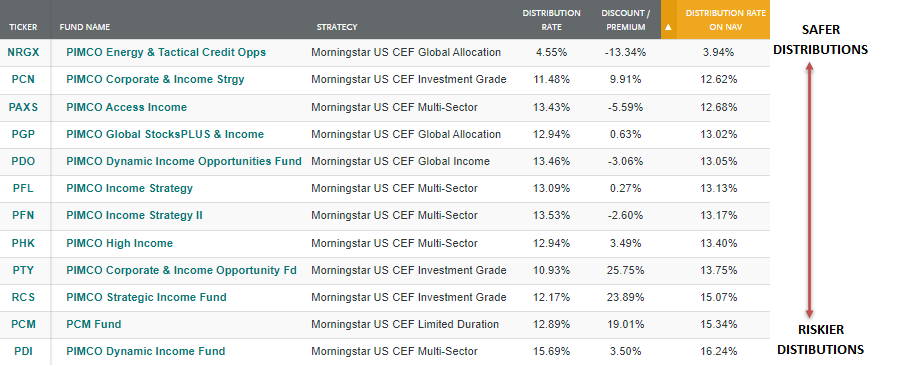

PAXS - PIMCO Update | Oct 2023 | Valuations Take A Tumble

2023-11-13 08:00:00 ET

Summary

- PIMCO taxable CEFs previously had high valuations, but now discounts are appearing across most funds.

- Leverage changes have been negative, with most funds reducing leverage by 20% to 40%+.

- My inclination is to favor PHK and PDI here, given the NAV track records and sector allocations. I'm not wild on PDO and PAXS' higher exposure to CMBS.

- PIMCO Energy and Tactical Credit remains my top buy at the moment as the fund is going through a special situation of a strategy shift.

- PCN fund looks interesting for the first time in years, but potential distribution cuts need to be navigated.

We noted just two months ago how valuations for PIMCO taxable CEFs were a bit excessive " With Valuations Moving Higher The Funds Are Not Compelling ." You can clearly see that in the chart of PIMCO Dynamic Income (PDI) below. Two months ago, the premium was almost 15%.

cefconnect

At that point, I said it was a good idea to take some off the table.

We think investors who are NOT buy-and-hold investors should think about lightening up any overweight positions and perhaps even tactically swapping out some of the PIMCO funds.

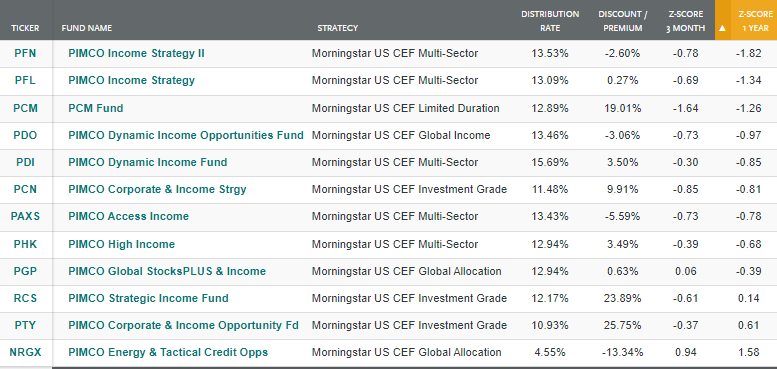

Today, the valuation story is very different with discounts materializing across most of the funds- something we could say about any taxable PIMCO fund two months ago. Eight funds of the 12 on the taxable side are now at a discount.

