PLTM - Physical Platinum: Favorable Supply-Demand Dynamics And Green Energy Potential

2023-05-29 04:48:02 ET

Summary

- The platinum market currently faces supply challenges, including production constraints in Russia and an energy crisis in South Africa.

- Demand is expected to grow, especially in the chemical and fuel cell segments.

- In 2023, platinum is expected to experience its largest deficit since the 1970s.

- Investing in physical platinum at current prices, such as through the abrdn Physical Platinum Shares ETF, could be an attractive investment opportunity.

- Considering current inventories and the potential impact of a recession, however, it may still be early days for platinum.

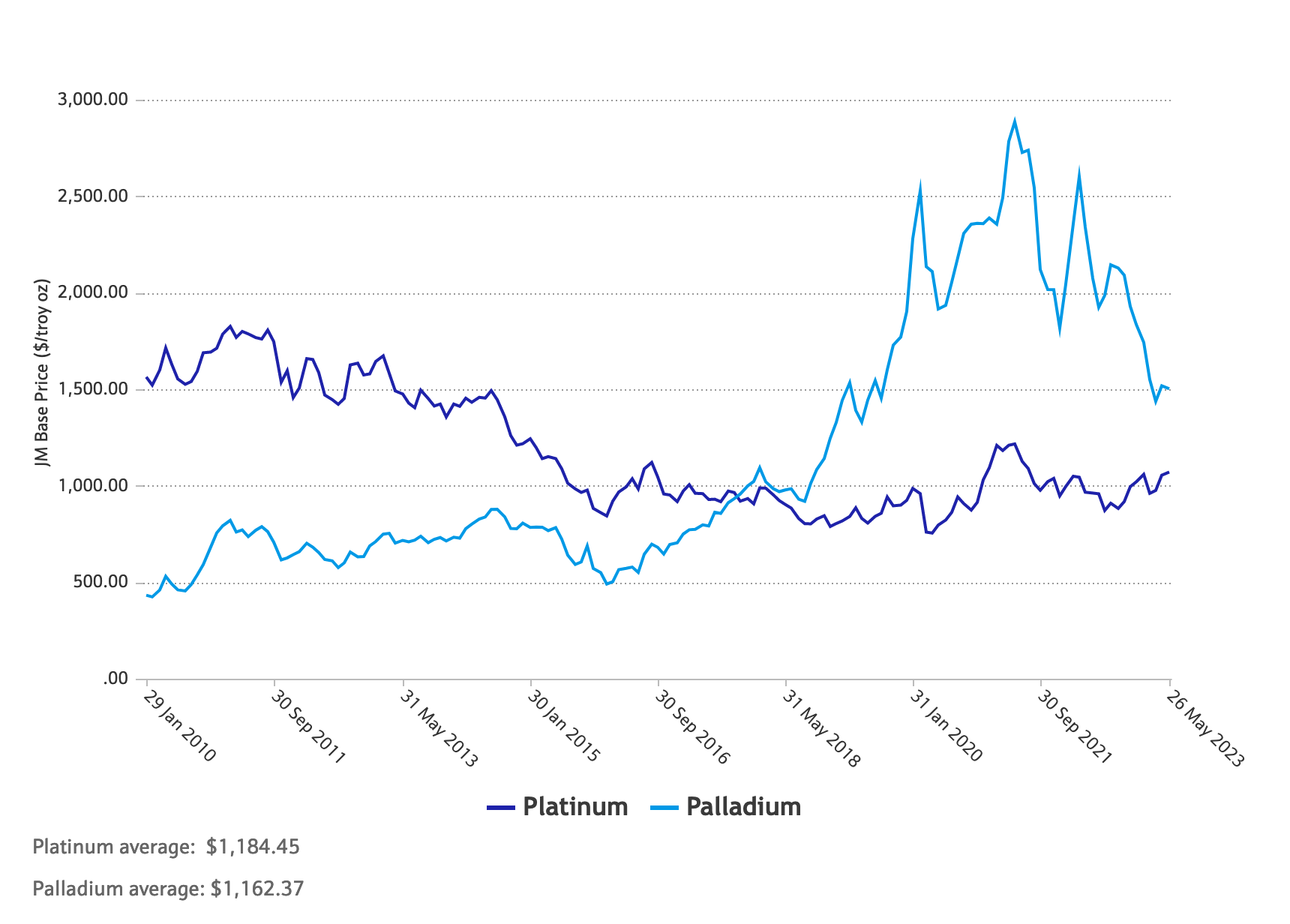

While often overshadowed by gold and silver, platinum-group metals have also emerged as promising investment opportunities. Palladium, for instance, experienced remarkable growth in the past decade. On the other hand, platinum prices have declined significantly over the same period of time.

Platinum and palladium historical prices from 2010 (matthey.com)

{kind=link}

The correlation between platinum and palladium prices is not a coincidence. These metals serve as substitutes for each other in the automotive catalytic converter sector, which accounts for approximately 40% of platinum demand and 75% of palladium demand. Historically, platinum was the more expensive metal, which led to palladium gradually surpassing platinum as the preferred choice for automobile manufacturers. As car production increased significantly, particularly in emerging economies, and emissions standards became stricter, the price of palladium soared.

Platinum still maintains a predominant role in diesel vehicles. However, in the past five years, the market share of diesel vehicles has declined due to stricter regulations imposed in Europe and Japan. Consequently, platinum has lost a significant portion of its market share to palladium in automotive applications. Furthermore, both metals' roles in the automotive industry have been challenged by the rise of electric vehicles (EVs), which do not require catalytic converters.

However, far from being a fading metal, platinum seems to have reached a multi-year low and could be poised for a rebound. The investment thesis for platinum is based on the assumption that industrial demand will remain strong while supply is likely to disappoint on the downside.

