DOC - Physicians Realty Trust Is Much Safer Than It Looks

2023-06-28 04:23:08 ET

Summary

- Physicians Realty Trust has a stable and safe investment profile, with a focus on outpatient transition in healthcare and investment-grade tenants.

- Despite recent trends not impacting the company's safety, its projected FFO growth remains low, raising questions about its valuation in an inflationary environment.

- DOC outperforms competitors in terms of fundamentals, with low debt and strong tenant performance monitoring, making it an attractive long-term investment option.

Author's Note: This article was published on iREIT on Alpha back in early/mid June of 2022.

Dear subscribers,

I covered Physician's Realty Trust ( DOC ) on iREIT on Alpha, our private investing group, a few months back. Since that time, the company hasn't really moved much in a positive way that would endear investors - and there are reasons for this, as I see it. In this article, I'm going to clarify those reasons for you and make sure that you understand what you're investing in when you're buying DOC.

I also want to make sure that you understand that when you "BUY" DOC, you're buying something potentially much better than you might expect in terms of stability and safety.

Let's review and recap on DOC, and see what we can expect out of the company on a 3-year forward basis.

Is DOC still the future of healthcare?

DOC hasn't been a superb investment - but then again, what a company does in 5-7 months really isn't indicative to me, unless something major that impacts company fundamentals has occurred. Nothing like that has occurred with DOC.

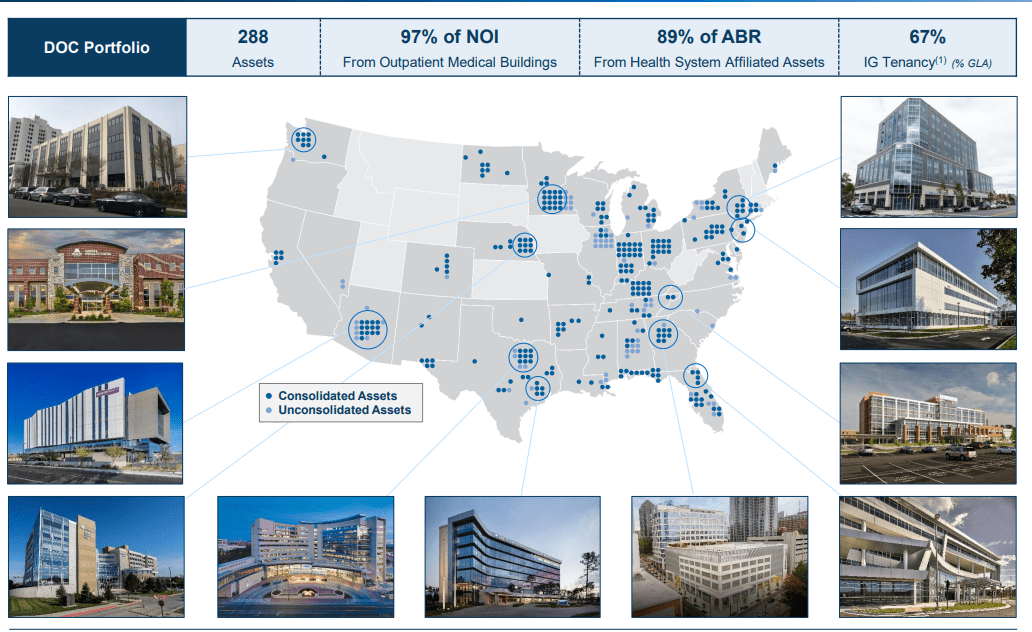

DOC markets itself as a portfolio containing "The future of healthcare". It manages nearly $6B worth of real estate portfolio spread into 291 properties, leased with a 93%+ occupancy rate with a 65% investment grade tenancy.

So, that's not bad. And while 5-year returns are looking bad, the company's portfolio growth since the IPO more years than has been excellent. If square footage was somehow a proxy for RoR, we'd be golden here.

