DOC - Physicians Realty Trust: Juicy Income Now On Sale

2023-10-09 10:23:17 ET

Summary

- Physicians Realty Trust offers a high-yield dividend of 8% and is currently attractively priced.

- Strong tenant base and a portfolio of high-quality assets, providing long-term security for rental revenues.

- Despite some risks, such as the potential impact of telehealth, Physicians Realty Trust is a viable long-term investment opportunity with stable earnings growth projected.

- Valuation suggests a compelling entry point in this REIT.

Physicians Realty Trust ( DOC ) is a real estate investment trust, or REIT, that pays a juicy quarterly dividend for income-thirsty investors. The stock has been crushed, along with countless other names. We have been actively starting to search for income names that are on sale. While we do see more pressure ahead, in this rate environment, for the long-term investor, DOC shares are attractive in the $10-$11 range, near decade lows.

DOC stock offers investors an attractive current dividend yield now approaching 8.0%. This is now a very high yield. While many have likely bought all the way down, we actually were short REITs for a few quarters during this carnage. However, we see 2024 as a turning point for many REITs, and we see Q4 as a turning point for broader markets. Thus, over the next two quarters, we want to take advantage of weakness in some key income names. While DOC is not without risk, we see it as viable for the long term.

While we are starting to look for buys, we will generally become much more bullish when the likelihood of rate cuts grow. We believe REITs are approaching a generational buying opportunity for income. Traders and investors looking for a bounce should keep this sector on their radar. While we have not bottomed, we do think we are getting close. For now, we think you start to leg into quality names, and while DOC has had mixed performance, we think the 8% yield is secure, and too good to ignore from here on down.

Regardless of what the bears may assert, our review of the company suggests it is not going out of business, despite being priced as if it is. The sector is in the midst of a fire sale, and we think you need to take advantage of the income opportunity. In the very-near term, it is best to avoid if you are worried about your capital in the next two quarters. However, for investors, sales like this do not come around too often. Volatility is your friend. You are buying a business here for the long term. While we are seasoned traders, we are viewing this as an investment.

We will be under a higher-for-longer rate environment, but 2024 is where we see REITs bottoming out as we see the Fed rate hike campaign coming to an end, as we have discussed this in depth among our investing group membership. We also see the first-rate cut in H2 2024. The economy just cannot continue to handle all of this pressure. While it has held up, the impacts of higher rates are starting to be felt. We are a debt-fueled economy. And companies with leverage, those who use debt, like REITs, have been hammered. For DOC, the most pressing risk might be the push to move to telehealth as much as possible, reducing the need for physical tenants and office space. Still, the tenant data is still strong here given that physical office space is necessary for DOC's tenants, and the balance sheet is holding up.

For those who trade with us, you may not be familiar with this income name. This REIT targets investment-grade tenants occupying some of the highest quality assets in the space. The company likes to have a focus on outpatient transition in terms of care. The tenants they seek are largely insulated from telehealth in our estimation. They also have some of the better landlord expense protections in the space. The company has geographic diversity, though they are more focused on the Eastern United States. Some key cities with tenants are Atlanta, Louisville, and Minneapolis. Most of their tenants need physical space, as they do business in cardiology, radiology, ambulatory surgery, orthopedics, and cancer services. People need to physically come in for such services, so the telehealth taking over argument just does not fly in our estimation.

As a REIT, this company does have property in 32 different states with over 250 outpatient medical properties and about $6 billion in real estate investments. The company enjoys a near 95% leased rate on the portfolio, and two-thirds of the tenants have investment grade ratings, adding to the long-term security of rental revenues. Over 90% of the net leasable square footage of the portfolio was either on the campus of a hospital or strategically affiliated with a health system.

One of the major things to consider for a REIT is the tenant base and the occupancy rate at properties. The portfolio is sound, and the company will keep generating recurring revenues for many years to come. Similarly, some 93% of rents come from absolute net or triple net lease agreements. The leases typically have terms of 5 to 15 years and include rent escalators of 1.5 to 4.0%. The company has made more property acquisitions recently, including in El Paso, TX, and funded construction of new facilities. While the cost of debt is on the rise, and this is a risk, DOC is thinking long-term. So should you.