Despite the narrative of a diminishing role in the automotive sector, internal combustion engine ((ICE)) vehicles are expected to persist for a considerable period. In absolute terms, the number of ICE vehicles is projected to continue growing for years to come, driven by increased penetration in emerging markets where electric vehicles (EVs) are still likely to be prohibitively expensive. In developed countries, the transition from ICE vehicles to EVs is also likely to take longer than anticipated, particularly due to the high dependence of battery-based vehicles on metals that are costly to mine.

Automotive demand represents only a fraction of the total industrial demand for platinum. In addition to its use in the automotive industry, platinum finds applications in chemical manufacturing, petroleum refining, glass production, electrical components, and laboratory equipment. Its catalytic properties make it indispensable in various chemical processes, including the production of fertilizers, nitric acid, and, notably, hydrogenation reactions.

Platinum serves as a catalyst in hydrogen-based fuel cells, facilitating the conversion of hydrogen and oxygen into water to generate electricity. Consequently, platinum is set to play a significant role in the emerging green economy, such as powering electric vehicles through fuel cells. While battery-based electric vehicles are expected to dominate the EV market, it is worth noting that fuel cell electric vehicles require seven times more platinum per vehicle than their ICE counterparts.

Platinum's role as a green energy metal might only become prominent in the 2030s. In the near term, demand for chemical applications is likely to be the primary driver of demand growth. According to the recent Platinum Quarterly Report , released by the World Platinum Investment Council (WPIC), chemical demand increased by 108% (+123 koz) year-on-year to 236 koz in Q1 2023. This increase is mainly attributed to greater paraxylene demand, particularly in China, as well as an increase in propane dehydrogenation ((PDH)) demand.

Platinum also benefits from its status as a precious metal. Jewelry accounts for approximately one-third of platinum demand, and while this sector is the most sensitive to potential economic downturns and is experiencing a slow decline, it still consumes around 1,900 koz per year. Platinum also exhibits a positive correlation with gold, which explains its role as a safe haven asset.

