DOC - Physicians Realty Trust: A Good Doctor Against Market Volatility

Summary

- Physicians Realty Trust owns a portfolio of medical office buildings that are leased to highly rated tenants under triple-net leasing arrangements.

- Shares in the stock have remained remarkably stable over the past year, down just over 5%, while broader markets swing between large gains and losses.

- In addition to share price stability, the stock offers investors a 5.5% yielding dividend. This can produce some positive performance in a market otherwise marked with double-digit declines.

- For risk-averse investors, DOC is a safe buy, but it is certainly not a generational buy for those seeking more opportunistic additions to their long-term portfolios.

Physicians Realty Trust ( DOC ) is a real estate investment trust ("REIT") that owns a portfolio of properties that are leased to physicians, hospitals, and health care delivery systems under triple-net leasing arrangements.

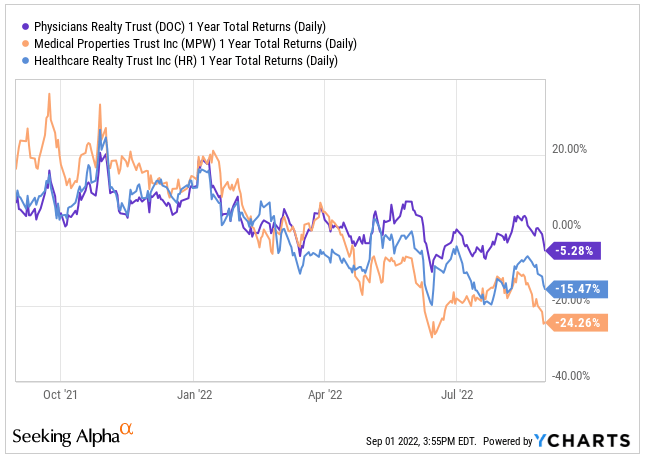

Operationally, they are similar to many other peers in the sector, such as Medical Properties Trust ( MPW ) and Healthcare Realty Trust ( HR ), to name two. But over the past year, the company has been the more stable peer, with shares down just over 5% versus double-digit declines in both MPW and HR. DOC is also fairing better than the overall S&P 500 , which is down about 12% on the year.

YCharts - 1-YR Returns of DOC Compared To Peers

{kind=link}

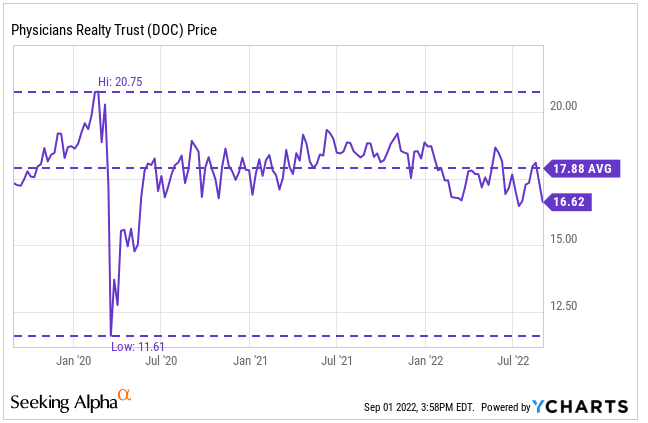

In fact, shares in the stock have barely moved since rebounding from their early 2020 lows, with just over $3 separating their 52-week range.

YCharts - Recent Share Price History of DOC

{kind=link}

For investors seeking to protect their principal from the recent market rout, DOC would make for a satisfactory portfolio holding. Though upside is limited, shares do offer a bond-like dividend payout, which is currently yielding approximately 5.5%. For other, more risk-tolerant and opportunistic investors, however, DOC is at most a mediocre investment, with recent earnings that were solid but free of any clear catalyst to send shares meaningfully higher.

DOC Has A Geographically Dispersed Portfolio With A Quality Tenant Base

DOC's portfolio includes just under 300 properties, nearly all of which are medical office buildings ("MOB") on the campus of a hospital or strategically affiliated with a health system. These properties are dispersed throughout the U.S in 33 states, primarily on the eastern half of the country. Some of their top markets include Georgia, Arizona, and Texas, which collectively account for just over a quarter of total annualized base rents ("ABR").

