SMP - PHINIA: Highly Catalyzed Spin-Off At 3.5x EBITDA - 100%+ Upside

2023-07-31 15:48:23 ET

Summary

- PHINIA, a manufacturer of fuel systems and aftermarket parts, is trading at a low valuation of 3.5x EV/EBITDA and a 20%+ free cash flow yield.

- Closing half the valuation gap between PHIN and their peers would drive a material uplift in the stock.

- Four major catalysts are expected to drive a rerating of PHIN's stock and generate 100%+ upside in the near-term.

- The company's Fuel Systems division has pricing power and a mission-critical role in vehicle production, while the Aftermarket segment is economically resilient.

Investment Thesis

PHINIA ( PHIN ) was spun off from BorgWarner ( BWA ) in early July as part of BWA’s push to move away from their legacy ICE business and towards a more electric vehicle focused future. Mainstream narratives around the imminent dominance of EVs combined with classic spin-off dynamics have left PHIN, a manufacturer of fuel systems and aftermarket parts, trading at an unjustifiably low valuation of 3.5x EV/EBITDA and a 20%+ free cash flow yield.

Over the next 12-18 months, there are four major catalysts that should drive a meaningful rerating of PHIN’s stock to close at least half the valuation gap with PHIN’s peers, driving 100%+ upside in the near-term.

Company Background

At its core, PHIN is a manufacturer of automobile and truck fuel systems which work to increase engine efficiency by controlling the amount of gasoline/diesel going from the fuel tank to combustion chamber. Whether it be through gasoline injection systems or fuel delivery modules, PHINIA’s products are focused on increasing the operational efficiency of vehicles.

While PHIN’s products have similar end-uses across their two business segments, Fuel Systems and Aftermarkets, the dynamics at play within the two divisions are unique and worth delving into to really understand the business and realize why mainstream narratives around electrification aren’t all they’re cracked up to be.

Fuel Systems – Mission Critical, Yet Low Cost

I think the best manufacturing businesses in the world are those whose offerings are a small part of the overall build cost yet occupy a mission-critical role in completing a project. In this regard, PHIN’s Fuel Systems division, which accounted for 65% of segment EBITDA ($377 million) is a standout performer, as despite improving arguably the most important metric for consumers when they buy an automobile (fuel efficiency), fuel systems cost a miniscule amount of the eventual sale price of a vehicle. To put some quick numbers on that, the average new car in the United States sold for $49,500 , as of early 2023, while fuel injectors, one of PHIN’s flagship products, cost between $400 - $1,000 . Or, put another way, between 0.8% and 2.0% of the eventual sale price.

I think this dynamic is tremendously important, as it means PHIN has a remarkable degree of pricing power, particularly on the wholesale side to automakers, as even a 10-20% price hike would translate to only a 0.2 – 0.4% increase in the overall cost of a vehicle. And while it is true that PHIN doesn’t operate a fuel systems monopoly, their products perform well, and it’s a pain for automakers to shift supply chains and find new suppliers who they can trust. EBITDA margins of 15%+ are reflective of Fuel Systems’ superior model. Long-term, even as ICE vehicle sales decline by a low single-digit percent every year, most of the decline should be made up for by incremental price increases through 2030.

Incremental market share gains in the commercial vehicle (CV) space will also stave off decline, as major hurdles remain before CVs can be viable in electric form, since battery constraints currently prevent the kind of range demanded by heavy-duty applications. This reality is largely behind the <1% EV penetration in the CV space. By 2030, PHINIA aims to have CVs make up >35% of revenue, versus 24% today.

Aftermarket

In addition to OEM customers, PHINIA also caters to retailers and body shops through their Aftermarket segment. With more 4,800 new SKUs launched annually, PHIN has cultivated its image as a supplier of virtually everything related to engine efficiency.

In contrast to Fuel Systems, whose earnings are tied to new ICE vehicle production and thus more cyclical, Aftermarket is far more economically resilient, as virtually all their SKUs are related to parts of a vehicle that must be replaced when they break (it’s hard to get your car moving with a broken starter). As a result, Aftermarket has historically grown more consistently and maintains healthy 16% EBITDA margins ($207 million of ’22 EBITDA) with low single-digit top-line growth.

