CTRA - PHX Minerals: Play On Royalties Not Production

2023-06-08 08:53:37 ET

Summary

- PHX Minerals is a royalty-focused energy company that primarily operates in the Haynesville Shale and SCOOP plays.

- The company is mostly focused on natural gas, which has delivered a very disappointing performance this year.

- The company is gradually converting from a WI to a much-higher margin royalty model that could offset some of the pricing weakness.

- The company has a very strong balance sheet and limited debt.

- The company is a bit expensive relative to its peers, but it is cheap compared to the market as a whole.

PHX Minerals Inc. ( PHX ) is an independent oil and gas company that operates throughout the United States, although its operations are primarily centered around the SCOOP and Haynesville Shale plays. These are not basins that are frequently discussed in the investment media, which could prove advantageous for the company in terms of valuation. In particular, its Haynesville Shale acreage positions it quite well to take advantage of the rising demand for natural gas over the coming years. This is a general thesis that I have discussed in numerous previous articles. PHX Minerals has a rather unique business model for an oil and gas company as the company does not actually produce oil and gas itself but simply takes a royalty interest in the wells that are drilled on its acreage. This reduces the need for expensive rigs and other equipment and should provide the company with superior margins compared to many other companies in the industry. The stock has unfortunately been adversely impacted by the weakness in oil prices that we have seen this year, but this weakness also appears to be creating a reasonable entry point for investors. Let us investigate and see if this company could be a good addition to a portfolio today.

About PHX Minerals

As stated in the introduction, PHX Minerals is an independent oil and gas company that primarily operates in the South Central Oklahoma Oil Province and the Haynesville Shale plays:

PHX Minerals

These are not plays that we hear about very often in the financial media or any media for that matter. This is rather surprising, particularly considering that the Haynesville Shale is one of the richest sources of natural gas in the United States. Indeed, the U.S. Energy Information Administration states that the Haynesville Shale contains more proven natural gas reserves than any basins in the United States except for the Marcellus Shale and Permian Basins:

U.S. Energy Information Administration

{kind=link}

The SCOOP play in Oklahoma is not nearly as large as the major basins in the country as the Department of Energy states that it has 433 million barrels of proved reserves, which is larger than only Appalachia and the Barnett Shale:

U.S. Energy Information Administration

{kind=link}

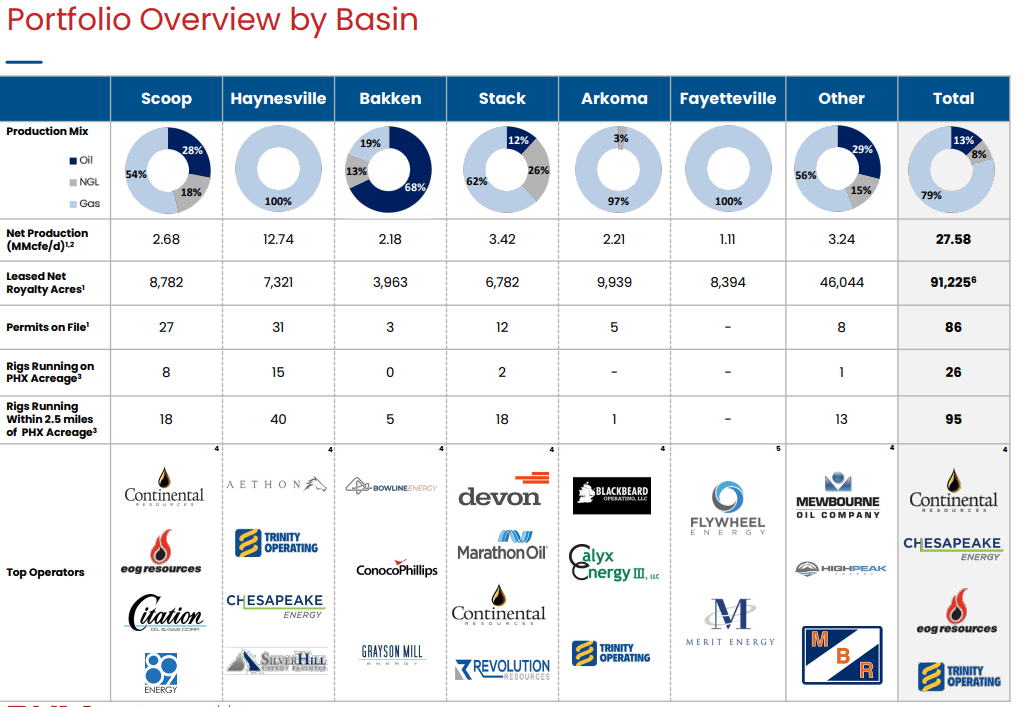

It is the natural gas that is the most interesting thing here as the International Energy Administration predicts that the global demand for natural gas will increase by 29% by 2040. This is due to its use as a supplementary fuel source to renewables, which are unable to support a modern electric grid on their own. PHX Minerals is very well-positioned to take advantage of that as its acreage is very heavily weighted towards natural gas. As we can see here, the majority of the production on the company's land in every basin except for the Permian is natural gas:

{kind=link}

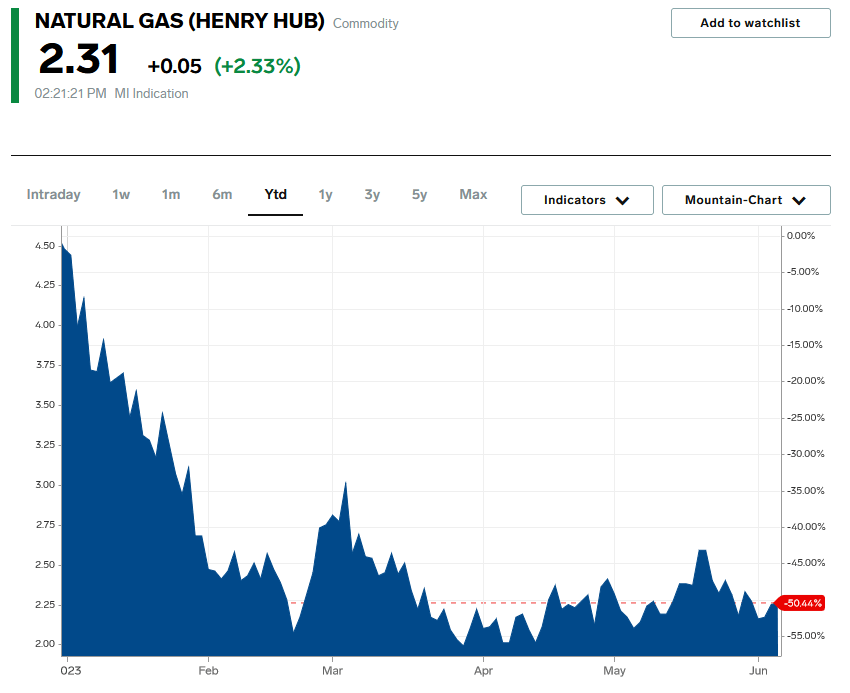

This is something that has unfortunately dragged on the company's stock price so far this year. As everyone reading this is no doubt aware, natural gas has delivered a very disappointing performance year-to-date. Since January 1, 2023, natural gas prices at Henry Hub are down a whopping 50.44%:

{kind=link}

This price weakness was primarily driven by a combination of a warmer-than-normal winter as well as the shutdown of the Freeport LNG terminal, which is otherwise a significant source of natural gas demand. These two supplies have resulted in a supply glut that has yet to clear up despite the fact that American natural gas producers have been cutting their output. PHX Minerals' share price is fortunately only down 19.09% year-to-date as of the time of writing, but this is still disappointing considering that the market as a whole has performed rather well so far this year.