In the most recent quarter growth continued . Total revenues increased $2.9 million, or 2.2%, for Q2, compared to a year ago. Rental and related revenues increased $1.9 million, or 1.4%. The company earns interest on some of the loans it has made, and saw interest income increase 38% from a year ago. Likewise, it also has a number of loans of its own, of course. And so, the interest expense line needs to be watched, as it is expected to grow over time with future financing being more expensive. Interest expense increased $3.4 million, or 19.7%, from a year ago, most notably from a $2.6 million increase due to the new $400 million term loan executed on May 24, 2023.

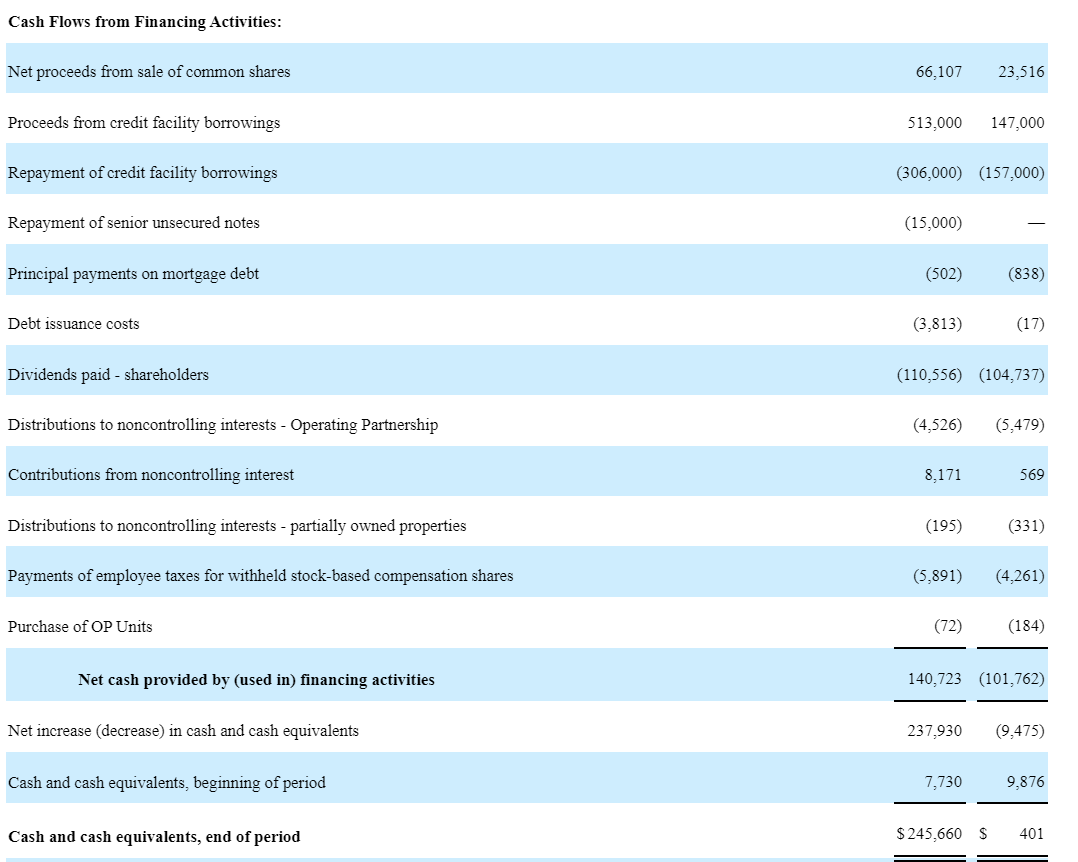

Total revenue was $268.4 million in Q2. While total expenses were $247.2 million. Factoring in some sales and equity gain, net income as $23.7 million, or $0.05. Normalized funds from operations were $0.25 per share. Cash flow is key. Looking at H1 2023 overall, net cash provided from operating activities was $145.8 million, while net cash used in investing activities was $48.6 million. The company generated $140.7 million in financing activities. A summary of that is below. Most notably, the dividend is why we buy the stock, and that cost about $110 million so far this year. The far right column is H1 2022, the second to last column is H2 2023.

10-Q for DOC second quarter 2023

{kind=link}

We still like the balance sheet here overall, but will keep an eye on debt.