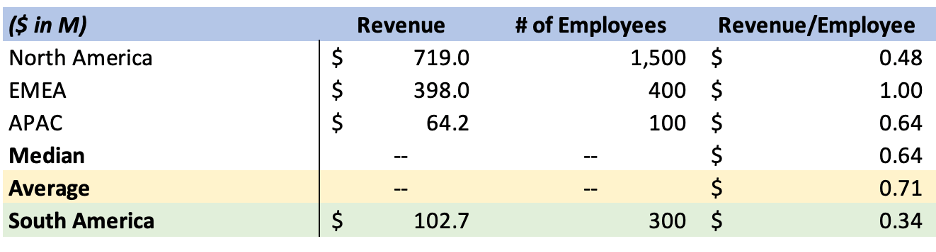

The South America Opportunity

On a go-forward basis, I believe there is a meaningful opportunity for Aftermarket in South America and particularly in Brazil, as car ownership rates are reaching increasing parity with the United States and Europe. PHINIA has recognized this opportunity and built up a presence in Brazil that positions them for growth, with multiple sales locations and manufacturing hubs. Another position of mine, AutoZone ( AZO ), and a major distributor of Aftermarket’s products, is likewise building out a presence in the region.

{kind=link}

Revenue/Employee Across Geographies (PHINIA Investor Deck)

Based on revenue/employee numbers, I believe there is an incremental $110 million revenue opportunity (~$15 million of EBITDA) over the medium term as revenue and EBITDA per employee reach levels more in-line with the rest of Aftermarket.

Shared Tailwinds

On a go-forward basis, both Fuel Systems and Aftermarket should be able to grow in the low single-digits, aided by three factors:

- Pricing: From a pricing standpoint, PHIN has historically been able to pass along cost increases without much pushback. In 2023, per their guidance, PHIN is planning to continue this with ~3% price hikes across the board. Assuming ~1.5% annual growth going forward is conservative in my view.

- Rising Vehicle Age: From 2023 to 2030, the average vehicle age across the world is expected to increase from 11 to 12 years. While that may sound small, it represents a 9.1% increase, or 1.25% compounded annual growth rate (CAGR). Despite problems tending to compound exponentially in vehicles as they get older, I’ll assume this only translates to 1.0% annual revenue growth.

- Global Fleet Growth: As Asia and Latin America become increasingly able to purchase more cars, the number of vehicles in the world is accordingly projected to increase, from 1.56 billion today, to 1.72 billion in 2030 – a 1.4% CAGR. Given PHIN’s exposure to Latin America, I’ll assume a 0.7% annual revenue tailwind.

Putting all this together, in my Base Case, I estimate annual revenue growth through the end of 2030 of around 3% per annum, which is roughly in-line with management’s guide of ~2% annual revenue growth through 2025.

Valuation – A Lot Can Go Wrong

As always, I prefer looking at companies through three valuation lenses: fair value today and then fair value ~3 years out in a bear and bull case. However, thanks to some interesting dynamics at play I believe PHIN, is uniquely positioned to outperform in a huge way over the next 12 – 18 months.

Short-term

Per PHIN’s 2023 guidance, they aim to earn $560 million of EBITDA, after adjusting for one-time expenses. Subtracting $150M for capex, $60M of interest expense (interest rates on their debt haven’t been finalized, so I penciled in 7%), and a 27% tax rate leaves us with $256 million of normalized 2023 free cash flow, versus a market cap of $1.25 billion. That’s a 20%+ FCF yield on a minimally leveraged industrial business (debt/EBITDA ~1.1x) with stable earnings !

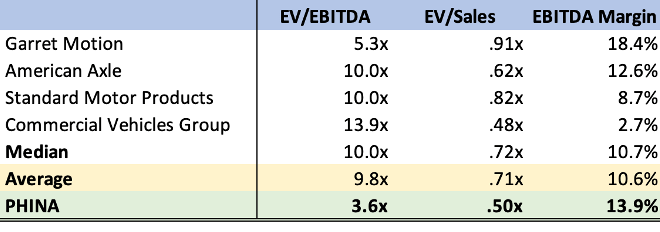

For context, peers Garrett Motion ( GTX ), American Axle ( AXL ), Standard Motor Products ( SMP ), and Commercial Vehicle Group ( CVGI ) all trade at EV/EBITDA multiples of between 5.0x and 14.0x, compared to PHIN at 3.6x.

To illustrate how little must change sentiment-wise for PHIN to move materially higher, for every turn EBITDA increases, the equity is worth 40% more , while for every 0.1x the EV/sales multiple increases, the equity is worth 30% more. As I write, PHIN trades at a 6.2x multiple discount to peers. Closing just half the gap implies 124% upside for the equity.

