PLL - Piedmont Lithium: Strong Potential But A Buy Not Just Yet

2023-05-12 10:00:42 ET

Summary

- Piedmont Lithium Inc has made strong moves to solidify its position as a supplier of lithium in North America.

- The company is starting production at one of the sites in 2023, but the other ones are a few years out.

- The company has maintained a strong balance sheet, but without a positive bottom line, I can't make a buy case and will keep PLL on hold for now.

Investment Summary

Piedmont Lithium Inc (PLL) is a company in the lithium space, a crucial commodity used in making rechargeable batteries for electric vehicles (EVs). This mining company is headquartered in North Carolina and primarily focuses on exploring and developing lithium deposits in the area. Piedmont Lithium has the potential to become a significant provider of lithium to the EV industry, making them an important player in the growing market for sustainable transportation. The company has acquired 3,250 acres of land in the northwest of Charlotte, North Carolina. Here the company has high exactions of the location, anticipating around $459 million in EBITDA in their presentation . I think PLL is an exciting opportunity in the lithium space, but it's hard to go with over more established companies that have successfully reached profitability already. I think the estimates for PLL are great and I am sure they will have incredible growth in the coming few years, but I am worried to invest before I see a positive net margin, therefore I will be rating them a hold for now.

Strong Demand And Potential Shortage

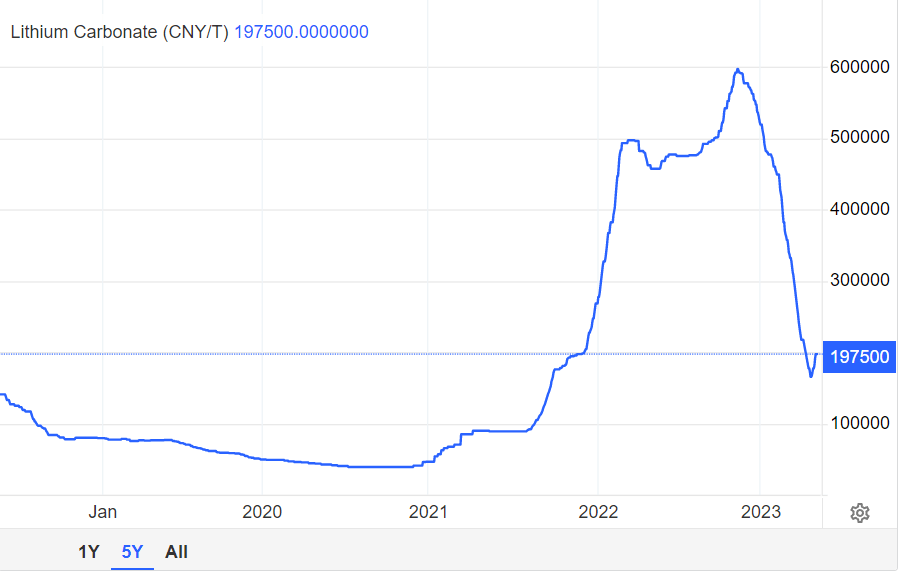

Lithium has been in the mouth of many investors in the last few years as it has become an important commodity for the EV industry as it's a necessary part of creating vehicles. But the demand seems to outweigh the supply which caused a massive rise in the price in both 2021 and 2022.

Lithium Price (tradingeconomics)

{kind=link}

The trend seems to remain strong though and there is an uptrend as more and more companies want to become sustainable and have EV fleets. The demand for EV vehicles helped spark the rise in price for lithium, something that benefits the long-term outlook for PLL as they will be supplying this eventually. The overall lithium market is expected to see an impressive 13.5% CAGR between 2023 - 2028. As PLL is expected to be able to in 2023 start production the company has a long runway to benefit from this market growth and demand. The first land production for PLL is in Quebec, where a high-purity lithium ore called "spodumene concentrate" is mined. Between 2023 and 2025 the ore available for sale is expected to be almost 5x from 56,500 to 240,500. This is why the future estimates are so positive with EPS growth of almost 90% YoY and resulting in a p/e of under 3 in 2025. Further boosting the long-term case for the company is the fact we seem to be facing a shortage of lithium in 2025 as well.

Risks

The main risk of investing in PLL right now is that they aren't yet profitable or even have revenues. The company has been able though to improve the EPS on a YoY basis. In 2022 for the first quarter, the EPS was negative $0.57 per share and improved to a negative $0.47 in 2023 for the first quarter. I think this is meaning the company is at least moving in the right direction as production starts to ramp up.

But with high expectations in the future, any challenges or hiccups will cause a chain reaction that eventually ends up with the share price seeing a fall and hurting investors. It doesn't have any fundamentals to trade on yet and that creates a lot of risk. The risk that I am not sure worth taking until we actually see proof of concept from the company. Besides that, the shares outstanding have of course been diluted over the last few years and I expect this to be a move that will continue to happen. The shares increased by more than 3x in the last 5 years, but the share price has done well, increasing 276% in the same period. Moving forward margins will be key to look at and if there is a clear sign of weakness I expect the share price to fall as the market corrects to the true value for PLL.