{kind=link}

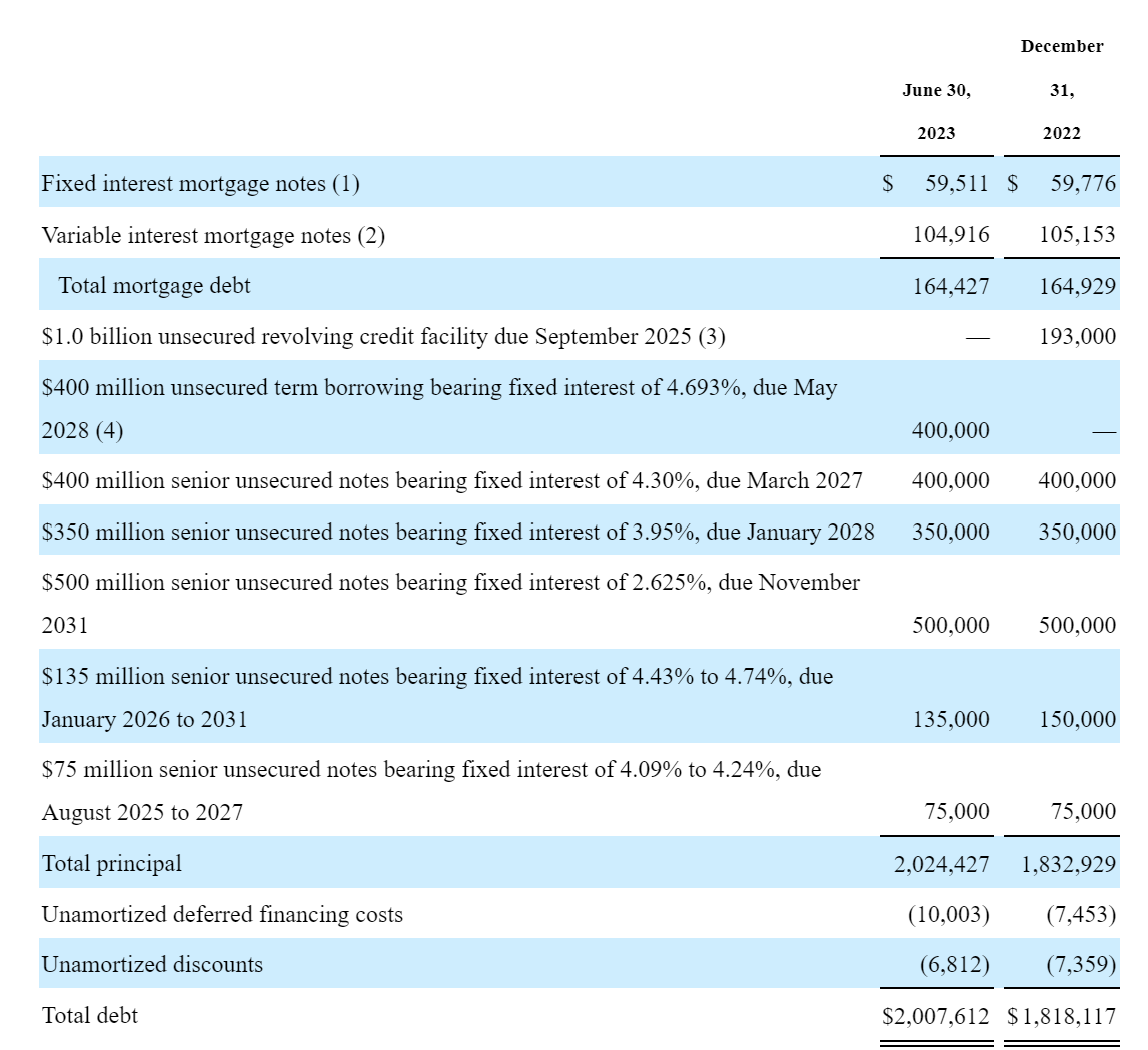

At the end of Q2, total debt was $2 billion, up from the start of the year due to financing activities. The next major debt is not due for another two years or so. And less than 15% of principal is due in the next 4 years.