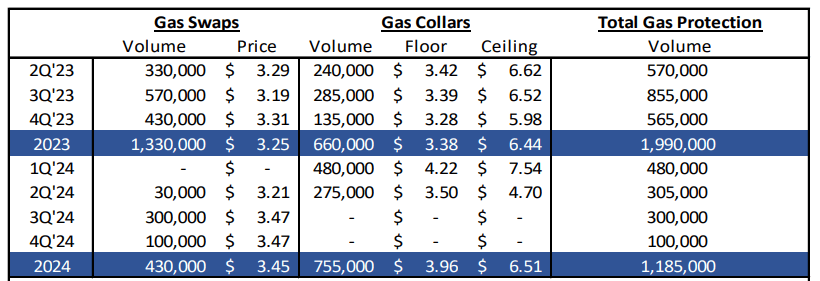

It is uncertain what the near-term future of natural gas prices will be, but PHX Minerals is surprisingly reasonably protected from price weakness. This is because the company employs a hedging strategy to protect itself. This is a common strategy used by smaller companies with significant exposure to volatile commodity prices. In short, the company employs derivatives such as futures and forwards contracts to lock in a selling price for the products that it sells. In the case of natural gas, the company has contracts to sell a total of 1.990 billion cubic feet of natural gas priced at $3.25 to $3.38 per thousand cubic feet:

{kind=link}

This is obviously significantly above the current price for natural gas. This limits the company's exposure to natural gas price fluctuations as it means that the company will be receiving the hedged price for its natural gas regardless of what the price of natural gas actually is. With that said though, PHX Minerals had actual royalty and working interest production of 2.482 billion cubic feet of natural gas equivalent in the first quarter of 2023 and has guided to a full-year production level of 8.60 to 10.00 billion cubic feet of natural gas equivalent, so these hedges do not even come close to covering the majority of the company's production. Thus, PHX Minerals does still have exposure to energy prices that should not be ignored.

As already mentioned, we have been seeing upstream natural gas producers cut back on their production in response to the supply glut and the resulting low prices. As such, PHX Minerals is not likely to benefit from an increase in its collected royalties to offset the impact of the low-price environment. The company's guidance is for full-year royalty and working interest production of 8.60 to 10.00 billion cubic feet of natural gas equivalents, as already mentioned. The company's royalty and working interest production for the full-year 2022 period was 9.697 billion cubic feet of natural gas equivalent. Thus, the company is guiding for flat to declining production this year. It can be at least somewhat confident in these figures due to the fact that the companies drilling on its acreage have shared their drilling plans with PHX Minerals. That is disappointing, as it means that PHX Minerals will not have additional products to sell and offset the fact that it is receiving less for each unit of product that it does sell.

However, it is important to note that there is a difference between royalty and working interest production. Mercer Capital provides definitions of each on its webpage :

- Royalty Interest: An ownership in production that bears no cost in production. Royalty interest owners receive their share of production revenue before the working interest owners.

- Working Interest: An ownership in a well that bears 100% of the cost of production. Working interest owners receive their share of the profit after (i) royalty owners have received their share and (ii) after all operating expenses have been paid.