June 2022 Investor Presentation - Map of Geographic Concentration

Tenant diversification and quality continues to be a source of strength for DOC, with no single tenant responsible for more than 5% of ABR. This contrasts with MPW, who has several high-profile operators , such as the Steward Health Care System, that account for a significant share of their total revenues, exposing them to greater tenant default risk.

DOC's tenants also have superb credit ratings, with 65% of the portfolio covered by investment-grade tenancy. This is an improvement over the 62% reported in 2021 , due in part to their recent sale of their Great Falls Hospital holding, one of the lower quality assets on their books. Although it is noteworthy that the facilities were sold at a 4.7% disposition cap rate after having been acquired at a 7.9% rate. So, while it was not the highest quality asset on their books, it was still an accretive investment with a successful exit.

Tenant Credit Quality Enables DOC To Drive Rents With Confidence

The diversified portfolio of highly rated tenants not only provides vital downside protection, but it also enables the company to comfortably drive rents knowing that their base is capable of absorbing the escalations. As it is, 98% of their portfolio is insulated from increased operating expenses due to built-in provisions . While this is common in the sector, DOC's ratio compares favorably to peers, whose portfolios are only 80% covered, in the case of HR.

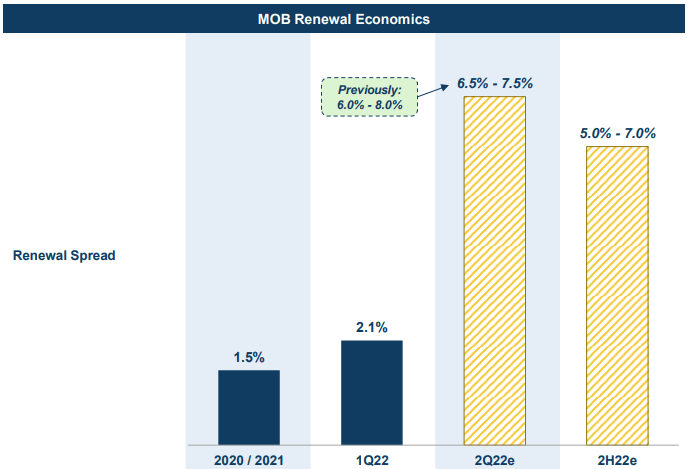

In addition to annual escalations, DOC is also posting healthy leasing spreads. In the current quarter, management reported 8% spreads on over 250k square feet ("sqft") of renewals. These spreads were the highest quarterly mark in the company's history. And they were largely preserved on an effective basis, as tenant improvement and incentive packages came in much lower than industry averages.

Q2FY22 Investor Presentation - Graph of Growth In Renewal Spreads

{kind=link}

Looking ahead, however, spreads are expected to moderate to between 5-7% due to rising construction costs. Still, that is high by their historical standards and should be one continued driver of internal growth in subsequent periods.

The continued rental growth would be on a leased and retention rate of 95% and 76%, which is in-line with long-term MOB averages. In addition, the company has about 100K square feet of signed but not yet commenced ("SNO") leases that are currently weighing on same-store ("SS") occupancy, but are expected to add nearly 3% upon commencement. This is also expected to improve SS net operating income ("NOI"), which came in shy of estimates in the current period.

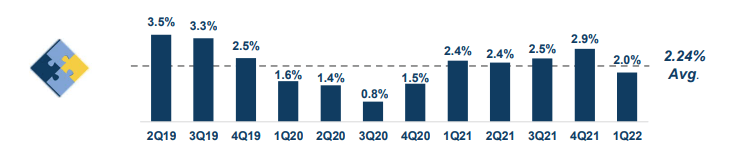

Though funds available for distribution ("FAD") were up 11% from last year, SS cash NOI was up just 2%. This was lower than every quarter in 2021, and it lags their historical average of 2.24%. Rising expenses is one aspect of this. But a more important driver is their SNO pipeline. If those leases were commenced and paying, SS NOI growth would have been 2.8%, which is more in-line with expectations.

