VNOM - PHX Minerals: A Good Natural Gas Royalties Play

2023-08-31 18:10:01 ET

Summary

- PHX Minerals Inc. operates primarily in the SCOOP and Haynesville Shale plays, with a significant presence in these regions.

- The company's business model involves taking a royalty or working interest in wells drilled on its land, exposing it to energy price fluctuations.

- Despite recent financial performance challenges due to low energy prices, PHX Minerals could benefit from the growing demand for natural gas in the Haynesville Shale.

- The demand for natural gas from LNG plants along the coast should be 10 billion cubic feet per day by 2030 and PHX Minerals is well positioned for this.

- PHX Minerals Inc. has a strong balance sheet and a very reasonable valuation.

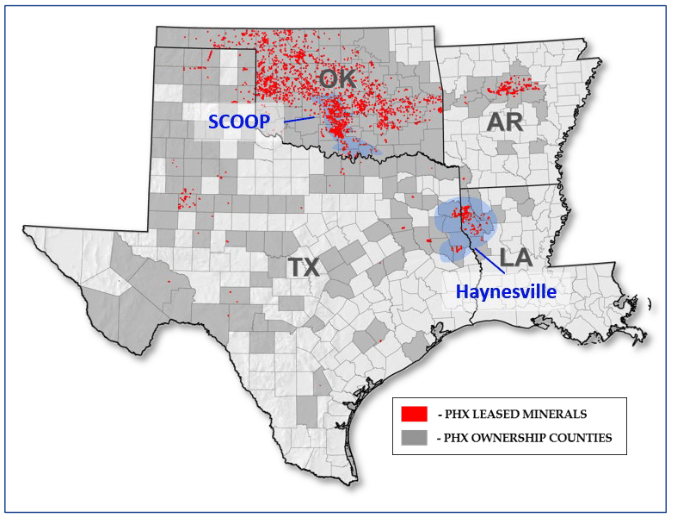

PHX Minerals Inc. ( PHX ) is an independent exploration and production company that primarily operates in the SCOOP and Haynesville Shale plays in Oklahoma, Texas, and Louisiana:

{kind=link}

The company does have operations in a few other regions, however. The substantial presence in these regions makes PHX Minerals somewhat unique among exploration and production companies, as there are relatively few that focus their operations in these two areas. The Haynesville Shale is growing in importance somewhat though, as its proximity to the Gulf Coast makes it a good production location for those companies that are looking to produce natural gas to feed the numerous liquefaction plants being constructed along the coast. PHX Minerals could be positioned to profit off of this growing demand for natural gas. I pointed out this natural gas opportunity for the company the last time that we discussed it, but it still remains valid as the natural gas export industry continues to have very strong fundamentals. PHX Minerals also boasts a very strong balance sheet and a reasonable valuation, so it could be an intriguing opportunity right now.

About PHX Minerals

As stated in the introduction, PHX Minerals is an independent exploration and production company that primarily operates in the SCOOP and Haynesville Shale regions of Oklahoma, Louisiana, and Texas but also has operations elsewhere in the country. The company’s operating locations are not the only unique thing about this company, though. Its business model is somewhat unique as the company does not actually drill for resources on its acreage. Rather, it simply takes a royalty or working interest in any well drilled on its land.

I explained the difference between a royalty and a working interest stake in my previous article on this company, but the important thing is that PHX Minerals receives a portion of the production from any well that is drilled on its acreage. The well is actually drilled and operated by an upstream exploration and production company such as Southwestern Energy ( SWN ), Continental Resources, Chesapeake Energy ( CHK ), and several others depending on the basin in which the company operates. However, the company’s practice of taking a stake in a well’s production does expose it to some of the same factors that affect the performance of other energy companies. One of the most important of these factors is energy prices.