DOC IR (DOC IR)

But the healthcare space is obviously notoriously fickle and risky. That's why my investments in the space have been sparse over the past 24 months. I do think that every sector has its quality participants though, and if you manage to identify them, you're in for profit.

The company targets investment-grade tenants occupying the best assets in the industry, with a focus on outpatient transition in terms of care. The REIT compares favorably in terms of same-property Cash NOI growth rates and has one of the best landlord expense protections in the industry.

The company is geographically diversified, with a focus on the eastern part of the US - less on the west. The top geographies are Atlanta, Phoenix, Dallas, Louisville, and Minneapolis. All excellent geographies, and what little there is on the coasts in riskier areas still are outweighed by what I would view as quality geographies.

{kind=link}

DOC IR (DOC IR)

Top tenants for DOC are Comonsprit, Northside Hospital, and University of Louisville Health. The top tenant has a 5% of ABR and is BBB+ rated.

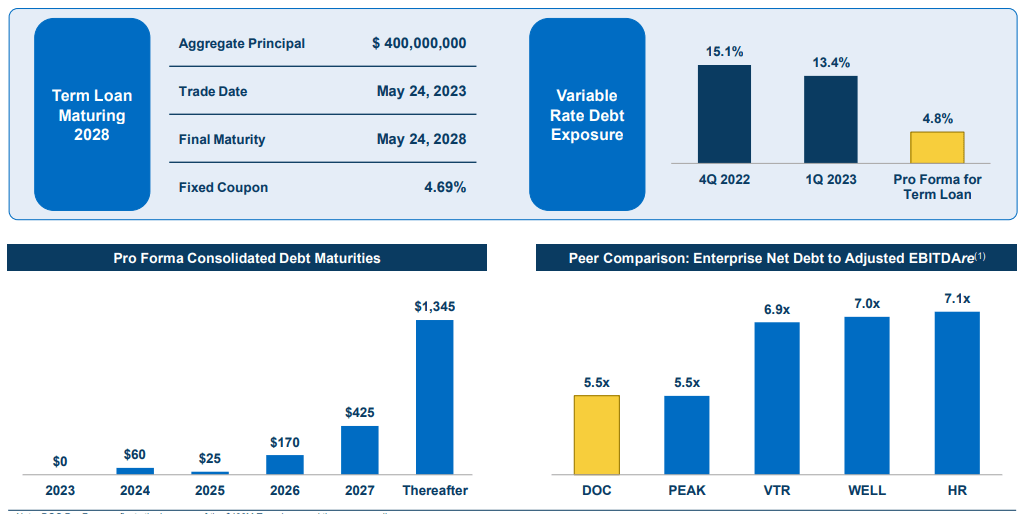

The only unrated in the top 10 is Northside Hospital, and together we have around 27-28% of annual ABR - a good diversification, all things considered, and with the credit ratings included. In terms of DOC debt, we're also in very good shape. DOC has a BBB rating and has a very attractive debt maturity - virtually nothing before 2025, and then it's just the revolver. Most of the company's notes aren't due until 2027 and beyond.

The advantages of DOC include growing much slower and safer than some of its far higher-risk peers, namely Medical Properties Trust ( MPW ). I'm in no way against MPW, I am a shareholder, but I don't fool myself into thinking that MPW is less risky than it actually is. MPW has risk - DOC has far less. The company's credit rating history attests to this.

DOC IR (DOC IR)

Recent trends haven't really, as I see it, put a dent in this company's safety either. The trends in the healthcare landscape remain favorable, even if the company's projected FFO growth does not. That's part of the main issue we'll revisit in valuation. How do you value a REIT that does not provide more than 1-2% FFO growth in a 4-9% inflation environment, with a 6% yield?

More on that later.