{kind=link}

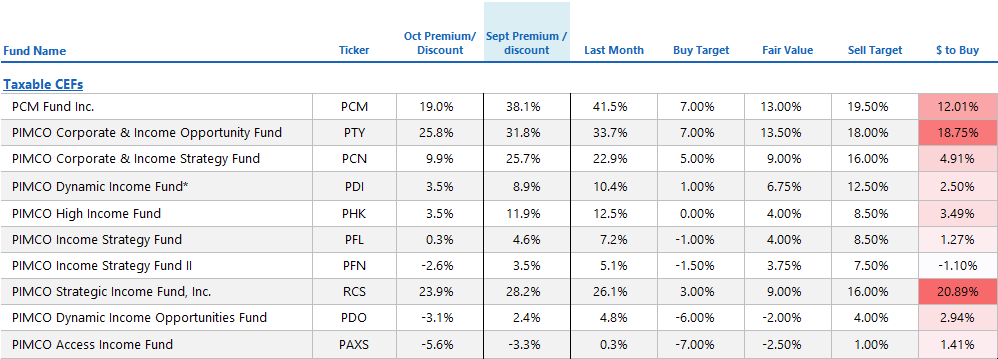

Even typically high premium funds like PCM Fund ( PCM ), PIMCO Corporate & Income Strategy ( PCN ), and PIMCO Corporate and Income Opportunity ( PTY ) have come way down in valuation and have since rebounded some.

- PCN: 29% premium to 2% to 10%

- PTY: 34% premium to 20% to 25%

- PCM: 47% premium to 21% to 19%

- PFN: 2% premium to -6% to -2%.

For PCN, that one looked interesting for the first time in many years but one has to navigate a potential distribution cut.

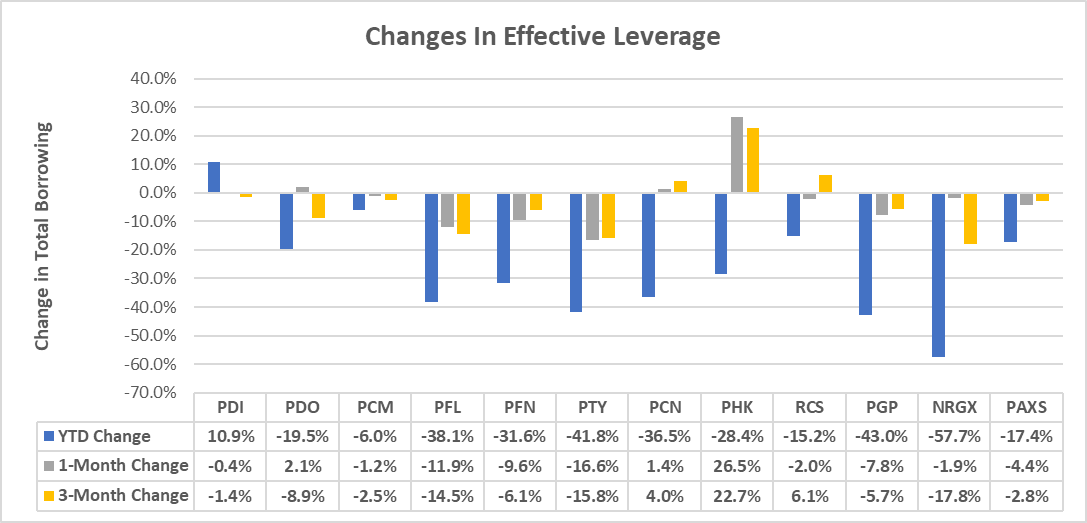

Leverage Changes:

In the last month, leverage change was not broad-based as some funds added while some funds reduced. Overall, YTD changes in leverage are decidedly negative with most funds reducing by 20% to 40%+. This is in line with PIMCO's outlook calling for increased volatility and a struggle for risk assets.

