PILBF - Pilbara Minerals: Lithium Price Play

2023-04-13 12:11:52 ET

Summary

- The Australian lithium miner Pilbara Minerals has seen windfall profits recently as its realized prices skyrocketed. However, lithium prices have crashed since.

- There is a good chance that the company can continue to stay profitable even at lower prices, and not all analysts believe the lithium price decline will continue much further.

- It still looks like a good long-term buy, but given the current price uncertainty, it would be a good idea to Hold, only to buy it at a better price.

With lithium in high demand and expected to remain so for the long term, the future of the likes of Australian lithium miner Pilbara Minerals ( PILBF ) looks bright. However, during times of optimism around specific sectors, stocks can have a tendency to run up far beyond what the fundamentals indicate. Not this one, at least right now.

In 2023 so far its price is slightly down by 2%, and its trailing twelve months [TTM] price-to-earnings (P/E) ratio is at 6.3x compared to the 12.8x for the materials sector as a whole. This is not to say that it has not been a good investment in the past years. In the last five years, its price has actually risen by 263%, because of the growing demand for electric vehicles [EV].

Here I take a closer look at its fundamentals to see why it has slowed down this year and whether its attractive P/E ratio indicates better times ahead, ahead of its quarterly update due later this month.

The company

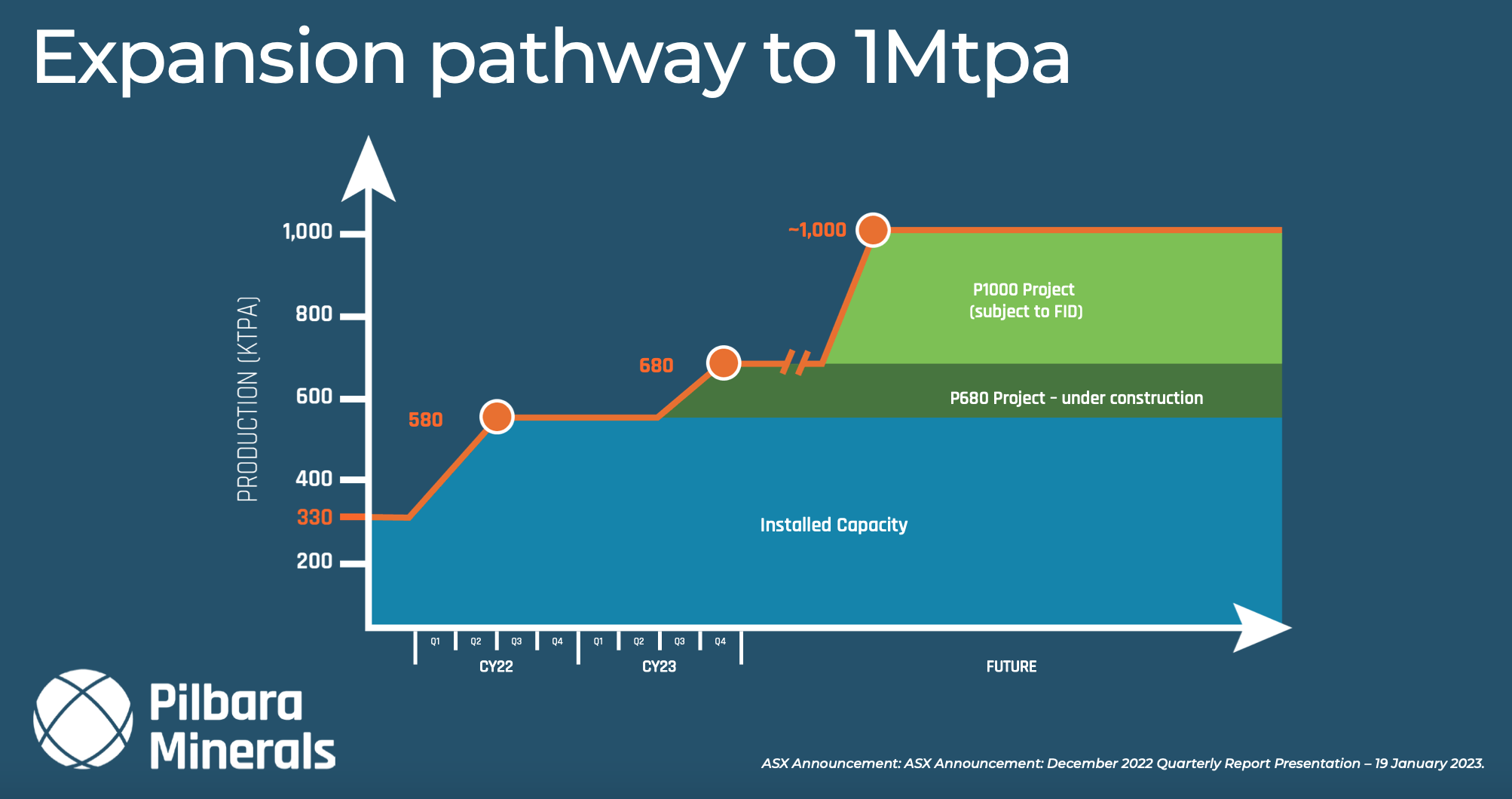

Founded in 2005, the company’s Pilgangoora Project has the distinction of being the largest hard-rock lithium mining operation in the world. It can produce up to 2 million tonnes each year and has a processing capacity of 580,000 tonnes of spodumene concentrate, a lithium mineral. With a mine life of over 26 years, it has much long-term potential as well. The company is also expanding its production (see chart below) and diversifying, which is discussed later on here.

{kind=link}

Can financial gains continue?

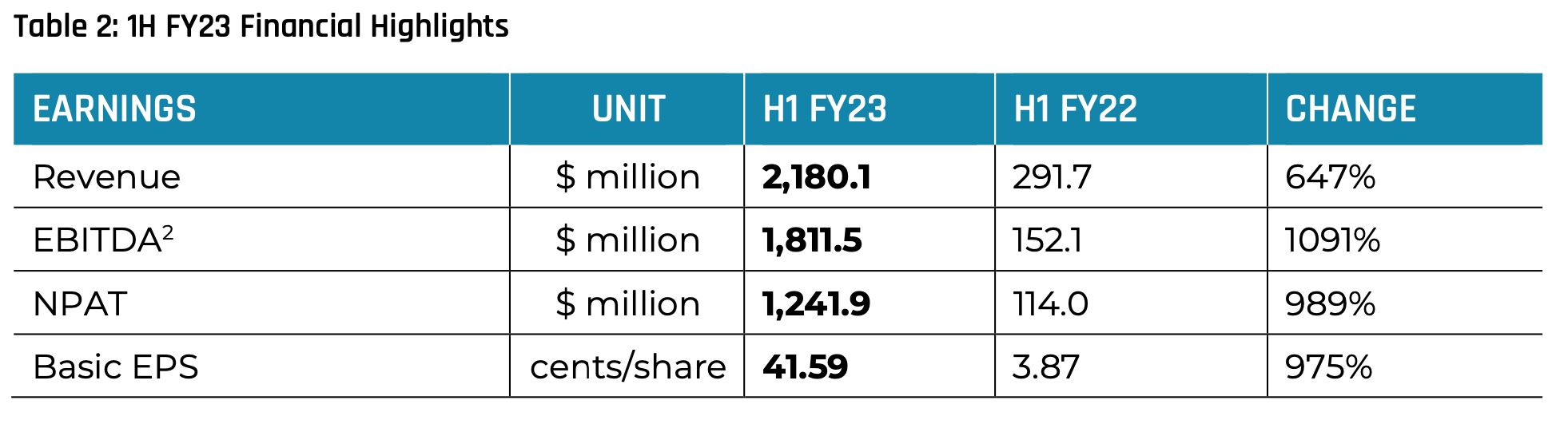

With a huge upturn in lithium price in the first half of 2022 (H1 FY23, ending December 31, 2022), the company saw a 305% year-on-year (YoY) increase in the average realized price. This of course showed up in its financials as well. While there is no doubt that its production was up by an impressive 83%, that was small compared to the revenue increase of 647% and earnings increase of 989%.