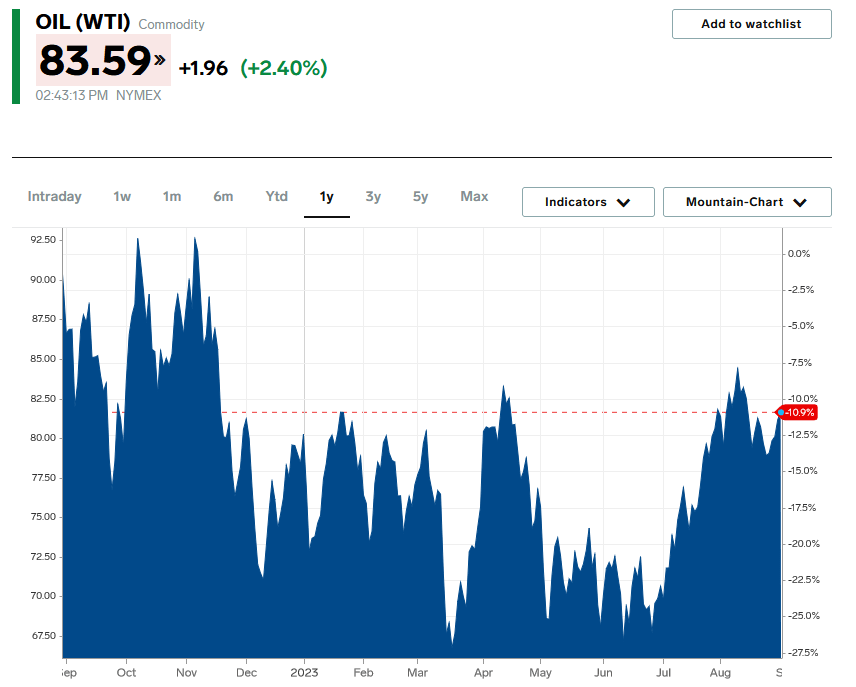

Unfortunately, energy prices were something of a drag on PHX Mineral’s recent financial performance. As of the time of writing, the price of West Texas Intermediate crude oil is down 10.90% over the past year but it was down quite a bit more over most of the trailing twelve-month period:

{kind=link}

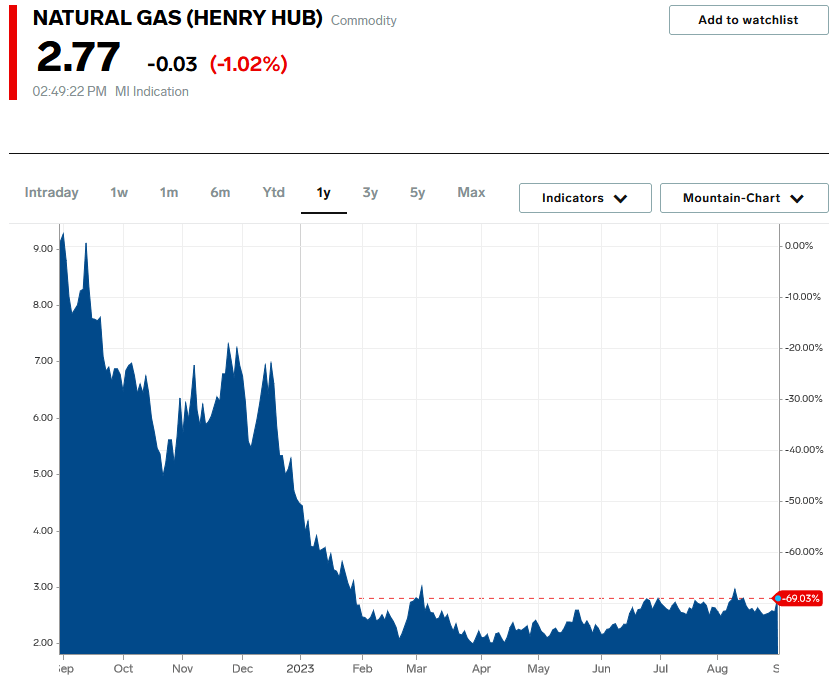

The performance of natural gas has been even worse. Natural gas at Henry Hub is down a whopping 69.03% over the past twelve months:

{kind=link}

There were a few reasons for this poor performance. In the case of crude oil, the Federal Government was selling crude oil from the Strategic Petroleum Reserve for much of the second half of last year as well as through July of this year to attempt to keep the supply of crude oil high and prices down. I explained the reasons for the low natural gas prices in a blog post earlier this year, but two of the major reasons were the warm winter and the temporary shutdown of the Freeport LNG facility. These two factors caused a glut of natural gas in North America, which pushed prices down due to the economic law of supply and demand.

Natural gas prices are generally more important than crude oil for PHX Minerals due to the production profile of its acreage. In the second quarter, the company received a total of 2.304113 billion cubic feet of natural gas equivalent. Of that, 1.854485 billion cubic feet was dry natural gas. Thus, approximately 80.49% of the company’s business is natural gas as opposed to crude oil or other hydrocarbons. Clearly, natural gas fundamentals are much more important to the company than crude oil. This is a good thing because the long-term fundamentals for natural gas are better than crude oil’s long-term fundamentals as we will now discuss.