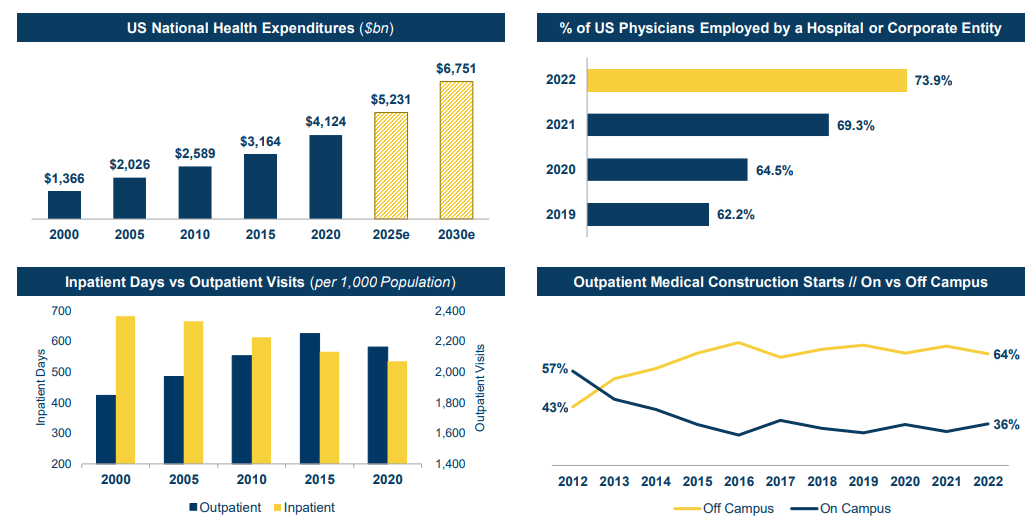

The trends for the entire landscape remain positive because the industry is in a position where DOC is well-positioned long-term to take advantage of a rising population and the consolidation of providers.

{kind=link}

DOC IR (DOC IR)

In fact, the company's entire portfolio was built with a focus on high-acuity specialists providing stability to the portfolio. Most of DOC, over 50%, is what is known as "Tier 1". What is Tier 1?

It's ambulatory surgery, cardiology, radiology, oncology, and Orthopaedics. What do these things have in common? They have the most significant tenant investment required, compared to Tier 3 which is only 23% of ABR. What we find here is things like Dentistry, Dialysis, and Podiatry. These things are in no way unimportant - but they have the lowest acuity, have limited referral networks, and can work with less investment. In a neighboring town, there's a dentist's office crammed in between two mechanics shops - and he's a good dentist, from what I've heard.

What I'm saying is you won't find a radiology lab/asset placed the same way. That's the point.

So, DOC knows what they're doing in the space. And whenever I find people who I have a conviction in "knowing what they're doing", I'm positive.

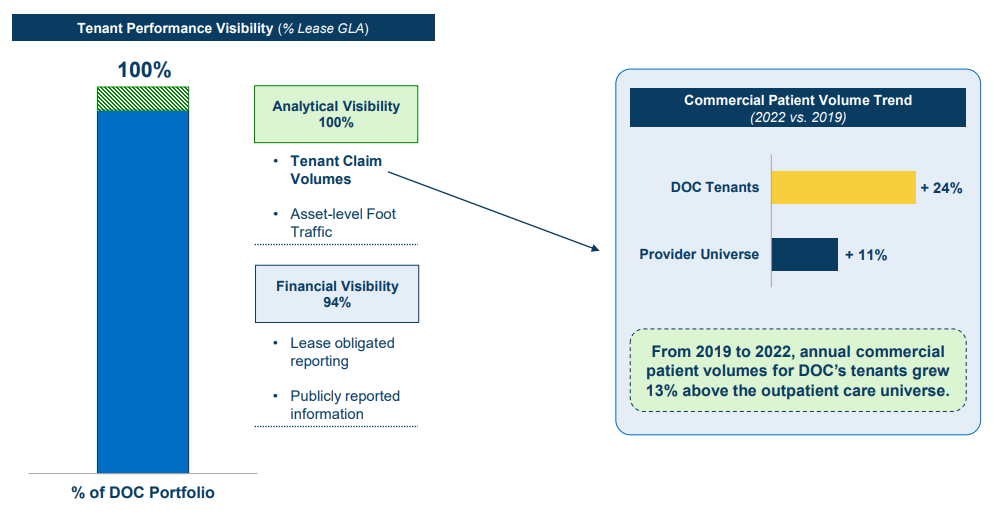

DOC is also very stringent to monitor tenant performance - and they do this with all of the company's tenants.