{kind=link}

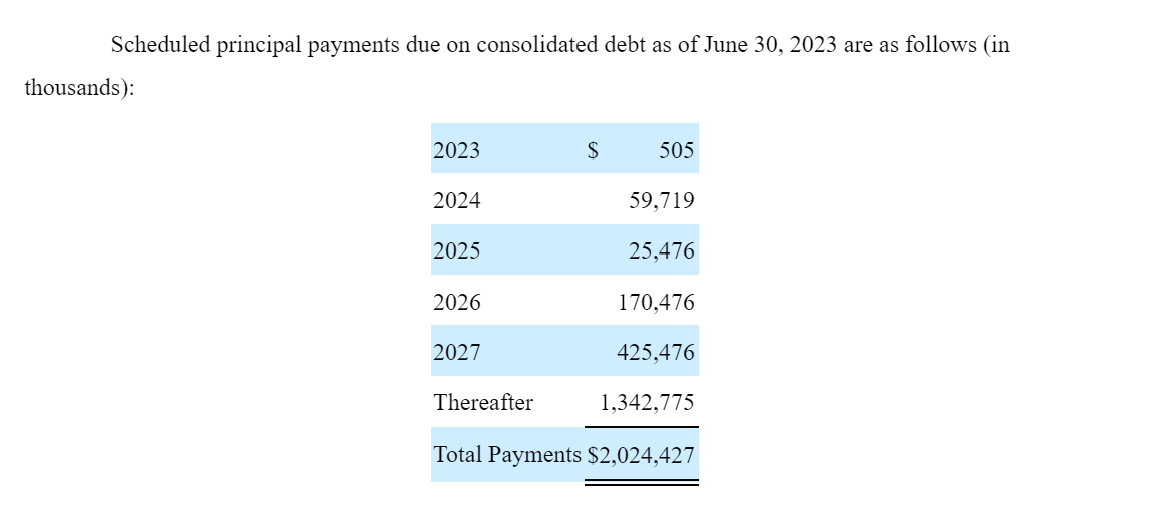

Folks, we like this debt calendar. As we move forward, we recognize that debt taken on will come at higher interest expense. We also have to watch risk associated tenants, but like that most are investment grade. The valuation here is also quite attractive, all things considered.