{kind=link}

Peer Multiple Comparison (Stock Analysis)

Now, trading at an enormous discount to peers despite superior operational results is all well and good, however, undervaluation in and of itself rarely causes a stock to move materially higher, especially in companies perceived as being in “terminal decline” … that’s where catalysts come into play. I’ve identified four catalysts which I think should collectively drive a material uplift in PHIN’s stock price over the next 12 -18 months.

Catalyst #1: H2 2023 / H1 2024 – Dividend Initiation & Buybacks

In their 2023 investor deck, PHIN committed to deploying 20-25% of free cash to a dividend, or around $50 million. On the current share count of 40 million shares, that’s $1.25 per share, or a 4.6% yield. Most industrial companies with low payout ratios trade at dividend yields of around 2%. I view it as highly likely that dividend investors will bid down the yield, to a more normal 2 – 2.5% yield once it’s initiated.

Now, the dividend is only <25% of free cash flow, which leaves ~$200 million still to be deployed every year on either M&A or buybacks. PHIN’s management has stated that they view accretive M&A as an option and based on the ParentCo’s history of spending ~25% of annual FCF on acquisitions, I’ll conservatively assume the same for PHIN.

That leaves 50% of free cash flow, or $125 million to be spent on buybacks. On the current market cap of $1.25 billion, that’s 10% of the market cap which could be bought back every year. I expect a buyback authorization and dividend announcement imminently.

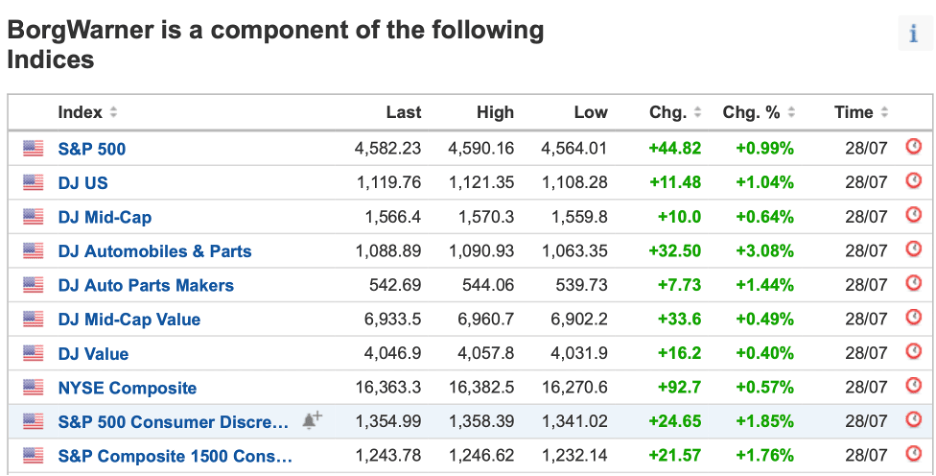

Catalyst #2: H2 2023 – Spin-Off Overhang Dissipating

The market cap of BorgWarner pre-spin was ~$11 billion, while the market cap of PHIN is $1.25 billion. Put another way, if you had a 5% position in BorgWarner, PHIN popped up as a 0.6% position following the spin-off. Chances are, if you were invested in BWA pre-spin, you were in it for the growth narrative and the electric revolution, something PHIN isn’t exposed to. Thus, when faced with the decision of either holding on to a 0.6% position in what’s perceived as a legacy “declining” business, or eliminating it, the average BWA investor would likely sell.

But that’s just the individual retail investor and fund manager; 95% of BWA’s float is owned by institutional investors who own BWA for no other reason than the fact that it’s a component of a lot of indexes … perhaps none more important than the S&P 500.

{kind=link}

Investing.com

My guess is that most of the ~20% decline in PHIN’s share price since the spin is the direct result of indiscriminate selling, and the fact that more than 100% of the float has traded since then supports the same conclusion.

As these negative dynamics abate in the second half of 2023 and trading normalizes, I expect the share price to dramatically rise. I’ve encapsulated my thoughts in the following formula: Less Volume + Greater Demand = Higher Prices. I won’t be winning a Nobel Prize for it, but it does a good job describing the situation.

