DOC - Physicians Realty Trust: An Adequate Hedge Against Market Volatility But Limited Upside Potential

2023-03-21 06:57:38 ET

Summary

- Physicians Realty Trust has an interest in a diversified portfolio of nearly 300 healthcare facilities.

- Their operating income is generated mostly from medical office buildings net leased to a high percentage of investment grade tenancy.

- In addition to share price stability, DOC stock offers investors an attractive dividend payout with a current yield in excess of 6%.

- Shares, however, appear fairly valued and have limited runway for further growth from current levels.

Physicians Realty Trust ( DOC ) has an interest in nearly 300 healthcare properties, located across 32 states.

Nearly all their net operating income (“NOI”) is derived from medical office buildings (“MOB”) that are leased to a high percentage of investment grade (“IG”) tenants. At the end of 2022, about 67% of their NOI was derived from IG tenancy .

Similar to other healthcare REITs focused on MOBs, DOC is well positioned to capitalize on favorable long-term demand trends. This includes a rapidly aging population and increasing demand for outpatient venues.

At occupancy levels hovering in the mid-90% range, DOC’s portfolio reflects both the continuing demand for their properties and the quality of their tenant base.

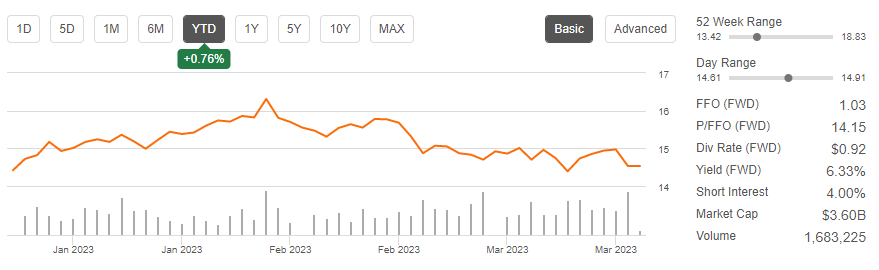

For investors, shares offer refreshing stability. The spread between their 52-week highs and lows, for example, is just under $5.50/share. In addition, the company currently provides a quarterly payout that yields about 6.2% at current pricing.

{kind=link}

Seeking Alpha - Basic Trading Data Of DOC

While the relative stability and dividend payout may lure some to new positioning, the stock lacks significant upside potential. 2022 results exhibited strength, but management did little to excite in their outlook for 2023. Current implied cap rates are also in-line with what one would expect in the sector. And for income investors, a high payout ratio limits the growth potential of the dividend. While the stock can be an adequate holding to hedge against market volatility, in my view it doesn’t provide significant value, otherwise.

Recent Results and Current Portfolio Metrics

In Q4 of fiscal 2022, DOC generated normalized funds from operations (“FFO”) of $0.26/share and normalized funds available for distribution (“FAD”) of $0.24/share. This was up about 5.4% over the same quarterly period last year, bringing their full year gain to 10.6%.

At year end, their total portfolio had a leased rate of 94.9%, up slightly on a YOY basis. Retention also held strong at 77%. Furthermore, during the year, they increased the amount of space leased to IG quality tenants to approximately 67% from 65% previously.

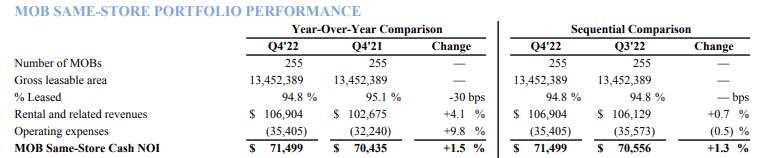

During the quarter, their MOBs recorded YOY same-store cash NOI growth of 1.5%. This came in below their historical growth rate of 2% to 3% due to a 30 basis point hit from vacancies at two primary locations, one at a MOB in Minnesota that was not renewed for strategic purposes. And the other at a facility in Pennsylvania due to tenant relocation. Barring these two assets, same-store NOI growth would have been 2%.

{kind=link}

Q4FY22 Investor Supplement - Summary Of Same-Store Cash NOI On YOY And Sequential Basis

In addition to the move-outs, operating expenses (“opex”) also weighed heavily, up 9.8%. It is worth noting, however, that the increase was driven by a +$1.2M incremental impact from one time insurance costs. Additionally, due to the nature of their leases, which are primarily triple net, the increase was offset by a 10.3% increase in recoveries.

Though the YOY increase missed expectations, they still logged sequential growth of 1.3%.

Overall, the company executed over 1M SF of leasing during the year. This includes over 800K SF of renewals at an average spread of 6%. And for more than 60% of the leases executed during the year, they had, on average, an annual escalator of 3% or greater.

Looking ahead, management sees renewal spreads in the mid-single-digits for 2023. This compares favorably to long-term MOB industry expectations of 2% to 3%. Additionally, they expect retention to remain within their historical targets of 75%.

On the financial side, general and administrative (“G&A”) expenses are expected to be up 4.5% at the midpoint. Additionally, capital expenditures (“capex”) is expected to be up about 5% at a midpoint of +$25M.

Liquidity and Debt Profile

During Q4, DOC utilized their at-the-market (“ATM”) program to realize +$74.3M in proceeds via the issuance of 5M shares at a weighted average price of $15/share. They further utilized the program early in Q1FY23 for net proceeds of +$65.8M.

The company also remains active in capital recycling. In the middle of 2022, for example, they disposed of three MOBs in Montana for total proceeds of +$116M, representing a cap rate of 4.7%. They then closed on an +$81.5M acquisition in September at an initial cap rate of 5.5%.