{kind=link}

DOC IR (DOC IR)

DOC is one of the few companies in the space, together with Healthcare Realty ( HR ), that delivers above 100 FAD/share history from 2016. And in the comparison here, we're looking at companies like Welltower and Ventas - in no way small or insignificant. But DOC is outperforming them - at least over the past 5+ years.

Renewal spreads for the company are more "in the air" than we might be used to. DOC managed 6% in 2022 - for the next 2 years, they're estimating between 5-7%, with the latest quarter showing a decline of 0.7% - not exactly positive - but much of this was from a single re-leasing that dragged down an otherwise strong quarter. Still, if we see more trends like this, we should expect numbers around that 5%, which is a further argument for why the company perhaps should be valued somewhat lower.

Where DOC still shines though, is fundamentals. DOC has some of the lowest debt to any company in this field, and it's far in the future.

{kind=link}

DOC IR (DOC IR)

So - with those things out of the way, and it is clear that the company in many ways is an outperformer that hasn't really outperformed in terms of FFO in the last few years, let's take a closer look at the current company valuation for DOC.

For the last quarter, results were unexciting - and unexciting is good because it implies stability, which DOC actually offers. FAD on a normalized basis was up 3% and came to nearly a quarter per share for the quarter. There was a consistent increase in same-store NOI at 1% portfolio-wide, which is below expectations overall, but good considering the times - and the company expects this to improve over the back half of the year as properties start rolling back online.

What we should keep an eye on are the renewal spreads - DOC is one of the few REITs I've covered here that show negative releasing spreads, but this was primarily due to one negative lease - so its not yet a pattern. In fact, the company observes that its rents are below current market rates, which implies additional pricing power on releasing and new leasing. The company allocates capital on a conservative and slow basis - this sort of approach is what i want to see, and it leads me to my positive view on the 1Q23 results, looking forward to 2Q23.

DOC - The valuation is starting to look better

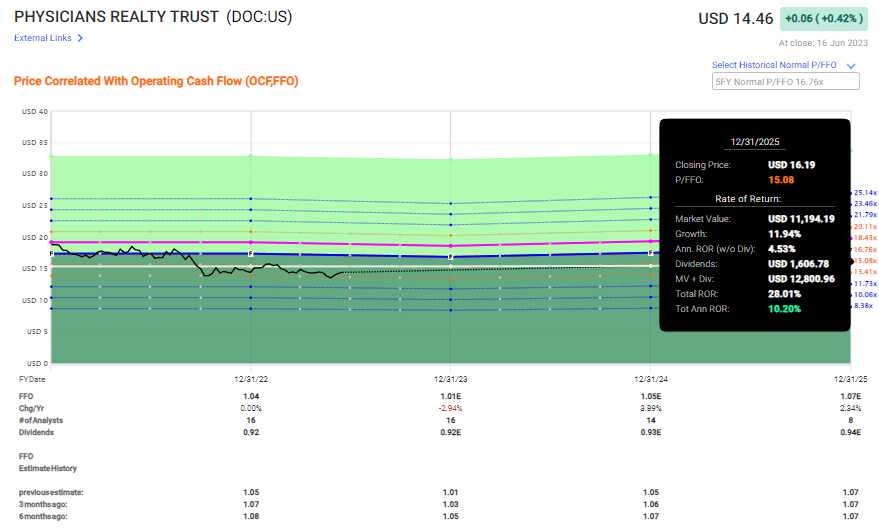

Valuation is of course the key differentiator that could cause us to really invest here. DOC tends to trade about at a 15-17x P/FFO. Given the high degree of predictability and quality to the company's portfolio, but now offset by a higher degree of inflation than expected, it impacts the average we should expect here.

