PLAB - Photronics: A Solid Buy Trading At 9 Times Forward Earnings 40% Upside

2023-08-10 06:51:55 ET

Summary

- Photronics has achieved significant improvements in margins and is undervalued, making it a buy at current levels.

- The company's unique position in the photomasking segment of semiconductors gives it pricing power and the ability to maintain high margins.

- While there is a high dependency on China for revenues, the company has experienced minimal impact from geopolitical tensions and is expected to continue operations in China.

Investment Thesis

With Q3 earnings just around the corner, I wanted to take a look at Photronics (PLAB) and see what it is worth now that the company managed to achieve very good improvements in margins in the last year and whether it can continue to hold on to them in the future. Even with a deterioration in gross margins in FY23 is assumed, the company seems to be undervalued currently and is a buy at these levels, but investors may be cautious of high dependency on China for revenues which may keep the company's share price cheap.

Briefly on Company

Photronics is a leader in manufacturing of photomasks, which are quartz plates that are commonly used in for the production on integrated circuits, or chips. The company specialises in two segments, Integrated Circuits and Flat-panel Displays or FPDs for short.

Outlook

It seems that the company didn't experience the same dire results as many other much larger semiconductor companies in recent years and quarters. The company is very uniquely positioned in the photomasking segment of semis. As CEO Frank Lee mentioned in the transcript that the company is looking to maintain these new margin levels going forward because the demand for the product outweighs the supply, which is the opposite for other semiconductors, so the company has a lot of pricing power in that regard, which will help the company maintain these fantastic margins going forward. I believe this is going to be very good for the company in the long run, especially now that the semiconductor industry's negative sentiment has started to reverse, and a lot of companies believe that the worst is over, and the throughs have been reached. So, if the company did so well during the most negative time in recent times in the semiconductor industry, I believe the company will do even better once the industry returns to growth, which is expected to be sometime in late '23 or early '24. I think that higher margins are sustainable, but I will be a little more conservative and say that margins will come down from those highs we saw in FY22 just to be on the safer side.

Risks

The company saw 51% of its total revenue in Q2 coming in from China. This is where I believe a lot of investors turn away from investing in companies that have such a large exposure to China due to geopolitical tensions. So far, the company experienced minimal impact from any restrictions that the US imposed on China. The company has been talking about these risks in Q4 '22 and the last two quarters, it seems that that is still the case. It is a very valid concern of course, but I don't believe the company will lose a substantial revenue portion and will be able to acquire any licenses/ tools need to continue its operations in and with China.

The tensions may escalate further and the share price may tank especially if the company does not diversify away from the dependency on revenue from China.

I would like to see the company diversifying a lot more in the future so the exposure to China is minimized, but we will have to wait and see how the next quarters develop.

The negative sentiment in the semiconductor industry may last longer than expected, which is the beginning of '24, coupled with elevated interest rates and inflation. These may keep the company's share price depressed and it may not reach the full potential.

The CEO has said that the company is enjoying a lot of pricing power right now because of the lack of supply for photomasks, however, competitors may be able to take some of that market share if they believe it is very profitable, which will bring down PLAB's competitive advantage and the margins may come down again to below 30% on gross.

Financials

Just to note, the below graphs will be as of FY22 and will have yearly figures to see the overall trend, however, I will include any necessary figures from the latest quarter to provide extra color.

As of Q2 '23, the company had around $412m in liquidity against $21m in long-term debt. This is a very good position to be in and follows the trend of other semiconductor companies that have a big pile of cash with little to no long-term debt obligations. This provides the company with a lot of flexibility around its operations, to expand its global footprint, experiment with new techniques and tools to be even more efficient, and reward long-term shareholders. It is safe to say the company has no insolvency risks.

