PAXS - PIMCO August 2023 Report | Valuations Come Back Down But Still Not Compelling

2023-09-04 07:00:00 ET

Summary

- PIMCO taxables have stagnant coverage levels and face potential distribution cuts, making them a risky investment.

- PIMCO muni CEF coverage remains weak and UNII levels are falling, indicating possible distribution cuts in the future.

- PDI and PAXS have seen a decline in price, bringing them closer to fair value, but NAV downtrends and low coverage pose additional risks.

- PDI looks more fairly valued after a steep decline in the last two weeks. Another $0.30 drop and I would be looking to add to my now small position.

- PAXS looks like the best deal, but here we need to be cautious about the steep NAV downtrend. I would be waiting until we saw a more definitive bottom in the NAV before adding.

(Since this report was released to members we have changed our recommendation)

The July UNII report was released and there was not much change in the coverage levels for the taxables. PIMCO Access Income ( PAXS ) is the best positioned here to weather a distribution cut but that comes with some added risks of higher cMBS exposure.

The combination of the high valuation, NAV declines and higher potential for a distribution cut is not the best combination and would prevent me from making any additional buys at the moment.

Overall, PIMCO Dynamic Income ( PDI ) coverage was stagnant in the 50s where it has been for the last few months. UNII (undistributed net investment income) fell by $0.10c to -$0.21. Clearly, no specials are in the cards for most of the PIMCO taxables unless something reverses big time.

Overall, the PIMCO taxables still look a bit rich here with a clear NAV downtrend and low coverage adding additional risks. However, the recent move lower in PDI and PAXS in price get them closer to fair value. I'm indifferent between adding and trimming here.

Since August 8th, PDI has lost $1.30 per share moving from overvalued to fair valued. I did trim a chunk of my PDI around those highs with my last sale at $19.19. I would look at adding those shares back around $18 or just under. PAXS looks a bit more compelling here but would look even better below $14.

However, for those looking for the best entry points, I would wait until we see a clear turnaround in the NAV trend before adding shares.

Coverage Levels Remain In The Doldrums

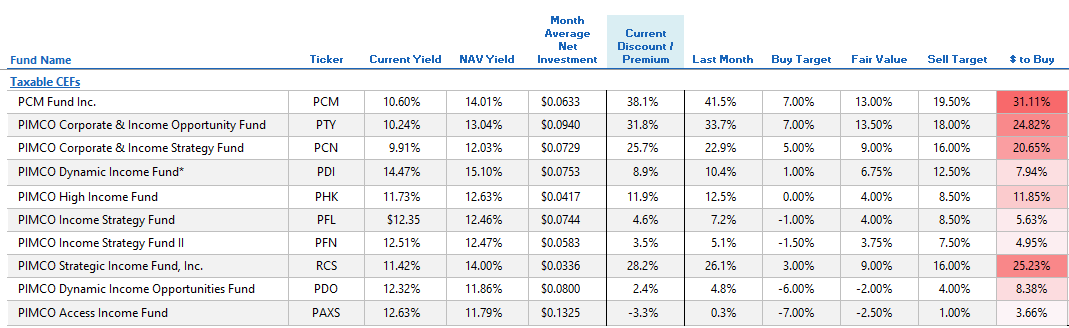

Average coverage did improve about 5 points in July across the suite of taxable CEFs. The funds that saw the most improvement were PAXS (+6 points to 95%), PDO (+13 points to 68%), RCS (+12 points to 72%) and PTY (+9 points to 54%).

PDI did improve slightly by 7 points but remains under 60% coverage. It has now been under that level since November of last year. It seems like a lifetime ago when coverage was above 100%, but that was just 10 months ago.

The volatility of the coverage ratios tends to lower their value in deciding whether or not to allocate capital to them. Coverage volatility can come from a host of factors, primarily their derivative book and asymmetric securities held in the portfolio.

Interest rate and currency forwards are the largest pieces of the derivative book and can cause large short-term swings in the coverage ratios. Currency hedges especially can cause significant distortions in coverage ratios. Foreign bonds held in these portfolios have their currency hedged back to dollars. As the currency moves, the value of those hedges moves around far more than the actual bond prices in which they are hedging. This causes the coverage to swing wildly on occasion.

