DOC - Physicians Realty Trust Near 52-Week Low Is A Buy

2023-05-26 08:05:03 ET

Summary

- Physicians Realty Trust carries a respectable portfolio of high-quality properties that are well-diversified by geography.

- Near-term expense pressures are expected to moderate, and it should enjoy long-term demographic and secular trends.

- Value and income investors may benefit from capturing this high-yielding stock while it's trading on the cheap.

There is clearly a bifurcation in the market today, with tech-heavy weighted S&P 500 ( SPY ) and Nasdaq indices widely outperforming the Dow Jones Industrial Index so far this year, especially after the recent strong results from chip giant Nvidia ( NVDA ).

Having indices being weighted based on market cap, as in the case of SPY and Nasdaq can actually cause more volatility down the road, as the continued flow of funds from index investors can exacerbate concentration risk. On the contrary, the DJIA is weighted based on share price and not market cap, making it less susceptible to the aforementioned risk.

Plus, while the market has gravitated towards technology stocks, many traditional income generating stocks have been left in the dust. This is not a bad thing for value investors, as it gives them the opportunity to layer into income stocks while they are trading on the cheap. In other words, capital gains are vanity, while income is sanity.

This brings me to Physicians Realty Trust ( DOC ), which as shown below, is now trading just shy of its 52-week low and is sitting 6% below the price (-3% total return thanks to dividends) since I last covered the stock back in November of last year. In this article, I discuss recent developments and why DOC is a worth a hard look for high yield and potentially strong gains.

{kind=link}

What's Up, DOC?

Physicians Realty Trust is one of two internally-managed REITs that are primarily focused on owning Medical Office Buildings, with Healthcare Realty ( HR ) being the other one. Unlike seniors housing, hospitals, and skilled nursing facilities, MOBs have largely bucked many of headline risks in the healthcare sector over the past 3 years.