{kind=link}

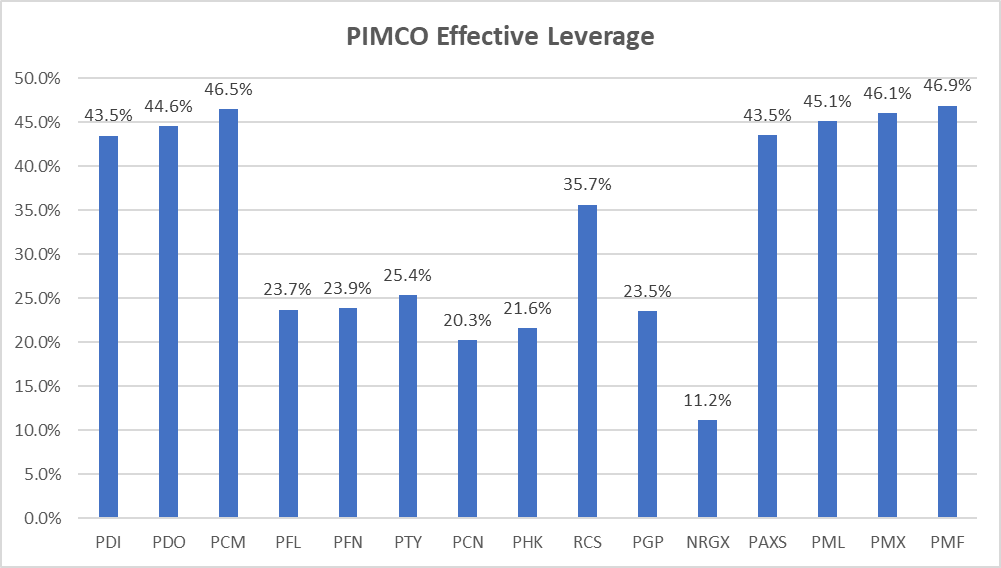

Effective leverage remains high across normal taxable funds like PDI (43.5%), PDO (44.6%), and PCM (46.5%).

{kind=link}

Those effective rates are nearing the upper end of the range for the last three years for those respective funds. PAXS is nearing the upper end of their since inception range. PDI is slightly lower at 43.5% compared to a three-year average of 45.2%.

We are starting to see some improvement in taxable NAVs which should help reduce overall leverage levels (if management chooses to). In the chart below, you can see that over the last three months, NAVs have continued to bleed lower as interest rates rose, and the funds continue to overdistribute.