Investment demand has been relatively small, averaging only a few percentage points in recent years. Moreover, net investment demand was negative in 2022 due to significant ETF disinvestments triggered by rising interest rates. However, as the current tightening cycle is expected to reach its conclusion soon, the investment case for all precious metals, including platinum, appears strong. ETF flows have already shown signs of reversal in the first quarter of 2023 (+43 koz).

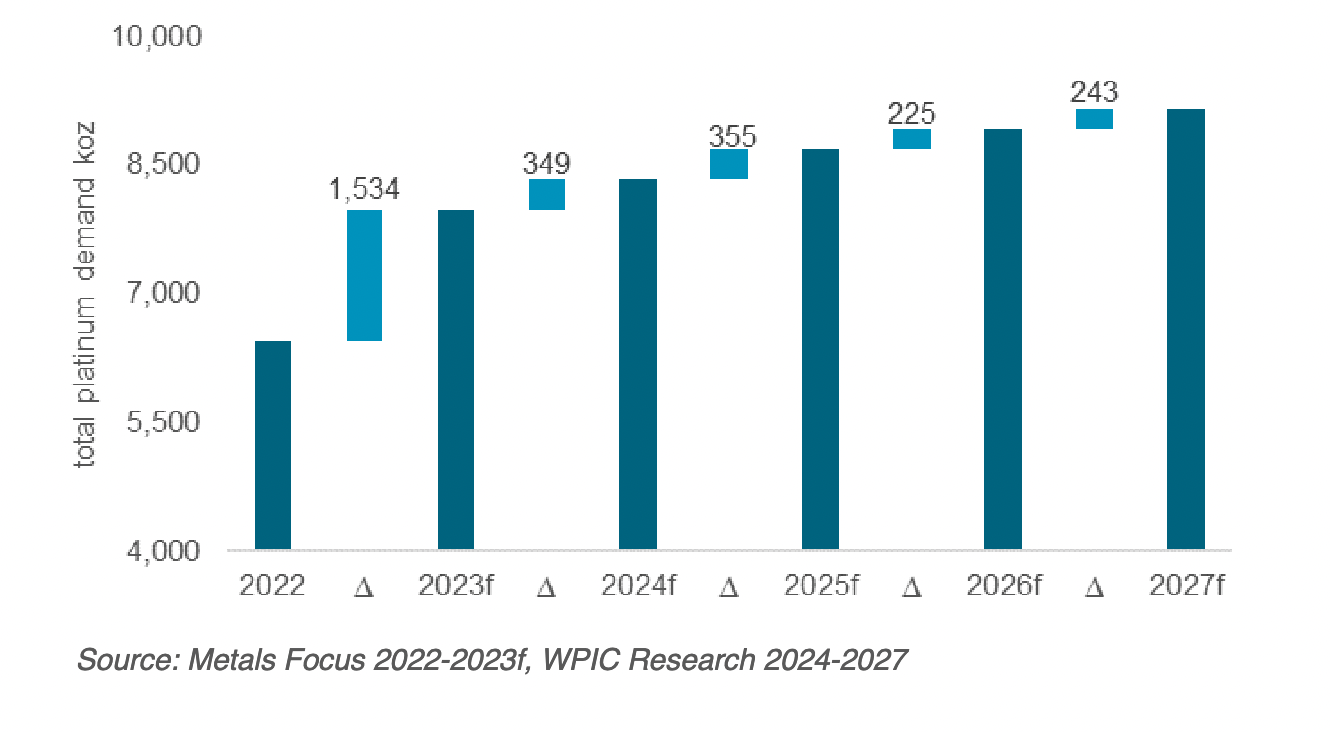

Overall, according to WPIC data, platinum demand will grow to approximately 9,000 thousand ounces by 2027, representing a 35% increase compared to 2022 levels.