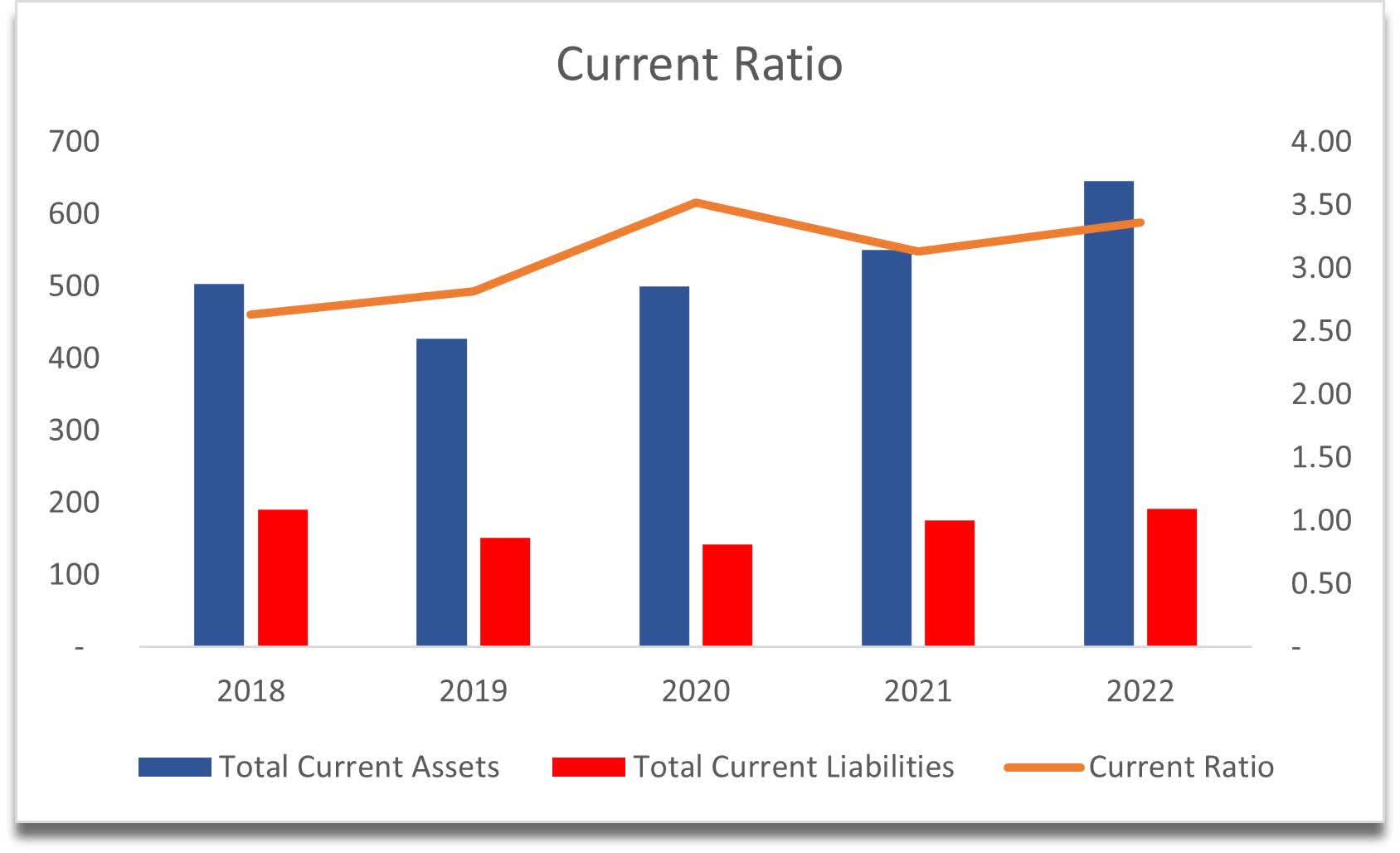

The large amount of cash pile also means that the company isn't being very efficient with its assets. It is great to have a lot of liquidity but in my opinion, there is an efficient range. The company's historical current ratio has been consistently over my top range, which is 2.0. I believe an efficient range is anything from 1.5 to 2.0. This would tell me the company has enough liquidity to cover its short-term obligations efficiently, but if anything over that range I think the company isn't being aggressive enough in using its cash reserves for growth. As of Q2 '23, the current ratio stood at 3.9.