{kind=link}

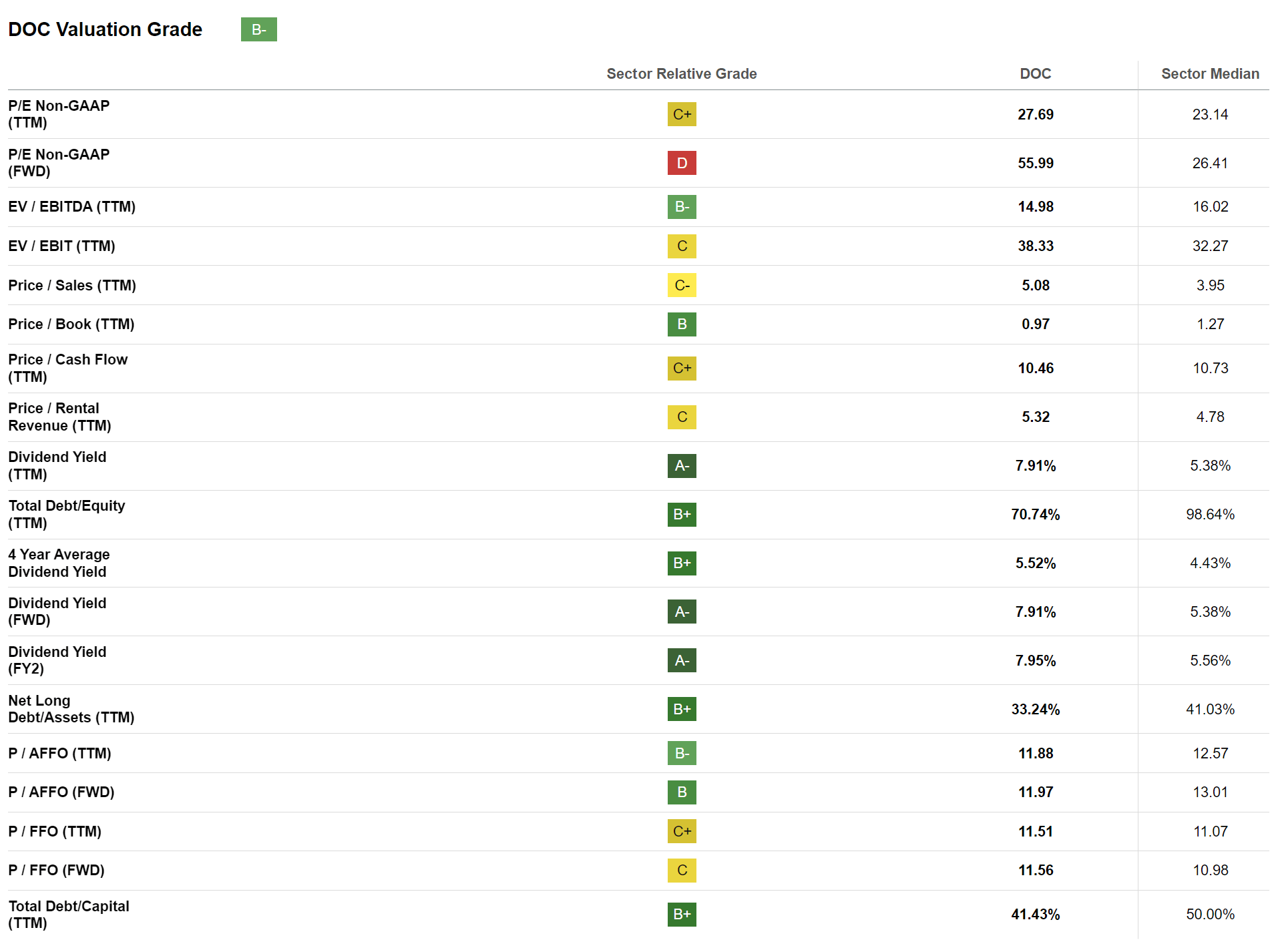

From a p/AFFO we are at 11X, which is attractive. The yield is attractive, of course, as is the price to book in our opinion. Leverage is well controlled as well.

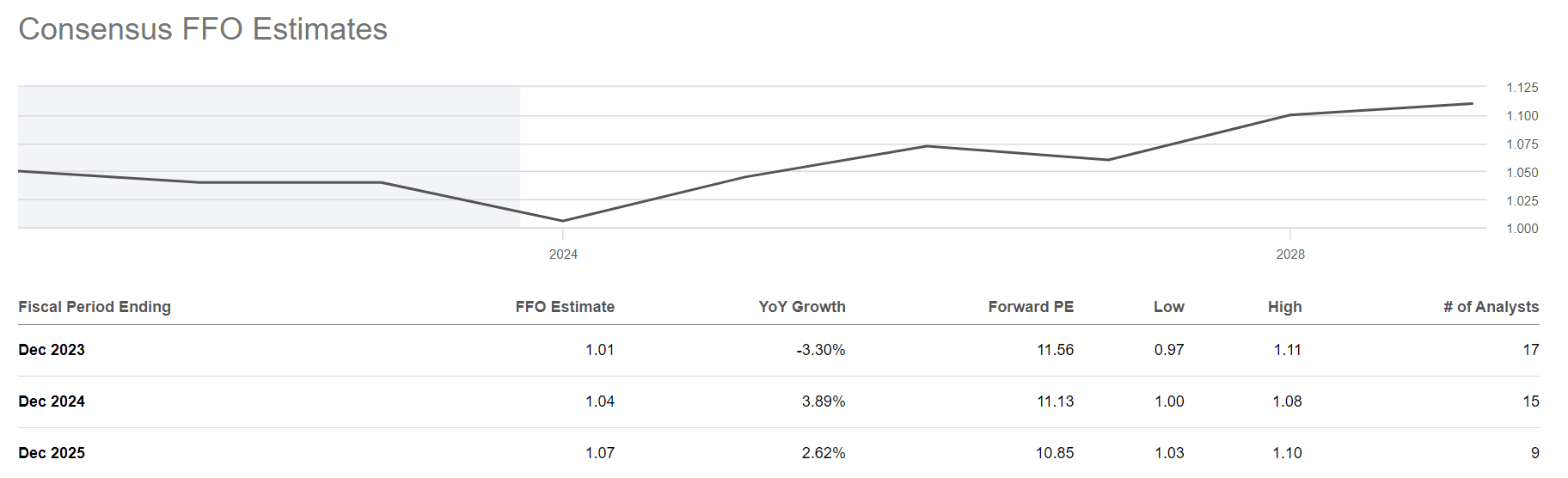

Looking ahead, the company is projected to enjoy stable earnings on an FFO (funds from operations) basis, according to the consensus.

{kind=link}

Consensus FFO is projected to grow, albeit very slowly. However, for an income generating name, which is why we are starting to get behind it, there is a lot to like about stable/slow growth. We think Physicians Realty Trust shares are a buy for income, with an 8% yield here.

For further details see:

Physicians Realty Trust: Juicy Income Now On Sale