{kind=link}

Falling lithium prices

However, much has changed in 2023. After climbing to record levels in November last year, lithium price has fallen off the cliff , as it were. The reasons for this sudden phenomenon, include a slowing down of electric EV demand in markets like Europe and China, as government subsidies encouraging their sales ended.

The likelihood of an increased supply of lithium is also seen as a reason for the falling price, with a Goldman Sachs ( GS ) expecting a 25% increase in demand compared to a 33% supply rise. Opinions on lithium price are divided, though. Citi, for instance, expects, prices to stabilize this quarter itself.

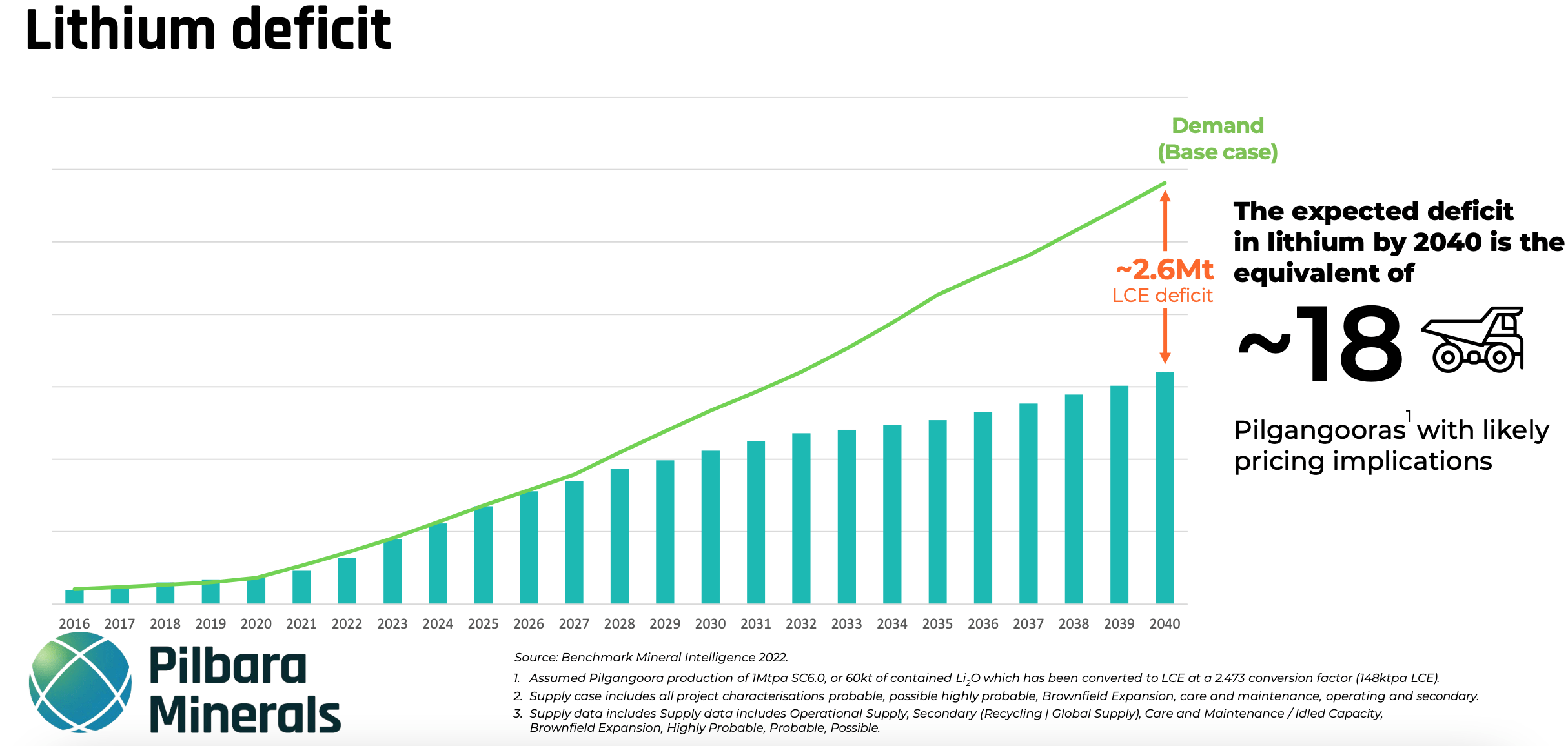

Further, Seeking Alpha’s Long Term Tips , who researches the sector, tells me “lithium prices seem to have neared a bottom”, attributing it in particular to Chinese lithium producers who have “slashed their production from low-quality resources (like lepidolite).” Pilbara Minerals’ own projections also show a supply deficit of lithium (see chart below).

{kind=link}

Also, unless lithium prices fall significantly from current levels, how much that would affect profitable miners like Pilbara Minerals remains to be seen, going by the strong margins lithium mining offers. For example, in FY22, Pilbara Minerals’ gross margin was nearly 80% and its operating margin was 78%. For H1FY23 the figures were even stronger, with the gross margin rising to 82.5% and the operating margin to 81%.

While it is quite possible that the company can see some cooling off in margins in the near future, the fact remains that it was profitable even when lithium prices were much lower. In H1FY22, when its average realized price was a much lower USD 1,232 per dry metric tonne (dmt), compared to the USD 4,993/dmt in H1FY23, it still had a robust operating margin at over 70%. The latest developments then mean that the company’s profits do not look under threat, at least for now.

Supply increase could take time