{kind=link}

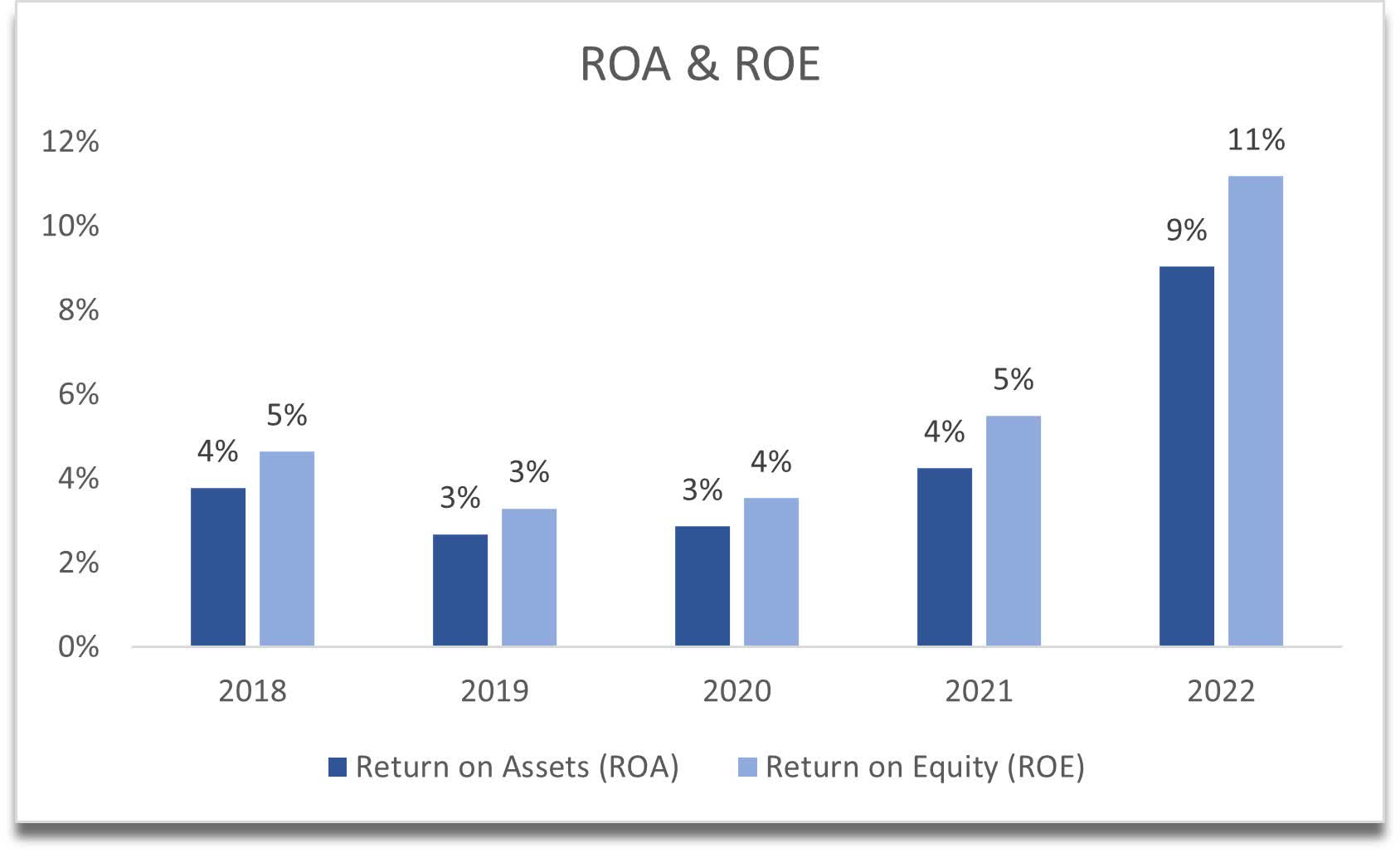

The company's ROA and ROE have also improved in FY22, which were boosted by net income doubling y-o-y. I think the company will be able to achieve similar returns going forward, which are above my minimums of 5% for ROA and 10% for ROE.