This decline in resource prices has certainly had an impact on PHX Minerals’ financial performance. In the second quarter of 2023, the amount of natural gas that was produced on the company’s acreage was close to record levels, but the price was substantially lower than in the same quarter of last year:

PHX Minerals

PHX Minerals reported an adjusted EBITDA of $4.1 million in the second quarter of 2023 compared to $7.2 million in the second quarter of 2022. This lower cash flow is despite the fact that the amount of natural gas that the company received as royalty payments was quite a bit higher than in the same period last year. Unfortunately, there does not appear to be a near-term catalyst that would drive natural gas prices back up. We are seeing some upstream producers beginning to reduce their production, but this will take quite a while to make its way through the system. Currently, forecasters are saying that the upcoming winter will be more typical than last year, so that could help reduce some of the natural gas oversupply if they are correct. However, it remains to be seen if the forecasters are correct about this, and how much of an impact it will have on the balance between natural gas supply and demand.

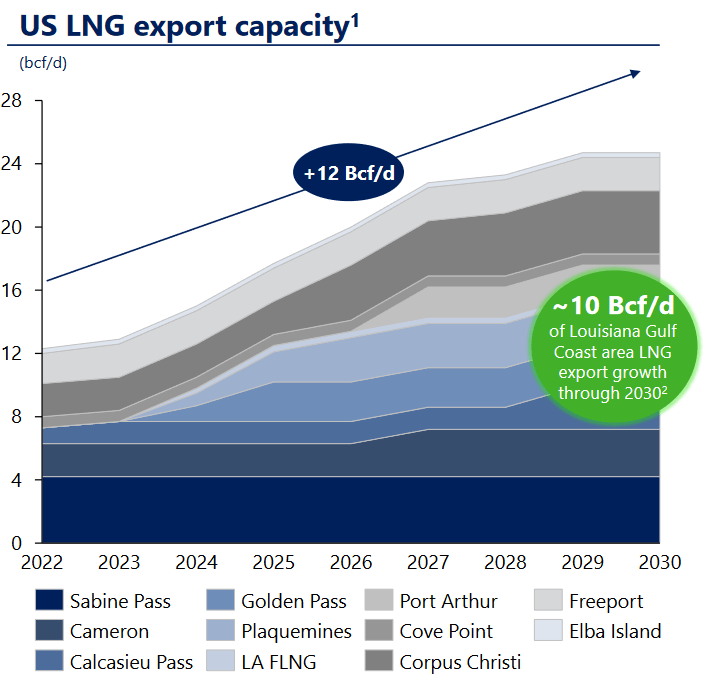

The long-term fundamentals for natural gas are much better than the near-term ones though, which is fortunate for PHX Minerals. As already mentioned, PHX Minerals has significant acreage in the Haynesville Shale. The Haynesville Shale is very well-positioned to supply natural gas to the liquefaction plants that are being constructed along the Gulf Coast. The demand from natural gas from these facilities will likely be enormous. Indeed, Wood Mackenzie states that the liquefaction plants currently under development will increase the demand for natural gas by 10 billion cubic feet per day by 2030:

