PLAB - Photronics: A Lot To Like But Not Quite A Buy

2023-12-20 16:46:44 ET

Summary

- Photronics' photomasks business is showing greater strength than the overall semiconductor market, and we highlight why this is the case.

- The business is also witnessing greater flow through to the operating profit level and operating cash flow level as the focus on high-end products and working capital management pays off.

- Even next year, PLAB could likely generate ample FCF to recommence its buyback program or even pay dividends (to the tune of $50m).

- Despite the favorable tailwinds we also note that Photronics may not necessarily be a rewarding investment at these levels.

Introduction

Investors looking for a rather steady and resolute business within the volatile semiconductor landscape may consider looking at the Connecticut-based entity, Photronics, Inc. ( PLAB ), a pure-play photomask business, which has been around for over five decades now. As we highlight in the latter half of our article, a fresh entry in PLAB is not ideal, but we certainly feel it has plenty of useful qualities that would warrant some consideration when you make your watch list.

Resolute Business With Encouraging Tailwinds

The broad semiconductor market has encountered a rough 2023, and will likely witness a decline of - 11% by the end of this year. However, within this semi-space, some avenues have not fared too badly, and one of those is the photomask space which PLAB specializes in, where growth will likely be flat during the same period.

Generally, photomasks play a critical role in the photolithography structure, and because of their importance in the design process, they are less susceptible to the cyclical hues that typically characterize the semi industry. For the uninitiated, photomasks are glass plates that contain microscopic images of electronic circuits. Put another way, they serve as templates for circuit patterns that will eventually be printed onto a wafer.

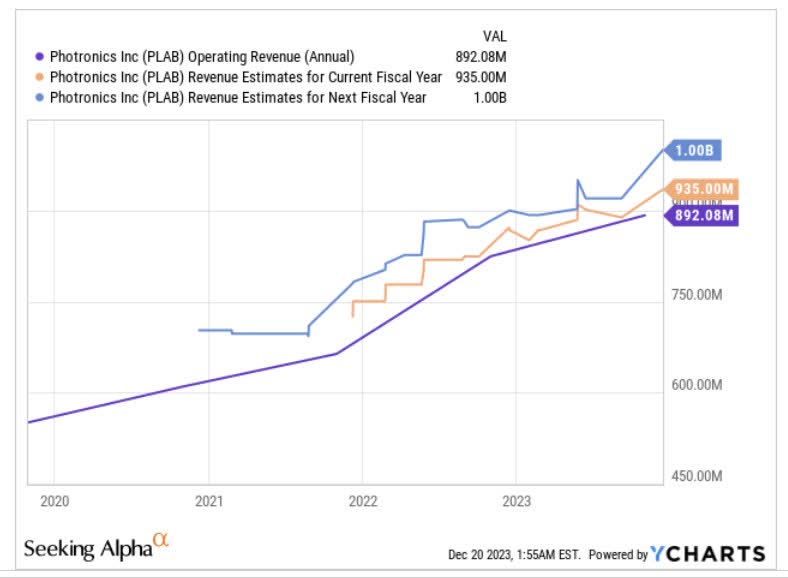

Note that whilst the photomask market saw flattish growth this year, PLAB actually ended up delivering 8% growth for the year, whilst also hitting record levels on the topline. Going forward the expectation is that this market could grow at less than 4% for the foreseeable future, but it looks like PLAB could well take share here, as consensus revenue forecasts for the next two years point to a higher CAGR of 6%.

{kind=link}

Now even though PLAB has its roots in America, it is actually quite well exposed to key markets across the world. Note that it has 11 manufacturing locations, with six of these in key Asian regions such as Taiwan, China, and Korea. It also has a couple of units in Europe, besides America.

Within the global markets, it helps that PLAB is keenly exposed to the Chinese region which accounted for close to 44% of group sales. This exposure has helped PLAB of late as it's a market that is seeing good impetus for new designs. Also note that quite unlike a lot of other markets where PLAB faces competition from the captive units of semiconductor entities, in China, there is a greater predilection to outsource these services to independent specialists such as Photronics.