{kind=link}

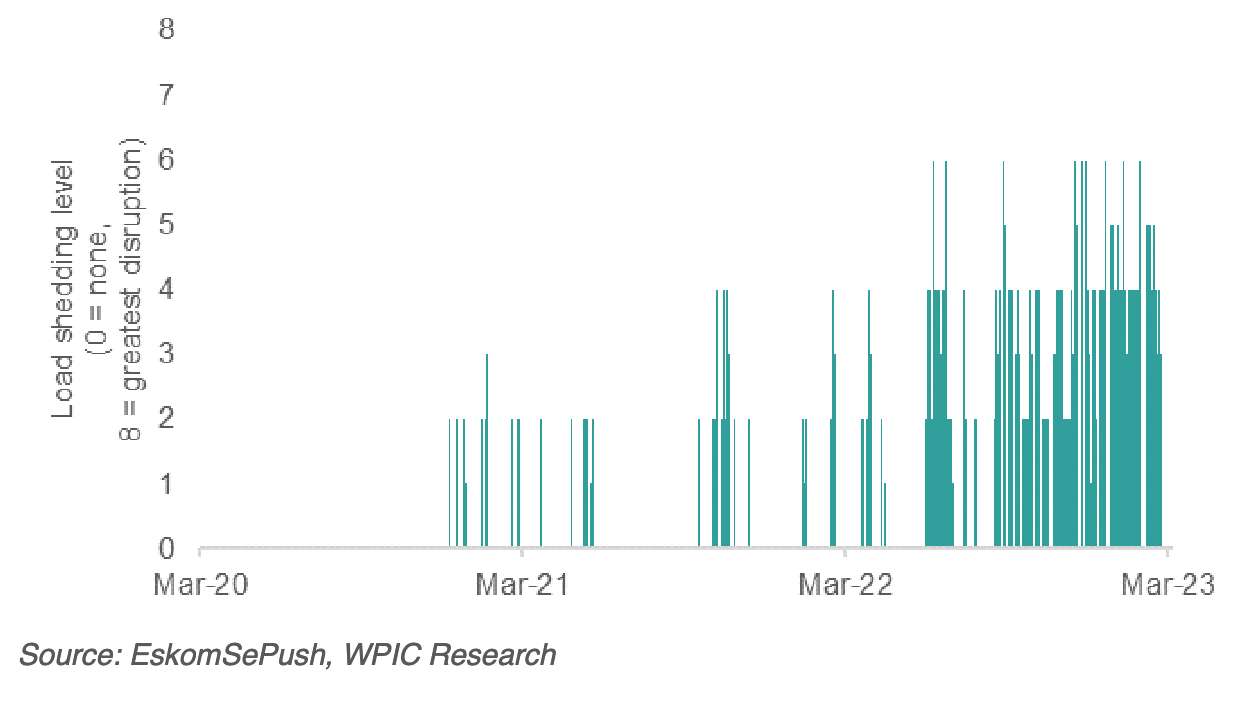

Platinum is also a supply story. Cracks have already emerged in platinum primary production, as evidenced by an 8% decline (-96 koz) in refined platinum production in Q1 2023 compared to the previous year. This decrease can be attributed primarily to South Africa, which experienced a 14% drop (-119 koz) due to ongoing processing constraints. Anglo American Platinum's Polokwane smelter, still not operating at full capacity following last year's rebuild, and maintenance activities at the Waterval smelter contributed to this decline. Additionally, the planned rebuild of Implats' Number 4 furnace impacted the company's output. The production of refined platinum has lagged behind mining production, leading to a buildup of semi-finished inventory. South Africa's energy crisis has further exacerbated this trend, affecting smelter availability due to load curtailments. The graph below illustrates the increasing frequency of load shedding by ESKOM, the South African state energy supplier, in recent months.

Increasing frequency of load shedding in South Africa (platinuminvestment.com)

{kind=link}

The likelihood of a supply shock in platinum, as well as palladium, is greater than for other metals due to their smaller production scale and high concentration in a few countries. Global production of platinum and palladium amounts to approximately 8,000 thousand ounces annually, whereas gold production stands at around 100,000 thousand ounces. The Bushveld Igneous Complex (BIC) in South Africa accounts for three-quarters of platinum mining production, with Russia being the second-largest producer (15%), and Zimbabwe, Canada, and the U.S. making up the remainder.