Financials

With companies that are yet to have any revenues, keeping a solid balance sheet in the meantime is incredibly important. It's all about managing the costs in order to dilute as little as possible to still keep investors on the hook.

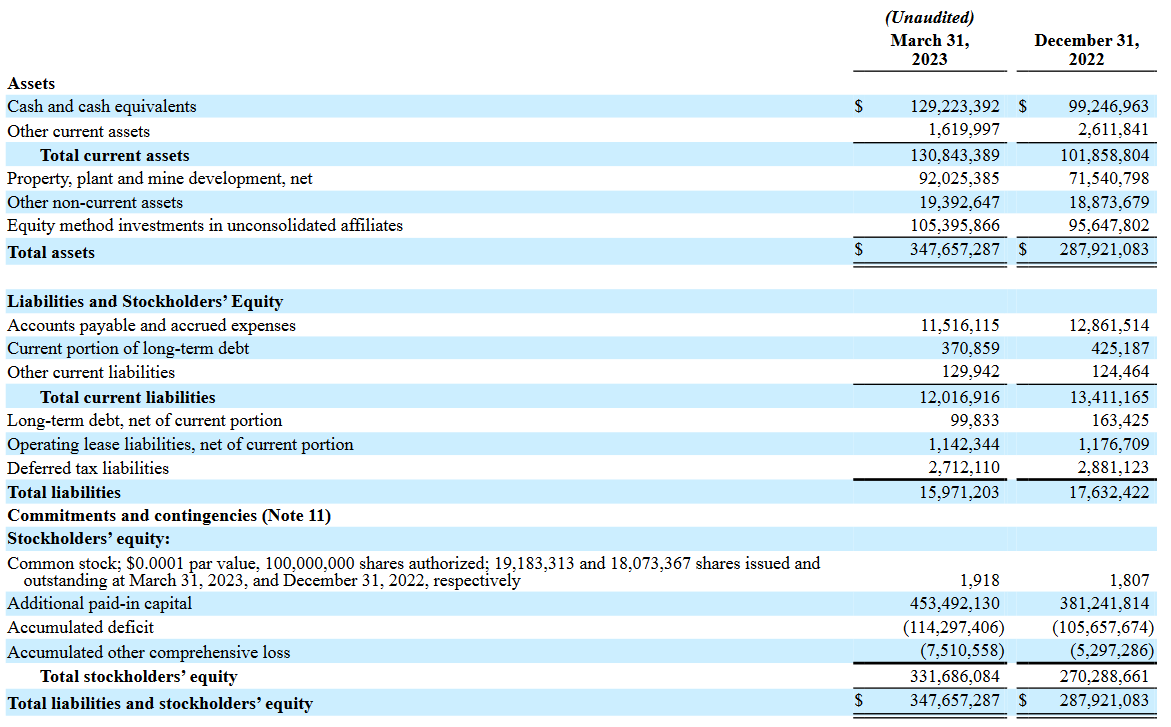

The company keeps a cash position of just under $130 million which makes up over a third of the total assets right now. The company has been able to decrease the cost of operations thankfully on a yearly basis as they move closer to production. In the first quarter, the company had loose amount to $8.1 million, a decrease of $1 million from a year before. Using this number the company would have another 4 years to operate before they run out of cash. That is barely when the Carolina operations start. I think this showcases that there will be more dilution of shares to help fund the company. Not necessarily a bad thing, but it doesn't make for a good buy case right now in my opinion. Instead, seeing a positive EPS and margins will give a much better picture of the possibility of the company.

Balance Sheet (Earnings Report)

{kind=link}

Looking at the balance sheet future, the company is maintaining a solid stance so far, with current assets massively outweighing the current liabilities, by 10x more. Long-term debt sitting at $99 million also seems very manageable, as only $370 000 is in the current portion.

All in all, I think PLL has done a fine job so far of navigating the tough environment of lithium and setting up operations. The future seems bright and if they can maintain this restraint and quality I see a lot of potential here.

Valuation & Wrap Up

It's tough to put a valuation on a company like PLL which hasn't yet been able to achieve a positive bottom line, or even generate revenues yet. The company has a strong outlook as they have started production in the first quarter of 2023. But I think the investment case or thesis right now is to simply wait until there is more clarity with the company. Looking at forward estimates the p/e sits at under 3 in 2025, so I don't think there is any rush buying in right now. It would of course mean there is a massive upside potential here if the company gets a valuation in 2025 similar to the sector with a p/e of around 13. It would put the share price at around $273, up 478% from the current price.

{kind=link}

I still see the company as speculative and am happy to miss out on some of those gains and invest in a company I am confident in and feel comfortable having capital in. Until then I will be rating PLL a hold and keep a close watch on the coming reports and updates on the company's projects they manage.

For further details see:

Piedmont Lithium: Strong Potential, But A Buy Not Just Yet