In addition to that, of late we've also seen a lot of euphoria surrounding AI , and this has prompted semi-manufacturers to focus more on EUV adoption whilst they increasingly outsource the traditional side of the business to specialists such as PLAB.

High-End Product Focus And Superior Working Capital Management Is Driving FCF

PLAB isn't just benefiting from strong topline growth; it's fair to say that the quality of growth too has picked up significantly as the high-end side of the IC business remains very strong (for instance in Q4, this segment witnessed an impressive revenue growth of 27% on a sequential basis, and 30% on a YoY basis as design activity remains robust).

Meanwhile, even in the FPD (Flat Panel Display) portfolio of PLAB's overall business, the high-end segment is seeing strong traction for AMOLED display masks, promoting growth of 23% in Q4. Management implied this trend was likely to persist in 2024 as well.

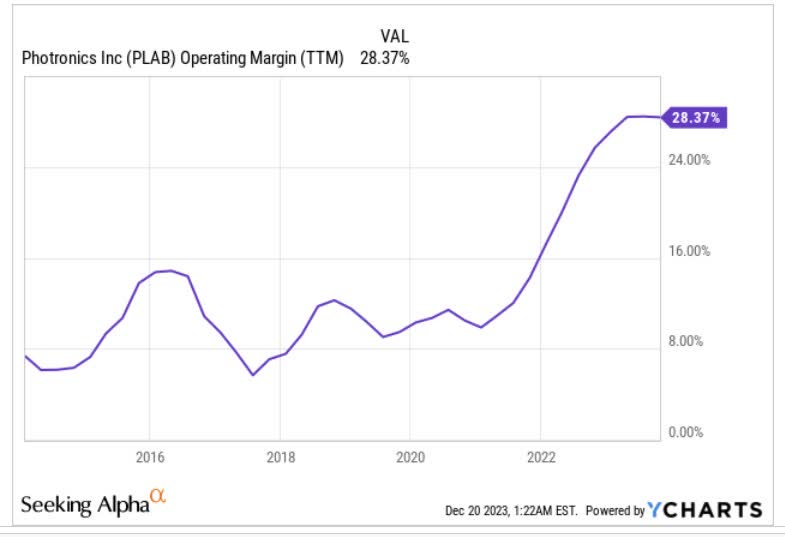

Now, given strong impetus at the high-end products, we're seeing better pricing, translating to a superior margin profile. Note that PLAB's margins are currently at decade-high levels of 28.4%.

{kind=link}

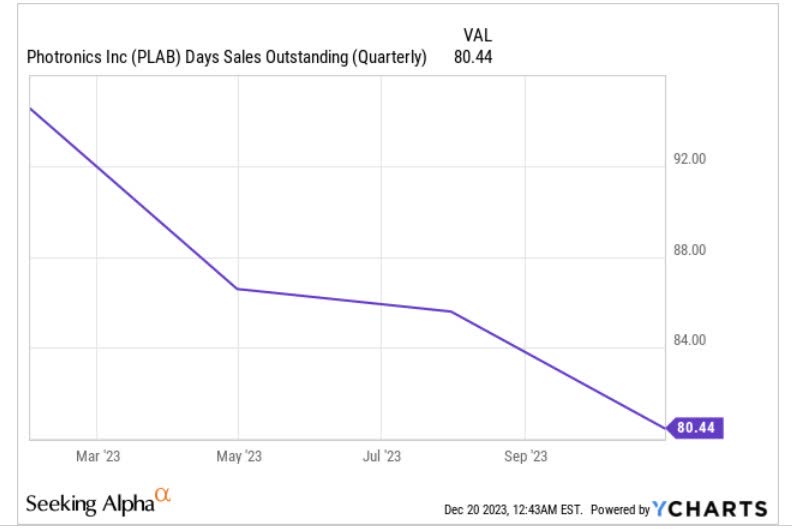

In addition to superior profitability, PLAB is also managing its working capital very efficiently. The accounts receivable component, which makes up the largest chunk of current assets has been witnessing consistent progress all through the year. Note how the DSO has been on a declining trend for four straight quarters.

