PXD - Pioneer Natural Resources: Solid Value At The Current Price

2023-07-19 04:26:52 ET

Summary

- Commodity prices, including oil, have seen a significant pullback after trading at near-decade highs for much of 2022 due to rising rates and slow economic growth.

- The article provides an analysis of energy holdings, reserves, and potential future production numbers, along with different probability outcomes for oil and natural gas prices.

- It also discusses the capital expenditure plan and its likely impact on dividends, as well as a cash flow analysis and a review of the dividend payout ratio.

Getting premium companies at a discount is hard. While mediocre and poor run corporations frequently struggle, investors often seldom see sell-offs in well-run companies that are in appealing sectors.

Today, there has finally been a pullback in most commodity prices, including in the energy market. While oil traded at near decade highs for much of the early part of 2022, rising rates and slowing economic growth caused West Texas Intermediate and crude oil prices to fall significantly over the last year.

One of the better run and larger independent oil and gas producers is Pioneer Natural Resources ( PXD ). This company operates almost exclusively in the Permian Basin in the Southwestern part of the United States. Pioneer's market cap is $49.62 billion.

Oil prices are down nearly 30% since peaking in the middle of last year. Not surprisingly, Pioneer Natural Resources has also sold off since brent crude oil and WTI prices peaked in the middle of 2022.

Today, Pioneer Natural Resources is a buy. The company is also one of the better run independent oil and gas producers, and the long-term outlook for oil prices remains bullish. Pioneer gets nearly two thirds of the company's revenues from oil production, and the company has proven the business model even with a weak natural gas market. Management is committed to aggressively returning cash to shareholders and the company's strong balance sheet gives the leaders of this energy producer a lot of options to maximize shareholder returns. PXD stock looks undervalued at the current price using several metrics.

Pioneer Natural Resources has maintained an impressive commitment to maximizing shareholder returns with a current policy of allocating 75% of quarterly free cash flow to dividends and buybacks. While this current policy is a change from the prior policy of returning 100% of available funds to shareholders with dividend and buybacks, the previous plan was unsustainable anyways. Management also recently stated that the company's plan is to return 40% of the current market capitalization to shareholders over the next 5 years. This initiative is predicated on WTI oil prices being at $80 a barrel or higher.

{kind=link}

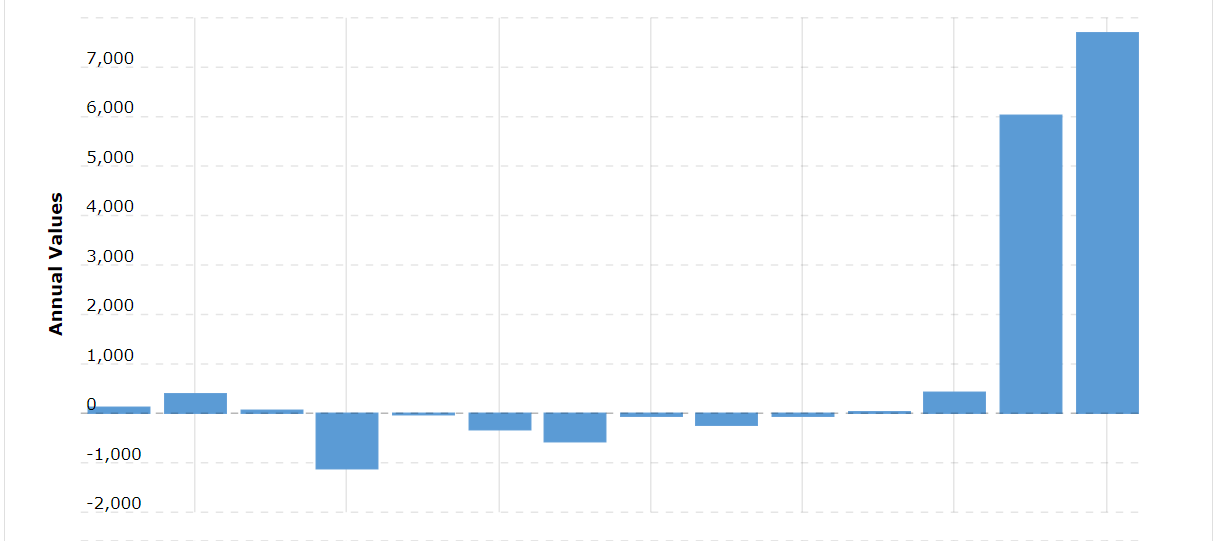

A Chart of Pioneer Natural Resources Annual Cash Flow (Macrotrends)