ycharts

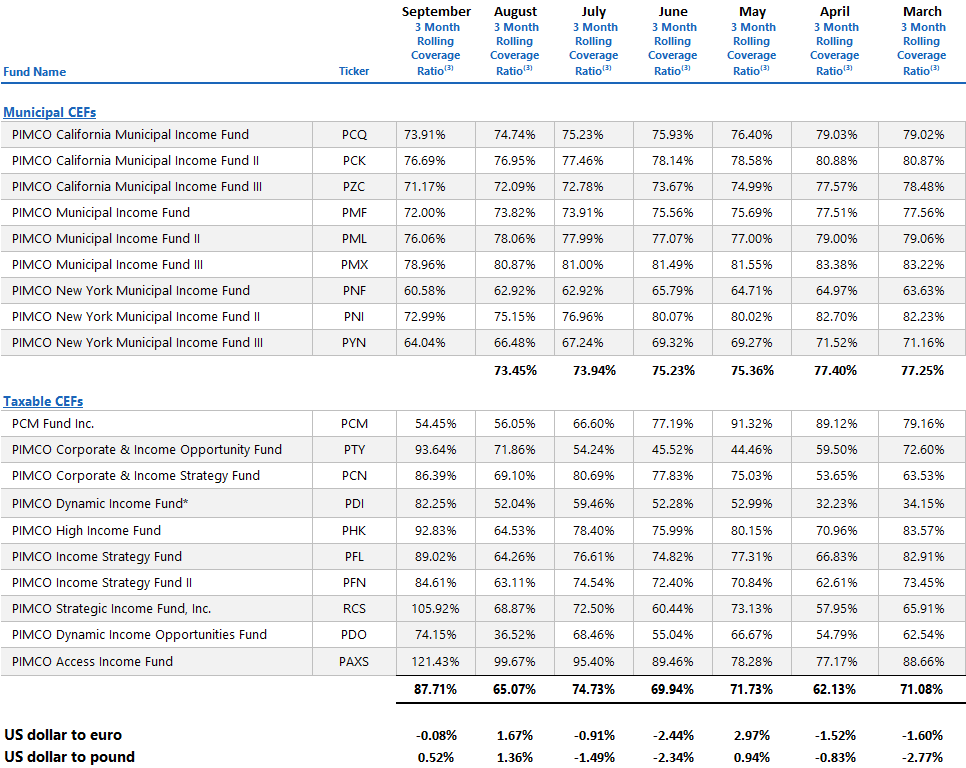

Coverage Improvement With Poor June Roll-Off

{kind=link}

Above are the coverage numbers through September. We saw significant improvement in the taxable, with the average moving from 65% to 87%. It remains to be seen what the driver of that improvement was other than the roll off of June's bad numbers.

The dollar was essentially flat against the euro and up a bit against the pound, but didn't contribute all that much to coverage changes.

ycharts

I still think the higher yield on NAV funds will eventually have to cut the distributions. The downward trend in the NAVs will eventually get the better of the funds and cause leverage to reduce, further compounding the under-earning.

PDI currently has the highest distribution rate on NAV among the funds at 16.24%. That is a steep bogey to hit each month unless you're in some real junky stuff - which looking at the latest holdings is not the case.

Even a portfolio of B-rated debt would yield only 9.5%. Levered up 50%, and you're at 14.25% before any expenses.

{kind=link}

Valuations Are Cheap But Recovering

In the last week, NAVs have started to recover a bit, which is leading to a sharp recovery in price. Valuations were dirt cheap. I didn't make any additional purchases of the PIMCO funds outside of PHK and PCN.

PIMCO High Income (PHK) remains a decent buy here at a 3-4% premium to NAV. The yield is 12.74% and the fund remains one of the best performers on NAV.

The table below shows total return NAVs with a split between PHK, PDI, and PFN while the newer funds, PAXS and PDO remain laggards.

ycharts

The cheapest funds are now more abundant on the taxable side. The cheapest fund and the only one below the buy target level (as of this writing) is PIMCO Income Strategy II ( PFN ) . However, several other funds are extremely close including:

- PIMCO Income Strategy ( PFL )

- PIMCO Access Income ( PAXS )

- PIMCO Dynamic Inc ( PDI )

- PIMCO Dynamic Inc Opp ( PDO )

{kind=link}

My inclination is to favor PHK and PDI here, given the NAV track records and sector allocations. I'm not wild about PDO and PAXS' higher exposure to CMBS, though I realize these securities are extremely cheap and that PIMCO is looking long-term. PAXS is actually one of my largest holdings, so I continue to maintain that position.

PIMCO Energy and Tactical Credit (NRGX) remains my top buy at the moment as the fund is going through a special situation of a strategy shift. They are moving away from equities/MLPs towards a traditional multisector approach that looks more like PDI, PDO, and PAXS. That will take time however and in the interim, you may have more volatility than you like.

Here is a summary of what is happening:

- Renamed to PIMCO Dynamic Income Strategy

- Ticker changed to PDX

- Reduce fee to 1.25% from 1.35%

- New investment objectives will be to seek current income as a primary objective and capital appreciation as a secondary objective.

- The Fund will also rescind its policy to invest, under normal circumstances, at least 80% of its net assets in investments linked to the energy sector. The Fund will, however, continue to invest at least 25% of its total assets in the energy industry.

- All of the changes described above will be effective on November 21, 2023

We think the fund will then be in a position to shift from a quarterly to monthly distribution (which investors love and reward, all else being equal, with a higher valuation) and a higher distribution/yield.

With a -14.5% discount, the fund is trading very cheap based on the assumption of those changes. If the fund looks more like PDI or PDO, then we should expect that discount to tighten significantly (but probably not to where PDI trades).

In addition, this will be a good barometer to where PIMCO thinks a sustainable distribution is and will be a tell for where they POTENTIALLY could adjust other, similar funds down the road.

For further details see:

PIMCO Update | Oct 2023 | Valuations Take A Tumble