{kind=link}

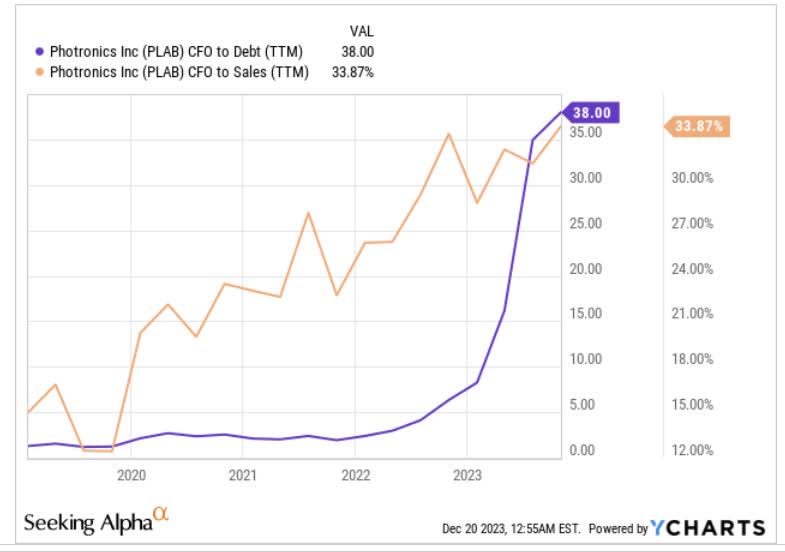

All in all, what we're seeing is very strong flow through from the sales line all the way to the operating cash flow level. The image below highlights how the Sales to operating cash flow which only stood at 12-15% levels during the pre-pandemic phase has now more than doubled and is now at 34%!

Meanwhile, the OCF generated is covering PLAB's minuscule leverage by a massive level of 38x, when a few years back the coverage was only in single-digit terms.

{kind=link}

Shareholder Distributions May Pick Up

Now, if PLAB can continue to generate sustainable and expanding FCF, it won't be too long before we see this being deployed in a larger chunk of share buybacks which have gone dormant for well over a year now. As things stand, PLAB still has $32m of its $100m share buyback program that is yet to be executed.

Next year management implied that they would spend $140m on CAPEX, so if we assume a similar OCF to sales conversion of 34% as seen this year, and take next year's revenue consensus of $935m into consideration, you could be looking at an adequate enough FCF of $177m. Already the company's cash and short-term investment balance is at decade highs of over half a million, so clearly it would make good sense to dole this out as either dividends (their credit covenants permit them to pay dividends to the tune of $50m if they choose to) or buyback the stock.

Closing Thoughts - Not The Most Optimal Point To Buy

Even though PLAB's business has some fine qualities, it is questionable if this is the most opportune time to get on board with the stock.

Firstly, the ongoing period (November-January) is when PLAB has traditionally had to contend with a slump in client purchasing initiatives. Besides the upcoming Q1 will likely also have a lower number of working days than usual (89 days for Q1-24 versus typical levels of 91 days).

We can get a sense of this in the implied sequential trend, for both the topline as well as the bottom line. After delivering Q3 revenue of $227.5m, PLAB management now expects a sequential decline of 1-5%. Meanwhile, the diluted EPS which stood at $0.72 in Q4 is expected to come off by 26-38% on a sequential basis.