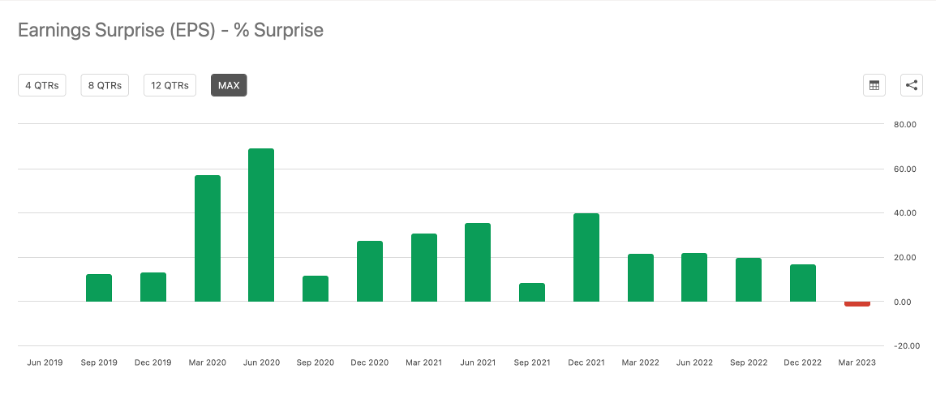

Catalyst #3: H1 2024 – Execution Against 2023 Guidance

Mr. Market despises uncertainty, and the current situation at PHIN screams of it. The management team is largely unknown, they haven’t held any earnings calls yet, and there’s no sense of what their cadence will be with guidance (is it beat-and-raise, hit it perfectly, or miss?). Based on BWA’s history of steadily beating consensus estimates, I believe PHIN will aim to establish a similar cadence going forward and likely set their 2023 EBITDA guidance at the low-end of their expected range to help build rapport with the Street. While we won’t know for sure until the first half of 2024 when they report full year results, BWA’s track record gives me a great deal of comfort.

{kind=link}

BorgWarner EPS Surprise (Seeking Alpha)

Catalyst #4: H1 2024 – Improving “Screen-ability” & Analyst Coverage

Putting all this together, I believe that by the first half of 2024 these three dynamics will collectively serve to increase “screen-ability” and attract analyst coverage, as by then I think PHIN will have the following characteristics:

- A 4.5%+ yielding dividend, versus no dividend today.

- A record of buying back 10%+ of their stock every year and not wasting capital on fruitless endeavors, versus no history today.

- A rapport with the Street, who will be more comfortable with the guidance PHIN sets forth, versus no rapport today.

Additionally, with a full year of earnings under their belt, PHIN will finally appear and look cheap when investors go into a stock screener, as strong 2023 results get reflected. Contrast that to today where nothing pops up in respect to analyst coverage and very little in respect to the income statement.

{kind=link}

Seeking Alpha

Mid-Term – 2027 Bear Case & Risks to the Thesis

The mid-term bear case for PHIN circulates around a complete failure to adapt to hybrid vehicles and a rapid acceleration in the adoption of electric vehicles across the board. In this scenario, I believe Aftermarkets will continue to perform reasonably well over the mid-term, as there’s a meaningful lag between EV adoption and impact to the repair market. Fuel Systems, however, would likely enter a controlled terminal decline of ~5% per year in a disaster scenario. On a combined basis, this would translate to -2% annual revenue growth. Assuming the cost structure doesn’t change, which I view as unlikely if the business were to enter true decline, overall FCF would decline by ~4% per year.

In this scenario, PHIN would still be cheap, as their 2024 free cash flow multiple would be at a ~40% discount to their peers. However, multiples across the board in the auto parts space would likely come down and PHIN could have ~15% downside (5.0x 2023 FCF).

{kind=link}

Author's own work

Mid-Term – 2027 Bull Case

From an earnings perspective, I assume PHINIA grows the top-line at just 3% per year through 2027 in my bull case and that FCF tracks revenue growth. In this scenario, FCF would ramp to $300 million, or $7.50/share. At the same time, if no cash is distributed to shareholders or deployed on M&A, PHIN will be trading at 3.5x EV/FCF in 2025 and 1.3x FCF in 2027. If shares in 2027 trade at just 5.0x free cash flow, PHIN could hit $72, supporting a 25%+ IRR.

{kind=link}

Author's own work

However, if, as I suspect, PHIN becomes a buyback machine, and 50% of FCF goes to share repurchases, then with $1.4 billion of available cash, at an average purchase price of $27 per share (assuming the share price goes nowhere), PHIN could repurchase ~55% of the float. That would push FCF/share in 2027 to $17. At 5.0x FCF that’s an $85 stock, or just under a 35% IRR. Toss in the 5% dividend and things start looking quite attractive.

Conclusion

In all likelihood, PHIN will be a relatively short-term investment for me. As catalysts play out heading into H2 2023 and H1 2024, the stock will likely materially re-rate, potentially as much as 100%+. I’ll be keeping close tabs on PHIN and look forward to providing an update if anything worthwhile occurs.

For further details see:

PHINIA: Highly Catalyzed Spin-Off At 3.5x EBITDA - 100%+ Upside