PAXS - PIMCO CEF Update: Coverage Continues To Fall Plus Recapping Our Strategy

Summary

- We provide a November update for the PIMCO CEF taxable suite.

- Taxable PIMCO CEFs continued to deleverage in November, bringing the average leverage level of the suite to its lowest in over a year.

- Distribution coverage also continued to fall at a pace faster than can be explained by deleveraging and rising leverage costs.

- CEFs using ARPS for leverage are becoming increasingly less competitive versus their non-ARPS counterparts.

- Finally, we highlight the key components of our allocation strategy in the suite.

This article was first released to Systematic Income subscribers and free trials on Dec. 26 .

In this article, we provide an update on the PIMCO CEF suite. Specifically, we discuss the changes in leverage and distribution coverage for the month of November. We also discuss the significant headwind faced by a number of taxable funds due to the high cost of leverage sourced by auction-rate preferreds or APRS. Finally, we comment on recent special distributions and highlight the main concepts of our allocation strategy within the PIMCO taxable suite this year.

Leverage Update

Taxable borrowings fell sharply in November.

Systematic Income

The cuts ranged from 7-13% across the suite.

Systematic Income

What was interesting is that, unlike in prior instances, these cuts did not happen in a month where NAVs fell significantly - a common pattern that indicates a forced deleveraging. Rather, NAVs held up well in November, meaning the funds cut borrowings more likely because of a bearish market call. So far, it's working out well as markets have been weak in December. The chart below shows that the average taxable CEF leverage level is the lowest it has been over the past year.

Systematic Income

Over the past 12 months taxable funds have shed a significant level of borrowings, ranging from 20% to 40%. This, along with a sharp rise in leverage costs, have reduced the amount of net income the funds are generating, all else equal.

Systematic Income

Coverage Update

Taxable coverage continued to slide for the second month in a row.

Systematic Income CEF Tool

Only three funds continue to boast six-month rolling coverage above 100%, down from all taxable funds having >100% coverage in August.

Two things are worth saying. First, it's tempting to conclude that the recent drop in coverage is due to the large special distributions across a number of funds, however, that doesn't seem to be the reason for the drop because funds without specials this year have also seen large drops in coverage and because coverage appears to be calculated independently of special distributions.

Second, it's also tempting to say that the large and continued deleveraging this year across the suite and the sharp rise in leverage costs that we have been highlighting repeatedly are finally coming home to roost. However, the sharp falloff in coverage (e.g. [[PDI]] from 146% to 96% over 2 months) is too sudden to be explained by these two factors. In our view, the trendline of net income and, hence, coverage is certainly moving lower however there is simply too much noise in the monthly figures to say with certainty where coverage really is at any given time.

ARPS Becoming A Significant Tailwind

As many PIMCO CEF investors know, the funds use a number of different leverage instruments. In this section we focus specifically on auction-rate preferreds or ARPS.

Investors who need a refresher on ARPS can have a look at our earlier article . In short, ARPS are used by a small number of funds, including PIMCO CEFs, as leverage instruments - akin to repo or credit facilities.

The chart below shows how the various CEFs break down with respect to their leverage instruments. In the taxable suite we see that most funds rely primarily on repo (green bars) however a number of funds such as [[PFL]], [[PFN]] and [[PTY]] use a sizable amount of ARPS (red bars).

Systematic Income CEF Tool

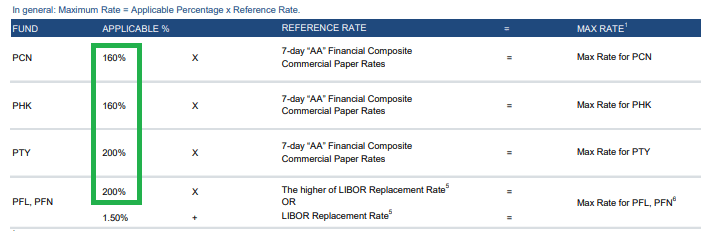

When ARPS fail at auction (which has been the case since the GFC) they are automatically reset to a Max rate . These rates are calculated for the PIMCO funds as a multiplier x a short-term rate, usually a commercial paper rate. The interest rate on many of these has been floored near zero in 2021 for the simple reason that 1.5x or 2x a very low number is still a low number. This allowed the funds to source leverage at unusually low levels within the CEF space. The table below shows the ARPS formulas.

{kind=link}

Obviously, this has now reversed - as short-term rates are moving higher these ARPS are becoming a real liability (pardon the accounting pun). For instance, [[PTY]] (which has 20% of it borrowings in preferreds) pays 2 x AA commercial paper on its ARPS so it paid a rate of near zero in 2021 while a fund like PDI had to pay around 1% on all of its borrowings (which were exclusively in repo).

However, second-grade algebra tells us that if we compare the PTY ARPS interest rate of 2 x short-term rate to the cost of repo which is very roughly short-term rate + 0.75% , at some point the multiplier effect will start to make a serious impact on the interest rate and the ARPS interest rate will be much more expensive than the repo and that's happening right now.

For example, if, as the Fed thinks, short-term rates will top out around 5%, PTY will be paying 10% on its ARPS while PDI will be paying around 6% on all of its financing - a big advantage for PDI. Granted, ARPS are a minority of PTY liabilities but it's clear that while funds like PTY enjoyed a lower leverage cost than non-ARPS funds (like PDI, [[PCM]], [[PDO]], [[PAXS]], [[RCS]], [[PGP]]) their leverage cost will now exceed that of non-ARPS funds. The table below from December shows that these funds are already seeing very high leverage costs on their ARPS.

