PTY - PIMCO CEF Update: SEC Goes After PIMCO For Paired Swaps

2023-07-27 10:53:42 ET

Summary

- We provide a June update for the PIMCO CEF taxable suite.

- The SEC fined PIMCO $6.5m for inadequate disclosure of its paired swap strategy.

- Coverage turned back down for taxable funds to close out the fiscal year.

- Most taxable funds continued to deleverage in light of high leverage costs and rich credit valuations.

In this article, we provide an update on the PIMCO CEF suite. Specifically, we discuss the changes in leverage and distribution coverage for the month of June. We also highlight PIMCO's recent settlement with the SEC due to an inadequate disclosure of its paired swap strategy.

Coverage Update

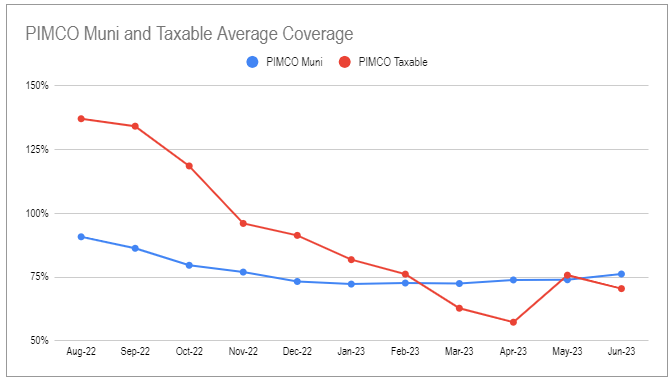

Taxable six-month rolling coverage fell back after a strong recovery in May. Tax-exempt coverage gained slightly and has been stable after cuts in the Muni funds earlier this year.

{kind=link}

The June sum of total net income across taxable funds fell back to the third lowest level in the past year after a sharp rise in May.

Systematic Income CEF Tool

As we discussed in the last month's update, the sharp jump in net income and coverage was surprising to see. In this sense, a fall back to the previous trend line was not unexpected.

With the fiscal year now over, we can check how coverage looks for the entire year. In the Muni suite, two New York funds PNF and PYN stand out as having relatively low coverage despite pretty brutal cuts earlier in the year.

Systematic Income

In the taxable suite, PAXS and PHK remain on the higher side while PTY, PDI and RCS bring up the rear.

Systematic Income

We are coming up to a 2-year anniversary of the previous cuts in the taxable suite. Interestingly, the average coverage at the time of the cuts in 3 funds (PTY, PFL, PFN) was about the same as it is now.

{kind=link}

Another interesting statistic is that we saw cuts in the taxable suite each year from 2015 to 2021. 2022 was the annus mirabilis of the taxable suite when there were no cuts for the first time in 8 years. If there are no cuts in 2023, it would likely be due to a combination of distributions already having normalized substantially over the years and due to the fact that the taxable funds hold a substantial amount of floating-rate assets. This second point is not entirely satisfying as we would see it show up in a higher coverage figure so this remains a question mark.

Systematic Income

Leverage Update

Unusually, total borrowings increased in the taxable suite. Until June, borrowings decreased nearly monotonically over the past year. It might seem odd to jack up borrowings in a period where corporate credit valuations are fairly rich.

Systematic Income

There is a simple explanation for this increase in borrowings, however, which is that nearly all the borrowings increase was due to PDI. PDI is by far the largest fund in the suite (it was a large fund at inception but grew even larger when it swallowed PCI and PKO). Outside of PDI, total borrowings would have continued to slide in June.

Systematic Income

The following chart shows the changes in borrowings in percentage terms highlighting that, on average, taxable funds continued to deleverage.

Systematic Income

This deleveraging trend makes a lot of sense in the context of two key dynamics: high and still increasing leverage costs and fairly rich valuations across the credit market.

Systematic Income

The recent increase in borrowings pushed up the leverage of PDI back to a mid-40 level.

Systematic Income

It now rejoins the highest-leverage funds like PCM, PDO and PAXS.

Systematic Income

Market Themes

The SEC has settled with PIMCO CEF PGP in an amount of $6.5m for the inadequate disclosure of the so-called "paired swaps" the fund held between 2014 and 2016. This is equivalent to about 2 weeks' worth of management fees collected on the taxable CEFs so it's somewhat of a slap on the wrist.

The order provides a good summary of the mechanics and reasoning behind paired swaps. We discussed these mechanics in a 2020 article for those who want the background. Basically, in a paired swap, PIMCO initiates two nearly identical swaps: a spot-starting swap and a forward-starting swap. A spot-starting swap is just a typical swap where fixed vs. floating cashflows are exchanged. A forward-starting swap is one that starts in the future - it has all the risk of a spot-starting swap but not the cashflows.

In a normal upward-sloping yield curve environment PIMCO would receive fixed / pay floating on the spot-starting swap and do the opposite on the forward-starting swap. Because in an upward sloping yield curve fixed cashflows were higher than floating-rate cashflows at the beginning of the swap, the spot-starting swap generated positive cashflow to PIMCO. The forward-starting swap offset the risk of the spot starting swap but without having negative offsetting cashflows.

In short, PIMCO achieved a zero risk position with positive cashflows. Obviously, this isn't manna from heaven and the forward-starting swap valuation fell by the amount of the positive cashflows that the spot-starting swap generated for PIMCO.

Why go through such a complicated strategy? The reason is that simply paying distributions out of the NAV shows up as ROC and ROC is viewed negatively by CEF investors. Paired swaps are basically non-ROC ROC i.e. the payments are unearned and come out of the NAV just like normal ROC but they don't show up as ROC in the accounting.

However the downside of this non-ROC ROC is that it's taxed as ordinary income whereas ROC is not taxed at all on day-1 (it reduces the cost basis so could be taxed as LT capital gains later on). This is not an issue for tax-sheltered accounts but is clearly problematic for taxable ones because it requires investors to pay, typically, a high level of tax on their own capital just so PIMCO doesn't have to show ROC.

Overall, this is more for historic interest - we don't see sizable forward swaps in the shareholder reports anymore so it seems that PIMCO are not using the strategy a whole lot right now.

Stance and Takeaways

We don't have any exposure to PIMCO CEFs at the moment. We rotated most of the exposure out at the end of last year when valuations zoomed higher. Most recently, we moved a small amount of residual exposure in PAXS to the new PIMCO ETF Multisector Bond Active Exchange-Traded Fund ( PYLD ) which should be much more resilient in a sell-off. Given a tight level of credit spreads and expensive CEF valuations, we are happy to dial down our risk exposure without totally leaving the income market.

Systematic Income

For further details see:

PIMCO CEF Update: SEC Goes After PIMCO For Paired Swaps