The dollar fell against their two key hedges, the euro and the pound, during July, applying additional pressures on coverage ratios. However, nearly all risk assets rallied in the month which likely helped to offset some or all of that downside pressure.

ycharts

PIMCO taxables are struggling on coverage but that can change quickly. The 3-month coverage ratio isn't really a good data point

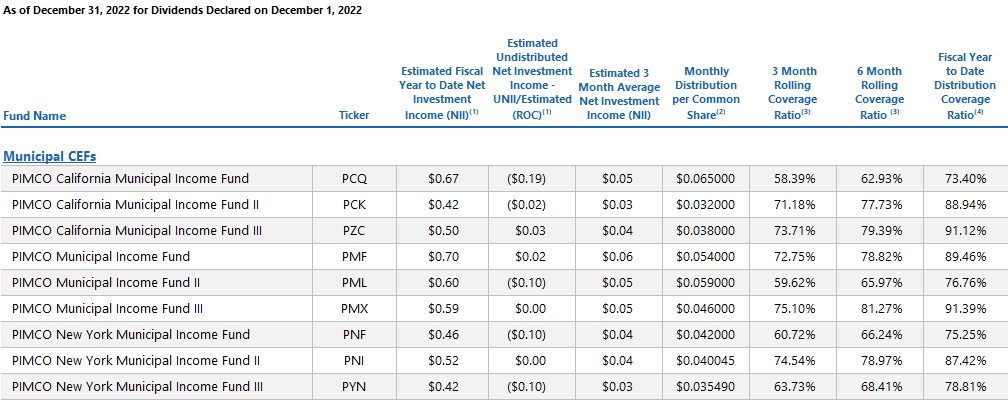

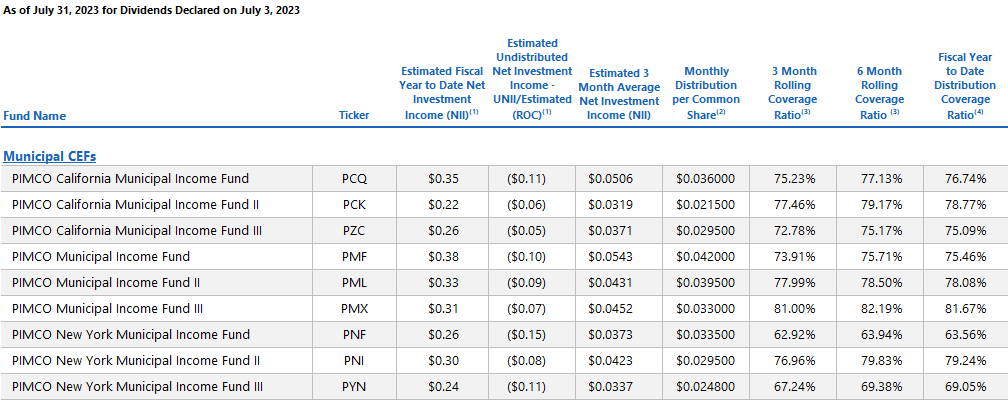

PIMCO muni CEF coverage has been very steady over the last several months, after their large cuts at the start of this year. Coverage remains fairly weak with most funds covering only about 70%-80% of the distribution.

UNII levels are again falling well into negative territory with most funds at or near double-digits. That is a level that has proven to typically result in a distribution cut at other sponsors. PIMCO cut their muni fund's distributions significantly in January when the funds had fundamentals that were close to where they are now. In some cases, a bit better.

Below is the UNII report from December (presumably when they decided to make the large distribution cuts).

{kind=link}

PIMCO

And here is the most recent report from July:

{kind=link}

PIMCO

The conclusion is simple: if things continue going the way they are, the muni funds will likely have to cut again. There is no doubt about that. Perhaps they will wait until January, which is a typical PIMCO thing to do. Perhaps not.