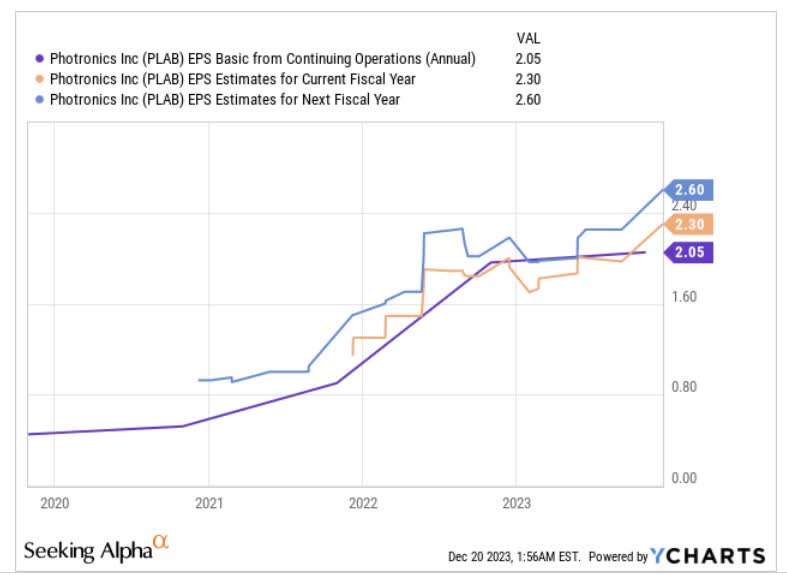

The stock's forward P/E valuations are no longer cheap either, even if one is to make allowances for the medium-term earnings growth rate. Based on consensus EPS estimates for the next couple of years, PLAB looks like it will deliver 8% earnings CAGR for that period.

{kind=link}

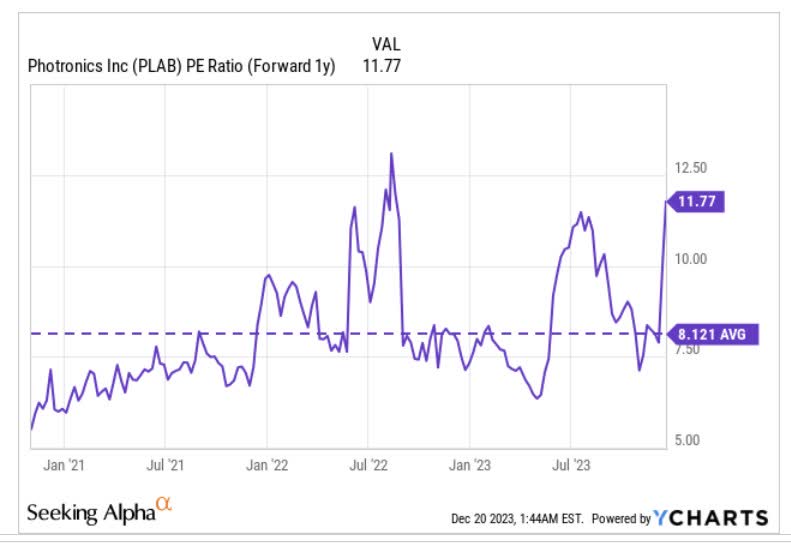

For that degree of medium-term earnings growth potential, a high single-digit P/E could have been deemed as acceptable, translating to close to a 1x PEG ratio, but rather what we have with PLAB now is a P/E of 11.8x, based on the October 2025 EPS. For context, that equates to a whopping 44% premium over the stock's 5-year forward P/E average figure of 8.1x

{kind=link}

Then, if we pivot to the charts, we can't say we're jumping for joy to discover the current risk-reward on offer. The image below measures PLAB's positioning relative to its peers from the semiconductor space. In Q2 this year, one could've maybe made a case for PLAB benefiting from some rotational interest for those fishing for bargain opportunities in the semi space, but at this juncture, that trade looks less attractive with the relative strength ratio well above the mid-point of its 5-year range.

