year, that number is expected to be $6.6 billion. This translates to 14.0% of its market cap. Moreover, net debt is expected to fall to $11.6 billion this year, which translates to a net leverage ratio of just 1.0x EBITDA.

Until 2025, free cash flow is expected to decline to $4.9 billion. This is not bearish but a margin normalization trend. New supply is coming online, reducing the massive tailwinds refiners enjoyed in 2021 and 2022. While I believe that the company will beat these estimates, $4.9 billion in 2025E free cash flow still implies a 10.3% free cash flow yield. That's very juicy.

When combining these numbers with the company's healthy balance sheet, we can conclude that shareholders are in a very good place, as PSX can and will distribute most of it through dividends and buybacks.

During the 51st Annual Scotia Howard Weil Energy Conference in March, the company explained how it wants to distribute cash.

So the number one of those 6 priorities is to deliver cash returns to shareholders now in the form of dividends and share repurchases.

The company has committed to returning $10 to $12 billion of cash to shareholders from July 2022 to the end of 2024, with approximately $5 billion of that coming in the form of dividends. The remaining balance will be utilized for share repurchases, totaling $5 to $7 billion. This translates to a buyback program of at least 10% of its shares until December 2024.

Phillips 66 is cautious about increasing dividends too quickly, but they expect the incremental cash from share repurchases to be consistent, resulting in potential dividend per share increases over time while maintaining a consistent share repurchase pace of about $2 billion per year.

Please note that caution is very important. Companies that do not engage in special dividends need to be very careful when it comes to hiking into strength. While the current situation is great for dividend hikes, the company needs to be prepared for future (cyclical) economic weakness. It would be terrible if the company were to hike its dividend so much that even a mild recession in the future would trigger the need to cut its dividend.

So, what about the valuation?

Valuation

Refinery stocks are volatile and highly cyclical. PSX shares are currently 9% below their 52-week high and 39% above their 52-week low. Shares are down 1.1% year-to-date.

FINVIZ

PSX is currently trading at 5.6x 2023E EBITDA, based on its $64.5 billion enterprise value, consisting of its $47.4 billion market cap, $11.6 billion in expected net debt, $4.6 billion in minority interest, and $940 million in pension liabilities.

As I wrote in January , PSX deserves to trade at 7.5x NTM EBITDA, implying a fair value of roughly $150. That's 47% above the current price.

The current consensus price target is $126, which means I'm way above that.

On March 9, UBS initiated PSX coverage with a buy rating ($139 target).

Please note that I do not expect the stock to start an uptrend immediately. The economic environment is truly horrible, and I would not even rule out a move lower to the $70 to $80 range.

However, as someone with more than 20% energy exposure, I'm not worried about that. I have increased my savings rate to buy high-quality stocks if they move lower.

The only reason why I do not own PSX is that I own its peer VLO. I also own both Exxon Mobil and Chevron, which come with high refining exposure. Also, as we briefly discussed, Chevron owns the other half of Phillips 66's chemical joint venture.

Takeaway

Phillips 66 is a fascinating company. While it did not generate high total returns in the past few years, it has become a cash cow. The company is expected to generate high free cash flow in the years ahead and distribute almost all of it to shareholders using both dividend hikes and aggressive buybacks. Its healthy balance sheet allows the company to do this.

The current dividend yield is 4.1%, backed by a low payout ratio and the aforementioned free cash flow and balance sheet tailwinds.

Ignoring potential recession risks, the company is in a good place to benefit from rising global chemical demand and its ability to boost its output. It also still benefits from a tight refining supply.

While I believe that the stock is 50% below its fair value, I do not rule out another move lower in light of economic challenges and the odds of investors de-risking their portfolios.

Investors looking for energy income might benefit from monitoring PSX closely for potential correction opportunities down the road.

For further details see:

Phillips 66: The Shareholder-Friendly Cash Cow