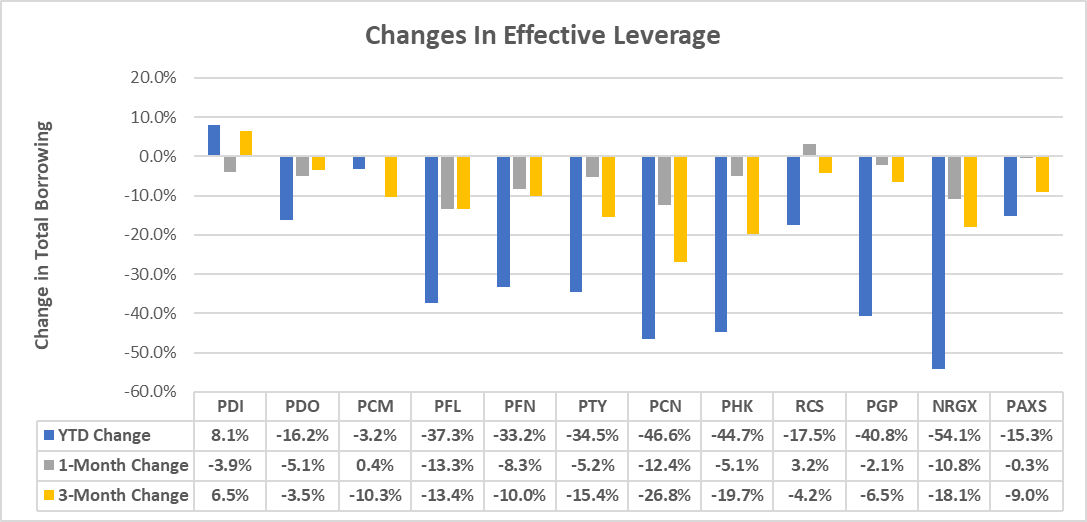

Leverage Update | Funds Continue To Shed Borrowing But Why?

{kind=link}

Alpha Gen Capital

In the last month, funds took down their leverage once again. This makes sense given PIMCOs forecast for a recession this year. They still are highly defensive though a recent video published on their blog noted how they are finding some good opportunities to allocate money. If they believe we are in a risk-off environment, it makes sense to take down leverage and reduce risk.

In the above table, you can see that PDI lowered leverage by nearly 4%, a big reversal from last month when they added big. Insiders tell me that they had several good opportunities in July to invest in cheap foreign assets and some cMBS which is why they added to borrowing.

PDI likely saw the bump while the others didn't simply due to size. PDI is large enough to gobble up a deal in size while the others typically get scraps from larger deals. Conversely, the smaller other funds (PTY, PFL, PFN, PCM) will have access to small opportunities and actually have it move the needle. That is not the case with PDI given its size. Being small and nimble is a bigger advantage over size in most cases.

Since the start of the year, you can see borrowing has come down significantly. That has reduced the average effective leverage by over 8.5% since January 1. That is a significant amount of leverage reduction.

Now, the change in the NAV has to come into play. As the NAV comes down- either due to over-distributing or due to lower asset values- all else equal, the effective leverage will rise. That is because the borrowing level stays the same (the numerator) while the total assets (denominator) falls.

So just to keep leverage flat in a declining NAV environment, the borrowing will have to be reduced. That is part of what we have seen this year as NAVs have fallen.

ycharts

Valuation Update | PIMCOs Are Still A Bit Rich In Taxable Land

Valuation, or the discount or premium to NAV, has moved materially higher in the last few months. Using PDI as a proxy, you can see that the premium has expanded from late March through mid-July. In last month's PIMCO update , we talked about the valuations being juiced materially. Look at the chart I had included in the report showing PDI's price and NAV:

cefconnect

And we concluded:

We think investors who are NOT buy-and-hold investors should think about lightening up any overweight positions and perhaps even tactically swapping out some of the PIMCO funds.

Action :

- Sell PCM, PCN, PTY, RCS

- Buy: N/A

- Consider Trimming: PDO, PDI, PHK

- Swap: PFL for PFN

- Swap: PDO for PAXS

Since then, PDI has seen its balloon deflate some. The premium, which reached almost 14%, has come back down to about 8.8%. This is much closer to our fair value estimate for the fund at 6.75%.

cefconnect

The only fund that looks semi-interesting here is PAXS, which is back to a discount at -3.3%. The discount is likely the result of the weaker ("weakest") NAV performance of the group. That is driven by the -22.9% allocation to cMBS.

{kind=link}

pimco

PDI would be a marginal buy if the shares fell another $0.30-$0.40 from here and PAXS are better buy if it falls another $0.20 or more. However, the NAV decline is a real concern and we would be cautious buying any shares of any PIMCO taxable until we see a definitive sign that they have bottomed and started to rebound. You may miss the nadir but it is worth it to avoid further NAV declines.

Concluding Thoughts

PIMCO taxables look a lot better from a valuation standpoint nearly across the board. They still look a bit overvalued in some funds (PCM, PTY, PCN, PHK, RCS) and likely should be sold. Others, PDI, PFL, PFN, PAXS look best valued here though not necessarily in the buy zone.

For me, I am sitting on the sidelines here waiting for much better valuations. NAVs are still falling and coverage/fundamentals are weak which, given the still not great valuations means I will wait and seek other opportunities.

On the muni side, I would still hold firm on the sidelines and wait until the valuation gets a bit cheaper, that incorporates a larger distribution cut. Right now, it appears that large cuts could be made nearly across the board. UNIIs are well negative and falling. Coverage remains well below 100%. We could see 10%-20%+ cuts in the next few months which would make these funds much cheaper.

For further details see:

PIMCO August 2023 Report | Valuations Come Back Down But Still Not Compelling