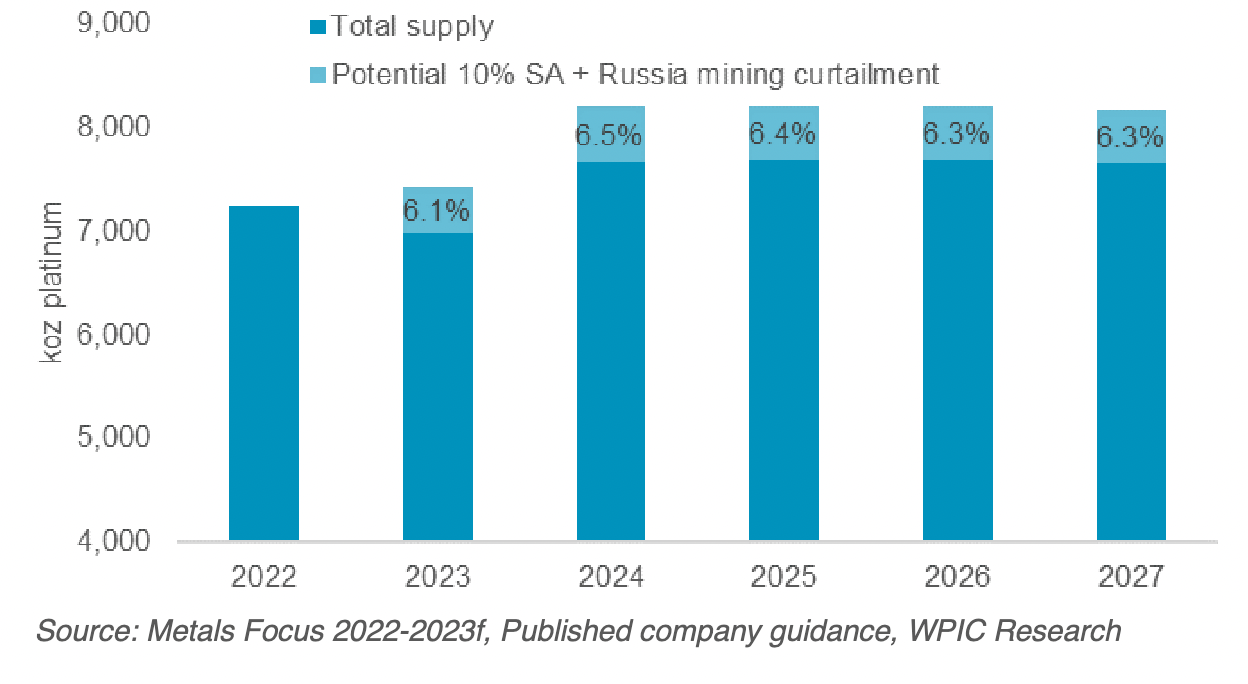

Mine production faces two risks: deteriorating operational conditions in South Africa and difficulties in procuring mining equipment and spares for Russian miners. South African producers' management commentary indicates potential production downside risks of 5% to 15% in 2023 alone. Norilsk Nickel has projected a production volume of 624 koz in 2023, which implies a 4.1% reduction compared to 2022. Given the current sanction environment, it remains uncertain whether Norilsk will be able to maintain production in the medium and long term. The WPIC is forecasting platinum mining to plateau in 2024, with the potential for a 10% production drop from Russia and South Africa.