{kind=link}

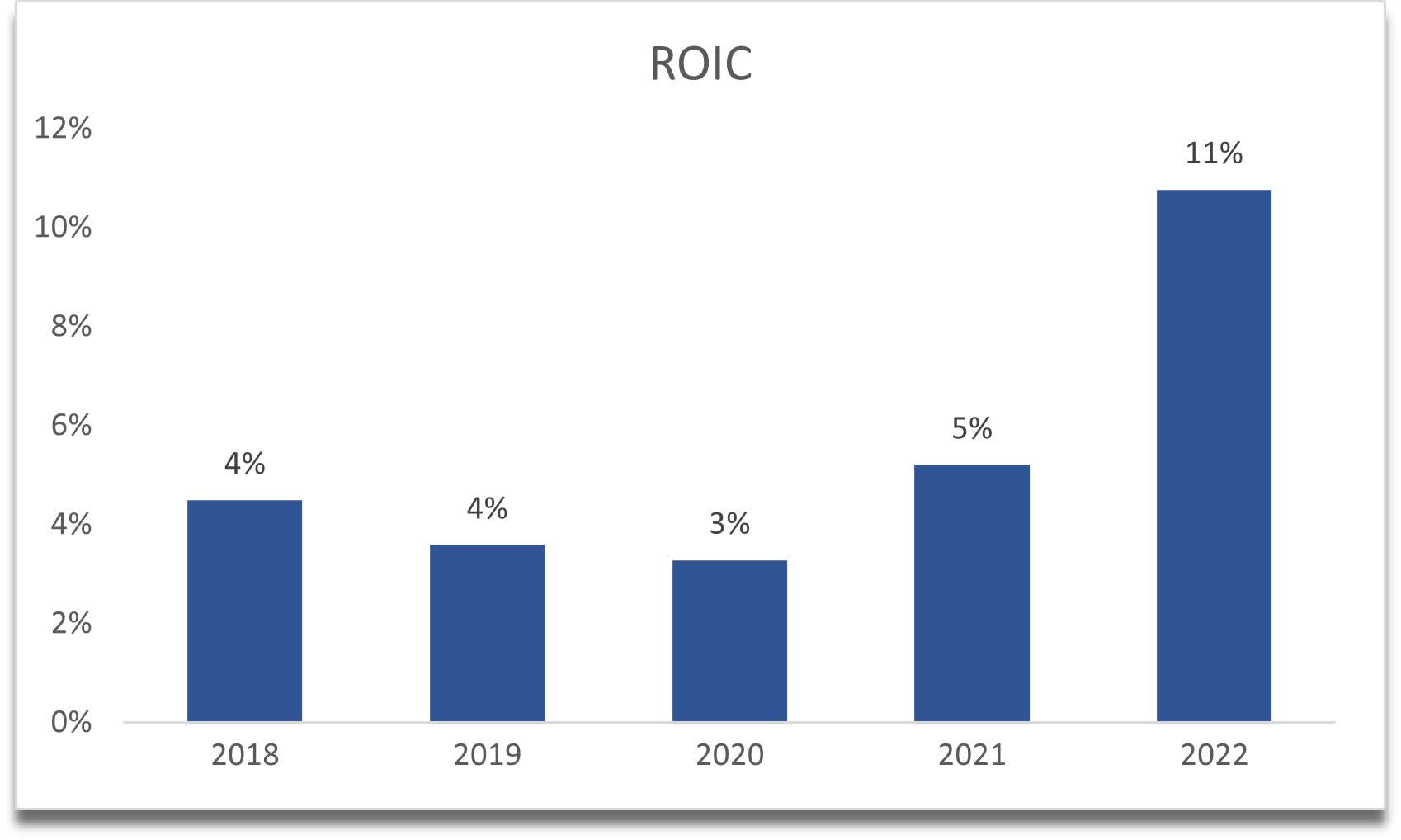

The same story can be said about the company's return on invested capital. It seems like the company has achieved a much better competitive advantage and a strong moat since FY21 and I believe this will be sustained as the CEO mentioned above that the company has a lot of pricing power in the industry.