{kind=link}

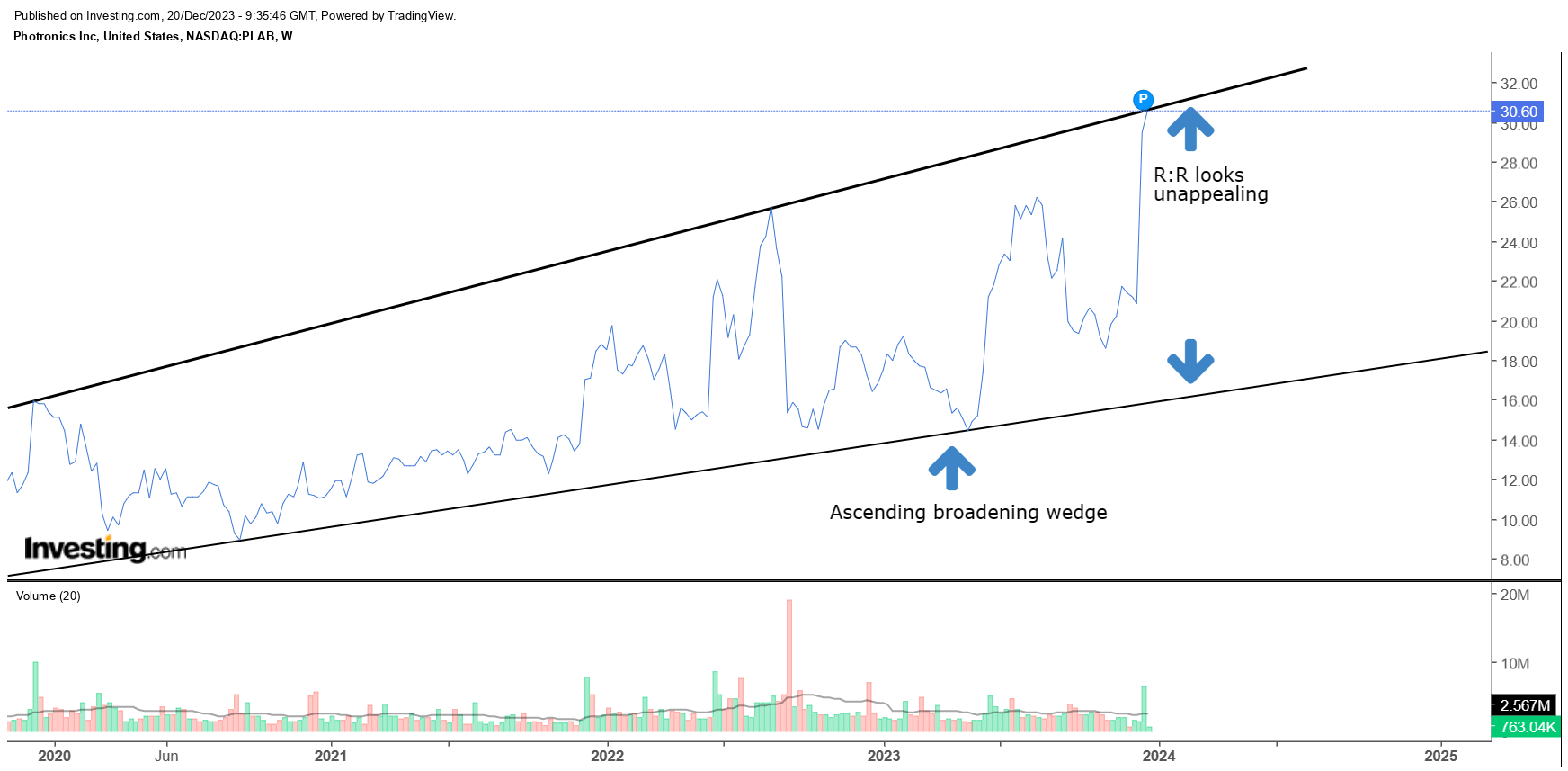

Finally, if we review PLAB's own weekly price imprints over the last four years, it looks as though the stock has been forming an ascending broadening wedge pattern. If you're contemplating a long position, when faced with this pattern, it is preferable to buy somewhere closer to the lower boundary which was the case even as recently as early December. However, given PLAB's remarkable strength since the Q4 results, the reward-to-risk equation has now tilted quite unfavorably with the price now perched close to the upper boundary of the wedge.

{kind=link}

For further details see:

Photronics: A Lot To Like, But Not Quite A Buy