{kind=link}

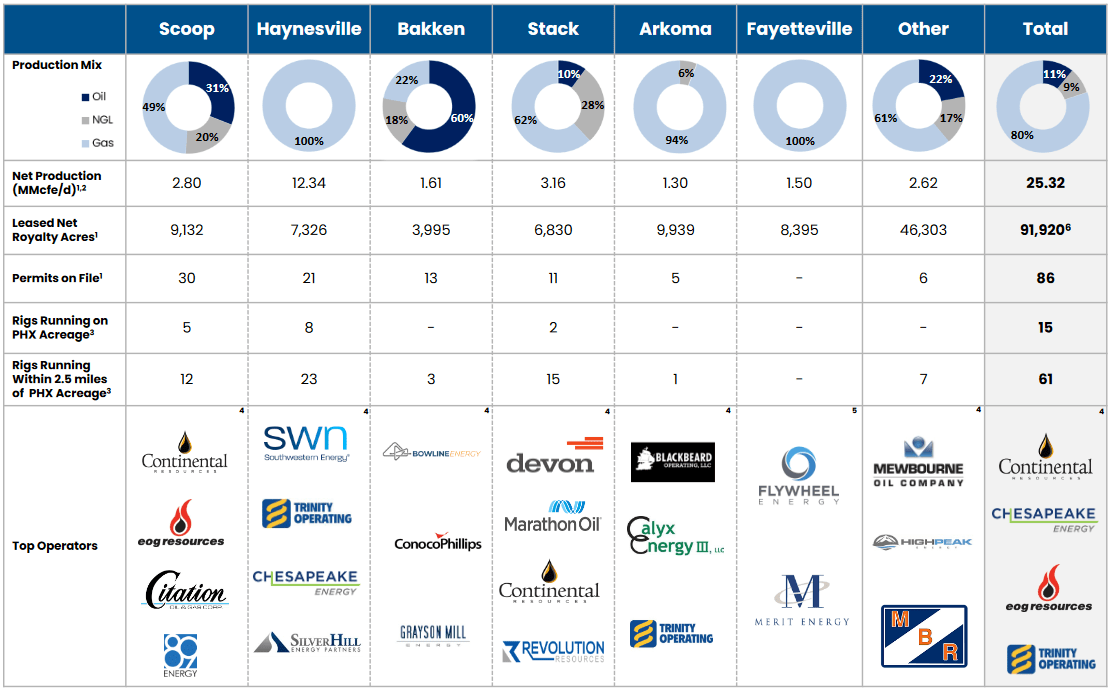

It seems reasonable that a significant percentage of the natural gas that will be supplying these plants will be produced in the Haynesville Shale and the Permian Basin. This is due mostly to their proximity to the Gulf Coast. The other major natural gas-producing region in the United States, Appalachia, will probably end up supplying East Coast utilities and the handful of liquefaction plants that are being constructed near Philadelphia, Pennsylvania. As of the time of writing, 48.74% of PHX Minerals’ total royalty production is in the Haynesville Shale, which is substantially more than any other basin:

{kind=link}

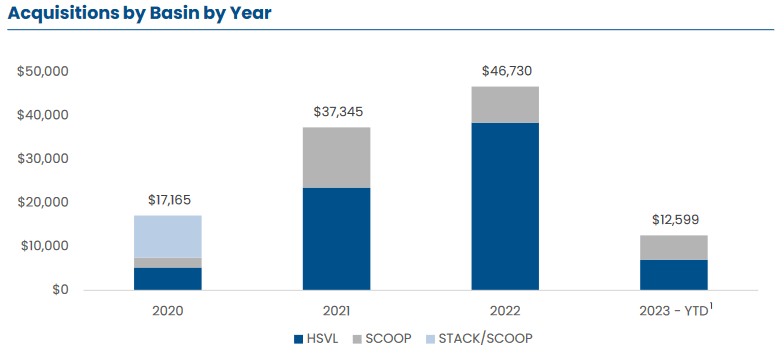

Thus, it is reasonable to assume that the company will benefit from any growth in natural gas production in the Haynesville Shale. After all, that scenario would almost certainly result in the company’s customers needing to lease more acreage on which to produce natural gas to satisfy the demand. PHX Minerals seems to realize this as it has been focusing its recent land acquisitions on the Haynesville Shale. We can see that quite easily here:

{kind=link}

As we can see, about half of the acreage that the company acquired this year was in the Haynesville Shale. It was substantially more than half of its acquisitions in 2021 and 2022. This all represents acreage that the company can lease out to its customers. Clearly, management sees a great deal of opportunity in the Haynesville Shale. I do, too, and this is one of the things that we can appreciate about this company.

Financial Considerations

As mentioned in the introduction, PHX Minerals has a very strong balance sheet. We can see this by looking at the net debt-to-equity ratio. As of June 30, 2023, PHX Minerals had a net debt of $23.5 million compared to $120.1 million in shareholders’ equity. This gives the company a net debt-to-equity ratio of 0.20 today. This is lower than the 0.29 ratio that the company had the last time that we discussed it. That is a positive sign as it indicates that the company managed to strengthen its balance sheet somewhat over the past quarter. Here is how the company compares to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| PHX Minerals |

| 0.20 |

| Northern Oil and Gas ( NOG ) |

| 1.17 |

| Diamondback Energy ( FANG ) |

| 0.41 |

| Viper Energy Partners ( VNOM ) |

| 0.28 |

| Coterra Energy ( CTRA ) |

| 0.14 |

I pointed out one important thing for this comparison in my previous article on PHX Minerals:

“Admittedly, not all of these companies are perfect peers for PHX Minerals due to its focus on collecting royalties rather than producing crude oil natural gas. Northern Oil and Gas and Viper Energy Partners both use a very similar model though, and as we can see, PHX Minerals compares fairly well to both of them.”

This is a good situation that strongly implies that we should not have to worry too much about the company’s leverage. The company’s use of leverage or lack thereof is somewhat more important for an energy producer like PHX Minerals than it would be for many other companies because of the inherent volatility of energy prices. Overall, everything looks good here.

