PILBF - Pilbara Minerals: Staying Neutral As New Headwinds Emerge

Summary

- Pilbara recently revised capex numbers higher and guided to additional project delays.

- Pricing gains are also slowing per the latest BMX auction, although they remain well above cost.

- The valuation is pricey on historical revenue numbers and could turn quickly with pricing, so caution is warranted here.

Western Australia-based miner Pilbara Minerals ( OTCPK:PILBF ) has seen its valuation de-rate in recent months amid signs of an electric vehicle demand slowdown and a potential battery supply chain de-stocking event. While the faltering sentiment on lithium is perhaps fair, Pilbara remains one of the cleanest ways to play the secular growth theme in Australia – not only does it have a simpler asset portfolio (vs. its vertically integrated peers), but its primarily domestic mining operations also suffer less geographic/legal risks.

That said, Pilbara remains exposed to capex increases, with the recent revision at P680 and the resulting P1000 delay weighing on the growth pipeline. Signs of pricing weakness (albeit relative to multi-year highs) at last month’s Battery Material Exchange auction are an added concern, given the high correlation to the stock price. With Pilbara already trading at ~10x revenue based on historical numbers and exposed to inflationary headwinds as well as a possible downcycle, I think caution is warranted here.

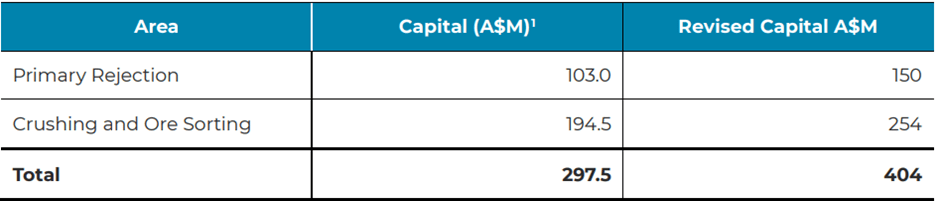

Higher P680 Capex is a Negative Surprise

Pilbara posted an ASX update late last month, citing an upward revision to the P680 project capex allocation to ~A$404m (up from ~A$298m prior). Key drivers of the change include inflationary pressures on material, equipment, and labor, resulting in higher costs to maintain the delivery schedule. This comes as a negative surprise, given Pilbara had been prudent on the cost front, even opting to self-manage the P680 project delivery to prevent cost and schedule overruns. While the higher capex will add strain to the balance sheet, the company has ample funding sources without needing to tap the capital markets. In particular, its recently secured ten-year A$250m debt facility from the state should be sufficient to fill the overruns.

{kind=link}

The only silver lining from the announcement was that capital costs will now include a narrower band for growth and contingency allowances of up to 8% (vs. the original -15%/+20% band). For context, this expansion (final investment decision ((FID)) in June last year) is planned to drive process improvements of 100kt/year over the average mine life of spodumene concentrate production. If successful, this would mean an additional 100kt/year of production capacity, driving the combined Pilgangoora project to 640-680kt/year of production.

Timing is crucial, though - market conditions are favorable now but will likely not remain this way for very long. Management has done well to capitalize thus far, securing a deal to supply a chemical conversion facility in South Korea via the POSCO JV. Further deal traction, while prices remain strong, should pave the way for more earnings upside.

P1000 Project Also Delayed

Following the P680 overrun, FID for the P1000 project has also been pushed back and is now scheduled one quarter later (i.e., in March 2023 vs. late December 2022 prior). Still, the commentary is positive, with management citing good progress on the P1000 expansion project feasibility study, including engineering and pricing estimations. Funding should be no issue either – Pilbara has the pre-FID funding of ~A$38m approved, which should cover long-lead item procurement and progress engineering. So while the additional quarter delay is a negative, the overall project schedule should remain on track otherwise.

The benefits of the project are clear, given the potential ~320kt/year addition to Pilgan, driving long-term Pilgangoora capacity up to 1Mt/year of spodumene concentrate. From here, execution will be key to ensuring favorable project economics, along with external factors such as the broader supply/demand trends.

Margins Stay Strong Even as Latest BMX Auction Sees a Modest Price Decline

The increased capex allocation comes on the heels of Pilbara’s December Battery Material Exchange auction , which saw a ~3% price decline from the prior month’s auction. Note, however, that these are Ngungaju volumes; Pilgangoora production, which falls under offtake, saw pricing gains at $6.3k/t following reviews with major offtake customers. Thus, the average price of $7.6k/t for 10kt remains well ahead of revised offtake pricing, though this is the first MoM decline in a while and is worth monitoring, in my view.

For now, the strong pricing signals a tight feedstock market and strong margins (note site costs run well below $1k/t). With the revised offtake pricing also applying from December 2022, expect an additional tailwind to FY23 earnings. How long the strong spodumene pricing environment lasts is the question, and, in the meantime, Pilbara’s execution on the growth pipeline and recoveries will be key to unlocking more production growth ahead.

Staying Neutral as a New Headwinds Emerge

The sentiment on Pilbara, alongside many other lithium names, has worsened, as evidenced by a double-digit % decline since October last year. Some of this drawdown is perhaps warranted given the negative news flow on EV demand (e.g., Tesla ( TSLA ) having to cut prices in China ), as well as potential de-stocking across the supply chain.

While it’s hard to fault management for the strong execution in the strong spodumene pricing environment, recent capex upgrades at P680 also indicate that inflation is weighing on the growth pipeline. And though the recently announced capital management framework and FY23 dividend are well-covered by the cash flow, mid to long-term sustainability is a concern should a pricing downturn emerge. For all its positives, Pilbara is still at the mercy of the cycle, and thus, further price declines could drive downside risk to the valuation.

For further details see:

Pilbara Minerals: Staying Neutral As New Headwinds Emerge