Projected platinum supply from mining (platinuminvestment.com)

{kind=link}

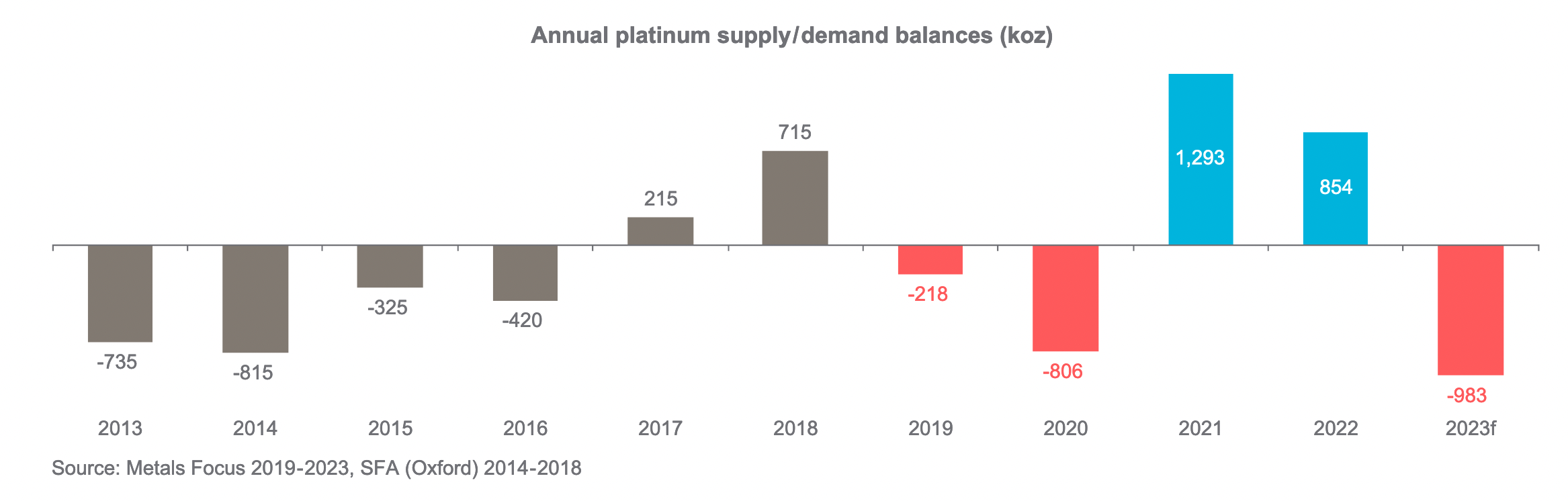

Over the past decade, the price of platinum has been depressed by declining industrial demand and large inventories. The graph below illustrates the supply/demand historical dynamics. Although the market experienced a deficit from 2013 to 2016, it managed to balance due to existing inventory. The market shifted to a surplus in 2017 and 2018 when the effects of palladium substitution and the declining market share of diesel vehicles began to be felt. A significant deficit was reported in 2020 due to curtailed mine production caused by COVID restrictions, but it transitioned to a surplus in both 2021 and 2022 as car production faced challenges related to COVID-related logistics and the global chip shortage. However, with industrial demand rebounding and mining production stagnating, the platinum market is expected to end 2023 with a deficit of 983 thousand ounces, the largest deficit since the 1970s.