PIMCO

What this means in practice is that a fund like PTY with a leverage cost of around 8% on its ARPS and a fee on managed assets of 0.65% has to earn more than 8.65% on the assets financed by the ARPS in order to pass on any income to investors. With the High-Yield Corporate Bond Index trading now at an 8.5% yield that's not a straight-forward proposition. Granted, the amount of assets financed by the ARPS is not huge at less than 10% for these funds, however, it is still the case that little if any income from these assets is filtering through to end investors and this number will only continue to fall in the near term as the Fed completes its hiking cycle.

Another consequence of this dynamic is that PIMCO taxable CEFs with ARPS (i.e. PTY, [[PCN]], [[PHK]], PFL, PFN) should be getting progressively cheaper (i.e. trading at a lower premium / wider discount) relative to PIMCO CEFs without ARPS. And this is what we see in the chart below. These funds started the year trading at an average valuation 6% higher than funds without ARPS but are now trading at a valuation 2% lower than funds without ARPS (e.g. PDO, PDI, PCM, RCS, PGP). We expect this trend to continue next year.

Systematic Income

A Comment On Special Distributions

PIMCO CEFs followed up their December regular distribution announcements with year-end special distributions. This year 6 funds had specials - 5 taxable (PCN, PTY, PAXS, PDI, PDO) and one tax-exempt ( PCQ ). Interestingly, all the taxable funds sourced the special from income while PCQ sourced it from capital gains. The PCQ special was small - about 30% of its regular monthly distribution which makes sense as we wouldn't expect much capital gains this year. The taxable specials ranged from 1.3 to 7.5x of regular distributions (and 1.3% and 6.6% of NAV) with PDO at the high end of this.

Overall, there were few surprises. As we discussed a number of times in these Monthlies, PDO and PAXS were expected to deliver large specials due to their relatively low distribution rates (till recently) and they delivered. We also said that the funds delivering large specials would likely catch a bid so it made sense for tactical investors to overweight these two funds. As it happened, PAXS did not react a whole lot but PDO jumped, trading up as high as a 6% premium. This made it very expensive in our view, particularly relative to PAXS and we thought this was unsustainable. Sure enough the fund's valuation deflated quickly and moved to a more reasonable 1.5% discount.

Systematic Income

Overall, one of the key themes in the taxable suite is that the more recently launched pair of PDO and PAXS has become less cheap relative to the rest of the taxable suite. The following chart shows that the average of PDO and PAXS valuations is only about 9% below the average of the rest of the PIMCO taxable CEF suite which is at the tighter end of its range since the launch of PDO (PAXS was launched in 2022). This ties into our allocation strategy we discuss below.

Systematic Income

Current valuations of PDO and PAXS are unusually close to a number of funds like PFN and PFL and these funds can be attractive rotation options, particularly once they address their ARPS issues. We wouldn't be surprised if PIMCO tenders for the APRS just like Virtus did with their funds this year which also held uneconomic ARPS.

Systematic Income

Review Of Our Allocation Strategy

As the year comes to a close, it's useful to review the allocation strategy employed within the PIMCO taxable suite this year.

This strategy consisted of a number of premises:

- Outside of the more idiosyncratic funds like RCS and PGP, the rest of the PIMCO taxable CEF suite has a broadly similar multi-sector credit allocation

- In an environment of high underlying yields, valuation tends to matter more than the level of management fees, meaning funds like PDO/PAXS which have tended to trade at significantly wider discounts but that also have relatively high management fees tend to be more attractive in the suite

- NAV distribution rates will tend to converge over time. Funds that underdistribute such as the pair of PDO/PAXS will tend to boast lower NAV distribution rates and, hence, feature relatively wide discounts. However, since their income generating power is as high as their counterparts in the taxable suite, they will likely either raise their distributions and/or deliver large specials, which will also tend to boost their valuations

- In an environment of rising short-term rates, CEFs using ARPS for their leverage will see an increasingly high cost of leverage relative to funds that don't use ARPS and their net income will fall faster than funds not using ARPS

- Relative changes in valuation within the suite frequently allows investors to rotate among very similar funds such as PDO and PAXS, generating additional alpha

- Allocating to funds within the taxable suite is best done in a countercyclical manner - as underlying yields widen (i.e. as NAV falls) and as discounts widen it makes sense to add exposure by rotating capital from drier-capital securities (i.e. lower-beta open-end funds, shorter-maturity bonds etc.) into the PIMCO CEFs and vice-versa

This strategy worked pretty well this year. PDO and PAXS spent most of the year trading at significantly cheaper valuations relative to the rest of the suite, likely due to their underdistribution. Both funds raised their regular distributions and delivered large specials, resulting in significant valuation gains for both funds and delivering a double-win for investors. Within the PIMCO taxable suite, we allocated primarily to these two funds in our Income Portfolios in anticipation of these events which have delivered as we hoped.

Frequent changes in relative valuation in this pair also offered investors additional opportunities to generate alpha. We made multiple rotations between the two funds this year.

And finally, as broader markets gyrated, the taxable suite offered a more or less attractive place to put capital to work. We downsized our allocation to the pair recently in favor of other securities which have held up better in this most recent period of weakness.

Currently, the pair offers a less compelling opportunity within the suite as the valuation differential chart above showed and we consider the two funds fairly priced. Moreover, the broader PIMCO taxable suite is not as compelling as it was earlier in the year as asset yields have moved lower in the last couple of months due to the drop in Treasury yields and stable credit spreads. If we see high-yield corporate bond yields move back up to a 9.5% level from the current 8.5% we would be tempted to increase our allocation to the PIMCO taxable suite, particularly if discounts widen further out. At the moment, we are keeping only a modest allocation to it.

For further details see:

PIMCO CEF Update: Coverage Continues To Fall Plus Recapping Our Strategy