June 2022 Investor Presentation - Same-Store Cash NOI Trends Since Q2FY19

{kind=link}

Some Limiting Factors On Future Growth

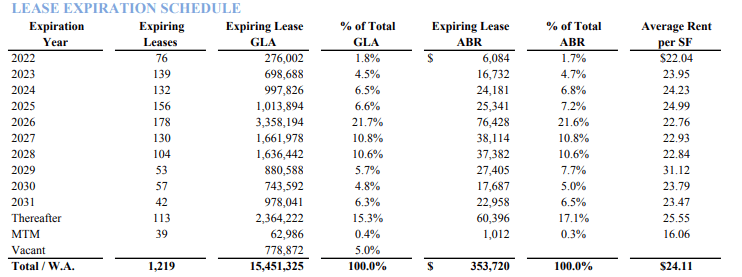

Longer weighted average lease terms ("WALT"), about six years for DOC, provides a sense of security to cash flows. But it does limit the rental markup opportunity to annual escalations, which may be lower than the growth in market rents. In addition, their lease expiration schedule is weighted more heavily towards later years. While a positive for safety, it is a draw on growth.

Q2FY22 Investor Supplement - Lease Expiration Schedule

{kind=link}

Given current market conditions, the environment continues to be marked as one of price discovery, with participants still hugging their corners as they assess valuations against their cost of capital, the economics of which have been scrambled by recent rate changes.

DOC, nevertheless, maintained their full-year investment guidance of +$250M. But it would be prudent to exercise some degree of skepticism on this, not because of their financial position but because of widening bid/ask spreads between market participants that could ultimately derail a deal that would have otherwise closed under normal operating conditions.

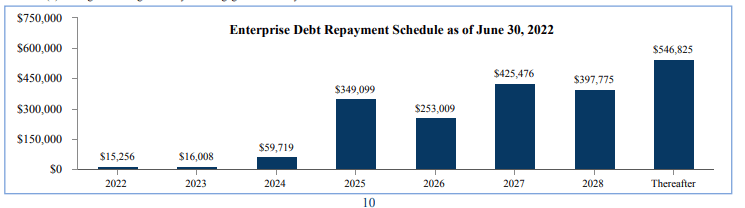

Well-Laddered Debt Maturities And A Stable Dividend Payout

DOC does have the flexibility to capitalize on new opportunities in the future, with total liquidity of over +$700M and no significant debt maturities until 2025.

Overall, their total debt burden represented just over 30% of their capitalization and about 5.65x adjusted EBITDAre from a net debt perspective. This is a conservative position to be in and one that faces few repayment risks.

Q2FY22 Investor Supplement - Debt Maturity Schedule

{kind=link}

The company is also comfortably in compliance with their debt covenant ratios and boasts of an investment-grade credit rating from all three agencies. This should provide them readily available access to capital when the time comes to roll over their obligations.

For income investors, the stock comes with a quarterly dividend of $0.23/share, which represents an annualized yield of approximately 5.5% at current pricing levels. From a safety standpoint, it accounts for about 85% of FFO and 88% of FAD. Though covered, it doesn't provide much room for further growth. In fact, the payout has been flat since 2017, when it was last at $0.225/share . For a growth investor, this isn't very appealing. But the relatively higher yield and safety does offset some of that disappointment.

Not A Generational Buying Opportunity

DOC owns a stable portfolio of MOBs that are leased to a large group of investment-grade tenants. The credit quality of the tenants is one strength that differentiates them from their peers. It also provides an enhanced degree of stability and predictability to their reoccurring cash flows and enables them to drive rents with the confidence that their operators could absorb the increases.

These increases include not only built-in escalation provisions but also renewal spreads that are at the highest quarterly levels in the company's history, 8% in the most recent filing period. Strong occupancy and high retention rates should also provide a continued runway for earnings growth.

Favorable industry fundamentals that include significant growth in nationwide health care spending due to an aging population and expected increases in life expectancy will further support demand for DOC's properties.

For risk-averse investors, DOC makes for a great portfolio holding. Its shares have traded in a tight 52-week trading range with just over $3 separating their highs and lows. The limited volatility in the shares would have offered investors valuable reprieve over the past several months, given the volatility in the broader markets. Granted, shares are still down 11% YTD. But compare that to their related peer, MPW, who is down nearly 40%.

For more opportunistic investors seeking to capitalize on the current market turmoil, however, DOC is not a stock that provides a generational opportunity. Its steady 5.5% yielding dividend is one draw, but there are higher yielding payouts elsewhere. Investors aren't likely to miss the lock-in opportunity on the yield, either, given the unlikeliness of a material run higher. With a multitude of alternatives in the current market environment, DOC offers safety through stability but not much else.

For further details see:

Physicians Realty Trust: A Good Doctor Against Market Volatility