Subsequent to year end, DOC acquired a medical condominium unit in Atlanta and a parcel of land in Arizona for a total purchase price of +$2.1M. This was paired with the disposal of a 30K SF MOB for total proceeds of +$2.6M

In addition to these ongoing recycling efforts, the company also has an extensive development pipeline. At present, there are more than +$200M at cost of opportunities under evaluation. At the date of the release, management had expected to move forward on many of the opportunities and were expecting stabilized project yields in the 7% to 8% range.

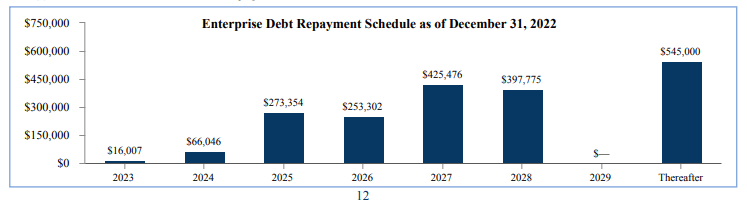

A sizeable liquidity position of over +$800M, comprised mostly of the availability on their revolving facility, and a manageable debt profile with a rated balance sheet and an accommodative debt ladder provides confidence that the company can meet all their reoccurring short and long-term obligations.

{kind=link}

Q4FY22 Investor Supplement - Debt Maturity Schedule

Dividend Safety

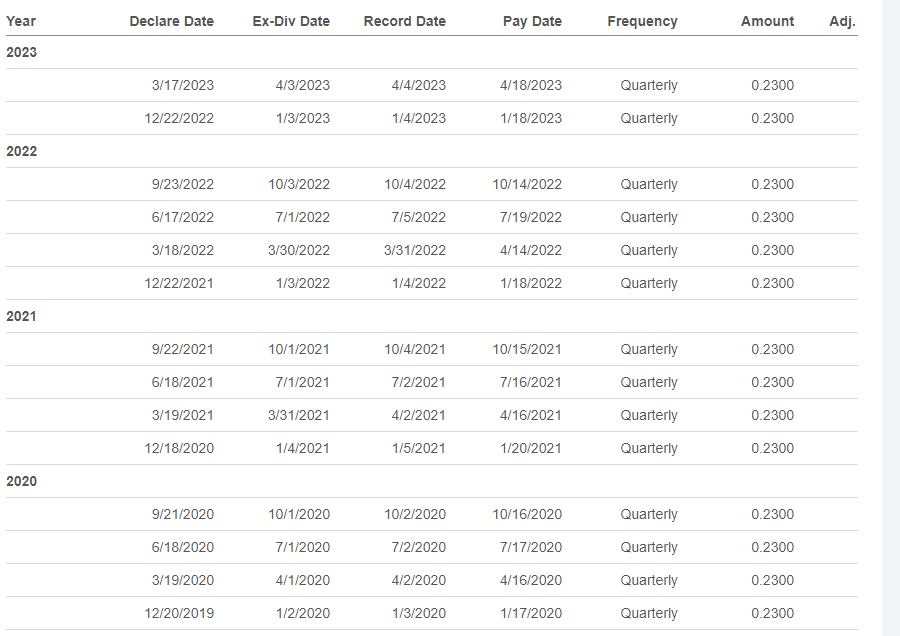

DOC currently provides a quarterly payout of $0.23/share. At current trading levels, this represents a yield of about 6.2%.

The payout has lacked growth through the years, but it has remained stable.

{kind=link}

Seeking Alpha - Dividend Payout History From 2020 To Present

On a yearly basis, DOC is generating about +$245M to +$260M in operating cash flows and is retaining over +$200M in free cash flow (“FCF”). In 2022, they paid out about 95% of FCF in dividends. And that is likely to continue moving forward.

In relation to FAD, the payout is tracking high, at over 90% of estimates. This leaves little room for growth in the dividend, and it does expose them to a higher risk of a future cut/suspension. The company does, however, benefit from strong debt coverage levels and a more favorable burden on tenant improvement costs in relation to their peers. This mitigates some of this risk.

Final Thoughts

A distinguishing characteristic of DOC’s portfolio is their exposure to IG tenancy. And in 2022, the company increased their exposure to 67% of their portfolio from 65% previously. This is significantly greater than their peers, whose exposure typically tracks in the mid-40% range, in the case of Healthcare Realty Trust ( HR ) and Healthpeak Properties ( PEAK ).

The retention of a quality base has enabled DOC to hold occupancy levels in the mid-90% range, which, too, is competitive against their peer set. Additionally, it has enabled the company to drive rents via renewal spreads and their annual escalators and expense recoveries, which also runs higher their peer group.

Their current leasing structure, for example, enables them to recover nearly 85% of their operating expenses. This is well above the peer average of about 65%.

While DOC continues to maintain favorable operating metrics, there wasn’t a lot to get excited about on their most recent earnings release. The company turned in strong full-year results but didn’t convey much excitement into the outlook, especially with regards to the transactional market, which continues to be marked with price discovery challenges.

At the end of 2022, the company traded at an implied cap in the mid-6s. They’ve since compressed slightly since then but not by much. And based on management commentary during their earnings release, this is about what transactions are currently fetching in the market.

The company utilized their ATM at a weighted average price in the $15/share range. This isn’t too far off current trading levels. Shares also appear fairly valued based on their current trading multiple of 14x forward FFO. Though the stock comes paired with a dividend payout yielding in excess of 6%, the payout is elevated in relation to available funds. At the very least, this is likely to keep a ceiling on any future hikes in the dividend.

For investors, I view DOC as an adequate hold. But there is not enough conviction for me for new or further initiation.

For further details see:

Physicians Realty Trust: An Adequate Hedge Against Market Volatility But Limited Upside Potential