Pioneer Natural Resources' cash flow of the last 2 years has been impressive, and the company's balance sheet should remain strong with oil prices likely to stay over $70 a barrel for multiple reasons. The company currently has $3.2 billion in liquidity, with $1.2 billion being free cash from the first quarter and $2.2 billion in a revolving credit line. Pioneer recently announced a newly authorized $4 billion dollar share buyback plan after reporting first quarter earnings. The company also reported that current net debt is $4.7 billion. Cash flow in the first quarter was $2.2 billion, with free cash flow being $948 million.

These first quarter earnings numbers came from realized oil prices of $75.15 and a realized natural gas prices of $3.79 per thousand cubic feet. Those prices exclude the impact of hedges and derivative contracts. Management expects the capital budget for 2023 to be $5 billion, and the company is predicting free cash flow for the current year to be $9 billion. The company's 5-year dividend growth rate is 86.81%, and this energy producer's 10-year dividend growth rate is 49.79%. Even though crude oil prices have sold off over the last year from record high levels in 2022, the company's current revenues and cash flow with WTI Oil prices at nearly $76 a barrel remain strong.

Pioneer gets nearly two-thirds of the company's revenues from oil production, and most of the natural gas and natural gas liquids that are produced come from the drilling for oil. While predicting the exact price of any commodity is very difficult, there are multiple reasons to believe that oil prices will remain in a higher range for some time.

Russian oil exports remain limited , and the energy industry is also still recovering from an extended period of significant underinvestment from 2016 to 2020 when prices were often at low levels. The recent bombing of key infrastructure in the Crimea, as well as the continued counter offensive by Ukraine, continue to suggest this conflict is unlikely to end anytime soon. Upstream investments in the energy sector have also fallen from $700 billion a year in 2014, to between $370 billion to $400 billion today.

The average decline rate per year globally of oil fields is also 6%. The IAEA is forecasting global demand for oil to increase by nearly 2% this year from 2022 levels. Oil demand is supposed to continue to grow by about a half a percent a year from now until 2030. The Energy and Information Administration also recently updated the agency's forecast for crude oil prices in 2023 to $79 a barrel, which is in-line with the $80 dollar a barrel model this company's current plan for returning cash to shareholders is based on. While the North American natural gas market is expected to remain weak for some time, Pioneer is much more levered to oil production, and the company has already proven they can operate successfully even in a tough natural gas market.

Pioneer Natural Resource's share price also looks cheap using several metrics. The company currently trades at 5.86x likely EBITDA, 6.19x projected cash flow, and 10.64x Non-GAAP forward earnings. Pioneer's 5-year average valuation is 6.76x projected EBITDA, 6.55x forecasted cash flow, and 23.08x likely Non-GAAP earnings. Oil prices have held up strongly even with economic growth rates slowing and rates rising over the last year. With recent data showing inflation is moderating , the Fed is likely to slow rate increases moving forward. The forward earnings models for Pioneer look conservative.

The best run companies in the most appealing sectors don't often sell off hard. Pioneer Natural Resources fell nearly 25% from peak to trough over the last year, when oil prices sold off hard in the back half of last year. Still, energy prices have held up strong during the recent recession, and Pioneer's earnings and cash flow remain impressive as well. While projecting economic growth or commodity prices is always inherently speculative, this company looks very well positioned for the long term.

For further details see:

Pioneer Natural Resources: Solid Value At The Current Price