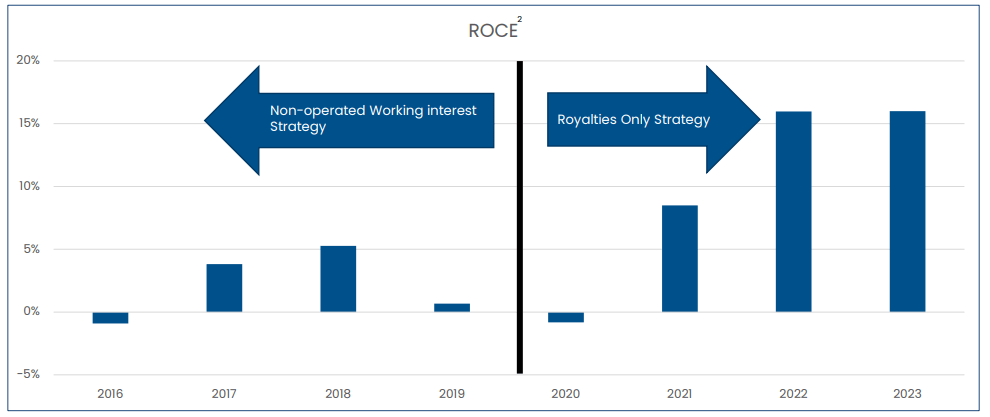

Obviously, royalty interests are going to have higher margins because the royalty owner does not have to pay a percentage of the well's costs. Over the past few years, PHX Minerals has been attempting to increase its royalties at the expense of working interest. The company made this shift in earnest starting in 2020, at which time it started taking only a royalty interest in the wells that are drilled on its acreage as opposed to taking a working interest. The company notes in its most recent investor presentation that this strategy has allowed it to substantially increase its return on capital employed:

{kind=link}

I commented on this in the introduction, as the lower expenses of the company's royalties-focused strategy boost its margins significantly. The reason that this is important as we go forward is that PHX Minerals' guidance actually states that its royalty production will increase in 2023, even though its total production remains static:

| FY 2022A |

| FY 2023E |

| Royalty Production (mmcfe) |

| 6,613 |

| 7,400 - 8,600 |

| Working Interest Production (mmcfe) |

| 3,084 |

| 1,200 - 1,400 |

Thus, the company will see its aggregate production remain static year-over-year. However, the balance will shift toward higher profit production. Thus, we could very easily see a situation in which PHX Minerals' revenue goes down due to the lower natural gas prices but cash flow and profit do not fall nearly as much. This is nice, even though we may still see the company's cash flow decline, as we did over the past few quarters:

Seeking Alpha

The increase in the royalty production that is expected this year represents a continuation of the growth that PHX Minerals has seen over the past few years. Since switching to its royalties-only strategy in 2020, PHX Minerals has grown its royalty production at a 41% compound annual growth rate. Thus, we have a situation in which the company is managing to grow its cash flow even without production growth. That is something that will likely be critical this year as natural gas producers work to reduce production.

Financial Considerations

It is always important that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the maturing debt, which can cause a company's interest expenses to increase under certain market conditions. This is something that could prove especially important today as interest rates are currently at the highest levels that we have seen since 2007. Thus, any debt that is rolled over today will almost certainly cause a company's interest costs to increase. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. This could be an especially big risk for a company like PHX Minerals due to its exposure to volatile commodity prices.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. The ratio also tells us the degree to which the company's equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of March 31, 2023, PHX Minerals has a net debt of $32.3 million compared to a shareholders' equity of $110.1 million. This gives the company a net debt-to-equity ratio of 0.29 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| PHX Minerals |

| 0.29 |

| Northern Oil and Gas ( NOG ) |

| 1.67 |

| Diamondback Energy ( FANG ) |

| 0.44 |

| Viper Energy Partners ( VNOM ) |

| 0.30 |

| Coterra Energy ( CTRA ) |

| 0.13 |

Admittedly, not all of these companies are perfect peers for PHX Minerals due to its focus on collecting royalties rather than producing crude oil or natural gas. Northern Oil and Gas and Viper Energy Partners both use a very similar model though and as we can see, PHX Minerals compares fairly well to both of them. As such, it appears as though the company is using leverage judiciously and not exposing its shareholders to an excessive amount of risk. This is a good sign.