{kind=link}

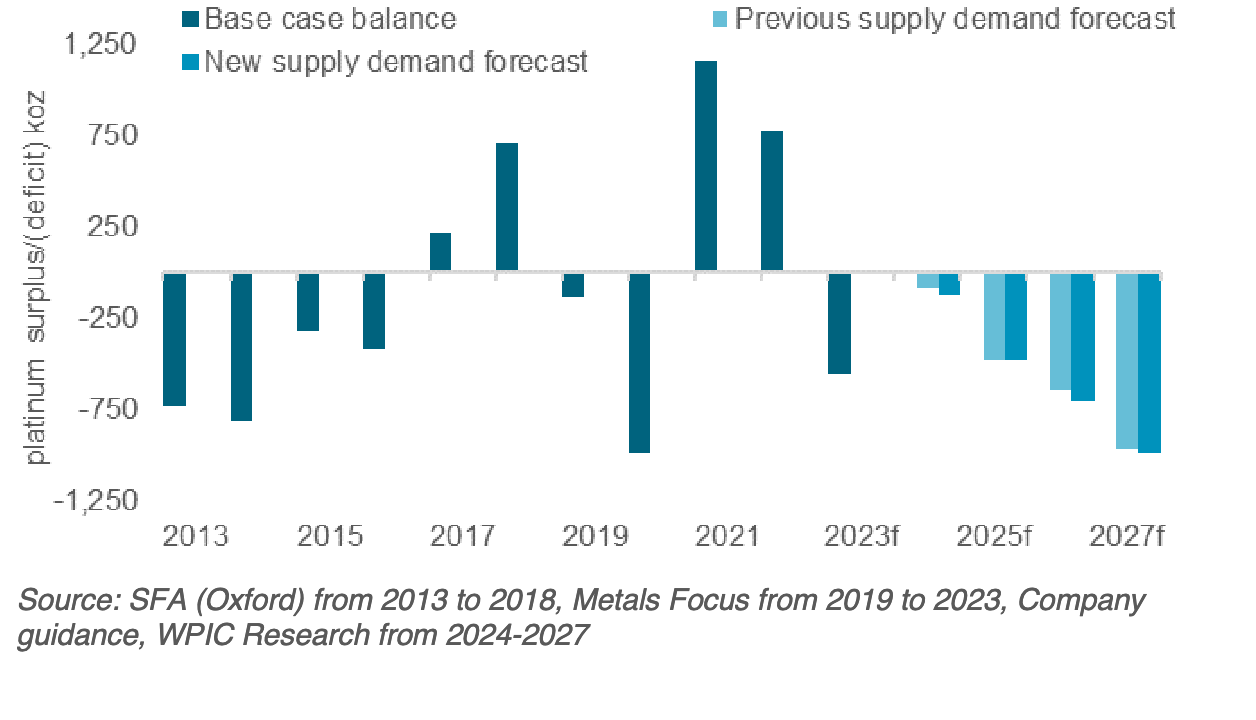

Furthermore, according to WPIC data, the market is projected to remain in a deep deficit until at least 2027. The deficit is expected to narrow in 2024 as new production comes online and a potential recession affects industrial demand, but it will start to deepen again by 2025.

Platinum expected deficit through 2027 (platinuminvestment.com)

{kind=link}

There is a case to be made for investing in the physical metal itself rather than miners. This is because most producers are exposed to South Africa or Russia. Despite having lower leverage, the physical metal may outperform miners.

One option for investors seeking exposure to physical platinum is the abrdn Physical Platinum Shares ETF ( PPLT ), an exchange-traded fund. PPLT is designed to track the price performance of platinum, net of expenses, which amount to 0.6% per annum. It offers a more cost-effective, convenient, and liquid investment vehicle compared to physical coins and bars. Unlike other ETFs that can hold derivatives, PPLT is fully backed by actual physical platinum bars. The ETF ensures transparency by holding allocated bars, and a daily bar list is available on the abrdn.com/usa/etf website. The platinum bars are securely stored in vaults located in London, UK, and Zurich, Switzerland.

In conclusion, given the platinum market's sustained structural deficits, limited supply, and positive demand outlook, investing in platinum at current prices provides an attractive investment opportunity. However, it is important to note that the supply/demand imbalance will take time to push prices higher. WPIC data indicates that significant inventories still exist, with above-ground stock estimated to be around 3,790 koz by the end of 2023, which exceeds the cumulative projected deficits until 2027. Moreover, since platinum is predominantly an industrial commodity, a potential recession in the Western world could impact demand in the short-term. While I believe platinum is positioned for significant appreciation over the current decade, this growth story is more likely to unfold toward the end of the 2020s, when inventories are depleted and the green energy transition is fully underway.

For further details see:

Physical Platinum: Favorable Supply-Demand Dynamics And Green Energy Potential