I'm moving down to a 15x P/FFO valuation target for DOC. Why am I doing this?

Because the company's current forecasts for 2023E are negative - and the subsequent quarters are less than 4% FFO growth per year, averaging less than 1.5% FFO per year on average. That means that on the basis of a 15x P/FFO forecast, we have double-digits for DOC here.

{kind=link}

DOC Upside 15x P/E (F.A.S.T graphs)

DOC has some attractive valuation targets - and they're conservative. 15 analysts follow DOC, and 8 of them are at positive stances, with ranges from $14-$19, averaging at around $16/share. This implies around 0.95x to NAV on a per-share basis.

S&P Global estimates NAV to be around $18-19/share. What this means is that the current share price and valuation are actually lower than the estimated net asset value of its portfolio.

It's important to know that DOC is in no way risk-free. What I say is that it's less risky than its peers, based not only on geography, but tenant credit quality ratings.

DOC IR (DOC IR)

The risk comes from the fact that the company, like many companies on the market today, are increasing or seeing unchanged positive sales, but their earnings are dropping. So square footage is up, but that FFO, that's dropping.

This to me indicates the need for impairing or discounting the amount of money we're willing to pay - and that's before accounting for inflation and other things we're currently still in the middle of. How much really depends on "how bad" things are.

I would say that the company reaches high if it goes there - but at $16-17/share, I would consider DOC cheap enough to at the very least consider. There's no shortage of REITs at this time that even have BBB, where you can get 5-8% yield relatively easily - in malls, offices, and healthcare, all of these areas have investments where this is possible. But out of these sectors, some are obviously more risky than others.

I would consider offices the riskier ones generally, healthcare like this one somewhere in the middle. The main problem is really that you're buying a company that typically trades at a massive premium cheaply, but that company isn't expected to massively outperform as we move forward, due to pressure from various directions and overall macro.

There are better yields to put your money into. There are also better safeties or more upside to put your money into. But let's say you're already heavily invested in Simon Property Group ( SPG ), like me - and you don't want to go deeper or go into the office REIT space. Then I would say that DOC shows up on your list as a potential investment. The company has conservative debt, and its management is excellent. Even if the "boat starts rocking", I don't expect the management of this company to break stride. They have prepared their REIT for coming turbulences, and the worst we might see are somewhat more impacted growth rates, meaning we actually go flat in FFO or even turn slightly negative.

However, this wouldn't necessarily impact the company's payout unless that decline became more material or longer-term.

For that reason, my stance on DOC remains a positive one. I'm adjusting my PT to reflect the new reality of growth as well as macro. I'm now down to $17/share. The iREIT share price target is still $20.5/share.

Thesis

- DOC is a good REIT - great quality assets and a good yield. You're also buying the company at significantly below 1x NAV, and locking in a very attractive, well-covered yield. The company is investment-grade rated and also leases to plenty of investment-grade tenants in turn.

- DOC is doing many things right - and the risks, following this article, are known to you.

- I have a small position in DOC and one that I would be interested in slowly expanding. The company works against too much market volatility with its qualitative portfolio and tenant safety. 6%+ yield, while not completely offsetting current inflation or better than all of the yields we can find out there, is enough to cushion things "enough" going forward.

- Our price target is $17/share and DOC is a "BUY".

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

This company is overall qualitative. This company is fundamentally safe/conservative & well-run. This company pays a well-covered dividend. This company is currently cheap. This company has a realistic upside based on earnings g rowth or multiple expansion/reversion.

Because the company fulfills all of my investment criteria, i'm positive and I consider them to be a "BUY" here.

For further details see:

Physicians Realty Trust Is Much Safer Than It Looks