Another metric that we can use to evaluate the company's debt level is the leverage ratio, which is also known as the debt-to-adjusted EBITDA ratio. This ratio basically tells us how many years it would take the company to completely pay off all of its debt if it were to devote all of its pre-tax cash flow to this task. As of March 31, 2023, PHX Minerals had a leverage ratio of 0.9x based on its trailing twelve-month adjusted EBITDA. That is a reasonable ratio that is below the 1.0x that we usually like to see for companies like this. It is also the lowest leverage ratio that PHX Minerals has had in many years:

PHX Minerals

Thus, it appears that the company should be in reasonable shape with respect to its debt load as it is in line with most upstream companies, which are the most exposed to cash flow volatility caused by commodity prices of anything in the energy industry.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a crude oil and natural gas royalty company like PHX Minerals, we can value it based on the forward price-to-earnings ratio. This is a similar ratio to the familiar price-to-earnings ratio that basically tells us how much we would have to pay for each dollar of earnings that the company is expected to earn over the next year.

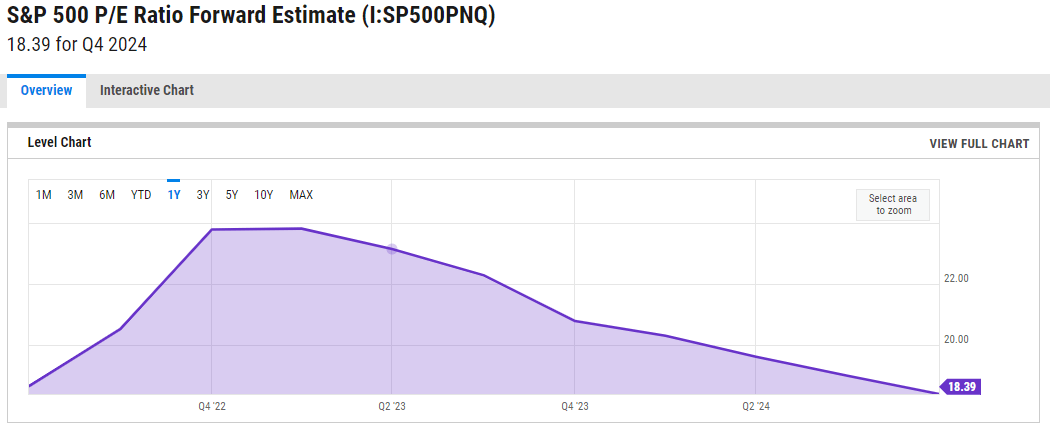

As of today, the forward price-to-earnings ratio of the S&P 500 Index ( SP500 ) is 18.39:

{kind=link}

As I have pointed out numerous times in the past though, pretty much everything in the traditional fossil fuel industry is substantially cheaper than the market as a whole. PHX Minerals is no exception to this. According to Zacks Investment Research , PHX Minerals has a forward price-to-earnings ratio of 9.80 at the current price. Here is how that compares to the company's peer group:

| Company |

| Forward P/E Ratio |

| PHX Minerals |

| 9.80 |

| Northern Oil and Gas |

| 3.88 |

| Diamondback Energy |

| 6.86 |

| Viper Energy Partners |

| 19.02 |

| Coterra Energy |

| 9.37 |

This is somewhat disappointing. Although PHX Minerals does appear to be substantially cheaper than the S&P 500 Index, it still looks to be somewhat expensive relative to its peers. As such, it may make sense to wait for a correction before buying shares of the company.

Conclusion

In conclusion, PHX Minerals is an independent crude oil and natural gas company with a unique twist in that it focuses on collecting royalties from wells drilled by other companies. This allows it to earn higher margins than many other firms in the industry, which could prove to be an advantage as energy prices remain low. The company appears reasonably priced relative to the market, although it is not a bargain in the already cheap energy sector. As such, it may make sense to wait for a correction. Fortunately, the correction may occur as the United States Treasury will be issuing about a trillion dollars' worth of new debt over the next month, forcing the sale of stocks in favor of Treasuries.

For further details see:

PHX Minerals: Play On Royalties, Not Production