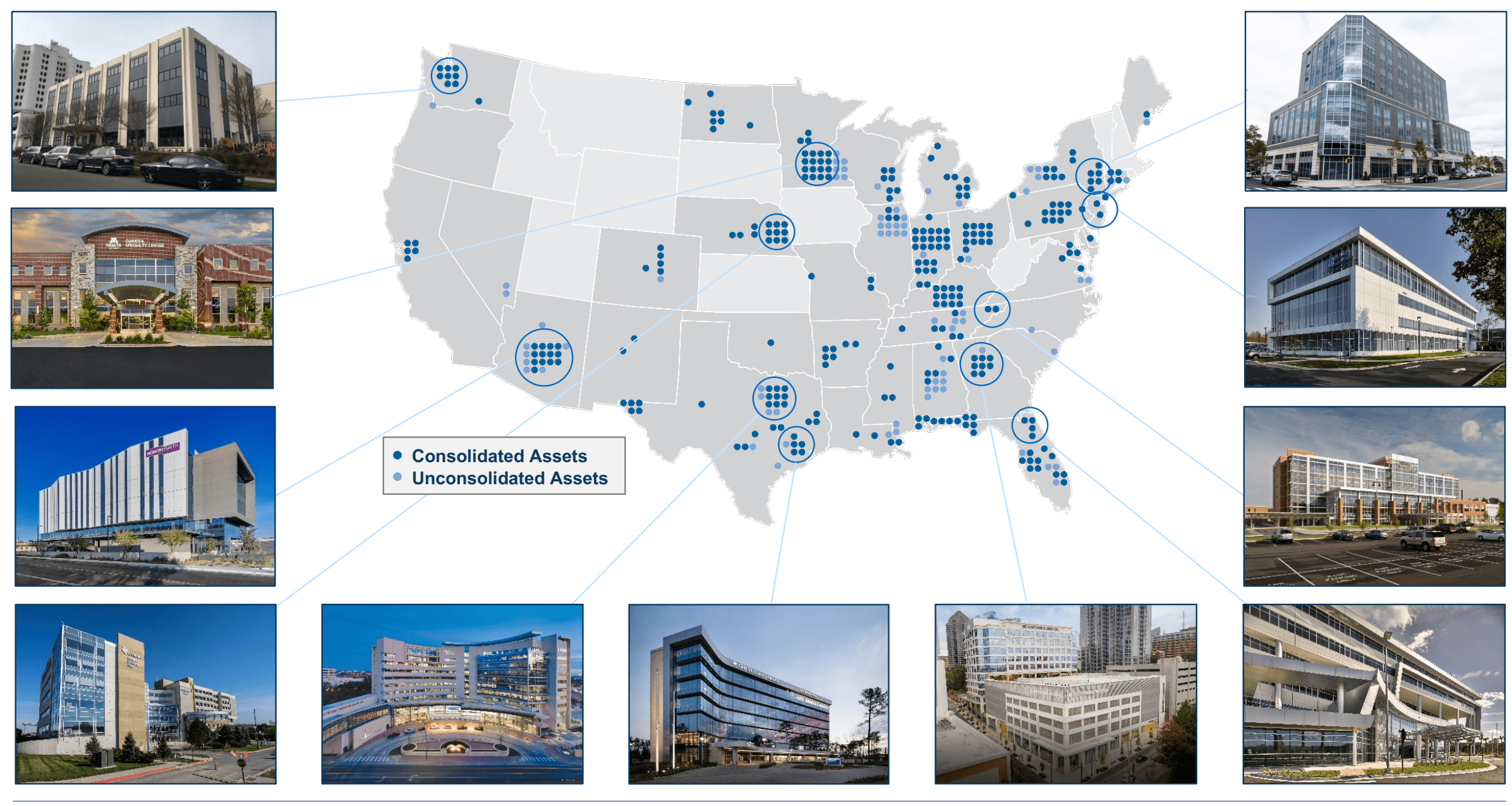

DOC's asset base is well diversified by geography and covers 290 properties, of which 67% are tied to tenants with investment grade credit ratings. Notably, 90% of DOC's IG-rated tenants have a credit rating of A- or better.

In another sign of quality, 89% of DOC's annual base rent stems from properties that are either on healthcare campuses or are affiliated with health systems. This helps DOC's tenants to enjoy the 'network effect' that comes with being associated with other healthcare providers and leading systems. As shown below, DOC's properties are in most U.S. states, with focus on densely populated regions in the Northeast, Sunbelt, Midwest, and West Coast.

{kind=link}

Meanwhile, DOC's portfolio is faring well, with a 95% leased rate. However, expenses rose during the first quarter to $123 million, up from $116 million in the prior year period. This put pressure on same-store cash NOI, which grew by just 1% YoY. Nonetheless, growth is still growth, and DOC has grown its same-store NOI for 20 consecutive quarters.

Looking ahead, I would expect for the bottom line to improve, with the addition of the Landmark portfolio that was just added last quarter. This is a high quality portfolio with 14 Class-A MOBs that are 95.5% leased (up by 50 bps since acquisition). It also compares favorably to the rest of DOC's portfolio, as its 100% on-campus/system affiliated and has 75% investment grade tenancy.

Moreover, 60% of DOC's properties now have annual rent escalators of 3% or more, comparing favorably to just 25% of properties having this in the 2018 to 2021 timeframe. Longer-term DOC should benefit from demographic tailwinds and the continued shift towards outpatient care. Plus, management expects the currently expense pressure to moderate and improve, as noted during the recent conference call :

For years, the fundamental case for owning outpatient medical facilities has been strong, but is now stronger than ever. First, healthcare providers benefit from undeniable demographic tailwinds currently and that will dramatically increase demand for services in both the near and long-term.

Second, due to Medicare's Progressive Payment System and Part C modernization, providers are incentivized to provide care at the lowest possible cost consistent with the clinical science available at the time to treat the patient safely and effectively.

Third, current expense pressures are temporary and correctable. These pressures are caused by the unique combination of real time inflation and backward looking payer revenue rates that are set based on past costs rather than current or future expected costs.

Importantly in this higher interest rate environment, DOC carries a solidly investment grade credit rating of BBB by the S&P, and has low leverage with net debt to EBITDA of 5.3x. Admittedly, DOC's dividend payout ratio is a bit stretched at the moment at 90%, based on forward FFO/share of $1.02, but I would expect for this ratio to improve as expenses moderate and rent grows.

Lastly, I believe there is value to be had with DOC yielding 6.8% at the current price of $13.50 and forward P/FFO of 13.2, sitting well below its normal P/FFO of 18.4. While analysts currently have a consensus Hold rating on DOC, their average price target of $15.85 implies a modest forward P/FFO of 15.5. Even with a more conservative P/FFO target of 15.0, DOC could deliver a potential 20% total return over the next 12 months.

Investor Takeaway

DOC's portfolio of high quality outpatient facilities is well positioned to benefit from long-term demographic and secular trends. Short-term pressure on expenses will likely moderate over time, and the addition of Landmark Healthcare should help improve near-term cash flows. With DOC currently trading at discounted valuation multiples and a dividend yield of 6.8%, I believe DOC is well worth a closer look for income-oriented investors.

For further details see:

Physicians Realty Trust Near 52-Week Low Is A Buy