{kind=link}

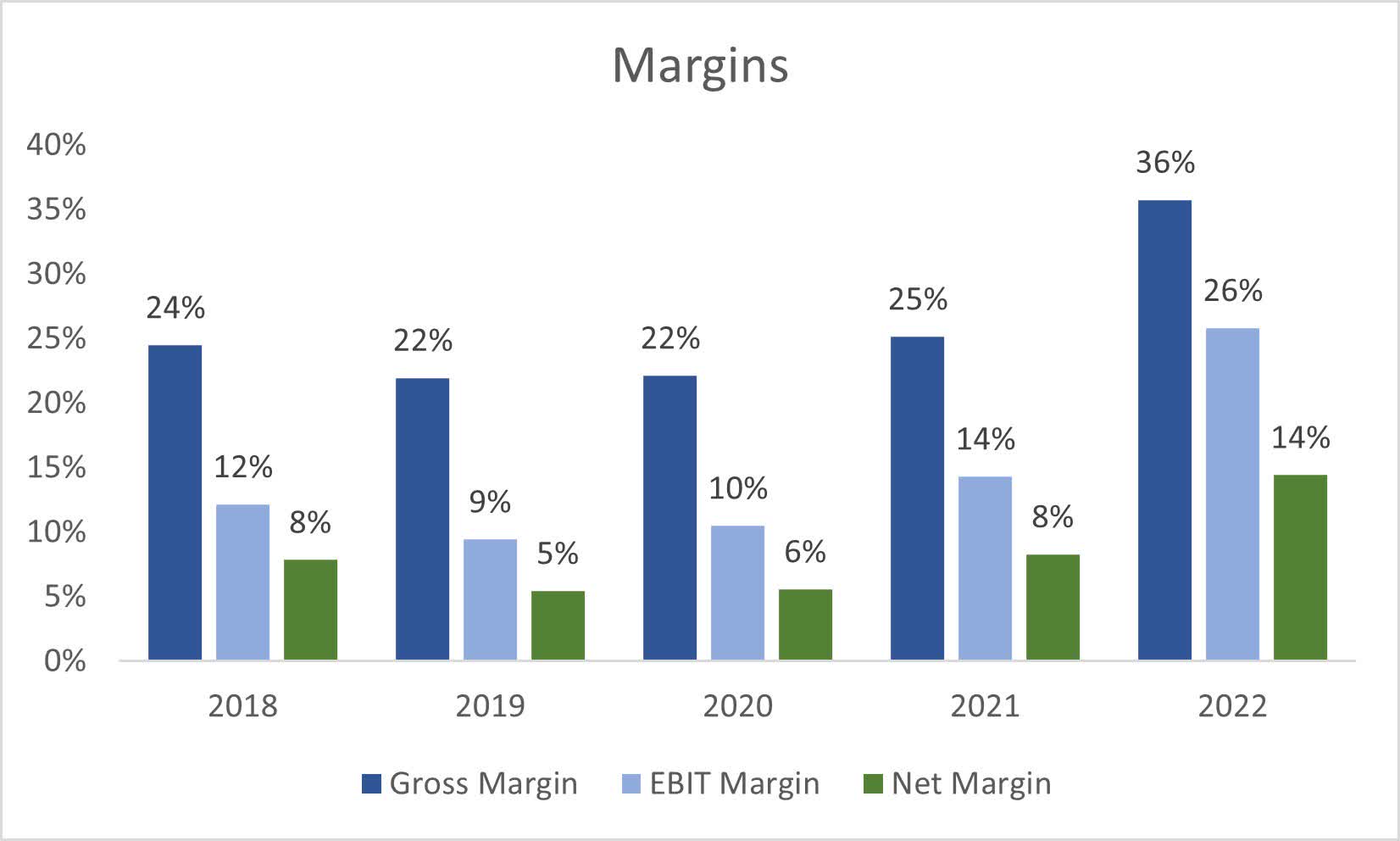

In terms of margins, I believe this is as good as it is going to get in the long run, which is quite an improvement from FY21 and if the company can sustain, it will reward its shareholders substantially over the long run.

{kind=link}

Overall, I see that something clicked in the company in FY22. It seems that the pricing power in FY22 was very strong, which enabled the company to achieve much higher margins and profitability, which may continue going forward.

Valuation

In the last decade, the company achieved around 8% CAGR, so I decided to apply similar growth for the next decade to keep it conservative. In FY22, the company managed to grow revenues by 24%, so my assumptions for the base case are at the lower end in my opinion. For the optimistic case, I went with around 12% CAGR, while for the conservative case, I went with 6% CAGR.

In terms of margins, I decided to lower gross margins by 400bps from FY22 and over the next decade to return these to FY22 levels, while keeping operating expenses in % of revenues the same. This will bring net margins from 14% in FY22 to around 19% by FY32.

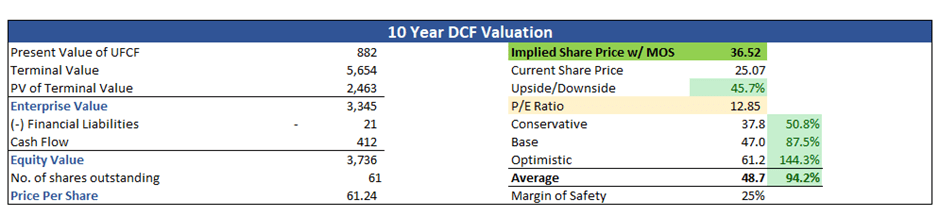

I will also add a 25% margin of safety to the final calculation, which is the lowest MoS I add to companies that have solid financials. With that said, I believe the company is around 42% undervalued currently and is worth $36.52 a share.

{kind=link}

Closing Comments

According to my FY23 estimates, the company is trading at around 9.6 times FY23 earnings, which I believe is very cheap. Even if we look at the only analyst that covers the company, the stock is trading at around 13x FY23 earnings. So, it seems that even after such a runup recently, the company still has a lot of potential to perform well and I believe that with the positive sentiment coming back to the semiconductor industry at the end of '23 and early '24, the company will be able to perform decently and will be able to retain its pricing power.

The earnings report is coming out on August 23rd (according to SA). I will wait patiently until the day to see how much of the revenue is going to come from China and what is the guidance for the rest of the year, but I don't think it will change much and will have my finger on the buy button.

For further details see:

Photronics: A Solid Buy Trading At 9 Times Forward Earnings, 40% Upside