Valuation

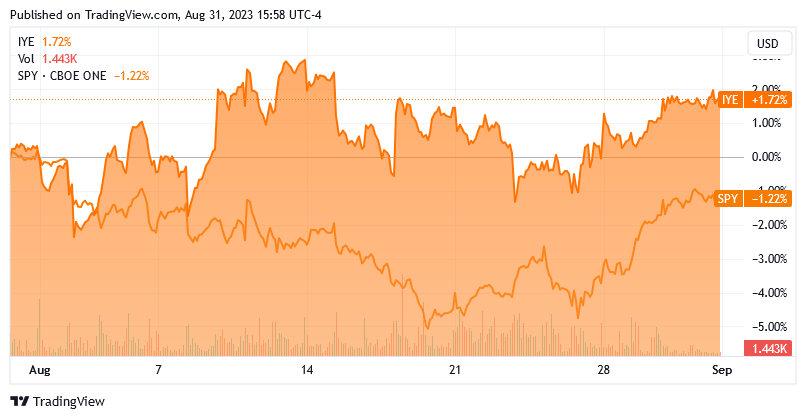

As I have pointed out in numerous previous articles, pretty much the entire traditional energy sector appears to be substantially undervalued relative to the broader market. This continues to be true despite the fact that the energy sector has outperformed the S&P 500 Index (SP500) by quite a lot over the past month. This chart shows the iShares U.S. Energy ETF ( IYE ) against the S&P 500 Index:

{kind=link}

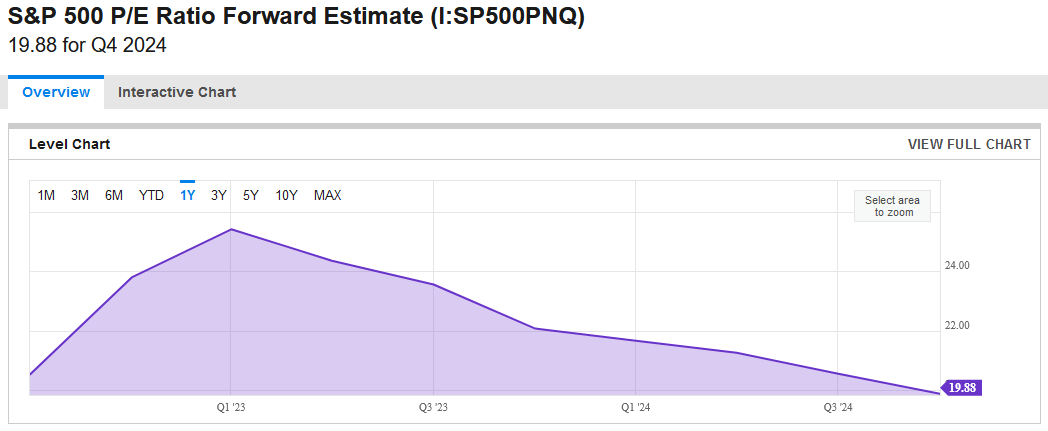

The weakness in the broader market has brought the forward price-to-earnings ratio of the S&P 500 Index to 19.88 at the current level:

{kind=link}

PHX Minerals is quite a bit below this, though. As of the time of writing, the company’s forward price-to-earnings is 9.35 according to Zacks Investment Research . Here is how that compares to the energy producers that we used for the peer comparison earlier:

| Company |

| Forward P/E Ratio |

| PHX Minerals |

| 9.35 |

| Northern Oil and Gas |

| 5.66 |

| Diamondback Energy |

| 8.73 |

| Viper Energy Partners |

| 16.94 |

| Coterra Energy |

| 12.23 |

PHX Minerals is only the median company here, which might imply that the stock is fairly valued. However, it is clearly substantially well below the comparable ratio for the S&P 500 Index. As such, it is very hard not to call this company undervalued. Overall, it is probably worth thinking about adding to a portfolio, especially if you want to have some exposure to the liquefied natural gas growth story.

Conclusion

In conclusion, PHX Minerals is a somewhat unique independent exploration and production company that appears to be well-positioned to profit from the coming liquefied natural gas boom. The company’s cash flow has struggled a bit from the low-price environment, but this will hopefully resolve itself as the demand for natural gas continues to grow since producers will probably restrict output until prices rise. PHX Minerals Inc. stock is trading at a reasonable price and the company boasts a very strong balance sheet. Overall, it might be worth considering as a play on natural gas.

For further details see:

PHX Minerals: A Good Natural Gas Royalties Play