Where lithium prices go next also depends on the speed of new supply. New mining projects can take years to become operational. A case in point is Pilbara Minerals’ own Mt Francisco project, which it owns jointly with Atlas Iron, another Australian miner. Exploration began in 2018, since when it has found reserves of lithium and other minerals like tin and tantalum. But the company says, only a small portion of the Mt Francisco area has been tested so far. Although, some analysts do expect the lithium supply to increase quite fast .

Diversification underway

Even so, as earlier discussed, it might not impact Pilbara Minerals’ ability to generate a profit. Further, the company’s diversification into value-added services could be a positive too. It has entered into a joint venture with the South Korean steel producer POSCO to develop a lithium hydroxide conversion facility. The project, which is expected to ramp up in 2024, will be among the few such outside of China. It has also partnered with the technology solutions provider Calix, which can produce a superior lithium product with higher concentration and fewer impurities.

What next?

All in all, the company in itself looks good to me, even if the current outlook is clouded by the current trends in lithium prices. With exceptionally strong margins, the company could stay profitable even if prices decline to their 2022 levels. As Long Term Tips further adds “... prices still remain well above the long-term average and over 3x greater than the $12/kg average estimate from just a few years ago.”.

Its diversification into value-added services, also sounds promising, though we will know how much they add to its performance only later in the year or next year. It has also started paying a dividend, with a healthy 6.1% forward dividend yield. And going by its performance so far, it looks safe to me too.

There is of course the risk that its profits could decline next year, and probably will if the lithium price keeps falling for now. And that means its P/E would not look quite as attractive as it does right now. Even in August last year, it was at a much higher 25.7x, which is to say it is not inconceivable. From a long-term perspective, it still sounds like a good stock to hold in the portfolio. But from a short to medium-term perspective, I’d go for a Hold for now, only because there could be a better price to buy it in the near future in my view.

For further details see:

Pilbara Minerals: Lithium Price Play